Mid-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

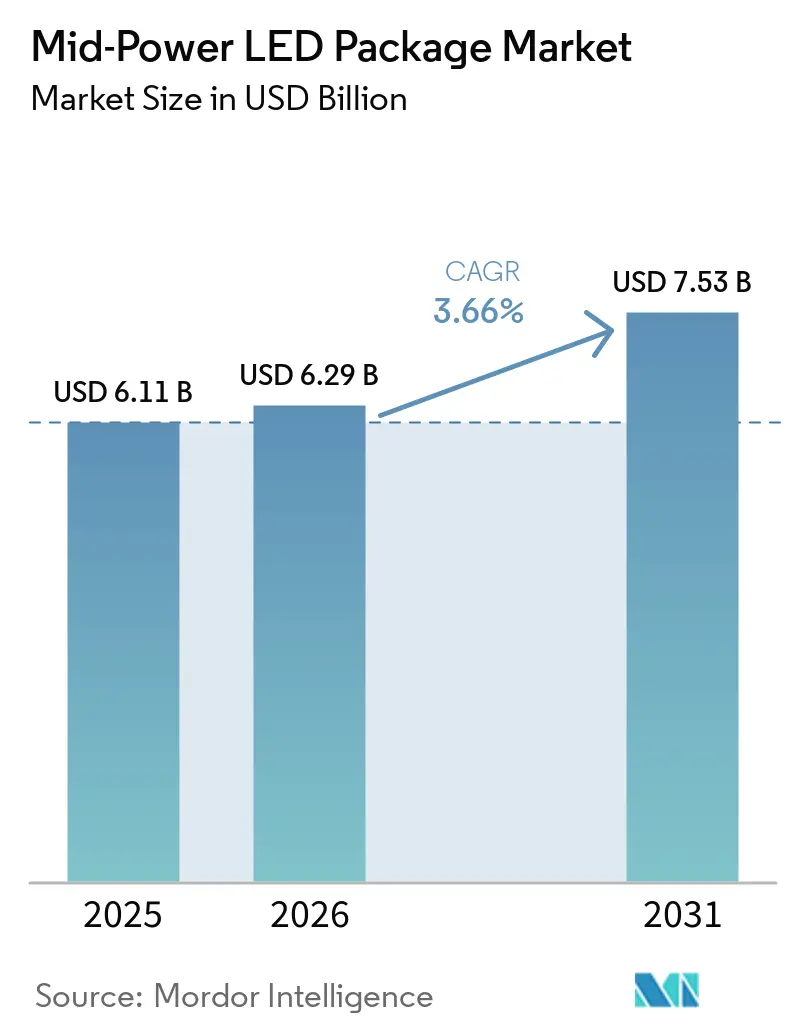

| Market Size (2026) | USD 6.29 Billion |

| Market Size (2031) | USD 7.53 Billion |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

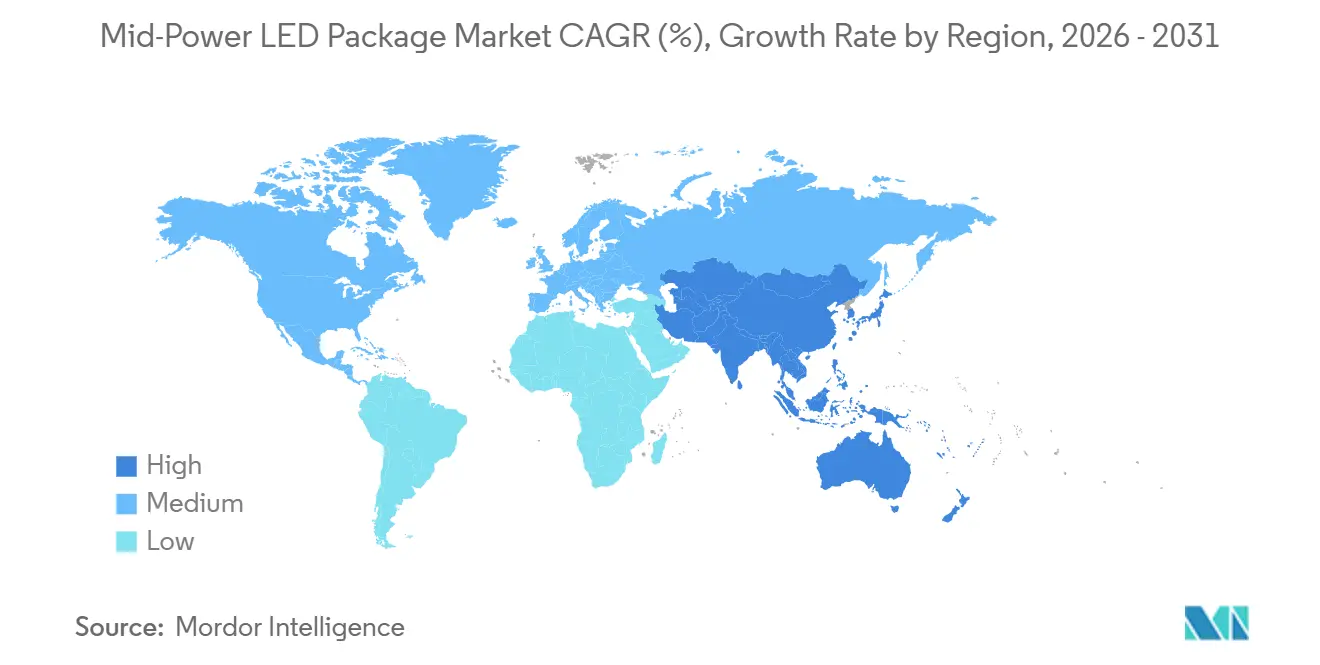

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mid-Power LED Package Market Analysis by Mordor Intelligence

The mid-power LED package market size is projected to expand from USD 6.11 billion in 2025 and USD 6.29 billion in 2026 to USD 7.53 billion by 2031, registering a CAGR of 3.66% between 2026- 2031. Sustained phase-outs of halogen and compact fluorescent lamps in North America and Europe, combined with municipal streetlight retrofits and rising MiniLED television adoption, keep shipment volumes resilient even as average selling prices stabilize after four consecutive years of erosion. Automotive adaptive driving-beam programs in Europe, North America, and China are now the principal catalyst for premium mid-power arrays, while the television supply chain is drawing incremental demand through higher local-dimming zone counts. Yttrium export licensing introduced by China in 2025 raised phosphor input costs and highlighted the risk of raw-material concentration, prompting manufacturers to qualify non-Chinese oxide sources or reformulate phosphor blends.

Key Report Takeaways

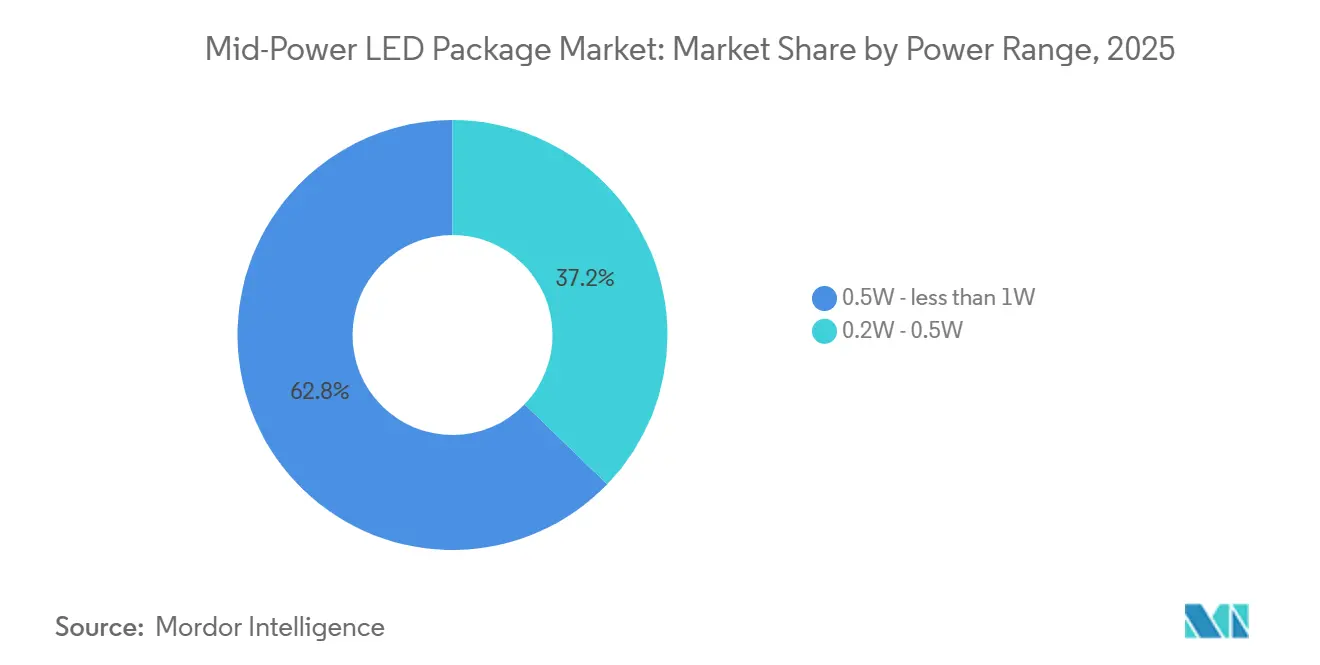

- By power range, the 0.5 W- less than 1 W class captured 62.80% of mid-power LED package market share in 2025 and is projected to grow at a 4.12% CAGR through 2031.

- By package architecture, surface-mount device formats held 73.50% revenue share in 2025, whereas chip-scale packages record the fastest expansion at a 4.23% CAGR over 2026-2031.

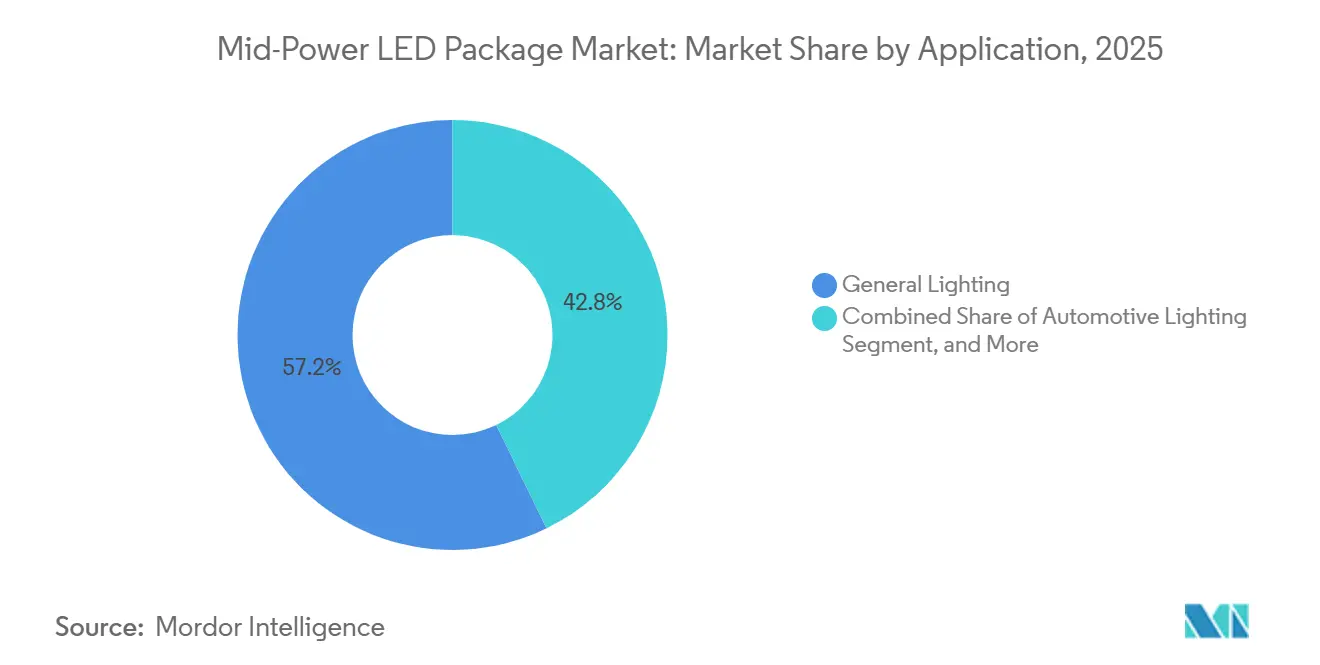

- By application, general lighting accounted for 57.20% of demand in 2025, while automotive lighting is advancing at a 4.54% CAGR through 2031.

- By geography, Asia-Pacific retained 68.90% of the mid-power LED package market share in 2025 and is projected to grow at a 5.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mid-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging Demand for Energy-Efficient General Lighting | +1.2% | Global, higher momentum in North America and Europe | Medium term (2-4 years) |

| Rapid Expansion of Automotive LED Headlamps | +0.9% | Europe, North America, China | Medium term (2-4 years) |

| MiniLED Adoption in TVs Boosting Mid-Power Backlights | +0.8% | Asia-Pacific core, spillover worldwide | Short term (≤ 2 years) |

| Cost Declines From Flip-Chip and CSP Manufacturing | +0.6% | Global, fabrication centered in Asia-Pacific | Long term (≥ 4 years) |

| Government Phasing-Out of Halogen Lamps | +0.5% | Europe, North America, selected Asia-Pacific, and South America markets | Short term (≤ 2 years) |

| Growing Smart-City Streetlighting Projects | +0.4% | India, China, Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Energy-Efficient General Lighting

LED technology supplied a significant share of China’s lamp stock in 2025, and Canada’s nationwide ban on mercury-based compact fluorescent lamps, which began in January 2026, is accelerating a similar transition across North America. The U.S. Department of Energy standard requiring 120 lumens-per-watt efficacy for general service lamps by July 2028 further compresses the viable window for halogen products. Roughly 30% of the global residential base still needs to convert, and another 15% of first-generation LEDs installed a decade ago will enter the replacement cycle, supplying a multibillion-unit addressable pool for cost-efficient mid-power packages. These lamps favor 2835 and 3030 surface-mount configurations that integrate seamlessly with legacy printed-circuit manufacturing lines. Government rebate programs and electric-utility incentives continue to steer procurement toward ENERGY STAR-qualified devices, reinforcing demand for packages with proven lumen-maintenance credentials and solidifying mid-power incumbency in volume A-lamp and linear applications.

Rapid Expansion of Automotive LED Headlamps

UN ECE R149 enforcement and FMVSS 108 adoption unlocked legal pathways for adaptive driving-beam headlamps across major automotive regions in 2025. Entry variants integrate 24-48 controllable pixels, whereas flagship trims exceed 100 pixels, dictating tighter forward-voltage and chromaticity bins and driving volumes for high-luminance mid-power arrays. Electric vehicle makers prioritize signature lighting for brand identity and efficiency, using mid-power matrix systems to display welcome animations and lane guides without excessive thermal load. Qualification cycles in automotive-grade 0 temperature ranges validate package reliability at junction temperatures near 105 °C, reinforcing the preference for ceramic-based mid-power dies. Tier-one suppliers such as ams OSRAM leverage established AEC-Q102 credentials to command price premiums while maintaining supply security for original equipment manufacturers looking to scale pixel densities cost-effectively.

MiniLED Adoption in TVs Boosting Mid-Power Backlights

MiniLED television panels exceeded 13 million units in 2025 as panel makers BOE, CSOT, and HKC ramped up capacity. Each 65-inch MiniLED set incorporates between 15 000 and 25 000 mid-power dies, translating panel volume gains directly into package consumption. Mid-power chips in 2835 and chip-scale footprints deliver the flux density and board-level reliability required for 10 000 zone local dimming while avoiding the cost penalties associated with full MicroLED emissive displays. Brands are exploiting MiniLED backlights to bridge high dynamic-range performance gaps versus OLEDs at mainstream price points, bolstering the mid-power LED package market through 2027. Rising competition among television makers nonetheless places continual pressure on per-lumen cost, making continued package innovation essential.

Cost Declines from Flip-Chip and CSP Manufacturing

Flip-chip and chip-scale package evolution removes wire bonds, trims thermal resistance by up to 60%, and eliminates package substrates, cutting material overhead while enabling higher current densities. Yield management remains the critical gating factor, as sub-99% die-bonding accuracy negates the manufacturing cost benefit of substrate removal. Equipment vendors are delivering advanced void-detection and reflow-profiling systems that keep void ratios below 5%, a prerequisite for automotive qualification. As yields rise, CSP’s footprint reduction enables higher pixel density, allowing mid-power arrays to enter design territory once reserved for separate high-power devices.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Intensifying Price Competition Squeezing Margins | -0.8% | Global, highest pressure in Asia-Pacific | Short term (≤ 2 years) |

| Thermal Management Limits for Higher Watt Density | -0.5% | Global, affecting high-power and dense arrays | Medium term (2-4 years) |

| Supply Chain Volatility of Key Phosphor Materials | -0.4% | Global, dependence on Chinese yttrium refining | Medium term (2-4 years) |

| Regulatory Push Toward Chip-on-Board Alternatives | -0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Competition Squeezing Margins

In January 2026, Chinese LED packaging companies, including MLS and Kinglight, increased quoted prices by 5–10%. This adjustment followed several years of sustained price declines that significantly compressed profitability for many mid-sized firms. The price increase is primarily due to rising input costs for gold, silver, and copper, which account for a substantial portion of overall packaging expenses. However, the sustainability of these price increases remains uncertain due to persistent oversupply in standard 2835 LED packages and the low switching barriers for customers, which limit pricing power. As a result, companies that are unable to balance rising costs through product differentiation are either exiting the market or pursuing consolidation strategies such as mergers and acquisitions. At the same time, surviving players are shifting their focus toward higher-value applications, including automotive lighting, horticulture, and MiniLED backlighting. These segments impose stricter performance requirements, enabling more stable pricing and longer-term supply agreements.

Thermal Management Limits for Higher Watt Density

At current densities above 200 A cm⁻², a standard mid-power package channels heat flux exceeding 12 000 W m⁻², a level that pushes junction temperature beyond the 85 °C sweet spot where luminous efficacy starts falling 4.2% per 10 °C rise.[1]Yongjun Huo et al., “Emerging Advanced Electronic Packaging Materials for Thermal Management in Power Electronics,” advancedscience.com Surface-mount packages on FR-4 boards exhibit two-to-three times higher thermal resistance than chip-on-board LEDs mounted on metal-core substrates, explaining their limited presence in stadium floodlights and high-bay fixtures. Flip-chip CSP variants alleviate some thermal burden, but they require near-perfect solder coverage to avoid void-induced hotspots, which drive up inspection and rework costs. Development efforts incorporating silicon-nitride ceramics or glass-based redistribution layers promise long-term relief, but commercialization timelines stretch beyond 2027, ensuring that heat dissipation will remain a ceiling on mid-power die current and lumen output in the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Mid-Range Packages Balance Output and Cost

The 0.5 W- less than 1 W band accounted for 62.80% of mid-power LED package market share in 2025, and its 4.12% forecast CAGR underlines sustained leadership in general lighting retrofits and emerging automotive matrix arrays. This power class aligns with driver-integrated circuit constraints, spreads thermal load across a manageable die area, and maintains compelling cost-per-lumen ratios that preserve vendor margin despite commodity pricing. Entry-level adaptive driving-beam modules, now projected to increase in 2026, predominantly specify 0.5 W-range devices that achieve pixel counts above 48 without exacerbating junction temperature, reinforcing the segment’s relevance in vehicle headlamps. In contrast, the 0.2 W-0.5 W segment serves indicators and wearables but faces substitution by smaller chip-scale packages offering similar flux within reduced footprints, restricting its growth pace.

Automotive lighting’s stringent forward-voltage and chromaticity binning tolerances are pushing mid-range packages toward finer electrical screening and narrower hue dispersion, with premium models demanding bins of ±0.1 V and two-to-three MacAdam steps. Thermal upgrades such as direct copper bonding and low-void SAC305 soldering uphold L₇₀ life beyond 50 000 h under accelerated-aging protocols, meeting original equipment manufacturer warranty terms. As MiniLED televisions penetrate mainstream price tiers, 0.5 W devices are also appearing in high-end backlights, balancing flux, efficiency, and pitch. The mid-range thus continues to anchor the mid-power LED package market size expansion while holding off encroachment from both lower-power CSPs and higher-power chip-on-board alternatives.

By Package Architecture: Surface-Mount Dominance Faces CSP Inroads

Surface-mount devices accounted for 73.50% of revenue in 2025, driven by mature 2835 and 3030 platforms that integrate seamlessly with standard pick-and-place equipment and offer abundant second-source options to luminaire manufacturers. Commodity troffers, tubes, and low-cost bulbs consistently favor surface-mount footprints because driver circuits and optics have been standardized around them for more than a decade. However, chip-scale packages are advancing at a 4.23% CAGR from 2026-2031, carving room in automotive, MiniLED, and architectural segments where thinner form factors and tighter pixel spacing outweigh higher capital expenditure. CSP’s sub-2.5 °C W-¹ thermal resistance, demonstrated in the LUXEON HL1Z Color Line launched in 2025, enables elevated drive current without shifting the color point, a decisive benefit for dense multi-color arrays.[2]Lumileds, “LUXEON HL1Z Color Line Simplifies Multi-Color LED Application Development,” lumileds.com

Wire-bond elimination cuts mechanical failure modes, yet yield sensitivity to voids and die-placement accuracy continues to cap output in lower-margin commodity lines. As process control improves, CSP adoption will erode surface-mount share by two-to-three percentage points annually, first in automotive daytime running lights and MiniLED televisions, and later in smart residential fixtures that prize slim optical chambers. Nevertheless, backward compatibility and cost discipline ensure surface-mount devices will remain the backbone of the mid-power LED package market through the forecast window.

By Application: General Lighting Maturity, Automotive Upside

General lighting generated 57.20% of revenue in 2025 and remains a mid-power stronghold, albeit with moderating unit growth as penetration surpasses 85% in several G20 economies. Retrofit waves triggered by Canada’s CFL ban and the impending U.S. 120 lm W-¹ standard still refresh volume, but the value mix tilts toward tunable-white and connected-control fixtures whose bill of materials emphasizes drivers and sensors over discrete LED content. Conversely, automotive lighting posts a 4.54% CAGR to 2031, fueled by the rollout of adaptive driving beams and electric-vehicle styling that elevates animated headlamp and taillight elements. Mid-power arrays offer a compelling cost-performance window for 24-102-pixel modules, sidestepping the yield penalties of full MicroLED implementations without resorting to bulky, high-power chips.

Smart-city streetlighting is emerging as an adjacent engine of growth, as contracts in Hyderabad, Delhi, and West Sussex validate large-scale conversions with centralized dimming and fault detection. Mid-power 2835 and 3030 lamps achieve up to 70% energy savings versus sodium vapor and layer in a further 10-20% through adaptive control. Specialty niches such as horticultural grow lights and medical-diagnostic illumination command higher average selling prices thanks to custom spectral bins, but volumes remain modest relative to general lighting and automotive applications. Collectively, these applications preserve a balanced demand profile that underpins the mid-power LED package market size trajectory.

Geography Analysis

The Asia-Pacific accounted for 68.90% of sales in 2025 and is sustaining a 5.10% CAGR through 2031, buoyed by dense wafer-to-module ecosystems in China, Taiwan, South Korea, and Japan. China’s April 2025 export-licensing rule on yttrium triggered a significant spike in oxide prices, compelling packagers to explore alternative refining sources in the United States and Europe. South Korea is strategically expanding higher-margin substrate and camera-module lines, evidenced by LG Innotek’s 600 billion KRW (USD 409 million) Gumi project slated for completion in 2026.[3]Asia Economy, “LG Innotek Signs MOU for Gwangju Plant Expansion,” asiae.co.kr The regional cluster thus anchors both commodity and premium segments.

North America and Europe contribute lower absolute volumes yet deliver higher gross margins per lumen thanks to stringent energy codes, such as California Title 24-2025, and eco-design directives that disallow low-efficiency lamps. Domestic epitaxial capacity is thin, so most component supply remains Asia-sourced, although Cree Lighting’s contract manufacturing deal in February 2026 signals incremental onshore integration. Municipal streetlight retrofits financed through performance-based contracts continue to replace sodium lamps, adding connected-lighting provisions that favor mid-power modules with integrated surge protection.

South America, the Middle East, and Africa trail in penetration, with LED adoption under 50% in many jurisdictions. India operates a unique bulk-procurement model through Energy Efficiency Services Limited, which leases fixtures under monthly service fees, driving price sensitivity while awarding large volumes to suppliers that meet output and lifetime standards. In these emerging territories, proven 2835 packages retain dominance, and the mid-power LED package market derives incremental growth less from technological leapfrogging and more from first-time conversions and grid-reliability considerations.

Competitive Landscape

The market exhibits a moderate concentration, with the top ten vendors playing a significant role. Nichia, Samsung, ams OSRAM, Seoul Semiconductor, and Lumileds preserve leadership through proprietary phosphor formulations, tighter binning precision, and automotive certifications that command 20-40% premiums above commodity alternatives. Chinese firms such as MLS, NationStar, and Kinglight wield cost leadership by integrating epitaxial wafer output with high-throughput packaging, enabling aggressive bids in price-sensitive contracts. Strategic differentiation is shifting toward system-level offerings: Lumileds combined metasurface enhancements with established die processes in 2025, doubling on-axis candela for MicroLED prototypes without exotic tooling. [4]Lumileds, “Breakthrough MicroLED Development Delivers Improved Emission Directionality and Efficiency,” lumileds.com Ams OSRAM’s February 2026 divestiture of a non-optical sensor line freed capital to sharpen focus on digital photonics and pixelated emitter platforms, signaling a move toward integrated hardware-software ecosystems.

Mergers and long-term supply agreements typify recent moves, as seen in Seoul Semiconductor’s partnership with OMINSU Vietnam to embed SunLike spectrum die in locally branded luminaires, broadening geographic reach through technology transfer. Western lighting specialists facing supply disruptions are pivoting to contract manufacturing arrangements, reflecting the need for resilient regional footprints that hedge geopolitical risk. Going forward, competitive advantage will hinge on the ability to deliver automotive-grade reliability, integrate smart-control interfaces, and manage scarce phosphor inputs, rather than solely on lumen-per-dollar metrics.

Mid-Power LED Package Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd.

OSRAM GmbH

Seoul Semiconductor Co., Ltd.

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: LG Innotek signed a 600 billion KRW (USD 409 million) investment agreement to double semiconductor substrate capacity and expand camera-module production at its Gumi plant.

- February 2026: ams OSRAM agreed to sell its non-optical analog and mixed-signal sensor business to Infineon for EUR 570 million (USD 608 million), with closing expected in Q2 2026.

- February 2026: Cree Lighting announced a long-term strategic manufacturing agreement with a U.S. industrial-lighting specialist to alleviate capacity constraints.

- September 2025: Lumileds unveiled the LUXEON HL1Z Color Line, a 1.4 mm CSP family enabling dense multi-color arrays.

Global Mid-Power LED Package Market Report Scope

The Mid-Power LED Package Market Report is Segmented by Power Range (0.2W–0.5W and 0.5W–Less Than 1W), Package Architecture (SMD including 2835, 3014, 3030, and Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 0.2W - 0.5W |

| 0.5W - Less Than 1W |

| SMD (Surface Mount Device) | 2835 |

| 3014 | |

| 3030 | |

| Others (3528, 3020, 5050, etc.) | |

| CSP (Chip Scale Package) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Power Range | 0.2W - 0.5W | |

| 0.5W - Less Than 1W | ||

| By Package Architecture | SMD (Surface Mount Device) | 2835 |

| 3014 | ||

| 3030 | ||

| Others (3528, 3020, 5050, etc.) | ||

| CSP (Chip Scale Package) | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and projected size of the mid-power LED package market?

The mid-power LED package market size stands at USD 6.29 billion in 2026 and is forecast to reach USD 7.53 billion by 2031.

How fast is automotive lighting expanding within this space?

Automotive applications are growing at a 4.54% CAGR through 2031 as adaptive driving-beam regulations gain traction.

Why are chip-scale packages gaining share?

CSP designs cut thermal resistance and component count, allowing slimmer, higher-pixel products without major cost penalties as manufacturing yields improve.

What raw-material risks affect LED phosphor supply?

China’s export licensing for yttrium oxide lifted prices by more than 40-fold in 2025, exposing supply chains to the risk of rare-earth concentration.

How are vendors protecting margins amid price pressure?

Leading suppliers focus on automotive-qualified, horticultural, and MiniLED backlight packages where higher performance requirements support price premiums.

Page last updated on: