United States Electric Vehicle Motor Lamination Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 7.23 Billion |

| Market Size (2030) | USD 10.35 Billion |

| Growth Rate (2025 - 2030) | 7.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Electric Vehicle Motor Lamination Market Analysis by Mordor Intelligence

The United States electric vehicle motor lamination market size reached USD 7.23 billion in 2025 and is projected to touch USD 10.35 billion by 2030, registering a 7.45% CAGR over the forecast period. Rapid scale-up of domestic EV assembly lines, efficiency-oriented motor regulations, and reshoring subsidies together propel revenue expansion, while tight electrical-steel supply keeps average selling prices elevated. Domestic automakers accelerate vertical integration to lock in critical magnetic components, tax incentives attract multi-billion-dollar steel investments, and ultra-thin non-oriented grades become mainstream as the Department of Energy tightens performance thresholds. Competitive dynamics stay moderately concentrated because capital-intensive stamping and metallurgical know-how deter new entrants, yet process innovation around rare-earth-free motors and low-scrap manufacturing unlocks fresh margin opportunities.

Key Report Takeaways

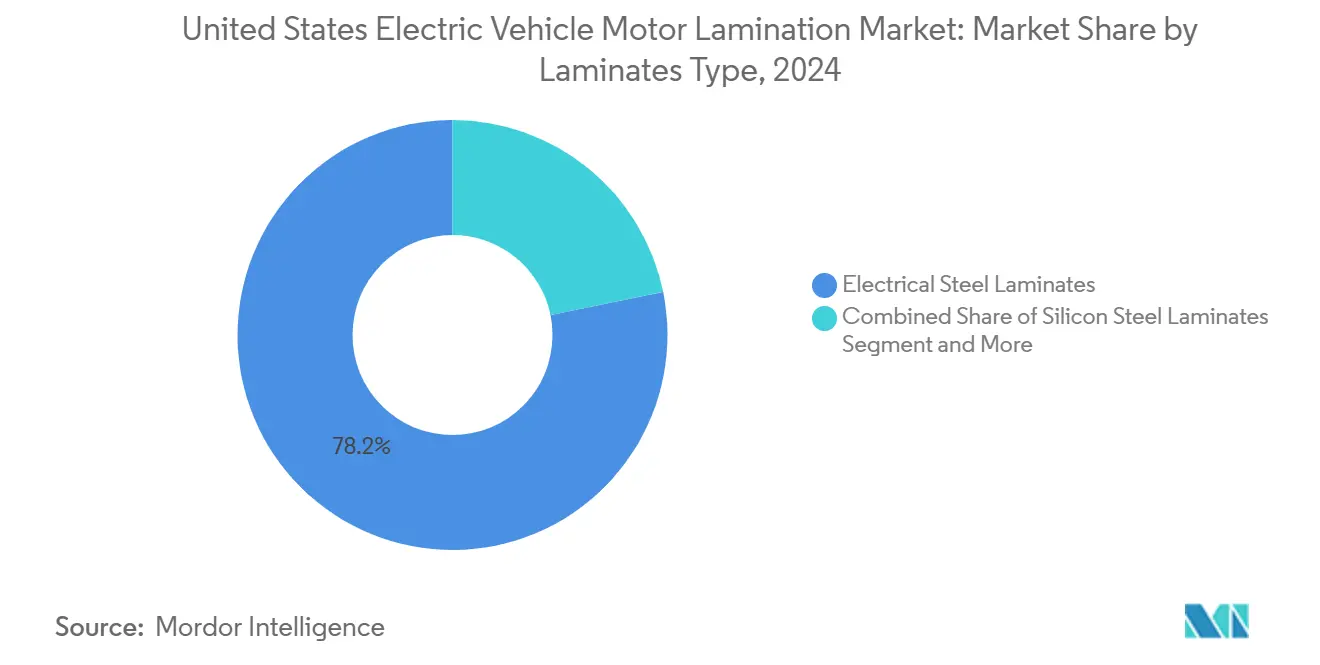

- By laminates type, electrical steel held a 78.23% share of the electric vehicle motor lamination market in 2024, while cobalt-iron laminates are anticipated to grow at a 14.17% CAGR through 2030.

- By motor type, PMSM accounted for 67.86% of the market in 2024, while SRM is projected to expand at a 13.42% CAGR through 2030.

- By vehicle type, passenger vehicles represented 62.47% of the market in 2024, while commercial vehicles are expected to record an 11.09% CAGR through 2030.

- By application, stator dominated with a 57.34% share in 2024, while rotor is forecast to grow at a 12.76% CAGR through 2030.

United States Electric Vehicle Motor Lamination Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRA-Driven EV Output Surge | +2.1% | Michigan, Ohio, Tennessee | Medium term (2-4 years) |

| DOE Thin Lamination Rules | +1.8% | Nationwide, early in California and Northeast | Long term (≥ 4 years) |

| OEM In-House E-Motor Build | +1.3% | Detroit, Southeast manufacturing hubs | Medium term (2-4 years) |

| United States NOES Capacity Growth | +0.9% | Midwest steel belt, Alabama, Arkansas | Short term (≤ 2 years) |

| RE-Free Motors Raise Steel Use | +0.7% | National R&D clusters | Long term (≥ 4 years) |

| State ZEV Rules Speed EV Growth | +0.6% | California and CARB-aligned states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IRA-Fueled Domestic EV Production Boom

Federal manufacturing incentives have triggered the largest industrial reshoring initiative in decades, with EV-related investments reaching USD 199 billion since the Inflation Reduction Act's enactment. The Advanced Manufacturing Production Credit provides direct subsidies for electrical steel lamination production, creating cost advantages that favor domestic suppliers over imports[1]"U.S. Electric Vehicle Manufacturing Investments, Jobs Continue to Grow," Environmental Defense Fund, edf.org.. This policy architecture fundamentally alters procurement decisions as automakers must source 60% of battery components domestically by 2025 to qualify for consumer tax credits, extending similar pressures to motor component supply chains. The geographic concentration in Georgia, Michigan, North Carolina, and Tennessee creates regional supply chain clusters that reduce logistics costs and improve just-in-time delivery capabilities for lamination suppliers.

DOE Efficiency Targets Mandating Ultra-Thin Laminations

The Department of Energy's proposed efficiency standards for expanded scope electric motors establish mandatory performance thresholds that necessitate advanced lamination technologies. Arnold Magnetic Technologies' Arnon NGOES demonstrates this technological shift, offering 0.004-0.007 inch laminations that reduce core losses by up to 50% compared to standard grades, enabling motors to exceed 98% efficiency[2]"Arnold's Arnon Electrical Steel Reduces Eddy Currents to Create Energy Saving Motors and Generators," ien.com.. The regulatory timeline provides manufacturers with adequate lead time to retool production processes, while the efficiency requirements align with California's Advanced Clean Cars II program that mandates 100% ZEV sales by 2035. Compliance costs will disproportionately impact smaller motor manufacturers who lack economies of scale for precision stamping equipment, potentially consolidating market share among larger players with advanced manufacturing capabilities.

Automaker Vertical Integration of E-Motors

Traditional automotive supply chain models face disruption as OEMs pursue vertical integration to control critical EV component costs and performance characteristics. General Motors' Ultium Drive system represents this strategic pivot, featuring five interchangeable drive units and three motors designed for in-house production to optimize battery integration and manufacturing efficiency. This approach mirrors Tesla's vertically integrated model, which has achieved superior cost structures and performance optimization through direct control of motor lamination specifications and sourcing. Ford's CEO emphasized the necessity of managing entire supply chains from raw materials to finished products. At the same time, Mercedes-Benz acquired YASA, a high-performance electric motor manufacturer, to secure proprietary technologies. The International Energy Agency notes that vertical integration reduces manufacturing costs and consumer prices while increasing market concentration, creating opportunities and risks for independent lamination suppliers. Suppliers face margin pressure as OEMs internalize higher-value assembly operations. Still, specialized lamination manufacturers can capture premium pricing through technical expertise and precision manufacturing capabilities that remain difficult to replicate in-house.

Domestic NOES Capacity Expansions (InduX, Cleveland-Cliffs)

Strategic capacity investments by domestic steel producers address supply chain vulnerabilities while capitalizing on policy-driven demand growth. Cleveland-Cliffs expanded its NOES production by approximately 70,000 net tons at the Zanesville facility, positioning the company to serve growing EV motor demand while maintaining its monopoly in US GOES production[3]"CLEVELAND-CLIFFS INC. Annual Report," sec.gov.. U.S. Steel's InduX™ advanced sustainable steels, produced at the Big River Steel facility, offer magnetic properties essential for EV motor manufacturing while containing up to 90% recycled content and reducing CO2 emissions by up to 75%. ArcelorMittal's USD 1.2 billion Alabama investment will add 150,000 metric tons of annual NOES capacity by 2027, representing the most significant single expansion in the domestic market. These capacity additions occur alongside modernization investments, with U.S. Steel's USD 3 billion Osceola, Arkansas, facility featuring two electric arc furnaces with 3 million tons annual capacity and endless casting technology. The geographic distribution of these investments creates regional supply hubs that reduce transportation costs and improve supply chain resilience. At the same time, advanced production technologies enable consistent quality standards required for precision motor applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrical-Steel Price Volatility | -1.4% | Acute for import-dependent buyers | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks | -0.8% | Domestic steel centers | Medium term (2-4 years) |

| High Scrap Rates from Precision Stamping | -0.6% | Nationwide stamping facilities | Medium term (2-4 years) |

| Environmental-Permit Delays | -0.5% | States with strict industrial permitting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrical-Steel Price Volatility

Raw material cost fluctuations create significant margin pressure for lamination manufacturers and downstream motor producers, with electrical steel prices experiencing 60-80% increases since 2020 due to supply chain disruptions and energy cost inflation. The OECD reports that global scrap steel markets face export restrictions from major suppliers like China and Russia, impacting input costs for electric arc furnace production that supplies much of the electrical steel used in motor laminations. China's recent export restrictions on rare earth elements compound pricing pressures, as automakers seek alternative motor designs that increase steel lamination content per unit. Cleveland-Cliffs' monopoly position in US GOES production and duopoly in NOES creates pricing power that transfers cost volatility to customers, while limited domestic capacity forces reliance on imports subject to trade policy uncertainties. The transformer shortage affecting grid infrastructure demonstrates how steel supply constraints cascade through interconnected markets, with wait times for large power transformers increasing significantly and costs rising proportionally.

Supply-Chain Concentration and Capacity Bottlenecks

Market concentration among electrical steel suppliers creates systemic risks that could constrain growth during demand surges. Cleveland-Cliffs' position as the sole US GOES producer and one of only two NOES manufacturers creates single points of failure that concern automotive procurement teams. Precision stamping capacity represents another bottleneck, with Feintool reporting a 41% decline in European e-lamination stamping sales due to political uncertainties and economic pressures, highlighting the specialized nature of this manufacturing step. High scrap rates from precision stamping operations, typically 15-25% for complex geometries, reduce effective capacity utilization while increasing waste disposal costs and environmental compliance burdens. Environmental permitting delays for new steel production lines add 18-36 months to capacity expansion timelines, as demonstrated by EPA regulations for coke oven operations that require extensive environmental impact assessments. The specialized workforce requirements for electrical steel production and precision stamping create additional constraints, as these skills cannot be rapidly scaled during capacity expansions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laminates Type: Electrical Steel Retains Scale, Cobalt-Iron Accelerates

Electrical steel commanded 78.23% of the United States electric vehicle motor lamination market share in 2024, reflecting long-established stamping lines, well-defined material standards, and wide compatibility with today’s permanent-magnet and induction motors. This dominance enables high-volume producers to secure favorable coil pricing and drive down per-kilogram conversion costs, reinforcing the segment’s bulk advantage even as input prices remain volatile.

Growing performance targets, however, are steering R&D budgets toward cobalt-iron laminates, the fastest-growing class with a 14.17% CAGR expected through 2030. These alloys deliver superior saturation flux density and lower core loss at high frequencies, attributes prized in next-generation traction drives that pair wide-bandgap inverters with high-speed rotors. Adoption is still limited by raw-material expense and supply-chain immaturity. Yet, pilot programs at luxury EV brands show that thin-gauge cobalt-iron can trim stator mass and boost efficiency, signaling a profitable niche for precision stampers willing to invest early in specialized tooling.

By Motor Type: PMSM Sets the Pace, SRM Builds Momentum

Permanent-magnet synchronous machines (PMSM) accounted for 67.86% of the United States electric vehicle motor lamination market in 2024, leveraging compact geometry and high torque density that align with mainstream passenger-car range and acceleration metrics. Standardized lamination stacks for interior-magnet designs keep tooling amortization low, offering suppliers competitive pricing on large annual call-offs tied to EV platform cycles.

Switched-reluctance motors (SRM) are projected to expand at a 13.42% CAGR to 2030, fueled by OEM efforts to curb reliance on rare-earth magnets. SRM architectures lean heavily on precise rotor and stator lamination shapes to manage audible noise and torque ripple, creating fresh revenue streams for stampers with laser notching and skewing capabilities. The shift also widens the addressable pool for cobalt-iron laminates because SRM duty cycles benefit from high-saturation alloys that contain iron loss despite magnet-free operation.

By Vehicle Type: Passenger Cars Dominate, Commercial Fleets Gather Speed

Passenger vehicles delivered 62.47% of the United States electric vehicle motor lamination market size in 2024 as federal tax credits, widening model choice, and dense charging networks enticed consumers from internal-combustion options. High production volumes sustain continuous-feed stamping lines, lowering scrap ratios and underpinning healthy supplier margins.

Commercial vehicles, covering light vans to Class 6 trucks, are on course for an 11.09% CAGR through 2030, powered by fleet decarbonization targets and total-cost-of-ownership gains in urban delivery routes. The duty cycle demands thicker back-iron and optimized slot geometry to handle repeated start-stop loads, prompting fleet operators to specify premium-grade laminations that resist mechanical fatigue. As e-commerce mileage accelerates, these platforms create a long-run growth engine that diversifies revenue away from the cyclical retail-auto segment.

By Application: Stator Cores Lead, Rotor Laminations Scale Up

Stators captured 57.34% of the United States electric vehicle motor lamination market share in 2024 because every motor topology, from PMSM to SRM, relies on densely packed slot laminations to generate magnetic fields. Continuous innovation in slot-fill factors and resin-bonding methods keeps stator demand proportional to escalating power ratings, preserving its revenue edge for material suppliers.

Rotor laminations are poised for a 12.76% CAGR between 2025 and 2030 as automakers migrate toward high-speed, high-efficiency drive units that require precision-skewed stacks and advanced balancing. Interior-permanent-magnet and flux-switching designs widen the lamination count per rotor, while magnet-less SRM concepts mandate finely profiled reluctance paths, both trends multiplying unit volumes. Suppliers that master zero-burr punching and low-scrap interlocking can therefore tap a faster-growing slice of the market without sacrificing the economies enjoyed on stator programs.

Geography Analysis

California spearheads demand, securing 23% ZEV penetration in Q1 2025 and enforcing a 2035 zero-emission sales mandate. The state’s USD 1.9 billion charging-network budget underwrites expansive passenger-car uptake. The Midwest and Southeast emerge as manufacturing heartlands: ArcelorMittal’s Alabama plant, U.S. Steel’s Arkansas mill, and Hyundai Steel’s planned Louisiana complex collectively add more than 5 million tons of annual automotive-grade capacity, cutting inbound freight to nearby OEMs.

Federal Section 48C and IIJA funds bridge regional disparities by subsidizing grid upgrades and charger rollouts nationwide, sustaining nationwide lamination orders. Michigan retains R&D prominence, hosting pilot lines for ultra-thin laminations that will feed next-generation motors, while Tennessee’s right-to-work laws and port access entice foreign OEMs.

Infrastructure density and policy frameworks thus sculpt a balanced yet regionally concentrated demand profile for the United States electric vehicle motor lamination market, granting suppliers predictable shipment lanes and lowering working-capital requirements.

Competitive Landscape

Market power remains moderate: Cleveland-Cliffs dominates GOES and co-dominates NOES, yet Worthington Steel, Tempel, and EuroGroup Laminations add stamping depth. Thyssenkrupp’s bluemint® powercore® and U.S. Steel’s InduX™ offer low-carbon alternatives that appeal to ESG-conscious automakers. Consolidation persists, as illustrated by Worthington’s bid for Sitem Group and EuroGroup’s Mexico expansion, which serves Volkswagen, Ford, and General Motors.

Strategic patents around rotor discharge protection and three-in-one drive units bolster OEM bargaining power, while suppliers answer with tool-steel coatings that cut scrap and extend die life. Environmental compliance tightens: July 2024 EPA coke-oven standards elevate production costs yet favor EAF-based newcomers with lighter regulatory loads.

Overall, suppliers differentiate via advanced metallurgy, edge-wound cores, and near-net-shape stamping, sustaining moderate rivalry but high entry barriers within the United States electric vehicle motor lamination market.

United States Electric Vehicle Motor Lamination Industry Leaders

-

Worthington Industries

-

EuroGroup Laminations

-

Carpenter Electrification

-

Feintool International

-

Cleveland-Cliffs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ArcelorMittal began construction of a new electrical steel line at its Calvert facility, marking the start of the company's largest US investment in specialized automotive materials. The project addresses growing demand for non-oriented electrical steel in hybrid and electric vehicle motors.

- March 2024: Worthington Steel agreed to acquire a controlling equity stake in Italy-based Sitem Group, a producer of electric motor laminations for automotive and industrial applications, expected to close in early 2025. This acquisition enhances Worthington's electrical steel lamination business and expands reach in the growing electric vehicle market.

United States Electric Vehicle Motor Lamination Market Report Scope

| Electrical Steel Laminates |

| Silicon Steel Laminates |

| Other Laminates Types (Nickel-iron, Cobalt-iron, etc.) |

| Permanent Magnet Synchronous Motors (PMSM) |

| Induction Motors |

| Switch Reluctance Motors (SRM) |

| Brushless DC Motors (BLDC) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-wheelers |

| Stator Laminations |

| Rotor Laminations |

| By Laminates Type | Electrical Steel Laminates |

| Silicon Steel Laminates | |

| Other Laminates Types (Nickel-iron, Cobalt-iron, etc.) | |

| By Motor Type | Permanent Magnet Synchronous Motors (PMSM) |

| Induction Motors | |

| Switch Reluctance Motors (SRM) | |

| Brushless DC Motors (BLDC) | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| Two-wheelers | |

| By Application | Stator Laminations |

| Rotor Laminations |

Key Questions Answered in the Report

What share did electrical-steel laminates hold in 2024?

Electrical steel secured 78.23% of total U.S. lamination revenue, reflecting mature supply chains and proven performance.

Which laminate material will grow fastest through 2030?

Cobalt-iron laminates are forecast to post a 14.17% CAGR as high-speed and magnet-free motor designs gain traction.

How dominant are permanent-magnet synchronous motors today?

PMSMs represented 67.86% of 2024 demand, benefiting from their high torque density and efficiency.

Why are switched-reluctance motors drawing attention?

SRMs avoid rare-earth magnets and are projected to grow at 13.42% CAGR, expanding opportunities for specialized laminations.

Which vehicle class will drive incremental lamination volume?

Commercial vehicles are set for an 11.09% CAGR because logistics fleets electrify last-mile routes.

What underpins rotor lamination growth?

High-speed interior-magnet and magnet-free topologies call for precision rotor stacks, supporting a 12.76% CAGR to 2030.

Page last updated on: