Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 88.30 Billion |

| Market Size (2031) | USD 166.30 Billion |

| Growth Rate (2026 - 2031) | 13.50% CAGR |

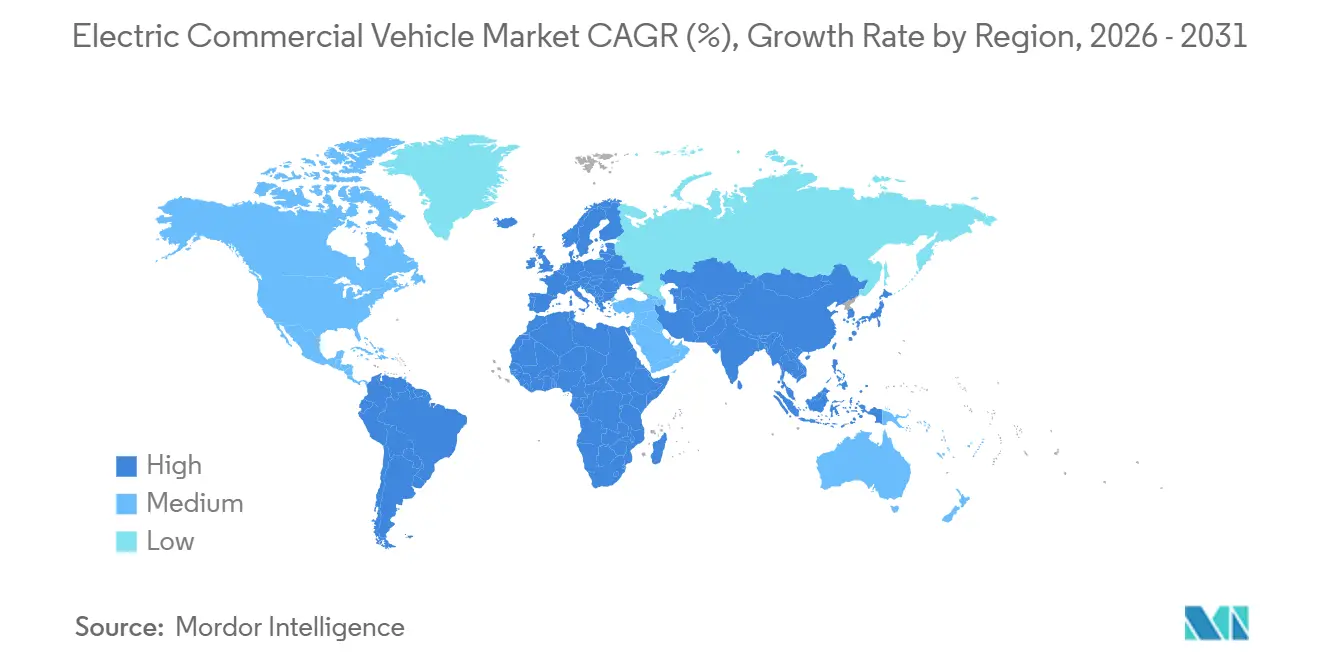

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

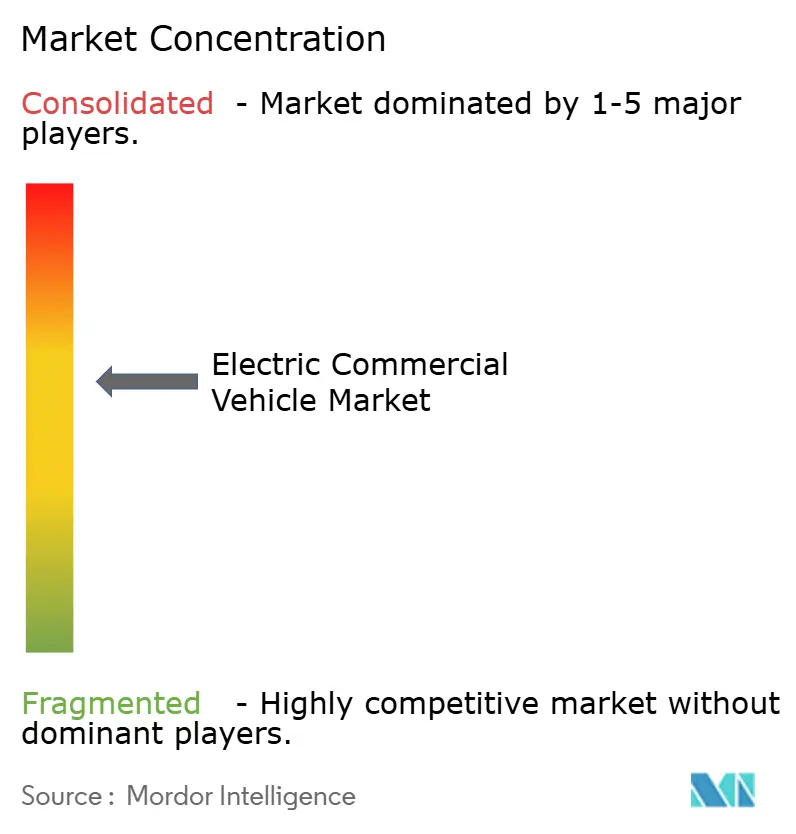

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Commercial Vehicle Market Analysis by Mordor Intelligence

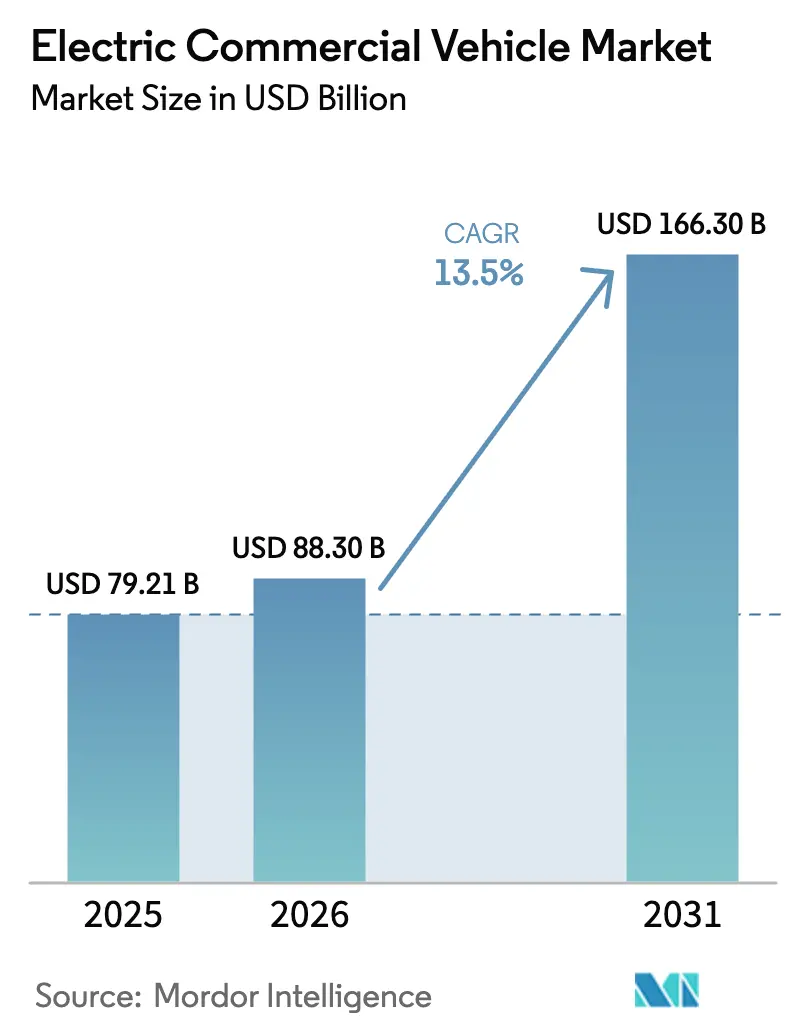

The electric commercial vehicle market size is expected to increase from USD 79.21 billion in 2025 to USD 88.30 billion in 2026 and reach USD 166.30 billion by 2031, growing at a CAGR of 13.5% over 2026-2031. Declining battery pack prices have pushed total ownership costs to parity with diesel across most urban and regional duty cycles, accelerating private-sector adoption. Regulatory mandates on both sides of the Atlantic are synchronizing supply and demand; the United States Environmental Protection Agency now requires a notable share of new heavy-duty sales to be zero-emission by 2032, while Europe enforces a 45% CO₂ cut for heavy trucks by 2030 [1]“Revised CO₂ Standards for Heavy-Duty Vehicles,” European Commission, europa.eu. China’s NEV development plan targets new energy vehicles reaching 20% of total new car sales by 2025. Together, these forces reshape fleet economics, expand manufacturer product lines, and attract capital into charging and hydrogen infrastructure, positioning the electric commercial vehicle market for sustained double-digit growth through the decade.

Key Report Takeaways

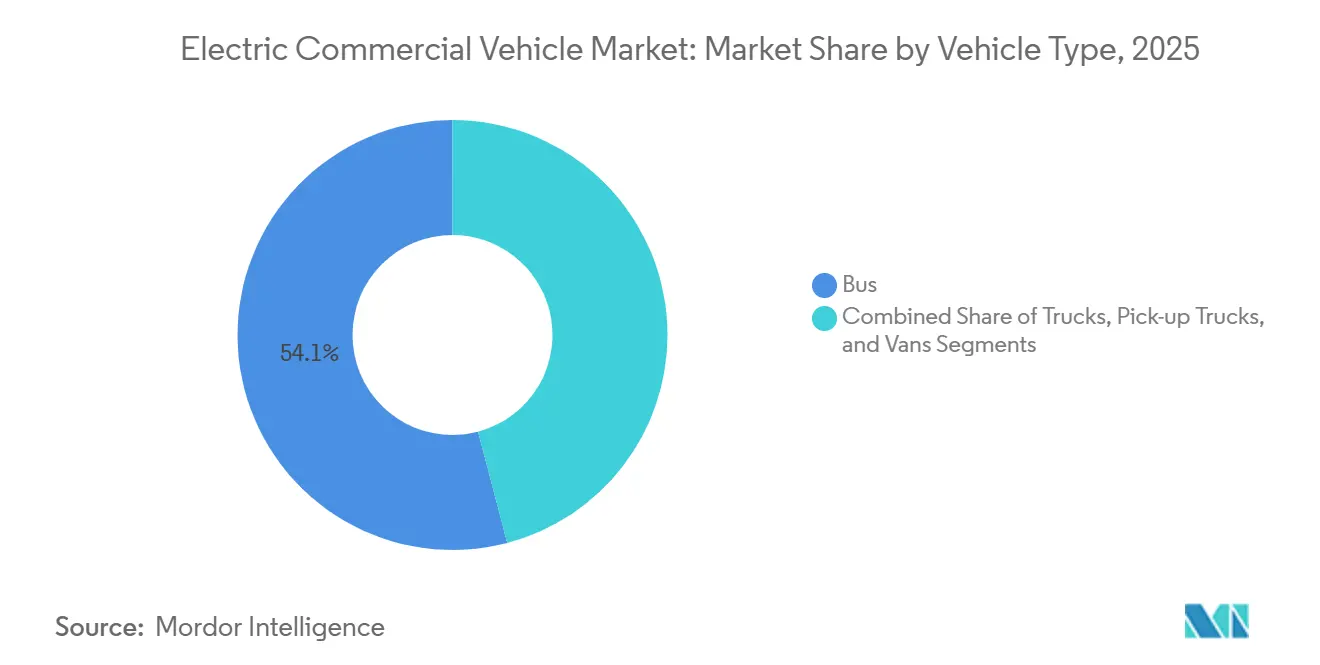

- By vehicle type, buses held 54.12% of the electric commercial vehicle market share in 2025, while trucks are forecast to post a 17.15% CAGR to 2031.

- By propulsion, battery-electric models commanded 82.36% of the electric commercial vehicle market in 2025, and fuel-cell variants are advancing at a 25.01% CAGR through 2031.

- By power output, 150-250 kW held 46.25% share in 2025, while the greater than 250 kW segment will grow at a 15.23% CAGR by 2031.

- By battery capacity, the 100-200 kWh range held a 50.12% share in 2025, while the greater than 200 kWh range is expected to grow at a 14.62% CAGR by 2031.

- By range, vehicles covering 150-300 miles of distance held 48.22% share in 2025, while the greater than 300 miles segment will grow at a 20.13% CAGR by 2031.

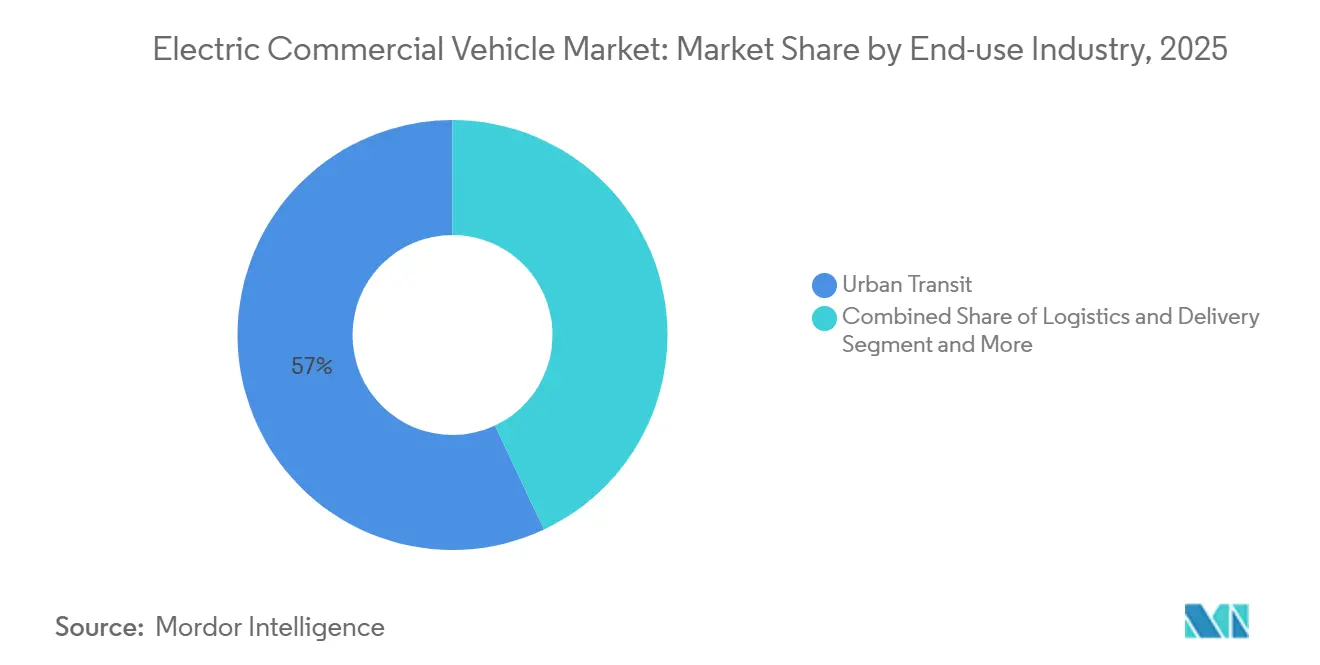

- By end-use industry, urban transit accounted for 57.03% of demand in 2025, and logistics and delivery are growing at a 16.44% CAGR through 2031.

- By charging type, depot AC charging accounted for 68.24% of the market in 2025, while opportunity/en-route DC charging is set to expand at an 18.33% CAGR by 2031.

- By geography, Asia-Pacific accounted for 62.18% of global revenue in 2025; the Middle East and Africa region is expected to expand at a 14.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Electric Commercial Vehicle Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery Costs Drive Breakeven | +4.1% | Global | Short term (≤ 2 years) |

| Zero-Emission Fleet Mandates | +3.2% | United States, EU, China, India | Medium term (2-4 years) |

| E-commerce Boosts E-Delivery | +2.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Hydrogen Hubs Fuel Cells | +2.3% | United States, Japan, South Korea, EU | Long term (≥ 4 years) |

| E-Bus Financing Programs | +1.8% | India, Southeast Asia, South America, Africa | Medium term (2-4 years) |

| Noise Regulations Drive E-Freight | +1.5% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Battery-Cost Decline Below USD 100/kWh Driving TCO Breakeven

In early 2025, lithium-iron-phosphate cell prices reached a significant milestone, crossing the breakeven threshold for high-mileage trucks. CATL's latest-generation cells offer enhanced energy density and cost efficiency, enabling extended ranges without exceeding axle-weight limits. When considering fuel and maintenance savings, Daimler Trucks' eCascadia demonstrates a notable cost advantage over diesel alternatives on regional routes in California. Reflecting a shift in market dynamics, PACCAR reported that a substantial portion of its 2025 orders were placed without relying on subsidies, highlighting the growing economic feasibility of these technologies. Projections suggest further cost reductions in the coming years, potentially eliminating the need for purchase incentives across most operational scenarios.

Government-funded Zero-Emission Fleet Procurement Mandates

The European Commission’s revised heavy-duty CO₂ standards stipulate a 45% cut by 2030 and a 90% cut by 2040, effectively sunsetting new diesel in medium-duty classes. China’s dual-credit scheme rewards over-compliance, prompting BYD to attribute a significant share of its 2025 domestic commercial sales to the incentive framework. India’s FAME-III allocates substantial funding to electric buses and charging infrastructure, with a particular focus on Delhi, Mumbai, and Bengaluru. Such programs spur bulk procurement, accelerate learning curves, and tighten supply chains faster than organic demand growth alone.

E-commerce-led Surge in Urban Last-Mile Delivery Vehicles

Parcel volumes in leading e-commerce markets increased significantly year over year in 2025, driving demand for battery-electric vans suited to dense routes. Amazon has rolled out more than 30,000 custom electric delivery vans from Rivian across the U.S., cutting per-package emissions compared to diesel and demonstrating the operational fit of electrification in last-mile logistics[2]"Everything you need to know about Amazon’s electric delivery vans from Rivian," Amazon, amazon.com. DHL is investing significantly to electrify its van fleet by the end of the forecast period, leveraging the economic benefits of operating in low-emission zones. London's Ultra Low Emission Zone, now covering all boroughs, imposes daily fees on non-compliant vans. This regulatory framework encourages a shift toward electric vehicles, particularly for routes with higher delivery volumes. Urban operations with frequent usage achieve cost recovery quickly, highlighting the critical role of delivery fleets in driving operational growth.

Hydrogen Hub Investments Accelerating Fuel-cell Trucks

By the end of the decade, the United States Department of Energy aims to introduce a significant number of fuel-cell trucks at California ports, supported by a major hydrogen hub program. Japan is planning to establish numerous refueling stations along key corridors to enhance hydrogen infrastructure. South Korea is focusing on increasing the adoption of fuel-cell trucks by providing substantial subsidies and maintaining affordable hydrogen prices. Hyundai's fleet has demonstrated the efficiency and practicality of fuel-cell technology for long-haul operations with quick refueling times. In Europe, a consortium is working to develop a comprehensive network of heavy-duty refueling stations across the continent. These coordinated efforts collectively strengthen the potential for scaling up fuel-cell technology in the heavy-duty vehicle segment.

Restraints Impact Analysis of Electric Commercial Vehicle Market*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-Charger Grid Constraints | −2.1% | North America, Europe, India | Medium term (2-4 years) |

| Battery Pack Payload Penalties | −1.6% | North America, Europe, China | Medium term (2-4 years) |

| Limited Residual-Value Benchmarking | −1.3% | Global | Long term (≥ 4 years) |

| High-Voltage Technician Scarcity | −1.1% | India, Southeast Asia, LatAm, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercial-grade Fast-Charger Grid Constraints on Highway Freight Corridors

The United States operates a limited number of heavy-duty DC chargers above 350 kW, falling short of corridor requirements. In Europe, interconnection queues are significantly long, delaying site energization and pushing fleets onto regional routes. Electrify America notes that a significant portion of its planned truck sites require substation upgrades, each of which entails substantial costs. Meanwhile, India's National Highways Authority has activated only a fraction of its planned truck-charging plazas, with full commissioning now delayed. These grid bottlenecks hinder the potential for long-haul battery-electric penetration until megawatt charging becomes more prevalent.

Payload Penalties from Large Battery Packs in Long-haul Segments

A large battery pack significantly reduces legal payloads in markets with strict gross weight limits. While exemptions exist in some regions, they are insufficient to fully address the revenue gaps for bulk haulers. Users of electric trucks on weight-sensitive routes face notable revenue losses per trip. Even as battery density improves, the gap will narrow but persist, keeping hydrogen as the favored choice for long-haul freight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Electric Commercial Vehicle Market Segment Analysis

By Vehicle Type:

Buses Lead, Trucks Accelerate on Logistics DemandBuses accounted for 54.12% of 2025 revenue, reflecting long procurement cycles and public subsidies that favor fleet-wide deployment in city transit systems, giving the electric commercial vehicle market size a bus-centred foundation. Trucks, however, are growing at 17.15% CAGR through 2031 as e-commerce giants electrify last-mile and regional routes. In recent years, BYD has delivered a significant number of electric buses globally, with the majority allocated to Chinese municipalities due to air-quality mandates. Meanwhile, Ford has experienced notable growth in the sales of its E-Transit vans across North America. While payload penalties hinder the adoption of battery-electric vehicles in long-haul heavy trucks, they steer near-term growth toward regional hauls within a limited radius. Vans, benefiting from modular battery packaging that maintains cargo volume, have become essential for parcel carriers. Notably, DHL's Streetscooter fleet has expanded substantially in recent years.

Continued municipal funding sustains bus dominance in emerging markets, yet the shorter four- to six-year replacement cycles in logistics fleets position trucks to overtake buses in annual volumes after 2028. Fleet operators such as UPS, Amazon, and JD Logistics are creating a secondary market for lightweight electric chassis, expanding supplier diversity beyond traditional bus-focused OEMs. Meanwhile, waste-management authorities and utilities adopt specialized electric chassis for stop-and-go duty cycles, further broadening truck demand. As supply chains mature and chassis versatility improves, trucks are set to become the volume engine of the electric commercial vehicle market, particularly in high-utilization parcel and municipal service routes.

By Propulsion:

BEV Dominance Challenged by FCEV in Heavy-DutyBattery electric powertrains captured an 82.36% share in 2025, benefiting from mature supply chains and the rapid decline in cell pricing, giving the electric commercial vehicle market a clear technology incumbent. Fuel-cell electric vehicles nonetheless post a 25.01% CAGR through 2031, targeting heavy-duty use cases where battery mass erodes payload economics. Hyundai’s XCIENT trucks have clocked more than 5 million kilometers with refueling, validating the business case for hydrogen in long-haul applications[3]"XCIENT Fuel Cell Fleet Racks Up 5 Million km, Reinforcing Hyundai’s Hydrogen Leadership," Hyundai Motor Company, hyundai.com. The United States hydrogen hub program earmarks 1,000 fuel-cell trucks for California ports by 2028, signaling public-sector confidence in the pathway. Plug-in hybrids serve range-constrained regions; Volvo’s plug-in FH variant made up a nominal share of its European electric sales in 2024.

Battery-electric traction will remain dominant in urban and regional fleets because depot charging and low energy prices preserve its cost advantage. Fuel-cell adoption depends on achieving cost competitiveness for hydrogen, which is expected as renewable electrolysis scales in the coming years. As regulators enforce stricter zero-emission standards, hybrid and non-plug-in variants are likely to decline. In the shifting propulsion landscape, batteries are expected to dominate urban routes. At the same time, hydrogen is poised to serve heavier, long-distance freight, expanding the market for electric commercial vehicles.

By Power Output:

Mid-Range Dominates, High-Power Segment Gains on Highway FreightThe 150-250 kW band held 46.25% of 2025 deliveries, aligning with Class 6-7 trucks used for regional distribution. Greater-than-250 kW drivetrains grow at 15.23% CAGR to 2031, catalyzed by Daimler’s eActros 600 and Tesla’s Semi, both of which eliminate range anxiety on major freight corridors. Less-than-150 kW systems dominate light vans such as Rivian’s EDV, where lower power improves affordability and efficiency.

High-power systems require 800-volt architectures that add 15-20% component cost yet enable one-megawatt charging, a critical feature for class 8 tractors. As megawatt infrastructure spreads across Interstate 5, Interstate 95, and European TEN-T corridors, high-power segments will capture a larger slice of the electric commercial vehicle market. Mid-range power will remain prevalent in municipal and regional fleets, where overnight depot charging is sufficient.

By Battery Capacity:

100-200 kWh Leads, >200 kWh Rises with Range DemandsPacks between 100-200 kWh claimed a 50.12% share in 2025, balancing cost, weight, and overnight-charging compatibility for regional work, reinforcing the central role of this block in the electric commercial vehicle market. Greater-than-200 kWh packs are advancing at 14.62% CAGR by 2031 as operators chase 300-mile ranges; Yutong's E12 bus, equipped with a high-capacity battery pack, completes long-distance journeys without the need for opportunity charging. Meanwhile, smaller battery packs power last-mile vans, which typically have shorter range requirements. This approach not only meets operational needs but also helps reduce vehicle costs. For instance, Ford's E-Transit, with a smaller battery, is more cost-effective than its larger counterpart.

Cell-level gains toward 300 Wh/kg enable higher-capacity batteries without breaching axle limits, nudging long-haul fleets to select packs with capacities of 250-400 kWh. Meanwhile, urban operators may downsize to limit capital outlay, proving that the pack capacity strategy will diverge by duty cycle.

By Range:

150-300 Miles Dominates, more than 300 Miles Expands on Battery AdvancesRanges of 150-300 miles accounted for 48.22% of 2025 shipments, aligning with regional and urban duty cycles and strengthening this sweet spot in the electric commercial vehicle market. More than 300-mile capability, growing at a 20.13% CAGR by 2031, appeals to transcontinental North American routes and European long-distance logistics. Volvo's FH Electric demonstrates impressive range capabilities on a single charge. Similarly, PepsiCo's Tesla Semis, even when fully laden, showcase performance that aligns seamlessly with daily driving requirements.

Less-than-150-mile variants remain vital for dense urban parcels; Amazon’s vans average 120 miles per day with ample buffer for seasonal drain. Range choice will track charging density: sparse coverage in India or Southeast Asia obliges higher-range purchases, whereas Europe’s expanding fast-charger grid supports more miniature packs.

By End-Use Industry:

Urban Transit Leads, Logistics Surges on E-commerceUrban transit accounted for 57.03% in 2025, thanks to centralized bus procurements under air-quality rules, which anchored public spending as the primary driver of the electric commercial vehicle market. Logistics and delivery grow 16.44% CAGR through 2031 as parcel volumes swell and low-emission zones impose a penalty price on diesel. Shenzhen plans to electrify a significant number of municipal buses and trucks by 2025, setting a replicable blueprint for other megacities. Waste management and utilities use stop-start trucks to meet municipal noise and emissions limits; Los Angeles ordered several electric refuse trucks in 2025.

High utilization in parcel delivery speeds payback to under three years, positioning logistics as the fastest-growing end-use. Nevertheless, the transit segment’s long vehicle life and scale keep it the single largest vertical through mid-decade.

By Charging Type:

Depot AC Dominates, Opportunity DC Grows with Highway FreightDepot AC charging owned a 68.24% share in 2025, leveraging off-peak tariffs between USD 0.08-0.12 per kWh and aligning with overnight dwell times, thereby supporting the bulk of the electric commercial vehicle market. En route, DC opportunity charging posts an 18.33% CAGR, which is critical for trucks that travel more than 300 miles per day. New York’s MTA has installed a significant number of depot chargers for e-buses, demonstrating the viability of the depot model for large fleets. Electrify America’s 350 kW network enables trucks to add substantial range in federally mandated 30-minute breaks.

Megawatt standards under CharIN and SAE will reduce recharge time to 15 minutes, tipping the long-haul preference toward opportunity charging. Depot models will stay dominant for urban fleets, while corridor operators migrate to high-power public sites.

Geography Analysis

APAC Electric Commercial Vehicle Market

Asia-Pacific controlled 62.18% of 2025 revenue, underpinned by China’s significant electric share of new urban bus orders and India’s FAME-III subsidy for buses and goods carriers. Japan’s Isuzu and Mitsubishi Fuso delivered several electric trucks focused on Tokyo and Osaka's low-emission zones. South Korea exported XCIENT fuel-cell trucks, sharpening domestic hydrogen expertise. The region benefits from centralized procurement, dense urbanization, and air-quality imperatives that accelerate public bus rollouts.

MEA Electric Commercial Vehicle Market

The Middle East and Africa region is expected to record the fastest growth, with a 14.18% CAGR by 2031. Under Vision 2030, Saudi Arabia's Public Investment Fund has allocated significant resources to establish electric bus and truck plants, aiming for substantial annual production in the coming years. Durban financed several e-buses through the African Development Bank, while Egypt aims to electrify a significant number of Cairo buses by 2028 with EBRD loans. Growth rides on sovereign capital and multilateral facilities in markets that lack domestic OEM depth but possess ambitious decarbonization agendas.

North America and Europe Electric Commercial Vehicle Market

North America and Europe mirror each other in regulatory stringency and infrastructure challenges. California’s Advanced Clean Trucks (ACT) regulation requires manufacturers to sell ZEVs as an increasing share of annual sales starting MY2024, reaching 55% (Class 2b–3), 75% (Class 4–8 straight trucks), and 40% (tractors) by MY2035. Canada set aside CAD 2.75 billion (~USD 2 billion) to electrify 5,000 buses by 2026-27. Europe’s 45% heavy-duty CO₂ cut by 2030 is reinforced by German truck subsidies and expanding low-emission zones in France and the United Kingdom. Both continents face grid connection delays along highway corridors, slowing long-haul penetration, yet policy certainty and purchase incentives keep uptake on track for a rapid climb through 2030.

Regulatory Landscape

The regulatory environment for electric commercial vehicles is increasingly defined by enforceable CO2 and greenhouse-gas performance standards for heavy-duty fleets across major markets. In the United States, the Environmental Protection Agency finalized Phase 3 Greenhouse Gas Emissions Standards in March 2024 for Model Year 2027 and later heavy-duty vehicles, using a performance-based framework that allows compliance through multiple technology pathways, including battery-electric and hydrogen fuel-cell powertrains. In Europe, Regulation (EU) 2019/1242 sets CO2 reduction requirements referenced to 2019 baselines, including a 15% reduction requirement during the 2025-2029 period and tighter targets from 2030 for broader vehicle groups.

Recent EU and UK actions have focused on implementation mechanics and compliance flexibility rather than changing the direction of travel. Regulation (EU) 2024/1610 strengthened the EU heavy-duty CO2 framework by amending Regulation (EU) 2019/1242, and in March 2026 the Council of the European Union adopted a targeted amendment to provide manufacturers flexibility in meeting CO2 targets. Separately, Regulation (EU) 2026/1046 adjusted emissions credit calculation rules for the 2025-2029 reporting periods, shaping how manufacturers optimize portfolios across vehicle types and reporting years. In the United Kingdom, the Heavy-Duty Vehicles (Carbon Dioxide Emission Performance Standards) (Vocational Vehicles) Regulations 2025 (No. 794) entered into force in July 2025, establishing procedures to identify and correct misreported vocational vehicles under CO2 performance standards.

Competitive Landscape

The market remains moderately concentrated, with BYD, Daimler Truck, Volvo, Traton, and Yutong collectively holding a notable share of 2025 unit sales, leaving room for regional specialists and start-ups to carve out niches. BYD’s vertically integrated model yields a significant operating margin in commercial vehicles, exceeding the sector average, which supports aggressive pricing in export markets. Daimler Truck and Volvo rely on dense service networks that secure brand loyalty among fleets transitioning from diesel, providing a hedge against cost-led challengers. Tesla secured several semi-truck orders from PepsiCo, Walmart, and UPS, despite limited after-sales coverage, demonstrating that performance credentials and fleet trial data can help offset service gaps.

Strategic alliances reshape the field. Daimler and Volvo pooled significant investment to fast-track fuel-cell systems, sharing R&D and infrastructure costs. Traton harmonizes battery modules across Scania and Navistar, cutting per-vehicle costs. Tata Motors, which holds a significant market share in India’s e-bus market, collaborates with local partners in Southeast Asia and Africa to circumvent tariffs and establish service capabilities. Chinese OEMs undercut European prices, triggering EU anti-dumping investigations that may shape competitive rules of engagement.

White-space opportunities remain in 150-300-mile long-haul segments where fuel-cell economics and service coverage are still developing, and in after-sales for emerging markets with severe technician shortages. New entrants focusing on battery-swapping heavy trucks, like India’s Blue Energy Motors, address downtime pain points. At the same time, leasing platforms collaborate with dealers to seed small electric vehicles across Indian metro areas, demonstrating that the ecosystem complements OEM strategies.

Electric Commercial Vehicle Industry Leaders

-

AB Volvo

-

Traton SE

-

BYD Auto Co., Ltd.

-

PACCAR Inc.

-

Daimler Truck AG

- *Disclaimer: Major Players sorted in no particular order

Electric Commercial Vehicle Market Companies Covered in this Report

- BYD Auto Co., Ltd.

- Daimler Truck AG

- AB Volvo

- Traton SE

- Zhengzhou Yutong Bus Co., Ltd

- Ford Motor Company

- Tesla Inc.

- Proterra Inc.

- Rivian Automotive Inc.

- Tata Motors Limited

- Olectra Greentech Limited

- PACCAR Inc.

- Nikola Corporation

- NFI Group Inc. (New Flyer)

- Hyundai Motor Company

- Isuzu Motors Limited

- Mitsubishi Fuso Truck & Bus Corporation

Market Opportunities and Future Outlook

Scale-up from pilots into repeatable, high-utilization use cases is creating near-term whitespace in regional haul, terminal operations, and municipal service fleets where duty cycles align with depot charging and predictable routes. A pocket of demand is also emerging around yard and port equipment, supported by fleet-grade procurement: Orange EV announced a 600-unit order for electric terminal trucks in June 2026, pointing to larger multi-site electrification programs in logistics nodes where centralized charging and uptime monitoring can be standardized. On-road heavy trucking is also shifting toward higher-volume supply, with Tesla starting high-volume production of Class 8 Semi tractors at its Reno facility on April 29, 2026, which improves vehicle availability for fleet trials that depend on steady supply, service planning, and parts pipelines.

Manufacturing localization and policy-linked roadmaps are broadening entry points beyond traditional early-adopter markets, particularly where governments and industry are building domestic capability alongside fleet electrification targets. In China, policy direction and market penetration offer a clearer signal for heavy-duty volume adoption: the heavy-duty new energy (NEV) truck market reached 29% penetration of new registrations in 2025 (231,100 units), and a 2030 master plan has been released targeting 40% NEV penetration for heavy-duty trucks over 12 tonnes, linking vehicle uptake with freight-corridor infrastructure buildout. In emerging markets, localization initiatives are creating supplier and assembler opportunities for trucks, vans, and supporting components, illustrated by the May 2026 partnership between Hybrid Motors Nigeria and Launch Design Shanghai to establish production facilities in Lagos and Abuja with a combined annual capacity of 70,000 electric vehicles. Across Europe, the 2025-2029 reporting cycle under the EU heavy-duty CO2 framework, along with country-level purchase support and CO2-linked toll differentiation (for example, Eurovignette-linked reductions in multiple countries), is encouraging fleets to evaluate total-cost pathways where charging access and route planning are treated as part of the vehicle procurement decision.

Recent Industry Developments in Electric Commercial Vehicle Market

- May 2026: TRATON GROUP issued a 500 million Euro green bond and secured a 350 million Euro green loan to fund investments in battery-electric commercial vehicles. The financing framework strengthens funding capacity for product development and industrialization across group brands, supporting broader platform rollouts and supply-chain commitments.

- December 2025: Volvo Trucks introduced the Volvo FL Electric with new battery technology, targeting improved usability for urban distribution applications. The update supports fleets with stop-and-go duty cycles by improving energy storage capability within a compact truck platform, reinforcing electrification economics in city logistics.

- September 2024: Volvo announced a breakthrough program to launch an electric truck platform with up to 600 km range, aimed at longer-distance operations. The move highlighted OEM prioritization of long-haul electrification through higher-energy storage and charging compatibility, raising the competitive bar for range-focused heavy-duty offerings.

Electric Commercial Vehicle Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers commercial road vehicles that move goods or paying passengers and use an electric powertrain, including battery electric, plug-in hybrid, hybrid, and fuel-cell models. It includes trucks, buses, vans, and pickups above 2.5 tons.

Scope exclusions: off-highway equipment, two and three wheelers, airport-only shuttles, and internal-combustion retrofits are not counted.

Segments Covered in This Report

-

By Vehicle Type

- Bus

- Trucks

- Pick-up Trucks

- Vans

-

By Propulsion

- Battery Electric Vehicles (BEV)

- Hybrid Electric Vehicles (HEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Fuel-cell Electric Vehicles (FCEV)

-

By Power Output

- Less than 150 kW

- 150-250 kW

- Greater than 250 kW

-

By Battery Capacity

- Less than 100 kWh

- 100-200 kWh

- Greater than 200 kWh

-

By Range

- Less than 150 miles

- 150-300 miles

- More than 300 miles

-

By End-use Industry

- Urban Transit

- Logistics and Delivery

- Waste Management

- Utilities and Construction

-

By Charging Type

- Depot (AC)

- Opportunity / En-route (DC)

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Egypt

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean fact base on fleet electrification, commercial vehicle registrations, and policy timelines, since those inputs shape adoption and pricing. We lean on public sources such as IEA EV outlook datasets, IEA Global EV Data, government transport and vehicle registration statistics, and city or national clean-transport policy portals.

To anchor volumes and trade signals, we also review customs import-export statistics, national energy agencies for charging and power pricing indicators, and peer-reviewed journals on battery cost and durability trends. Supporting checks include company annual reports, investor presentations, and reputable press coverage of fleet tenders and depot charging deployments. Where useful, analysts also reference paid subscriptions for company financials and intelligence, patent databases, and shipment-level trade data. These examples are not exhaustive, and many other public and paid sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test adoption assumptions and price curves, especially where published statistics lag the market. We speak with fleet operators, vehicle OEM and component stakeholders, charging and infrastructure experts, and channel participants across the Americas, EMEA, and APAC to confirm what is actually being ordered, delivered, and put into service.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 48% |

| Mid tier: 56% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 15% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that reconstructs demand by combining commercial vehicle sales and parc signals with electrification penetration, then converts it into value using observed price bands by vehicle class and powertrain. Once the first cut is produced, it is checked with selective bottom-up approximations such as sampled model-level pricing, announced fleet orders, and channel feedback on delivery run rates, and then totals are adjusted when the gaps are explainable.

Inputs include commercial vehicle registrations and sales by class, fleet procurement and tender activity, battery pack cost direction and typical pack sizes by use case, charging infrastructure rollout pace for depots and corridors, and policy markers such as zero-emission mandates and incentive sunsets. Where smaller countries or niche vehicle classes have limited public data, gaps are handled using regional analogs and penetration curves validated in interviews, and then scaled back to local macro and vehicle parc context. For forecasting, scenario analysis is used because regulation timing, infrastructure readiness, and total cost of ownership improvements can shift adoption in steps, and those scenarios are aligned with what primary respondents expect in their planning cycles.

Data Validation & Update Cycle

Results are validated through cross-checks against independent signals like EV charging additions, battery supply announcements, and commercial vehicle shipment and registration trends, so major mismatches are flagged early. When outliers appear, assumptions are reopened, and respondents are re-contacted if the variance looks tied to a real market change rather than a data issue.

Before sign-off, the model goes through multi-step analyst reviews, including logic checks on unit-to-value conversions, currency timing consistency, and year-on-year growth realism by region and vehicle type. The report is refreshed annually, and interim updates are made when material events occur, such as policy changes, sharp battery price moves, or demand shocks. Right before delivery, a final pass is completed so clients receive the latest view available at that time.

Mordor Intelligence's Electric Commercial Vehicle Market Size Measured Against Other Published Estimates

It is normal to see different market values for electric commercial vehicles because publishers do not always count the same powertrains, weight thresholds, and use cases, and they also pick different base years. Currency conversion timing and whether forecasts assume steady adoption or step changes driven by regulation can add another layer of spread.

By tracking registration and delivery indicators and refreshing the adoption and pricing assumptions annually, Mordor Intelligence keeps the value tied to road-going trucks, buses, vans, and pickups above 2.5 tons and avoids spillover from adjacent mobility categories or infrastructure spending. Another common gap comes from powertrain boundaries, since some sources focus only on BEVs, while others mix hybrids and fuel-cell vehicles, and that changes the starting value and the growth profile.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 88.30 B (2026) | |

| Global Consultancy A | USD 80.69 B (2025) | Uses a different base year and often emphasizes BEV and PHEV splits, which can shift what gets counted when hybrids and fuel-cell vehicles are included, and it can also change the implied price curve used for early years. |

| Regional Consultancy B | USD 62.09 B (2024) | Reports an earlier base year and may apply different inclusion rules around related ecosystem items and technology buckets, which can compress or expand the vehicle-only value depending on what is bundled into the market boundary. |

Taken together, the spread is mainly explained by base-year timing and by what each source chooses to include as an electric commercial vehicle. Our approach stays traceable because the value is built from clear demand signals, checked with real-world ordering and delivery feedback, and then reviewed for consistency before publication.

Key Questions Answered in the Report

How large is the electric commercial vehicle market in 2026?

The electric commercial vehicle market size is USD 88.30 billion in 2026 and is forecast to grow to USD 166.30 billion by 2031 at a 13.50% CAGR.

Which regional market leads global adoption?

Asia-Pacific accounts for 62.18% of 2025 global revenue thanks to China’s near-universal electrification of urban bus fleets and India’s new subsidies.

What vehicle type represents the biggest share today?

Buses hold 54.12% share in 2025 because municipal transit agencies bulk-purchase electric fleets under clean-air mandates.

Which propulsion technology is growing fastest?

Fuel-cell electric trucks post a 25.01% CAGR through 2031 as hydrogen hubs and weight-sensitive long-haul routes gain support.

Page last updated on: