North America Automotive Retrofit Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

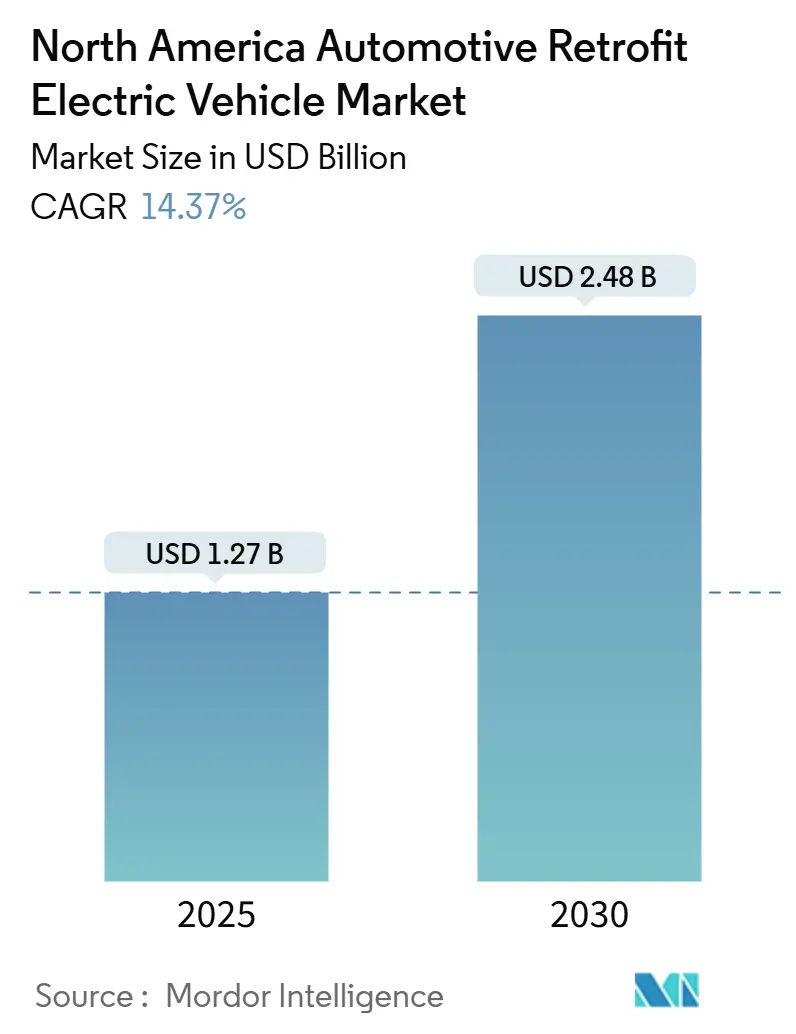

| Market Size (2025) | USD 1.27 Billion |

| Market Size (2030) | USD 2.48 Billion |

| Growth Rate (2025 - 2030) | 14.37% CAGR |

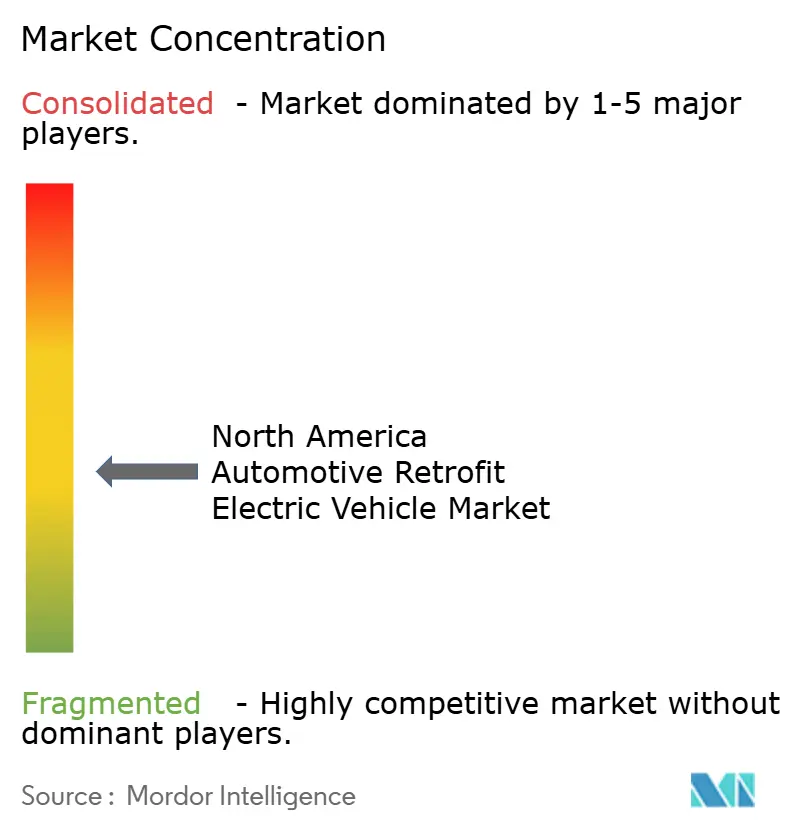

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Retrofit Electric Vehicle Market Analysis by Mordor Intelligence

The North America Automotive Retrofit Electric Vehicle Market size is estimated at USD 1.27 billion in 2025, and is expected to reach USD 2.48 billion by 2030, at a CAGR of 14.37% during the forecast period (2025-2030). Fleet operators and individual owners view retrofitting as a practical route to electrification because it preserves existing vehicle assets while satisfying stricter Environmental Protection Agency (EPA) and California Air Resources Board (CARB) standards. Battery pack prices averaged USD 115 per kWh in 2025, down around four-fifths since the decade, a decline sharply narrows the cost gap between conversions and new battery-electric vehicles. The Inflation Reduction Act’s Section 45W credit of up to USD 40,000 per heavy conversion and USD 7,500 for lighter vehicles further improves payback periods for commercial fleets. Programs such as the Diesel Emissions Reduction Act (DERA) distribute a considerable amount each year for diesel-to-electric upgrades, concentrating demand in regions that fail to meet federal air-quality limits.

Key Report Takeaways

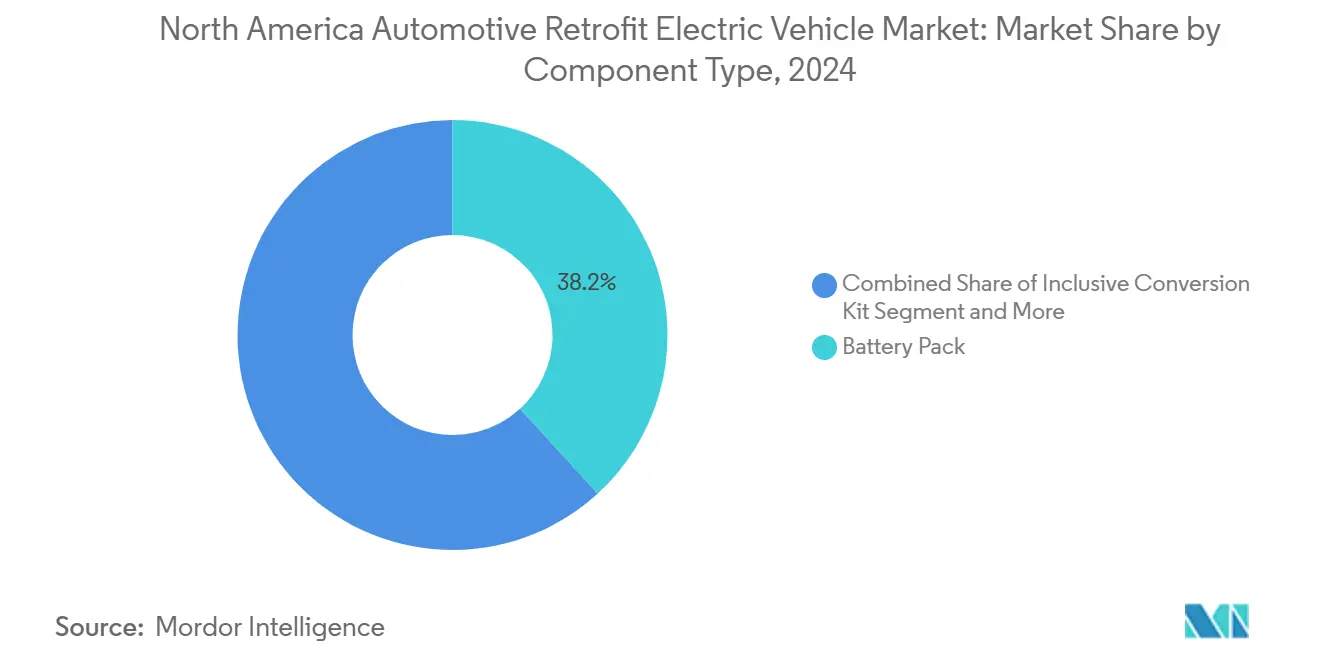

- By component type, battery packs led with 38.16% of the North America automotive retrofit electric vehicle market share in 2024, while chargers are projected to post the fastest 14.46% CAGR through 2030.

- By vehicle type, passenger cars held 47.16% of the North America automotive retrofit electric vehicle market share in 2024, yet heavy commercial vehicles are forecast to expand at a 14.41% CAGR to 2030.

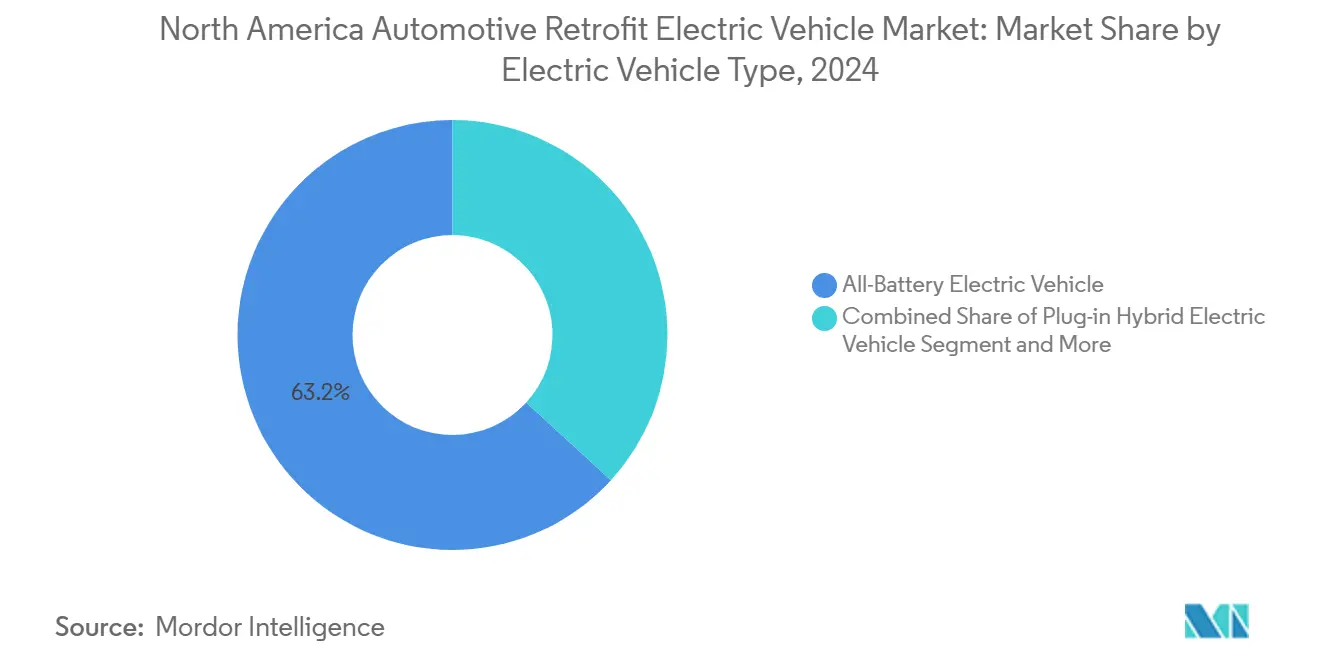

- By electric vehicle type, all-battery conversions captured 63.24% of the North America automotive retrofit electric vehicle market share in 2024 and are expected to log the highest 14.48% CAGR through 2030.

- By installation channel, professional fleet retrofitters controlled 67.11% of the North America automotive retrofit electric vehicle market share in 2024 and are set to advance at a 14.51% CAGR during the outlook period.

- By country, the United States accounted for 78.47% of the North America automotive retrofit electric vehicle market share in 2024 and is anticipated to register a 14.39% CAGR to 2030.

North America Automotive Retrofit Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Epa/Carb Emission-Compliance Deadlines | +3.2% | United States, with spillover to Canada | Medium term (2-4 years) |

| Rapid Li-Ion Usd/Kwh Decline | +2.8% | Global, with manufacturing concentration in North America | Short term (≤ 2 years) |

| Federal & State Retrofit Grant Programmes | +2.1% | United States, selective state programs in Canada | Medium term (2-4 years) |

| Inflation Reduction Act 45W Commercial EV Tax Credit | +1.9% | United States exclusively | Long term (≥ 4 years) |

| Circular-Economy Push To Extend Ice Fleet Lifecycles | +1.4% | North America and EU, with early adoption in urban centers | Long term (≥ 4 years) |

| Fleet-Insurance Premium Discounts | +0.8% | United States, with emerging programs in Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening EPA / CARB Emission-Compliance Deadlines

EPA multipollutant standards require more than half of fully electric and around one-tenth of plug-in hybrid sales by 2032, while California’s Advanced Clean Cars II rule mandates around two-fifths of zero-emission sales by 2026 and complete by 2035. Retrofits give fleet owners with long-lived assets a compliance path without replacing entire vehicles. CARB streamlined conversion approvals in 2023, cutting certification time and cost, which accelerates market entry for retrofit kit suppliers. Demand intensifies in non-attainment air-quality zones where enforcement is strict. As regulators phase in penalties for high-emission fleets, certified conversion solutions gain a durable advantage.

Rapid Li-Ion Usd/Kwh Decline & Kit Modularisation

Battery pack prices fell in 2025 and could grow exponentially by 2035, with Inflation Reduction Act credits pushing the effective cost below USD 60 per kWh before 2030. Lower cell costs reduce total conversion outlays by up to 35% compared with 2022 levels, improving return on investment for commercial fleets. Modular kits standardize wiring harnesses, control algorithms, and mounting brackets, enabling quicker installations and higher technician throughput. Legacy EV offers a five-tier kit lineup that covers do-it-yourself to plug-and-play solutions, signaling a broader shift toward mass-market accessibility. Improved battery-management software and liquid cooling extend warranty life and limit degradation.

Federal & State Retrofit Grant Programmes (Dera, Clean Heavy-Duty Vehicle)

DERA grants cover up to 45% of an eligible diesel-to-electric repower, channeling roughly USD 115 million per year into zero-emission projects. California alone received more than USD 900,000 in 2023 for bus electrification. Parallel initiatives under the Joint Office of Energy and Transportation earmark USD 46.5 million for charging performance R&D, easing infrastructure bottlenecks. Many grants prioritize environmental-justice ZIP codes, which accelerates adoption in urban freight corridors. Scrappage rules ensure permanent emissions cuts by requiring destruction of the removed diesel engine.

Inflation Reduction Act § 45W Commercial Ev Tax Credit For Repowers

Section 45W allows a 30% credit, capped at USD 40,000 for vehicles above 14,000 lb and USD 7,500 otherwise. January 2025 IRS guidance published safe-harbor cost models, simplifying claims for small fleets. Tax-exempt entities such as municipalities may receive direct payments rather than credits, broadening the customer base. The provision expires in 2032, giving retrofitters a clear, multi-year demand runway. An 18-month recapture clause protects federal revenue while providing operators confidence that credits will not be clawed back after minor operational changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-front Kit | -2.4% | Global, with acute impact in price-sensitive segments | Short term (≤ 2 years) |

| Scarcity of Certified Installers | -1.8% | North America, with rural areas most affected | Medium term (2-4 years) |

| Unclear Residual-Value Assessment | -1.2% | United States and Canada, affecting fleet financing | Long term (≥ 4 years) |

| Patch-Work Local Zoning & Permitting | -0.9% | United States, with state-level variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Kit and Certification Cost

Complete conversions range from USD 6,000 to over USD 20,000 after labor, representing as much as 50% of the price of a new electric model. Smaller installers face EPA and CARB fees exceeding USD 5,000 per system certification, pushing them out of the market. Although Legacy EV markets a kit, professional installation often doubles the total bill. Individual owners and small fleets without tax appetite struggle to capture credits, limiting retail uptake. High-end commercial applications remain the early winners because their duty cycles justify the investment.

Scarcity of Certified Installers & Workforce

Only 16% of automotive technicians possess EV qualifications, creating wait times exceeding eight weeks in some regions. Electrician shortages further slow depot charger installation, forcing fleets to phase conversions. The Society of Automotive Engineers partnered with ChargerHelp! to launch a national certification, yet capacity lags demand. Goodwill’s pilot EV tech training graduates 300 students annually, which is insufficient for the thousands of conversions expected annually. Rural counties feel the pinch as installers cluster in major metros, adding travel cost and downtime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Battery Packs Anchor System Value

Battery packs accounted for 38.16% of the North America automotive retrofit electric vehicle market size in 2024, underscoring their central role in overall bill-of-materials and integration complexity. Thermal management modules, battery-management software, and high-voltage wiring drive cost and engineering effort. Suppliers now offer pack-in-box designs that bundle cooling, mounting, and monitoring in a single unit, cutting installation hours by two-fifths. Charger hardware is the fastest-advancing component class, logging a 14.46% CAGR as fleets request split-phase AC charging for depot use and public-fast-charge interoperability. Integrated motor-inverter packages reduce wiring bulk and allow easier placement within cramped engine bays. ZF’s eBeam Axle, rated at 300 kW, illustrates a shift toward drop-in electrified drivetrains for light trucks, lowering axle swap labor time to two hours. Combined DC-DC converter and onboard charger units also streamline conversion layouts, which is critical when technician bandwidth is scarce.

Continued battery-chemistry advances such as lithium-iron-phosphate-plus-manganese hybrids promise longer cycle life, enabling warranty periods aligned with eight-year financing terms. Second-life battery programs allow retrofitted packs to be sold into stationary storage after vehicle end-of-life, improving total asset economics. Component vendors now package telematics gateways that feed State of Health data to fleet portals, giving operators early warning of pack degradation. These upgrades help the North America automotive retrofit electric vehicle market maintain momentum by improving reliability perceptions among conservative fleet managers.

By Vehicle Type: Heavy Commercial Fleets Lead Expansion

Passenger cars held 47.16% of the North America automotive retrofit electric vehicle market share in 2024, reflecting early adoption by enthusiasts and small business owners. Yet heavy commercial vehicles will post the quickest 14.41% CAGR due to the favorable total cost of ownership when diesel prices stay above USD 3 per gallon. Parcel carriers, school districts, and transit agencies view repowers as a means to accelerate compliance with zero-emission mandates while keeping chassis they already own. ETruck Transportation’s hybrid Class 8 package, slated for series production in late 2025, retains the existing transmission and cuts fuel use up to 40%, lowering payback to four years.

Light commercial van conversions also rise as e-commerce drives last-mile trip counts; operators can retrofit a high-roof van in three days at a cost roughly one-third below a factory electric model. Two-wheelers and niche off-road vehicles are gaining attention where range needs are modest and parking regulations penalize noisy engines. Across segments, financing institutions now bundle retrofit loans with charging-station leases, smoothing cash flow for small haulers. These dynamics keep the North America automotive retrofit electric vehicle market attractive to component makers that can tailor solutions across varied duty cycles.

By Electric Vehicle Type: All-Battery Systems Dominate

All-battery retrofits captured 63.24% of the North America automotive retrofit electric vehicle market in 2024 and are on track for the highest 14.48% CAGR to 2030, buoyed by simple architecture and zero-tailpipe-emission eligibility under strict state rules. Pure-battery layouts remove internal combustion elements, easing certification under the EPA Clean Alternative Fuel Vehicle umbrella. Plug-in hybrids remain relevant for range-critical rural delivery routes where public chargers remain scarce, though their added complexity raises labor costs by 18% over full-battery builds.

Conventional hybrids lose share as regulators focus on full electrification, yet they remain a bridge for operators not ready to risk charging downtime. NetGain Technologies’ engine-motor interface promises a 30-month payback on mixed-duty fleets by allowing incremental electrification without expensive driveline swaps. Batteries with high-silicon anodes are expected to enter retrofit supply chains by 2027, delivering one-fifths higher energy density that maintains vehicle payload. Advances like these ensure that North America's automotive retrofit electric vehicle market size, which is tied to all-battery conversions, keeps expanding as battery supply chain localization reduces lead times.

By Installation Channel: Professional Retrofitters Capture Most Revenue

Professional fleet retrofitters controlled 67.11% of the North America automotive retrofit electric vehicle market in 2024 and are forecast to climb at a 14.51% CAGR through 2030, a trend driven by complex certification and warranty requirements. Operators prefer turnkey services that bundle system design, installation, emissions testing, and tax-credit paperwork. Large retrofit shops now sign multiyear maintenance contracts, including over-the-air software updates and periodic traction-battery health audits.

DIY and enthusiast workshops remain a vibrant but smaller niche, serving hobbyists and older classic-car conversions where regulatory pressure is lighter. Online platforms offer video-supported kits, yet insurers often demand professional sign-off to underwrite liability policies. Major installers partner with community colleges to scale capacity to create 12-week conversion-technician boot camps. Rising labor costs push shops toward modular kit solutions that reduce wrench time, thereby protecting margins and keeping the North America automotive retrofit electric vehicle industry competitive even as technician shortages persist.

Geography Analysis

The United States represented 78.47% of the North America automotive retrofit electric vehicle market in 2024, and is growing at a 14.39% CAGR to 2030, aided by Section 45W credits up to USD 40,000 and DERA grants that distribute USD 125 million annually. California’s waiver for Advanced Clean Cars II accelerates adoption, while Texas and Florida trail due to patchwork permitting. Midwest states leverage brownfield depot sites for charging hubs, lowering grid-upgrade costs. Workforce shortages remain most acute in the Great Plains, delaying rural conversions.

Canada’s zero-emission vehicle share reached around one-fifth in Q4 2024, and the federal roadmap predicts a USD 104 billion contribution to gross domestic product by 2040[1]“Zero-Emission Vehicle Update Q4 2024,” Natural Resources Canada, nrcan.gc.ca . Yet the retrofit segment faces weaker tax incentives than new EV purchases. Quebec maintains a provincial rebate that keeps its EV share above 30%, whereas British Columbia slipped to 22.8% after it capped subsidies at CAD 4,000 (USD 3,000) in 2024. The country needs an estimated 679,000 public chargers by 2040, making repowers an interim compliance tool while infrastructure builds out.

Mexico and the rest of North America form nascent markets. Mexico’s Olinia project, launched in January 2025 with MXN 25 million (USD 1.4 million), prioritizes domestic EV manufacturing, yet retrofit opportunities emerge from a 2035 fossil-fuel phase-out target[2]“Plan de Electromovilidad Olinia,” Government of Mexico, gob.mx . Limited high-power charging along freight corridors slows adoption, pressuring fleets to favor plug-in hybrid repowers for long-haul duty. Cross-border supply chains promise cost savings once the United States–Mexico–Canada Agreement (USMCA) streamlines rules-of-origin for battery modules. Collectively, geographic disparities reinforce the need for localized policy support to sustain the North America automotive retrofit electric vehicle market.

Competitive Landscape

The market remains fragmented, with no firm exceeding one-tenth of the revenue share in 2024. Traditional drivetrain suppliers such as BorgWarner, Dana, and Bosch extend electrification portfolios through acquisitions and joint ventures, leveraging long-standing OEM ties. Dana's growing sales and announced electrification backlog signal the scale incumbents can deploy[3]“2023 Annual Report,” Dana Incorporated, dana.com. Start-ups, including Legacy EV and Lightning eMotors, specialize in modular conversion kits and fleet repowers. Yet, Lightning trimmed its headcount by 20% in late 2024 to cut costs after a slow municipal order cycle.

Technology strategy converges on scalable, software-defined architectures that allow over-the-air torque mapping and remote diagnostics, features that fleets demand to minimize downtime. Certification know-how under EPA and CARB rules is an entry barrier, favoring firms that invest early in testing labs. White-label agreements let smaller kit designers piggyback on large integrators’ approvals, broadening market reach while containing compliance expenses.

Rural installation deserts create an untapped opportunity for mobile retrofit units, trailers equipped with lifts, diagnostic rigs, and battery hoists that can convert vehicles at customer depots. Financing innovations such as power-purchase-agreement-style contracts spread capital costs over kilowatt-hours consumed, appealing to budget-strapped school districts. These initiatives keep competitive intensity high and ensure continued innovation within the North America automotive retrofit electric vehicle market.

North America Automotive Retrofit Electric Vehicle Industry Leaders

Legacy EV

Lightning eMotors

EV West

XL Fleet (Spruce Power)

SEA Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Stellantis Pro One introduced manufacturer-backed retrofit packages for light commercial vans, pairing OEM warranties with dealer installation networks.

- December 2024: EPA granted California a waiver for Advanced Clean Cars II, locking in a pathway to 100% zero-emission sales by 2035.

North America Automotive Retrofit Electric Vehicle Market Report Scope

| Inclusive Conversion Kit |

| Electric Motor |

| Battery Pack |

| Controller |

| Charger |

| Others (Axle, DC-DC Converter, etc.) |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| All-Battery Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| Hybrid Electric Vehicle |

| Professional Fleet Retrofitters |

| DIY / Enthusiast Workshops |

| United States |

| Canada |

| Mexico |

| By Component Type | Inclusive Conversion Kit |

| Electric Motor | |

| Battery Pack | |

| Controller | |

| Charger | |

| Others (Axle, DC-DC Converter, etc.) | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| By Electric Vehicle Type | All-Battery Electric Vehicle |

| Plug-in Hybrid Electric Vehicle | |

| Hybrid Electric Vehicle | |

| By Installation Channel | Professional Fleet Retrofitters |

| DIY / Enthusiast Workshops | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North America automotive retrofit electric vehicle market?

The North America automotive retrofit electric vehicle market size reached USD 1.27 billion in 2025.

How fast is the retrofit segment growing?

The market is projected to advance at a 14.37% CAGR and could double to USD 2.48 billion by 2030.

Which component captures the most revenue in retrofit projects?

Battery packs dominate with 38.16% share because they include costly thermal and control systems.

Why are heavy commercial vehicles converting fastest?

Fleet operators gain sizable fuel and maintenance savings plus Section 45W tax credits of up to USD 40,000, leading to a 14.41% CAGR for heavy trucks.

How do Section 45W credits work for repowers?

The credit equals 30% of the conversion basis, capped at USD 40,000 for vehicles above 14,000 lb and USD 7,500 for lighter units, and is available through 2032.

What limits wider consumer adoption of retrofit EVs?

High up-front kit costs and a shortage of certified installers make it challenging for individual owners to justify conversions.

Page last updated on: