United States Electric Shavers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

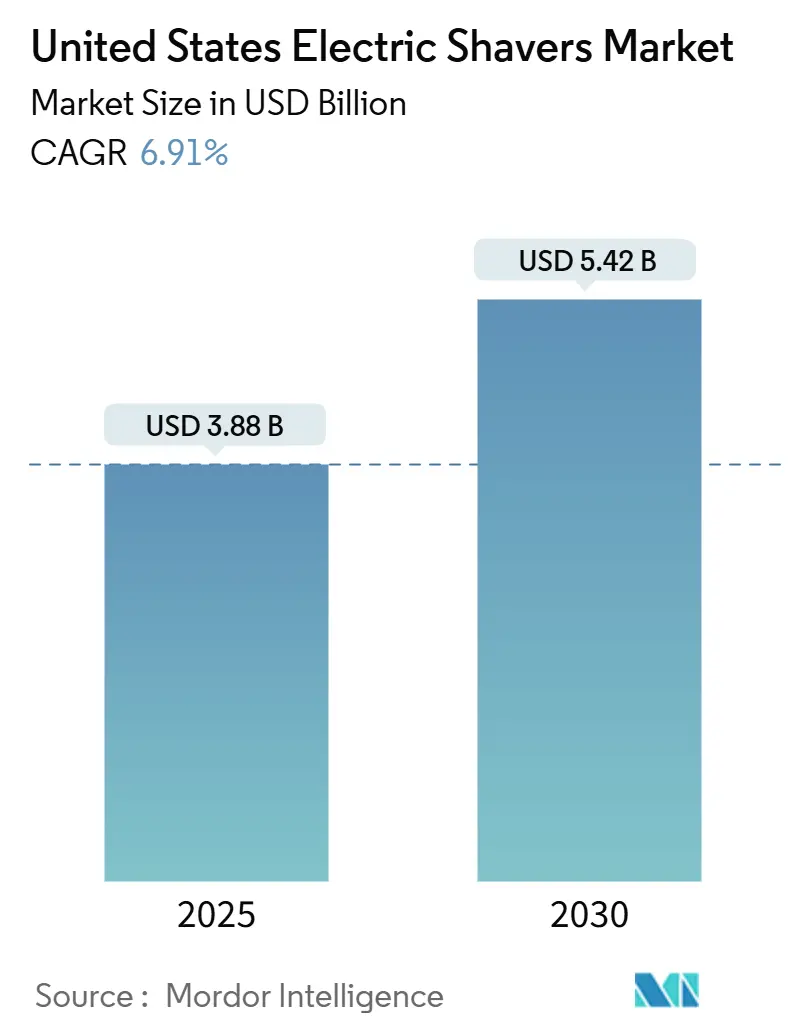

| Market Size (2025) | USD 3.88 Billion |

| Market Size (2030) | USD 5.42 Billion |

| Growth Rate (2025 - 2030) | 6.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Electric Shavers Market Analysis by Mordor Intelligence

The United States electric shavers market size is valued at USD 3.88 billion in 2025 and is projected to reach USD 5.42 billion by 2030, advancing at a 6.91% CAGR over the forecast period. Technological sophistication, particularly the integration of artificial intelligence (AI) and the Internet of Things (IoT), continues to elevate performance, while sustainability mandates and a widening consumer base reinforce demand. Foil models hold the lead because they deliver closer shaves that are perceived as safer for the skin, whereas rotary units grow the fastest as their cutting mechanisms improve comfort. Growing female adoption, premiumization, and direct-to-consumer subscription programs further accelerate the United States electric shavers market, despite inflation-linked down-trading and demographic headwinds. Competitive intensity remains moderate, with the top four brands accounting for approximately half of the total revenue, leaving room for disruptors that can differentiate themselves through smart features, circular economy design, or gender-inclusive messaging.

Key Report Takeaways

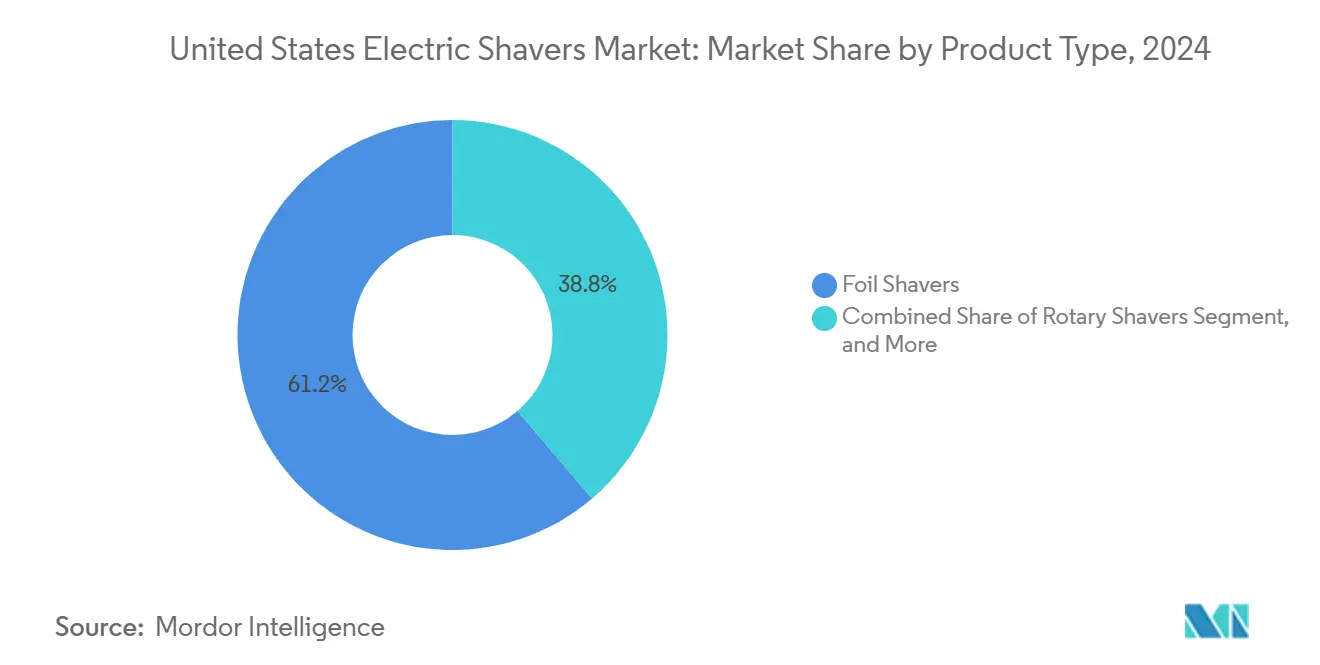

- By product type, foil shavers captured 61.24% of United States electric shavers market share in 2024, while rotary shavers are forecast to expand at a 7.23% CAGR through 2030.

- By end user, men accounted for 86.89% of the United States electric shavers market size in 2024, whereas women will post the highest growth at a 7.39% CAGR by 2030.

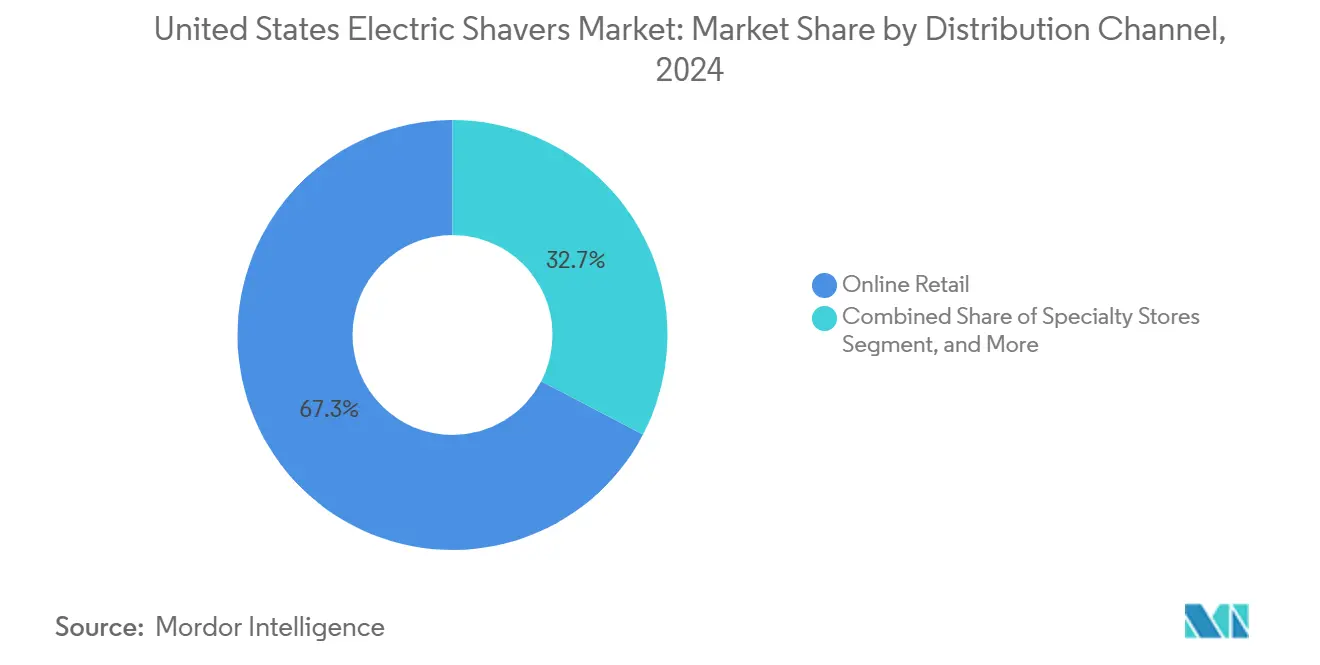

- By distribution channel, online retail commanded 67.34% of revenue in 2024 and is set to grow at a 7.11% CAGR to 2030.

- By price range, the premium segment is projected to rise at the fastest 7.67% CAGR between 2025 and 2030, overtaking mid-range units in value contribution.

United States Electric Shavers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for skin-safe grooming solutions | +1.2% | National, urban clusters | Medium term (2-4 years) |

| Rising penetration of e-commerce-exclusive grooming brands | +1.8% | National; strongest in West and Northeast | Short term (≤ 2 years) |

| Integration of AI and IoT features enabling personalized shaving | +1.5% | National; early adoption in tech-forward regions | Long term (≥ 4 years) |

| Shift toward sustainable, recyclable shaver materials | +0.9% | National; driven by coastal-state regulations | Medium term (2-4 years) |

| Increase in female adoption due to body-positive marketing | +1.1% | National; strongest in urban areas | Medium term (2-4 years) |

| Expansion of subscription-based blade and head-replacement models | +0.6% | National; higher-income segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Skin-Safe Grooming Solutions

Dermatological safety remains a top purchasing criterion as consumers replace manual blades that cause nicks and irritation. Philips’ SkinIQ technology adjusts motor speed in real-time, reducing irritation incidents by 30% compared to conventional electric shavers. [1]Philips, “Shaver 9000 Series with SkinIQ Technology,” philips.com Hypoallergenic foils coated with diamond-like carbon cut friction and extend blade life. Dermatologists increasingly recommend electric shavers to patients with conditions such as pseudofolliculitis barbae, boosting credibility. As a result, electric shaver penetration is increasing in households with sensitive skin, particularly in metropolitan areas where disposable incomes and skincare awareness are more prevalent. These trends materially lift replacement rates and average selling prices in the United States electric shavers market.

Rising Penetration of E-commerce-Exclusive Grooming Brands

Digital-native labels leverage direct-to-consumer (DTC) logistics to bypass retail markups and maintain gross margins 20-30% higher than those of store-shelf incumbents. [2]Drug Store News Staff, “Male Grooming Market Continues to Evolve,” drugstorenews.com Amazon alone accounts for 54% of male grooming spend, creating unprecedented brand visibility and enabling data-driven personalization. Subscription models pioneered by Dollar Shave Club lock in predictable revenue and drive customer lifetime value in the United States electric shavers industry. Incumbents are responding by launching proprietary web shops, but the learning curve around community engagement and rapid product iteration favors agile DTC challengers that can target microsegments, such as women’s body groomers or specialty beard trimmers.

Integration of AI and IoT Features Enabling Personalized Shaving

Smart sensors inside premium units now track stroke speed, applied pressure, and facial-hair density. Collected data synchronizes to companion apps that advise on shave angle, cleaning routines, and replacement timing, enhancing satisfaction and encouraging accessory sales. Machine-learning algorithms learn user patterns, automatically adjusting blade rotations for dense versus sparse zones, which improves closeness and comfort. IoT connectivity further automates reorder cycles for foils, batteries, and lubricants, bolstering subscription revenue in the United States electric shavers market. Voice-assistant compatibility positions shavers as part of a broader connected-bathroom ecosystem sought by tech-savvy consumers.

Shift Toward Sustainable, Recyclable Shaver Materials

Sustainability is a differentiator as regulators tighten e-waste guidelines and consumers demand circular-economy solutions. Panasonic’s take-back program recovers more than 100,000 units annually for recycling, cutting landfill disposal, and capturing valuable cobalt and nickel. [3]Panasonic, “Environmental Initiatives—Sustainability & Citizenship,” panasonic.com Bio-based plastics and recyclable aluminum housings reduce carbon footprints, although they currently carry a 10-15% price premium. Lithium-ion battery disposal rules, especially stringent in California, incentivize modular packs that simplify end-of-life separation. Early-mover brands gain goodwill and a regulatory head start, influencing premium purchase decisions and corporate gift contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stagnating birth rates limiting new male users | -0.8% | National; pronounced in Northeast and Midwest | Long term (≥ 4 years) |

| Regulatory scrutiny on lithium-ion battery disposal | -0.4% | National; stricter in California and Northeast | Medium term (2-4 years) |

| Rebound of barbershop culture reducing at-home grooming time | -0.6% | Urban metros | Short term (≤ 2 years) |

| Inflation-driven down-trading to cheaper manual razors | -1.1% | National; lower-income segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stagnating Birth Rates Limiting New Male Users

U.S. fertility has been below replacement since 2023, reducing the flow of young males entering primary grooming years. The 18-35 cohort, therefore, scales more slowly, constricting volume growth for entry-level electrics. Immigration mitigates losses in coastal cities but does little for mature Midwest markets. An aging population also maintains legacy shaving habits, resisting expensive upgrades. Collectively, these demographic realities shave 0.8 percentage points off the forecast CAGR for the United States electric shavers market.

Inflation-Driven Down-Trading to Cheaper Manual Razors

Battery metals like lithium and nickel have surged 500% and 250% respectively, lifting finished-goods prices well above CPI gains. Cash-strapped households, therefore, switch to manual razors, which are priced 60–70% lower on an annual-use basis. Mid-range electric units (USD 50-150) absorb the biggest hit as consumers either splurge on features-rich premium models with longer lifespans or regress to disposables. Down-trading particularly weakens volume forecasts, even though unit ASPs rise. The resulting demand bifurcation reorients brand portfolios toward high-margin flagships and subscription-based consumables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Foil Technology Dominates Despite Rotary Innovation

Foil shavers generated 61.24% of revenue in 2024, giving them the largest slice of the United States electric shavers market share. Rotary devices, however, will deliver the sharpest 7.23% CAGR, lifting their portion of the United States electric shavers market size as blade architecture innovations erase historical comfort gaps.

Foil’s micro-perforated screens enable precise, close shaves that dermatologists endorse for sensitive skin. Premium foil models add multi-directional flex heads and titanium-nitride coatings to minimize heat. Rotary systems answer with 360-degree contour tracking and lift-and-cut geometries, exemplified by Philips’ MultiPrecision blades that capture flat hairs in a single pass. Hybrid platforms, such as Panasonic’s MultiShape, combine foil and rotary heads into modular form factors, enabling users to switch modes and increase average basket values per device. Clippers, multigroomers, and niche head shavers appeal to multi-purpose shoppers and professional barbers. Yet their collective share remains subordinate because the home-use market still prioritizes clean-shave closeness over versatility.

By End User: Male Dominance Faces Female Market Disruption

Men contributed 86.89% of 2024 revenue, underscoring historical male targeting in the United States electric shavers market. Women’s uptake is expected to accelerate at a 7.39% CAGR, expanding their market share as gender-inclusive advertising and body-positive narratives normalize female electric shaver use.

Billie, now under Edgewell, exemplifies the commercial upside of inclusive branding, having scaled subscription sales with pastel-toned, dermatologically safe shavers priced for female spend tolerances. Manufacturers are increasingly offering interchangeable heads for legs, bikini lines, and underarms, further blurring the lines of gender segmentation. Shared-household devices offer cost advantages but must strike a balance between motor torque calibrated for dense beard hair and low-irritation foils suitable for delicate skin. Regulatory frameworks treat all devices similarly; however, marketing watchdogs are now scrutinizing gender-stereotypical claims, nudging communication strategies toward unisex utility.

By Distribution Channel: Digital Commerce Reshapes Retail Dynamics

Online platforms captured 67.34% of revenue in 2024 and are expected to add a 7.11% CAGR, widening their lead and consolidating purchase journeys for the United States electric shavers industry. Physical supermarkets and hypermarkets still convert impulse buys, but will cede ground as consumers research specifications, watch video reviews, and redeem subscription offers online.

Algorithm-driven recommendations on Amazon and social commerce integrations on Instagram accelerate consideration-to-purchase cycles. Direct-brand webstores exploit zero-party data to personalize bundles, upsell accessories, and automate replenishment. Pharmacies retain a last-minute advantage for replacement foils and mobile chargers, but they carry a limited number of SKUs. Specialty grooming outlets face rent pressure unless they pivot to experiential services, such as in-store blade-care clinics or barber-led tutorials, that justify premium pricing.

By Price Range: Premium Segment Drives Value Migration

Mid-range shavers accounted for 45.78% of the 2024 value, but premium units are expected to command the highest 7.67% CAGR, further intensifying their grip on the United States electric shavers market size. Consumers seeking longevity and smart capabilities rationalize upfront outlays for units that deliver five-year motor warranties, wireless Qi charging, and AI-driven shaving analytics.

Economy tiers struggle under material cost inflation and eroding differentiation versus manual blades. Private-label lines may fill entry-level gaps, but warranty concerns and subpar battery life threaten user satisfaction. Brands thus lean on premiumization as diamond-like carbon coatings, waterproof IPX7 housings, and app ecosystems increase ticket sizes and defend against commoditization, offsetting volume softness from down-trading.

Geography Analysis

Southern states generated 34.67% of 2024 revenue as young, rapidly growing metro areas such as Dallas, Houston, and Charlotte added new grooming consumers. Population gains and higher disposable incomes among millennial and Gen Z cohorts underpin resilient replacement cycles for mid-range foil shavers. Retail partnerships with regional supermarket chains reinforce brand visibility, while local influencer campaigns accelerate the adoption of premium beard-trimming kits.

The West posts the fastest 7.32% CAGR through 2030, increasing its contribution to the United States electric shavers market share as tech-savvy professionals adopt AI-enabled grooming. California’s strict e-waste rules encourage brands to pilot recyclable housings and swappable battery packs, setting precedents for national rollouts. Higher household incomes in Seattle, San Francisco, and Denver support premium price points above USD 200, driving an expansion of blended ASP.

The Northeast offers steady, high-value demand centered on dense urban corridors. Subscription penetration is highest in New York and Boston, where on-demand logistics allow 24-hour full-head delivery. Nevertheless, aging demographics moderate unit volumes. In contrast, the Midwest lags, restrained by slower economic growth and cultural loyalty to manual shaving. Domestic production potential remains a bright spot: brands signaling “Made in USA” provenance tap into regional pride and mitigate logistics risk exposed during 2024-2025 supply disruptions.

Competitive Landscape

The top four manufacturers-Philips, Braun, Panasonic, and Wahl-collectively hold roughly 50% of the United States electric shaver market share, indicating moderate concentration. Their scale ensures access to R&D resources for patenting AI algorithms, low-friction foils, and modular battery systems. However, DTC insurgents like Manscaped and Meridian Grooming carve out niches through humor-driven marketing and social media virality, winning over younger cohorts who are unconvinced by legacy brand prestige.

Strategically, incumbents are converging hardware with software ecosystems. Philips pairs SkinIQ sensors with a proprietary grooming app that prescribes personalized routines and sells consumables. Panasonic emphasizes circular-economy credentials via national take-back programs that reclaim motors and nickel for reuse, satisfying environmentally minded millennials. Edgewell’s acquisition spree-USD 1.37 billion for Harry’s and USD 310 million for Billie-illustrates how heritage firms can secure DTC expertise and female demographics without the time-consuming organic build.

Barriers to entry now pivot on regulatory compliance and software talent rather than purely manufacturing scale. Lithium-ion battery disposal rules require traceable supply chains, which adds documentation overhead that small importers may not be able to bear. Conversely, niche opportunities still abound: smart head shavers for bald consumers, barber-grade trimmers engineered for continuous duty, and eco-friendly travel shavers for sustainability-conscious tourists.

United States Electric Shavers Industry Leaders

Koninklijke Philips N.V.

Panasonic Holdings Corporation

Braun GmbH

Wahl Clipper Corporation

Andis Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Wahl launched the PRO SERIES High Visibility Trimmer with diamond-hard coatings priced at USD 149.99

- February 2025: Philips introduced the Shaver 9000 with SkinIQ adaptive sensing, cutting irritation by 30%

- January 2025: Panasonic added MultiShape modular heads to its ARC line, blending rotary and linear modes

- December 2024: Edgewell completed its USD 310 million acquisition of Billie to deepen female DTC channels

United States Electric Shavers Market Report Scope

| Foil Shavers |

| Rotary Shavers |

| Clippers and Multigroomers |

| Other Product Types |

| Men |

| Women |

| Unisex / Shared Devices |

| Online Retail |

| Supermarkets and Hypermarkets |

| Specialty Stores |

| Pharmacies and Drugstores |

| Other Distribution Channels |

| Economy |

| Mid-Range |

| Premium |

| By Product Type | Foil Shavers |

| Rotary Shavers | |

| Clippers and Multigroomers | |

| Other Product Types | |

| By End User | Men |

| Women | |

| Unisex / Shared Devices | |

| By Distribution Channel | Online Retail |

| Supermarkets and Hypermarkets | |

| Specialty Stores | |

| Pharmacies and Drugstores | |

| Other Distribution Channels | |

| By Price Range | Economy |

| Mid-Range | |

| Premium |

Key Questions Answered in the Report

How large is the United States electric shaver sector in 2025?

It is valued at USD 3.88 billion, with a 6.91% CAGR forecast to 2030.

Which product format grows fastest through 2030?

Rotary shavers will record a 7.23% CAGR as blade-head designs improve user comfort.

What share do online channels hold?

Digital commerce accounts for 67.34% of 2024 revenue and will expand further due to DTC brands and subscriptions.

Why are women driving new demand?

Body-positive marketing and female-specific designs push women’s adoption at a 7.39% CAGR, the highest among end users.

How are regulations shaping product design?

Stricter e-waste and battery-disposal rules, especially in California, accelerate the shift to recyclable housings and modular batteries.

Which U.S. region shows strongest growth potential?

The West leads with a projected 7.32% CAGR thanks to higher incomes and early adoption of AI-enabled grooming technology.

Page last updated on: