Europe Electric Vehicle Lamination Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

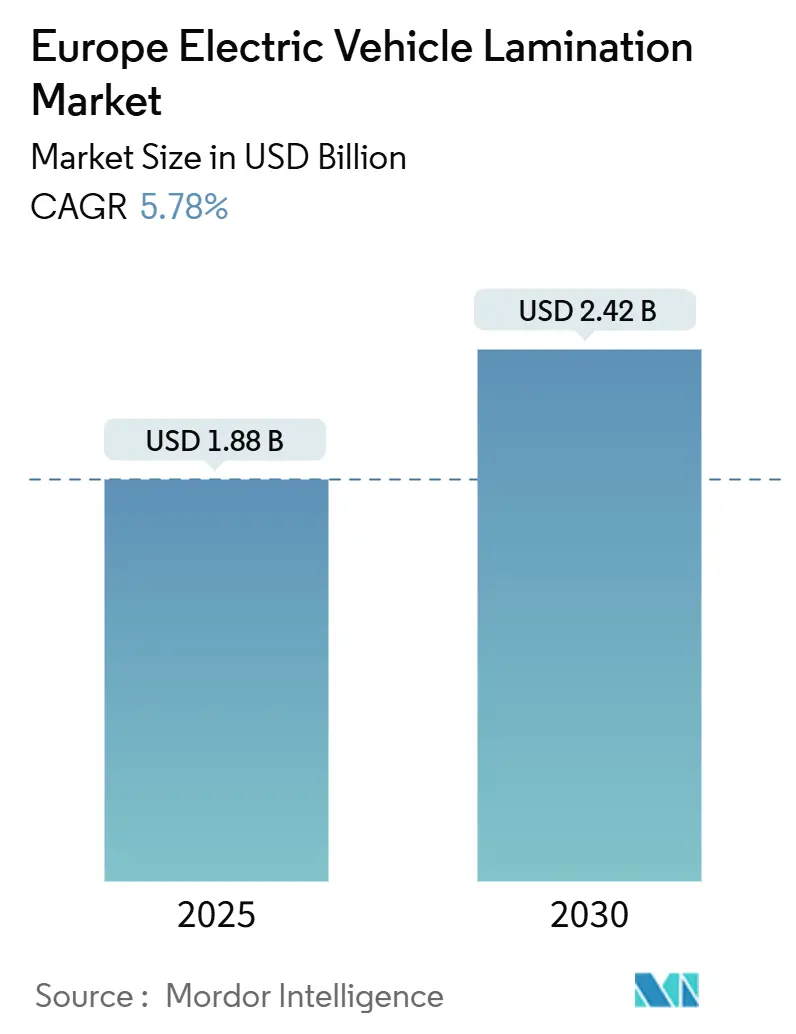

| Market Size (2025) | USD 1.88 Billion |

| Market Size (2030) | USD 2.42 Billion |

| Growth Rate (2025 - 2030) | 5.78% CAGR |

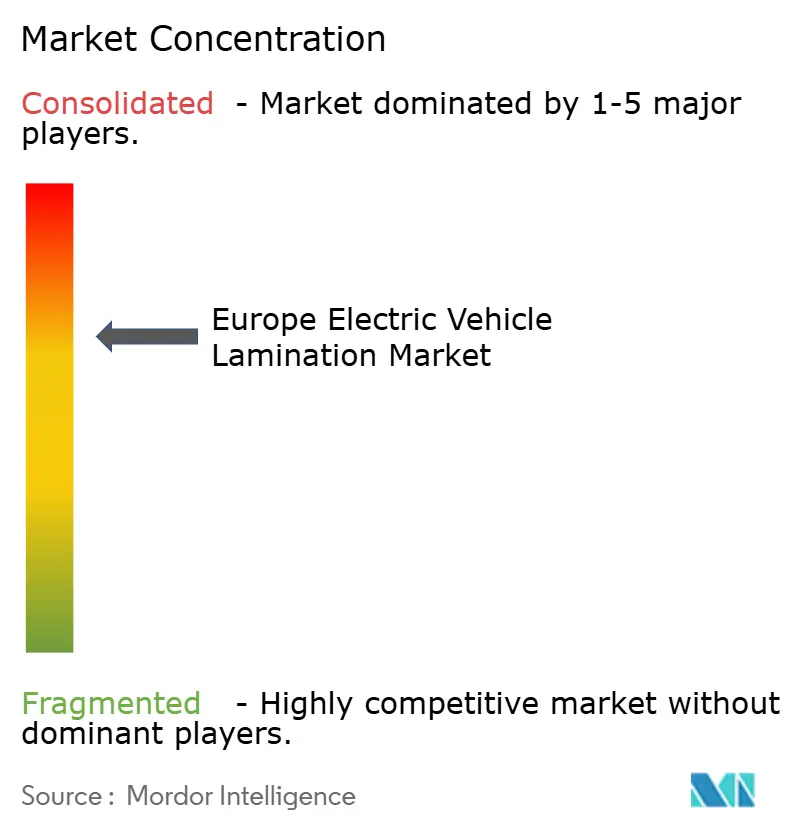

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Electric Vehicle Lamination Market Analysis by Mordor Intelligence

The European electric vehicle lamination market reached USD 1.88 billion in 2025 and is projected to reach USD 2.42 billion by 2030, registering a 5.78% CAGR over the forecast period. The measured growth stems from strict EU carbon-reduction rules, automaker localization programs, and rapid migration toward ultra-thin electrical-steel grades that curb core losses and raise motor efficiency above 95%. Vertically integrated steel makers are boosting regional capacity, yet raw-material volatility and the capital intensity of progressive-die stamping continue to pressure margins. Germany anchors demand through its automotive cluster, while Spain benefits from low-cost renewable power for energy-intensive lamination processing. Technology advances such as 6.5% Si-Fe laminations and axial-flux motor designs open efficiency pathways yet disrupt traditional supply-volume assumptions.

Key Report Takeaways

- By laminates type, Electrical Steel held 68.12% of the European electric vehicle lamination market share in 2024, whereas 0.23 mm silicon-steel grades are forecast to grow at 14.10% CAGR through 2030.

- By motor type, PMSM dominated with a 46.23% share in 2024; SRM is poised to expand at an 18.30% CAGR to 2030.

- By vehicle type, passenger cars commanded a 72.45% share of the European electric vehicle lamination market size in 2024, while two-wheelers are advancing at a 22.50% CAGR through 2030.

- By application, stator laminations accounted for 61.04% share in 2024 and rotor laminations are growing at 15.40% CAGR to 2030.

- By geography, Germany led with 29.31% share in 2024; Spain records the fastest regional CAGR at 13.20% for 2025-2030.

Europe Electric Vehicle Lamination Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EU Electric-Vehicle Production Targets | +1.2% | Germany, France, Spain, Netherlands | Medium Term (2–4 Years) |

| Tightening Motor-Efficiency Regulations (Ecodesign ENER Lot 1) | +0.9% | EU-Wide; Strongest in Germany, France | Short Term (≤ 2 Years) |

| OEM Localization of Motor-Core Supply Chains | +0.8% | Germany, Poland, Czech Republic | Medium Term (2–4 Years) |

| Cost-Down Pressure Favoring High-Yield Stamping Technologies | +0.6% | Germany, Italy, Spain | Long Term (≥ 4 Years) |

| Rapid Shift Toward Si-Fe 6.5% Laminations for High-Speed E-Axles | +0.7% | Germany, France, Netherlands | Short Term (≤ 2 Years) |

| Recycling-Friendly Lamination Architectures | +0.4% | EU-Wide; Led by Germany, Netherlands | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Surging EU Electric-Vehicle Production Targets

The Fit-for-55 legislative package compels automakers to lower fleet CO₂ by 55% before 2030, pushing assembly plants to retool for full-battery platforms that use up to four times more lamination per vehicle than mild-hybrid lines[1]"European Green Deal: Commission proposes transformation of EU economy and society to meet climate ambitions," European Commission, ec.europa.eu.. Mercedes-Benz earmarked EUR 40 billion for EV manufacturing, while Volkswagen allocates EUR 52 billion, moves that tighten demand for thin-gauge cores able to support high-rpm e-axles. Supplier contracts now run five years or longer to avoid material shortfalls. As schedules compress, steel makers commit to just-in-time agreements that encourage co-located stamping shops inside power-train campuses. These capacity pacts lock in volumes and limit spot-market volatility, reshaping how the Europe electric vehicle lamination market balances risk and growth.

Tightening Motor-Efficiency Regulations

The ENER Lot 1 rule set raises minimum IE3-plus thresholds for 50 Hz motors between 0.12 kW and 1,000 kW, nudging OEMs toward sub-0.23 mm steels that cut eddy-current losses by up to 25%. Compliance adds EUR 50–80 per motor but lowers lifetime electricity costs enough to achieve payback within two years. Certification under IEC 60034-30-1 favours suppliers with robust test labs, further consolidating the playing field. Small fabricators struggle to fund the metrology upgrades that EU accreditation auditors now inspect annually. As a result, the Europe electric vehicle lamination market sees rising premium for proven quality stamps.

OEM Localization of Motor-Core Supply Chains

BMW plans to source majority of its laminations from European sites by 2026, citing geopolitical risk and freight savings. Stellantis opened procurement hubs in Turin and Rüsselsheim that tender regional suppliers on a three-month cadence, increasing transparency but compressing margins. POSCO’s new Polish plant delivers two million motor cores yearly, cutting lead times into central-European vehicle plants to under five days. The localisation drive tightens the European electric vehicle lamination market by shifting Asian capacity onshore, spurring further brownfield expansions. Fabrication veterans upgrade ERP and quality-control systems to synchronize with OEM digital twins for end-to-end traceability.

Cost-Down Pressure Favoring High-Yield Stamping Technologies

Progressive-die lines reach 85% material yield compared to 70% for legacy presses, saving up to 280 kg of silicon steel for every 1,000 motors produced. Italian-built servo presses add closed-loop thickness sensing to keep tolerance within 2 µm, slashing scrap. Although each line costs EUR 2-5 million, payback arrives in under 18 months amid volatile metal prices. Worthington’s EUR 180 million purchase of Sitem Group brought proprietary die-lubrication tech that improves punch-life by 20% and raises uptime across its eight European plants. Such gains preserve supplier margins even as automakers request annual 2-3% price concessions, cementing high-yield tooling as a must-have capability in the European electric vehicle lamination market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Volatility of High-Grade Electrical Steel | –0.8% | EU-Wide; Acute in Germany, France | Short Term (≤ 2 Years) |

| Capital-Intensive Progressive-Die Investments | –0.6% | Germany, Italy, Czech Republic | Medium Term (2–4 Years) |

| Limited Coating Options for Ultra-Thin Laminations | –0.4% | Germany, Netherlands, France | Medium Term (2–4 Years) |

| Emerging Axial-Flux Motor Designs That Need Fewer Laminations | –0.5% | UK, Germany, Netherlands | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Supply Volatility of High-Grade Electrical Steel

EUROFER notes that only four regional mills currently melt the highest-quality Si-Fe, making the market vulnerable to outages and energy-price swings that can vary costs by 20% quarter-to-quarter. With Chinese export quotas tightening, buyers hedge with dual-sourcing yet still face occasional allocation cuts. Automakers lock annual price-down clauses, so lamination suppliers absorb sudden spikes. These shocks depress margin growth within the Europe electric vehicle lamination market and slow expansion plans until more capacity comes online.

Capital-Intensive Progressive-Die Investments

A single die set tailored to one traction-motor design can cost EUR 700,000, and new high-speed presses push project outlays beyond EUR 5 million. Smaller shops hesitate without multi-year volume guarantees. With model cycles shortening, ROI risk rises because redesigned rotors often require entirely new tool stacks. Financing hurdles stall greenfield projects and keep market power with cash-rich conglomerates, limiting the overall CAGR of the Europe electric vehicle lamination market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laminates Type: Electrical Steel Dominance Drives Efficiency

Electrical steel laminates captured 68.12% of the European electric vehicle lamination market share in 2024, anchored by mature supply chains and well-established magnetic properties. Silicon-steel 0.23 mm grades are projected to post a 14.10% CAGR to 2030 as high-speed e-axles proliferate. In value terms, the European electric vehicle lamination market size for this sub-segment is forecast to climb from USD 1.28 billion in 2025 to more than USD 1.7 billion by 2030. Integrated mills are coupling metallurgical tweaks with laser-textured coatings to lower core losses by another 8%.

ArcelorMittal's iCARe product range demonstrates the technological evolution within electrical steel grades, incorporating advanced coating systems and metallurgical refinements that support recycling-friendly architectures[2]"iCARe®: ArcelorMittal’s range of electrical steels for automotive," ArcelorMittal, automotive.arcelormittal.com.. The segment benefits from established supply relationships and proven performance characteristics that reduce qualification risks for automotive applications. However, raw material dependencies and energy-intensive production processes create cost volatility that manufacturers must navigate through long-term supply agreements and operational efficiency improvements. ISO 14001 environmental management standards increasingly influence material selection decisions as OEMs prioritize sustainable supply chain practices.

By Motor Type: PMSM Leadership Faces SRM Challenge

PMSM retained 46.23 of % European electric vehicle lamination market share in 2024, due to its efficiency and torque characteristics prized in premium vehicles. However, SRM is accelerating at 18.30% CAGR because it avoids rare-earth magnets whose prices swung 40–60% in 2024 alone. The European electric vehicle lamination market size linked to SRM is set to double by 2030, creating upside for fabricators able to stamp thicker, tooth-rich stator designs.

Induction motors stay relevant in commercial vans where robustness trumps peak efficiency. BLDC holds pockets in micro-mobility requiring compact packages. The shift forces toolmakers to build modular dies that switch between slot geometries overnight. Suppliers with multi-motor portfolios cushion utilization dips and capture cross-segment synergies, reinforcing the moderate concentration profile of the European electric vehicle lamination industry.

By Vehicle Type: Two-Wheeler Electrification Accelerates

Passenger cars drove 72.45% of 2024 revenue on sheer volume, but two-wheelers now clock a 22.50% CAGR as cities ban combustion scooters in low-emission zones. The European electric vehicle lamination market size tied to two-wheelers could quadruple by 2030, powered by shared e-moped fleets and subsidy vouchers. Rotor cores in bikes weigh under 800 g yet still demand sub-0.3% core-loss performance, driving interest in nano-crystalline steels despite price premiums.

Commercial-vehicle uptake remains steady as logistics firms count long-term fuel savings. Geofencing rules in France and Germany earmark downtown delivery zones for zero-emission vans, adding a predictable demand stream. Variants with integrated drives and in-wheel motors widen lamination formats, requiring quick-change die shoes. This diversity underpins steady capacity utilization in the European electric vehicle lamination market.

By Application: Stator-Rotor Balance Shifts

Stator laminations delivered 61.04% of 2024 sales, yet rotor laminations will grow 15.40% CAGR through 2030 as permanent-magnet flux levels climb and skewed-slot geometries proliferate. The European electric vehicle lamination market size for rotor parts is forecast to reach just under USD 1 billion by 2030. Thicker back irons and complex hub notches lift tonnage per unit, balancing shrinking stator stacks enabled by high-frequency drives.

Precision increases especially on outer diameter concentricity, pushing the adoption of servo-presses with on-board vision metrology. Co-molded rotors that lock magnets via epoxy fill are emerging, trimming assembly time but tightening oven-bake windows. Suppliers adding post-processing like skewing and shaft assembly secure higher margins and de-risk reliance on raw stamping alone in the European electric vehicle lamination market.

Geography Analysis

Germany controlled 29.31% of 2024 revenue. The country's dominance reflects established supply relationships between major automakers (BMW, Mercedes-Benz, Volkswagen) and integrated steel producers, creating competitive advantages through proximity and technical collaboration. Thyssenkrupp's EUR 300 million investment in Bochum specifically targets 0.2mm electrical steel production, demonstrating a commitment to advanced lamination technologies[3]"Investment in the future for electric mobility: thyssenkrupp takes a new high-tech annealing and isolating line into operation in Bochum," thyssenkrupp, thyssenkrupp-steel.com..

Spain registers the fastest growth at 13.20% CAGR as new battery gigafactories secure cheap solar power, cutting lamination annealing costs by up to 18% versus northern Europe. OEMs widen Iberian sourcing to earn Scope 3 emission credits tied to renewable electricity. The Netherlands and the UK specialize in R&D prototypes and axial-flux discs, exporting stamped stacks across EU borders tariff-free under Rules-of-Origin clauses.

Poland and the Czech Republic emerge as cost-competitive hubs after POSCO and Mitsui built core factories near existing wire-harness plants. Access to skilled toolmakers and EU structural funds lowers capex hurdles. As energy grids decarbonize, regional advantages will pivot toward logistics proximity and digital-passport compliance, reshaping capacity placement in the Europe electric vehicle lamination market.

Competitive Landscape

The European electric vehicle lamination market remains moderately consolidated; the top five players account for a major chunk of the revenue. Integrated steel producers like ThyssenKrupp, ArcelorMittal, and POSCO lock in upstream metal supply while owning progressive-die assets, safeguarding margins during price swings. Specialist fabricators such as EuroGroup Laminations and Worthington Industries differentiate through servo-press uptime, intricate skewing, and quick-change tooling.

Strategic moves in 2024-2025 reinforce localization. ThyssenKrupp added 200,000 t capacity in Germany; POSCO launched a two-million-unit core plant in Poland; Worthington acquired Sitem to secure the know-how across eight EU factories. Joint R&D centers with OEMs iterate rotor laminations for axial-flux discs, pushing tolerances below 5 µm without secondary grinding. Smaller shops survive by servicing two-wheeler and niche aerospace lines with low batch sizes.

Price competition focuses on yield. Plants boasting more than 85% material utilization win multiyear contracts even if press-hour rates run higher, reflecting OEM emphasis on embodied-carbon metrics. Digital passports under the EU Battery Regulation favor ISO 14001-certified mills like Metglas and Aperam, adding compliance weight to customer audits. Over the next five years, tooling investment cadence will decide share shifts as EV platforms migrate to higher switching frequencies and thinner steels, demanding constant capex reinvention.

Europe Electric Vehicle Lamination Industry Leaders

-

EuroGroup Laminations S.p.A.

-

voestalpine AG

-

Tata Steel Europe (Cogent Power)

-

Thyssenkrupp AG

-

Aperam S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Arnold Magnetic Technologies launched Arnon Non Grain Oriented Electrical Steel in 0.004" (0.102mm) thickness, achieving core loss reductions up to 50% versus conventional grades for high-frequency motor applications exceeding 1 kHz switching frequencies.

- December 2024: Worthington Industries acquired controlling stake (52%) in Sitem Group for EUR 180 million (USD 195 million), consolidating progressive die stamping expertise and expanding European lamination manufacturing capabilities across 8 production facilities.

Europe Electric Vehicle Lamination Market Report Scope

| Electrical Steel Laminates |

| Silicon Steel Laminates |

| Other Laminates Types (Nickel-iron Laminates, Cobalt-iron Laminates, etc.) |

| Permanent Magnet Synchronous Motors (PMSM) |

| Induction Motors |

| Switch Reluctance Motors (SRM) |

| Brushless DC Motors (BLDC) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-wheelers |

| Stator Laminations |

| Rotor Laminations |

| Germany |

| United Kingdom |

| Spain |

| Italy |

| France |

| Netherlands |

| Rest of Europe |

| By Laminates Type | Electrical Steel Laminates |

| Silicon Steel Laminates | |

| Other Laminates Types (Nickel-iron Laminates, Cobalt-iron Laminates, etc.) | |

| By Motor Type | Permanent Magnet Synchronous Motors (PMSM) |

| Induction Motors | |

| Switch Reluctance Motors (SRM) | |

| Brushless DC Motors (BLDC) | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| Two-wheelers | |

| By Application | Stator Laminations |

| Rotor Laminations | |

| By Country | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe electric vehicle lamination market in 2025?

It stands at USD 1.88 billion and is projected to grow at 5.78% CAGR to reach USD 2.42 billion by 2030.

Which country leads regional demand?

Germany controls 29.31% of revenue thanks to its dense automotive cluster and new 0.2 mm electrical-steel capacity.

What is the fastest-growing motor type used by EV makers?

Switch reluctance motors are expanding at an 18.30% CAGR due to rare-earth independence and cost advantages.

Why are 0.23 mm silicon-steel laminations important?

They cut eddy-current losses, enabling motor efficiencies above 95% in high-speed e-axle designs.

How will EU regulations affect lamination sourcing?

Fit-for-55 and Ecodesign rules drive localisation and demand for ultra-thin, recyclable laminations, reshaping supplier networks.

What restrains capacity expansion most?

The multi-million-euro cost of progressive-die presses and tooling discourages smaller entrants from scaling production.

Page last updated on: