Market Overview

| Study Period | 2017 - 2029 |

|---|---|

| Forecast Data Period | 2025 - 2029 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 109.5 Billion |

| Market Size (2029) | USD 211.3 Billion |

| Growth Rate (2025 - 2029) | 17.86% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Electric Car Market Analysis by Mordor Intelligence

The United States Electric Car Market size is estimated at 109.5 billion USD in 2025, and is expected to reach 211.3 billion USD by 2029, growing at a CAGR of 17.86% during the forecast period (2025-2029).

The U.S. electric vehicle market is experiencing unprecedented transformation through strategic manufacturing investments and technological innovations. Major automakers are establishing robust domestic production capabilities, with industry leaders like Tesla and Toyota demonstrating significant manufacturing prowess, producing 321,742 units and 457,400 units respectively in 2022. Companies are increasingly focusing on vertical integration, with several manufacturers announcing plans to establish domestic battery production facilities. For instance, in February 2023, Ford became the first automaker to commit to manufacturing both nickel cobalt manganese (NCM) and lithium iron phosphate (LFP) batteries within the United States, aiming to enhance accessibility and diversify the supply chain.

The industry's technological landscape continues to evolve rapidly, particularly in battery technology and charging infrastructure. The sector has witnessed a remarkable 80% decline in lithium-ion battery prices since 2010, making electric vehicles increasingly cost-competitive with traditional combustion engine vehicles. This advancement is complemented by the expansion of charging infrastructure, with the number of publicly available charging stations surpassing 100,000 in 2022. The industry is also seeing innovations in fast-charging technology, with several manufacturers introducing vehicles capable of rapid charging capabilities, significantly reducing charging times and enhancing consumer convenience.

Strategic partnerships and collaborations are reshaping the competitive landscape of the U.S. electric vehicle industry. In June 2023, Ford Next introduced a pioneering pilot program targeting Uber drivers in select markets, offering flexible electric vehicle leasing options. Similarly, automotive manufacturers are forming alliances with technology companies to enhance their vehicles' capabilities. For instance, in December 2022, BMW Group partnered with Airconsole to integrate casual gaming features into their vehicles through curved screens, demonstrating the industry's move toward enhanced in-vehicle entertainment experiences.

The industry is witnessing a significant shift in manufacturing and supply chain strategies, with a strong focus on localizing production and securing critical components. Major manufacturers are investing heavily in domestic production facilities, with companies like Stellantis and Samsung SDI announcing plans to construct lithium-ion battery manufacturing facilities. In May 2023, BMW launched its fully electric BMW 5 Series, showcasing the industry's commitment to expanding electric vehicle offerings across various vehicle segments. These developments are accompanied by innovations in vehicle design and functionality, with manufacturers introducing features like automated parking systems and enhanced driver assistance capabilities. The growth of the electric vehicle market is further driven by these advancements, indicating a robust forecast for the electric vehicle market.

United States Electric Car Market Trends and Insights

Rapid growth in electric vehicle sales driven by government initiatives and increasing demand in the US

- The United States has witnessed a significant surge in the adoption of electric vehicles (EVs) in recent years. This uptick can be attributed to a heightened awareness of EVs, growing environmental concerns, and the implementation of government regulations. Notably, in 2016, California introduced the Zero-Emission Vehicle (ZEV) program aimed at curbing carbon emissions and improving air quality. This initiative has not only spurred the growth of electric cars within California but has also influenced other states to adopt similar ZEV regulations. Consequently, the nation saw a remarkable 634% surge in demand for battery electric vehicles (BEVs) from 2017 to 2022.

- The demand for electric commercial vehicles in the United States is also on the rise. Factors such as the booming e-commerce industry, increased logistics activities, and governmental initiatives for cleaner transportation have fueled this growth. In a significant move, the governor of New York signed the Advanced Clean Truck (ACT) Rule in September 2021. This rule sets a target for all new light-duty vehicles to be zero-emission by 2035 and the same for medium- and heavy-duty vehicles by 2045. As a result, the United States witnessed a 21% surge in demand for electric commercial vehicles in 2022 compared to the previous year.

- Governmental efforts, including rebates, subsidies, and strategic plans, are further bolstering the electrification of vehicles nationwide. In May 2022, President Biden unveiled a USD 3 billion plan to expedite domestic battery manufacturing, with the aim of transitioning gas-powered vehicles to electric ones. This push is expected to significantly boost electric mobility in the country, particularly during 2024-2030, thereby amplifying the demand for battery packs.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The US population continues to grow steadily, driven by immigration and economic opportunities that require strategic planning

- The CVP is expected to experience consistent growth, driven by technological advancements, a focus on sustainable transportation, and the US's commitment to automotive innovation and reducing carbon emissions

- The recent US auto interest rate of 3.6% reflects fluctuations influenced by monetary policies, credit demand, and economic conditions, with a modest increase indicating optimism in the post-pandemic recovery

- The United States achieved a milestone of 128,000 EV Charging Stations in 2022, and the country is poised for continued growth in green mobility

- Rising demand and strategic product launches drive the electric vehicle market in the US.

- The United States remained a net crude oil importer in 2022, importing about 6.28 million bpd of crude oil from 80 countries

- The US exhibits remarkable economic resilience and growth, driven by factors like robust financial markets, technological advancements, and adaptable policies

- The United States grapples with fluctuating inflation but aims for stability for long-term economic leadership

- Evolution of Mobility as a Service (MaaS) in the United States: a focus on shared rides, car rentals, car-sharing, and ride-hailing and taxi services

- Decreasing battery pack prices and government initiatives drive the US electric vehicle market

- The recovery of the US used car sales market can be attributed to several factors, including the economic revival after the challenges of 2020 and the increasing consumer preference for used cars due to their cost-effectiveness

- From 2017 to 2022, North America, especially the US, witnessed a shift in hybrid and electric vehicle production, with Tesla and Toyota seeing significant growth

Segment Analysis: Vehicle Configuration

SUV Segment in US Electric Car Market

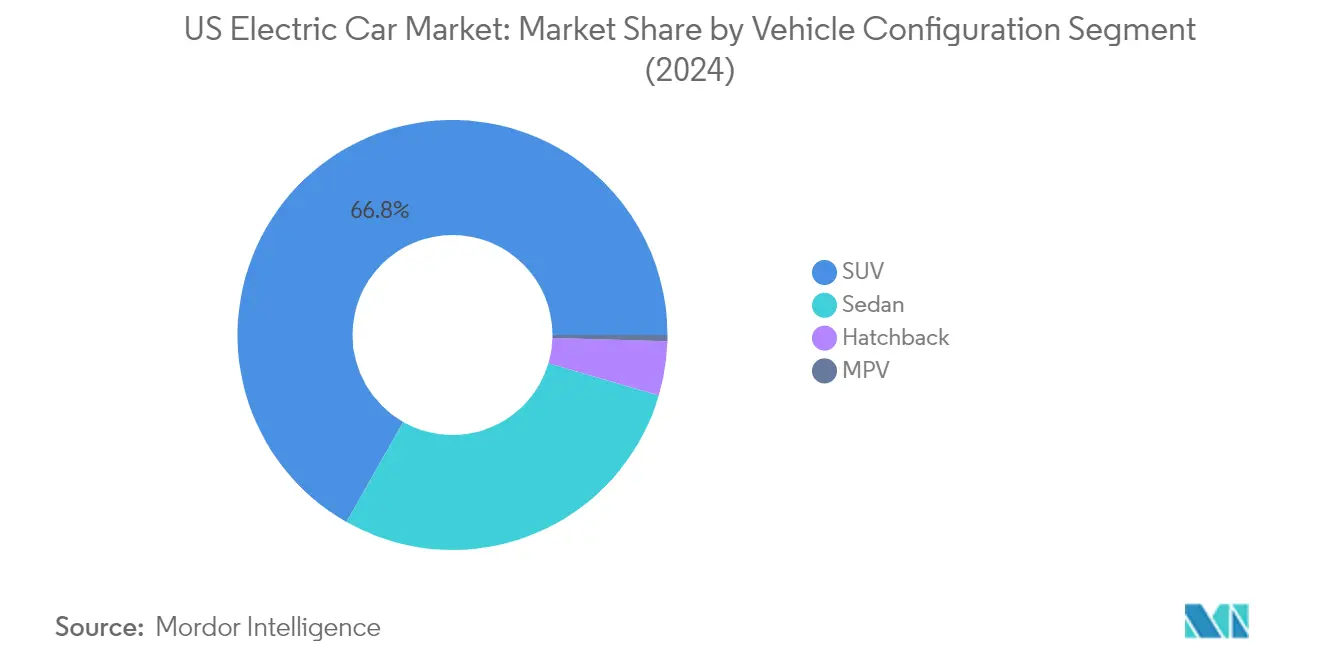

Sport Utility Vehicles (SUVs) have emerged as the dominant force in the US electric car market, commanding approximately 67% market share in 2024. This substantial market position is driven by several key factors, including the growing consumer preference for vehicles that offer both space and versatility. The segment's success is further bolstered by the introduction of new electric SUV models from various manufacturers, offering consumers a wide range of options across different price points. The increasing availability of charging infrastructure and improvements in battery technology have made electric SUVs more practical for everyday use, while government incentives and environmental regulations continue to favor the adoption of electric vehicles in this category.

MPV Segment in US Electric Car Market

The Multi-Purpose Vehicle (MPV) segment is demonstrating remarkable growth potential in the US electric car market, with a projected growth rate of approximately 19% during 2024-2029. This accelerated growth is attributed to the increasing demand for versatile family vehicles that combine the benefits of electric propulsion with practical space utilization. Manufacturers are responding to this trend by introducing new electric MPV models with advanced features, improved range capabilities, and enhanced charging technologies. The segment's growth is further supported by the rising awareness of environmental sustainability among family-oriented consumers and the expanding charging infrastructure across urban and suburban areas.

Remaining Segments in Vehicle Configuration

The electric sedan and hatchback segments continue to play vital roles in the US electric car market, each catering to distinct consumer preferences and needs. Electric sedans maintain their appeal among business professionals and luxury vehicle buyers, offering a perfect balance of performance, comfort, and efficiency. The hatchback segment serves urban dwellers and first-time electric vehicle buyers, providing practical solutions for city driving with their compact size and maneuverability. Both segments are experiencing continuous innovation in terms of design, technology integration, and performance capabilities, contributing to the overall diversity of the electric vehicle segments.

Segment Analysis: Fuel Category

BEV Segment in US Electric Car Market

Battery Electric Vehicles (BEVs) have emerged as the dominant force in the US electric car market, commanding approximately 48% market share in 2024. This leadership position can be attributed to several factors, including significant advancements in battery technology, expanded charging infrastructure networks, and enhanced vehicle ranges that now compete effectively with conventional vehicles. Major automakers have substantially invested in BEV production capabilities, with companies like Tesla, Ford, and General Motors expanding their all-electric vehicle lineups. The segment's growth is further supported by federal and state-level incentives, including tax credits of up to $7,500 for qualifying vehicles, making BEVs increasingly attractive to American consumers. Additionally, the declining battery costs and improving charging infrastructure have addressed key consumer concerns about range anxiety and initial purchase costs.

FCEV Segment in US Electric Car Market

The Fuel Cell Electric Vehicle (FCEV) segment is demonstrating remarkable growth potential in the US electric car market, with projections indicating an impressive growth rate of approximately 34% during 2024-2029. This accelerated growth is driven by significant investments in hydrogen infrastructure development and increasing recognition of FCEVs' advantages, particularly their quick refueling times and longer operating ranges. Major automotive manufacturers are expanding their FCEV offerings, while government initiatives supporting hydrogen infrastructure development are creating a more conducive environment for FCEV adoption. The segment is particularly gaining traction in regions with established hydrogen refueling networks, notably in California, where strategic investments in infrastructure development are paving the way for wider FCEV adoption.

Remaining Segments in Fuel Category

The remaining segments in the US electric car market consist of Hybrid Electric Vehicles (HEV) and Plug-in Hybrid Electric Vehicles (PHEV), both playing crucial roles in the transition to cleaner mobility solutions. HEVs continue to serve as an important bridge technology, offering improved fuel efficiency without the range anxiety associated with pure electric vehicles. PHEVs provide a versatile solution by combining the benefits of both electric and conventional powertrains, making them particularly attractive to consumers who want the flexibility of both technologies. These segments are supported by established manufacturing capabilities and growing consumer acceptance, particularly among buyers who seek reduced environmental impact while maintaining the familiarity of traditional vehicle operation.

Competitive Landscape

Top Companies in United States Electric Car Market

The US electric car market is dominated by established players like Tesla, Toyota, Honda, Hyundai, Ford, and BMW, who are actively shaping the industry through continuous innovation and strategic initiatives. These companies are investing heavily in research and development to enhance battery technology, improve charging infrastructure, and develop advanced driver assistance systems. Manufacturing facilities are being expanded and modernized across multiple states to increase production capacity and meet growing demand. Strategic partnerships with technology companies and battery manufacturers are becoming increasingly common to accelerate innovation and secure supply chains. Companies are also focusing on developing comprehensive product portfolios that span different vehicle segments and price points, while simultaneously investing in charging networks and customer service infrastructure to enhance the ownership experience. This dynamic landscape is reflected in the EV market share by company, highlighting the competitive positioning of these major players.

Market Consolidation Drives Industry Evolution Pattern

The US electric car market exhibits a high degree of consolidation, with a mix of global automotive giants and specialized electric vehicle manufacturers competing for market share. Traditional automakers are leveraging their established manufacturing capabilities, extensive dealer networks, and brand recognition to transition into the electric vehicle space, while pure-play EV manufacturers are differentiating themselves through technological innovation and direct-to-consumer sales models. The market is characterized by intense competition, with companies investing in vertical integration strategies to control critical components of the supply chain, particularly in battery production and charging infrastructure development.

The industry is witnessing a wave of strategic alliances and partnerships, particularly in areas such as battery technology development, charging infrastructure deployment, and autonomous driving capabilities. Joint ventures between automotive manufacturers and technology companies are becoming increasingly common, as firms seek to combine their respective expertise in vehicle manufacturing and software development. These collaborations are reshaping traditional industry boundaries and creating new competitive dynamics, with companies focusing on building comprehensive ecosystems around their electric vehicle offerings rather than just selling vehicles. This evolution is a key aspect of the electric vehicle industry analysis, providing insights into how market consolidation is influencing the electric vehicle market share.

Innovation and Adaptation Key to Success

Success in the US electric car market increasingly depends on companies' ability to innovate across multiple dimensions while maintaining operational efficiency. Incumbent manufacturers must focus on accelerating their transition to electric vehicles while maintaining profitability in their traditional business segments. This requires careful management of research and development investments, strategic partnerships for technology access, and efficient capital allocation across different business units. Companies must also develop robust supply chain strategies to ensure consistent access to critical components, particularly semiconductors and battery materials, while building strong relationships with charging infrastructure providers.

For new entrants and smaller players, differentiation through technological innovation and unique value propositions is crucial for gaining market share. This includes developing specialized vehicles for specific market segments, offering innovative charging solutions, or providing unique customer experiences. Companies must also navigate evolving regulatory requirements, particularly around emissions standards and safety regulations, while maintaining flexibility to adapt to changing market conditions. Building strong brand identity and customer loyalty through superior product quality, after-sales service, and customer engagement will be critical for long-term success in this highly competitive market. The electric vehicle industry trends and electric automotive industry developments underscore the importance of innovation and adaptation in achieving success.

United States Electric Car Industry Leaders

Honda Motor Co. Ltd.

Hyundai Motor Company

Tesla Inc.

Toyota Motor Corporation

Volkswagen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023: Volkswagen France announced that it created a fast charging network under the "Electrify France" label, covering its distribution networks for Volkswagen Commercial Vehicles, Audi, SEAT, CUPRA, and Škoda brands.

- September 2023: Volkswagen reduced production at its Wolfsburg plant for three weeks from September 11, 2023, due to a shortage of engine parts from Slovenia.

- August 2023: Volkswagen plans to assemble the battery in Navarra, as confirmed by the works council. It will partner with Hyundai Mobis for battery assembly while the contract is pending, despite Hyundai Mobis' earlier confirmation.

United States Electric Car Market Report Scope

Passenger Cars are covered as segments by Vehicle Configuration. BEV, FCEV, HEV, PHEV are covered as segments by Fuel Category.Vehicle Configuration

| Passenger Cars | Hatchback |

| Multi-purpose Vehicle | |

| Sedan | |

| Sports Utility Vehicle |

Fuel Category

| BEV |

| FCEV |

| HEV |

| PHEV |

| Vehicle Configuration | Passenger Cars | Hatchback |

| Multi-purpose Vehicle | ||

| Sedan | ||

| Sports Utility Vehicle | ||

| Fuel Category | BEV | |

| FCEV | ||

| HEV | ||

| PHEV |

Market Definition

- Vehicle Type - The category includes passenger cars.

- Vehicle Body Type - This include various body types such as Hatchbacks, Sedans, Sports Utility Vehicles, and Multi-purpose Vehicles.

- Fuel Category - The category exclusively covers electric propulsion systems, including various types such as HEV (Hybrid Electric Vehicles), PHEV (Plug-in Hybrid Electric Vehicles), BEV (Battery Electric Vehicles), and FCEV (Fuel Cell Electric Vehicles).

| Keyword | Definition |

|---|---|

| Electric Vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| BEV | A BEV relies completely on a battery and a motor for propulsion. The battery in the vehicle must be charged by plugging it into an outlet or public charging station. BEVs do not have an ICE and hence are pollution-free. They have a low cost of operation and reduced engine noise as compared to conventional fuel engines. However, they have a shorter range and higher prices than their equivalent gasoline models. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. |

| Plug-in Hybrid EV | A vehicle that can be powered either by an ICE or an electric motor. In contrast to normal hybrid EVs, they can be charged externally. |

| Internal combustion engine | An engine in which the burning of fuels occurs in a confined space called a combustion chamber. Usually run with gasoline/petrol or diesel. |

| Hybrid EV | A vehicle powered by an ICE in combination with one or more electric motors that use energy stored in batteries. These are continually recharged with power from the ICE and regenerative braking. |

| Commercial Vehicles | Commercial vehicles are motorized road vehicles designed for transporting people or goods. The category includes light commercial vehicles (LCVs) and medium and heavy-duty vehicles (M&HCV). |

| Passenger Vehicles | Passenger cars are electric motor– or engine-driven vehicles with at least four wheels. These vehicles are used for the transport of passengers and comprise no more than eight seats in addition to the driver’s seat. |

| Light Commercial Vehicles | Commercial vehicles that weigh less than 6,000 lb (Class 1) and in the range of 6,001–10,000 lb (Class 2) are covered under this category. |

| M&HDT | Commercial vehicles that weigh in the range of 10,001–14,000 lb (Class 3), 14,001–16,000 lb (Class 4), 16,001–19,500 lb (Class 5), 19,501–26,000 lb (Class 6), 26,001–33,000 lb (Class 7) and above 33,001 lb (Class 8) are covered under this category. |

| Bus | A mode of transportation that typically refers to a large vehicle designed to carry passengers over long distances. This includes transit bus, school bus, shuttle bus, and trolleybuses. |

| Diesel | It includes vehicles that use diesel as their primary fuel. A diesel engine vehicle have a compression-ignited injection system rather than the spark-ignited system used by most gasoline vehicles. In such vehicles, fuel is injected into the combustion chamber and ignited by the high temperature achieved when gas is greatly compressed. |

| Gasoline | It includes vehicles that use gas/petrol as their primary fuel. A gasoline car typically uses a spark-ignited internal combustion engine. In such vehicles, fuel is injected into either the intake manifold or the combustion chamber, where it is combined with air, and the air/fuel mixture is ignited by the spark from a spark plug. |

| LPG | It includes vehicles that use LPG as their primary fuel. Both dedicated and bi-fuel LPG vehicles are considered under the scope of the study. |

| CNG | It includes vehicles that use CNG as their primary fuel. These are vehicles that operate like gasoline-powered vehicles with spark-ignited internal combustion engines. |

| HEV | All the electric vehicles that use batteries and an internal combustion engine (ICE) as their primary source for propulsion are considered under this category. HEVs generally use a diesel-electric powertrain and are also known as hybrid diesel-electric vehicles. An HEV converts the vehicle momentum (kinetic energy) into electricity that recharges the battery when the vehicle slows down or stops. The battery of HEV cannot be charged using plug-in devices. |

| PHEV | PHEVs are powered by a battery as well as an ICE. The battery can be charged through either regenerative breaking using the ICE or by plugging into some external charging source. PHEVs have a better range than BEVs but are comparatively less eco-friendly. |

| Hatchback | These are compact-sized cars with a hatch-type door provided at the rear end. |

| Sedan | These are usually two- or four-door passenger cars, with a separate area provided at the rear end for luggage. |

| SUV | Popularly known as SUVs, these cars come with four-wheel drive, and usually have high ground clearance. These cars can also be used as off-road vehicles. |

| MPV | These are multi-purpose vehicles (also called minivans) designed to carry a larger number of passengers. They carry between five and seven people and have room for luggage too. They are usually taller than the average family saloon car, to provide greater headroom and ease of access, and they are usually front-wheel drive. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the sales volume with their respective average selling price (ASP). While estimating ASP factors like average inflation, market demand shift, manufacturing cost, technological advancement, and varying consumer preference, among others have been taken into account.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.