United States Electric Vehicle Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

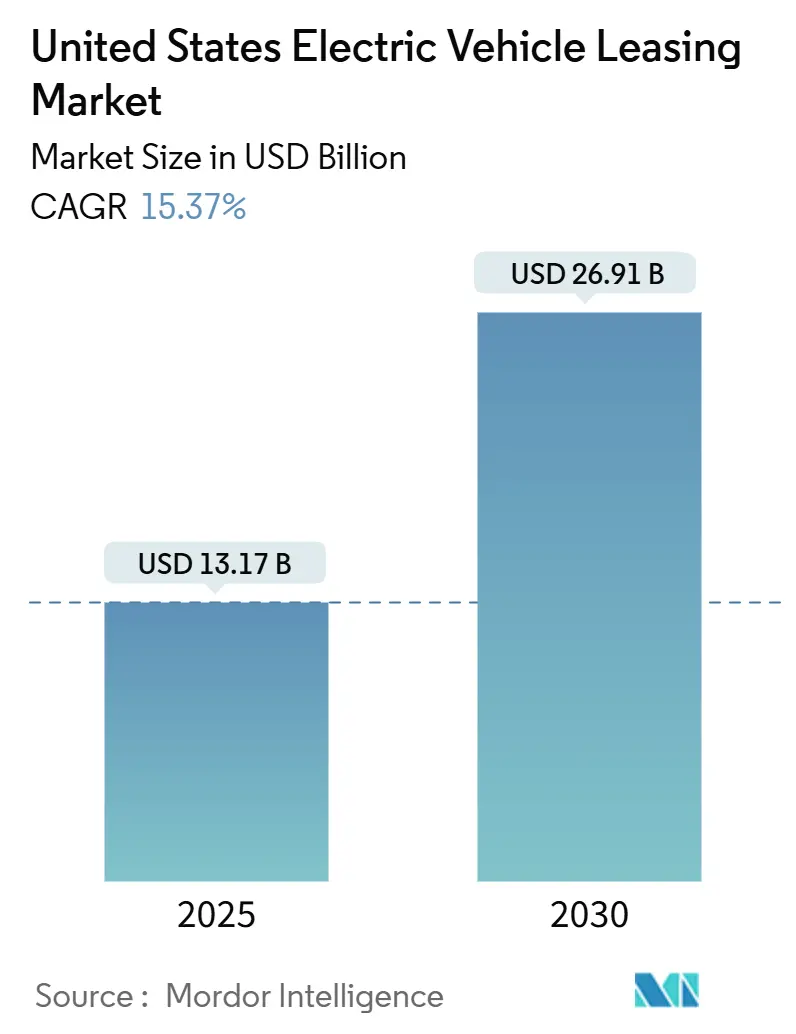

| Market Size (2025) | USD 13.17 Billion |

| Market Size (2030) | USD 26.91 Billion |

| Growth Rate (2025 - 2030) | 15.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Electric Vehicle Leasing Market Analysis by Mordor Intelligence

The US Electric Vehicle Leasing Market size is estimated at USD 13.17 billion in 2025, and is expected to reach USD 26.91 billion by 2030, at a CAGR of 15.37% during the forecast period (2025-2030). The expansion is propelled by the federal commercial-vehicle tax credit that removes income and sticker-price thresholds, making leases the most affordable route into an EV for many households. Captive finance subsidiaries are deliberately discounting money factors to accelerate deliveries, while subscription-style contracts create a fresh value proposition that blends flexibility with low upfront costs. Fleet electrification mandates in logistics and municipal services add dependable volume, and removing residual-value anxiety through manufacturer buy-back guarantees is widening lender participation. Together, these forces realign automotive finance economics and magnify the role of leasing in the broader transition to zero-emission mobility.

Key Report Takeaways

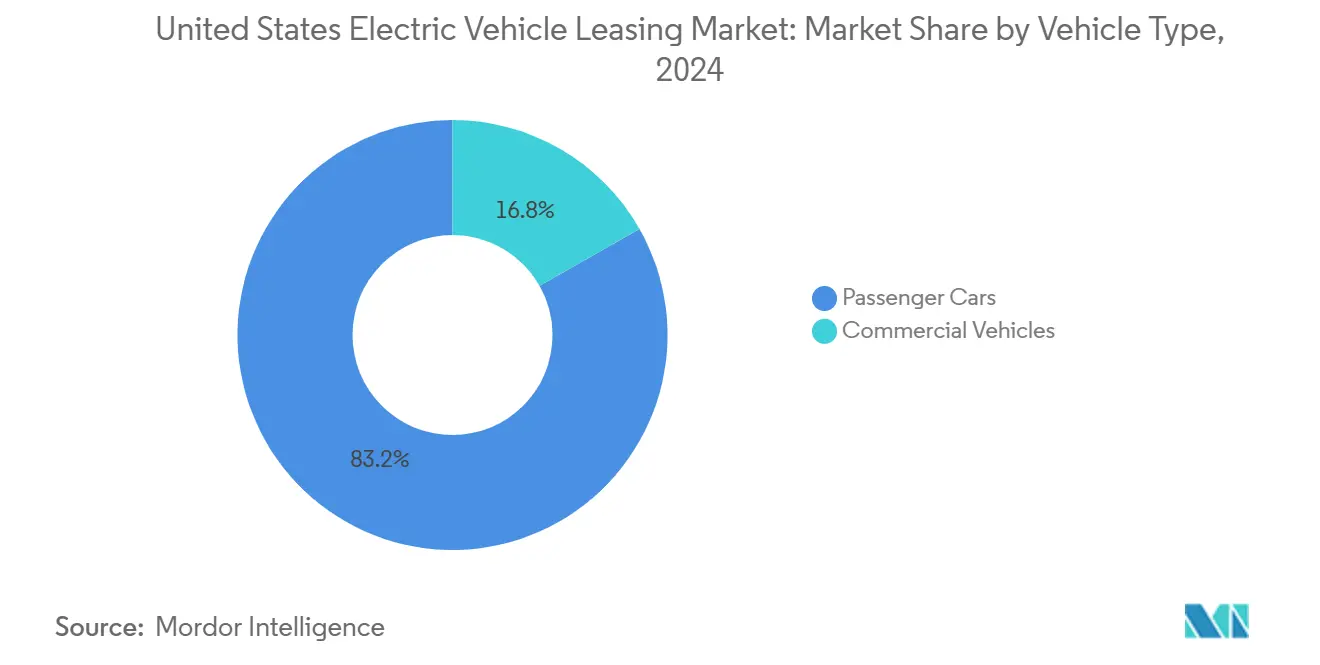

- By vehicle type, passenger cars controlled 83.17% of the United States electric vehicle leasing market share in 2024, while commercial vehicles are on pace for the fastest lift at a 15.51% CAGR through 2030.

- By propulsion type, battery electric vehicles captured 76.15% of lease originations in 2024; fuel-cell electric cars are projected to rise the quickest with a 15.45% CAGR.

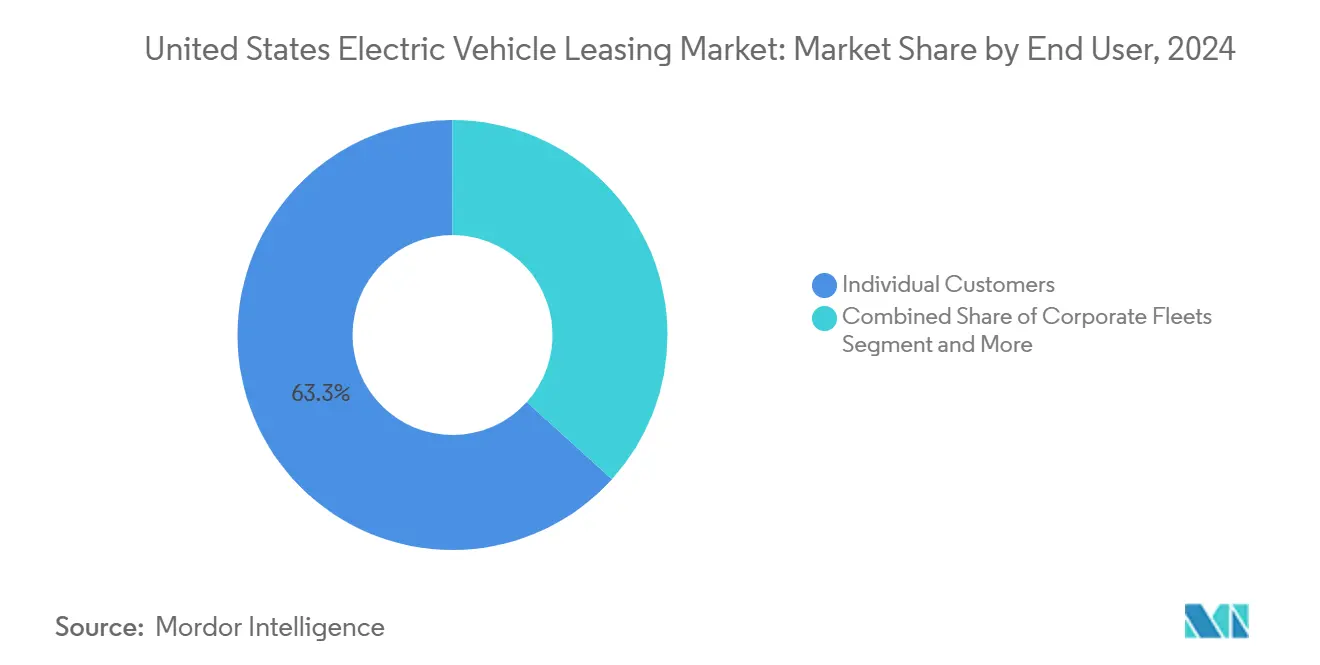

- By end-user, individual customers generated 63.27% of contracts in 2024, yet ride-sharing and delivery platforms are growing briskly at a 15.48% CAGR through 2030.

- By duration, mid-term leases of one to three years held 54.38% of signings in 2024, whereas sub-12-month deals are advancing at a 15.53% CAGR.

Global valuation is built by aggregating outputs from multiple countries and regions, with United states being one of the contributors. Our global electric vehicle leasing market size represents that cumulative total.

United States Electric Vehicle Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal EV Tax Credit Applied | +4.2% | National | Short term (≤ 2 years) |

| Declining Battery Costs | +3.1% | National | Medium term (2-4 years) |

| OEM Captive Finance Arms | +2.8% | National | Medium term (2-4 years) |

| Growth Of Subscription-Style "Flex" Contracts | +1.9% | Urban markets, California leading | Long term (≥ 4 years) |

| Ira Cell And Pack Content Subsidy | +1.7% | National | Short term (≤ 2 years) |

| Battery Second-Life Revenue | +1.4% | National, with California's early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal EV Tax Credit Applied To Leases

Section 45W recast leasing math by permitting an incentive on every transaction, regardless of the lessee’s income or the vehicle’s MSRP, and dealers now apply for the benefit as instant cash at delivery[1]“Section 45W Commercial Clean Vehicles Credit,” Internal Revenue Service, irs.gov. The tool compresses monthly payments, which pushes many electric models below comparable gasoline alternatives and explains why leases exceeded half of new EV registrations in late 2024. Captive lenders capitalize on the rule by blending the tax credit into residual calculations, magnifying upfront savings without eroding profit targets. Although some dealers keep a portion of the credit, watchdog reviews show that competitive pressure is standardizing near-full pass-through in metropolitan areas. For households with limited tax liability, the arrangement is decisive, creating true parity in effective cost versus combustion vehicles for the first time.

Declining Battery Costs Lower TCO

Pack prices dropped below USD 100 per kWh in 2025, slashing acquisition premiums and nudging three-year lease break-even mileage to roughly 25,000 miles a year in delivery settings. Lithium iron phosphate chemistries dominate entry-level models, bringing higher cycle life and stabilizing residual-value estimates for lessors. As a result, commercial clients can recoup lease payments through fuel and maintenance savings within 30 months, cementing the economic case for electrification. Rapid chemistry turnover does, however, raise obsolescence risk; each new generation can outdate the incumbent fleet faster than the typical lease cycle. Lessors mitigate that risk by bundling software-defined feature updates into contracts, preserving vehicle competitiveness throughout the term.

OEM Captive Finance Arms Expand Lease Offerings

GM Financial, Ford Credit, and Tesla Financial Services deploy their balance sheets to underwrite below-market money factors that smaller lessors cannot match[2]“Economic Well-Being of U.S. Households,” Board of Governors of the Federal Reserve System, federalreserve.gov . The captive model allows manufacturers to manage inventory swings and shape demand while internalizing residual-value exposure. Tesla reported a operating leases in Q1 2025, underscoring the scale of direct financing used to strengthen brand loyalty. Independent lessors lack comparable cost visibility and must price residual risk more conservatively, widening the monthly-payment gap and consolidating share with captive networks.

Growth Of Subscription-Style “Flex” Contracts

Urban consumers embrace month-to-month access packages that wrap insurance, maintenance, and charging into a single fee, prioritizing flexibility over long-term equity. Companies piloting the model allow drivers to swap between electric and conventional vehicles, easing range anxiety and boosting first-time EV exposure. Operators harvest telematics data to optimize vehicle rotation and extract secondary revenue from partnerships with charging providers. Capital intensity remains formidable, yet venture-backed firms in California demonstrate break-even potential once fleet utilization climbs above 80%. Municipal congestion-pricing proposals could further tilt demand toward flexible access over outright ownership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Interest-Rate Environment | -2.1% | National | Short term (≤ 2 years) |

| Limited Rural Charging Infrastructure | -1.8% | Rural markets, particularly in the Mountain West | Medium term (2-4 years) |

| OEM Software Locks Create Residual-Value Risk | -1.3% | National, Tesla vehicles are most affected | Medium term (2-4 years) |

| State Mileage-Tax Proposals Deter High-Usage Fleets | -0.9% | California, Wyoming, Hawaii, Michigan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interest-Rate Environment Inflates Monthly Payments

Elevated federal-funds targets throughout 2024 pushed automotive lease money factors to decade highs, and EVs felt a heavier impact because higher sticker prices amplify financing costs. Subprime applicants faced the sharpest spike, eroding net savings from the tax credit and nudging some shoppers toward used gasoline vehicles. Captive lenders partly absorb the stress by treating finance income as a marketing lever, yet independent lessors must fully price risk. That split entrenches a dual-track market in which customers with access to OEM finance enjoy substantially lower payments than those sourcing funding on the open market.

Limited Rural Charging Infrastructure

Public DC-fast availability remains thin outside major corridors, forcing fleets to shoulder private-depot installation expense that lengthens payback timelines. Only one-fifths of local governments applied for federal infrastructure grants under the Bipartisan Infrastructure Law, and most recipients cluster in metropolitan counties. The imbalance restricts lessor appetite for rural fleet contracts and narrows the geographic footprint of the United States electric vehicle leasing market. Low-density counties in the Mountain West see adoption rates less than one-third of the national average despite abundant solar potential and cheap electricity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Acceleration

Commercial vehicles are on course for a 15.51% CAGR between 2025 and 2030, taking advantage of high annual mileage that fully unlocks operational savings within a single lease term. The United States electric vehicle leasing market size for commercial fleets grows exponentially and continues to benefit from generous tax credits that flow through regardless of income restrictions. Enterprise Fleet Management’s purpose-built units for Domino’s created the nation’s largest electric pizza-delivery fleet, and the South Pasadena Police Department’s Model Y patrol cars prove durability under heavy-duty cycles. Yet, that outlier has not reversed the macroeconomic logic that favors electrification. Insurers now price battery-specific coverage products, narrowing premium gaps with combustion vehicles and further enhancing total cost of ownership.

Passenger cars remain the volume anchor with 83.17% of 2024 leases, supported by well-established financing channels and consumer familiarity with three-year terms. The United States electric vehicle leasing market share leadership of the segment comes from its vast addressable base of commuters who prioritize predictable monthly payments over vehicle equity. Federal leasing incentives shortened the affordability gap, and dealership data reveal that more than three-fifths of first-time EV lessors were previously payment buyers of gasoline models. Growth trails commercial contracts because average annual mileage sits below the breakeven threshold for fuel savings to dominate. Still, enhanced resale certainty and second-life battery pathways reduce residual-value discounts, giving lenders greater confidence to underwrite mainstream sedans and crossovers.

By Propulsion Type: Fuel Cells Emerge Despite Infrastructure Limits

Battery electric vehicles hold 76.15% of the propulsion mix and form the backbone of the United States electric vehicle leasing market size. Overnight home charging remains the decisive advantage, and maturing supply chains have stabilized pack lead times to fewer than eight weeks for most volume models. Captive finance groups bundle wall-box installation into lease contracts, transferring convenience into an embedded service and raising churn barriers. Secondary market data show better-than-expected price retention for lithium iron phosphate models, especially those fitted with bidirectional charging that increases utility for stationary power.

Fuel-cell electric vehicles expand at a 15.45% CAGR through 2030, even though public hydrogen filling stations cluster mainly in California. Fleet operators in heavy urban delivery prioritize the advantageous refill time and payload efficiency compared with battery vans. Policymakers view hydrogen as a strategic complement for long-haul freight, which could open new growth lanes once corridor infrastructure develops. Plug-in hybrids continue to serve as a transition technology for rural drivers, but their share is forecast to taper as charging density improves and battery costs keep falling.

By End User: Ride-Sharing Platforms Accelerate Adoption

Ride-sharing and delivery platforms will chart a 15.48% CAGR, supported by corporate incentives and mileage patterns that quickly recoup lease costs. Uber offers up to USD 2,000 per driver for new EV sign-ups and shares anonymized trip data with Tesla to guide charger placement. High utilization—often above 50,000 miles annually—mitigates depreciation concerns and yields monthly fuel savings north of USD 300, meaning gross earnings improve even after factoring lease payments. Telematics integration helps platforms optimize charging schedules and minimize downtime, which raises vehicle productivity and fleet-wide revenue.

Individual consumers still occupy 63.27% of contracts, buoyed by the immediate credit and the comfort of fixed monthly outlays. Surveys indicate a rising share of suburban households now price an EV lease below what they paid for a premium gasoline SUV in 2023, anchoring sentiment that the switch does not require lifestyle compromise. Corporate fleets hold steady as sustainability commitments crystallize into formal procurement targets; Ernst & Young reports that around three-fifths of logistics managers see decarbonization as a strategic imperative. Government agencies provide consistent baseline demand through grant-backed acquisitions prioritizing emission reduction over short-term return metrics.

By Duration: Short-Term Contracts Gain Traction

Short-term leases under 12 months are scaling at a 15.53% CAGR as consumers embrace pay-as-you-go mobility. Subscription providers embed maintenance, insurance, and charging within a single payment, catering to drivers who value choice and digital convenience. The United States electric vehicle leasing market size for these flex contracts remains modest but influential, because it channels thousands of first-time EV experiences every month. Operators deploy digital-twin analytics to anticipate maintenance events and redistribute vehicles across cities to smooth load, improving asset yields and compressing turnaround times.

Mid-term leases spanning one to three years still dominate at 54.38% of originations, mirroring historical patterns of household vehicle replacement cycles. Lessees enjoy warranty coverage for the full term and can upgrade when technology nodes advance. Contracts exceeding three years are fading as buyers grow wary of battery innovations that arrive faster than conventional model refreshes, eroding the appeal of locking into a five-year deal. Lessors prefer shorter horizons too since they retain the agility to re-price residuals in response to market sentiment shifts.

Geography Analysis

California is the nucleus of the United States electric vehicle leasing market, driven by state rebates that stack atop the federal USD 7,500 credit and a robust network of public chargers. The Low Carbon Fuel Standard generates liquidity for charging operators, funneling a decent amount toward EV programs over the next decade[3]“Low Carbon Fuel Standard Market Report 2025,” California Air Resources Board, arb.ca.gov . Yet, revenue lost from shrinking gasoline taxes is forecast to crest annually by 2030, prompting legislators to pilot road-usage fees that could add operating costs for high-mileage fleets. The Northeast corridor benefits from compact urban layouts and utility partnerships that install curbside chargers on existing street-light poles, lowering infrastructure cost by as much as 60%. Multi-family dwellers embrace leasing to avoid upfront charger installation, and city councils encourage flex-contract providers that ease curb congestion. Cooler climates reduce battery efficiency, but software-controlled thermal-management improvements narrow the winter range deficit to under 15%, preserving lease appeal year-round.

Texas embodies a dual narrative: abundant renewable energy brings the lowest off-peak electricity rates among central states, yet the absence of statewide EV incentives tempers consumer adoption. Commercial prospects remain bright because of freight volume along the I-35 corridor, where logistics players trial electrified last-mile vans supported by warehouse DC-fast sites. Policy uncertainty over emission mandates adds execution risk, leading lessors to structure opt-out clauses tied to regulatory developments. The Mountain West lags due to sparse charging nodes and harsh winter conditions that shave range by up to 25%. Colorado and Utah stand as exceptions, rolling out generous utility rebates that bridge the economic gap and accelerating adoption in ski-resort shuttle operations.

Southeastern states showcase mixed uptake. Lower electricity prices and large resident fleets favor eventual scale, but weaker state incentives and entrenched dealership franchise laws slow near-term leasing momentum. Florida’s hurricane resiliency codes drive demand for bidirectional-charging EVs that can power homes during grid outages, influencing residual-value modeling and creating a unique lease-pricing premium for V2H-enabled models.

Coverage of the electric vehicle leasing market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for Japan, India, and South Korea, each shaped by local operating conditions.

Competitive Landscape

The United States electric vehicle leasing market displays moderate concentration, with the top five captives and disruptors holding roughly three-fifths of originations. Tesla Financial Services wields vertical integration, offering same-day underwriting and vehicle delivery that trims friction and secures brand loyalty. GM Financial targets mainstream buyers with subsidized rates on the Chevrolet Equinox EV and Silverado EV, capturing economic tiers that Tesla does not directly serve. Ford Motor Credit combines zero-down packages with home-charger installation to lock in family SUV drivers.

Technology-led entrants like Autonomy and Finn attack the flex-contract niche, exploiting digital onboarding and dynamic pricing to carve share from traditional three-year leases. Their asset-light models hinge on residual-buyback guarantees from OEMs. Independent lessors without manufacturer backing face thinning margins as captives use finance income as a strategic lever rather than a profit driver. Platform partnerships with ride-sharing giants offer a lifeline, enabling scale through guaranteed utilization.

Strategic moves underscore competition intensity. In late 2024, Tesla broadened its lease-end buyout ban beyond Model 3 to Model Y, steering used units into its certified-pre-owned channel. GM Financial launched SmartLease+, bundling Level 2 charger hardware and installation into payments at a premium price. Honda entered the hydrogen segment with the CR-V e:FCEV lease program, leveraging California fuel credits to entice early adopters. These initiatives illustrate how firms use financing terms to shape technology adoption trajectories and defend their share.

United States Electric Vehicle Leasing Industry Leaders

Tesla Financial Services

GM Financial

Ford Motor Credit

Hyundai Capital America

Volkswagen Credit

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Honda announced lease pricing for the 2025 CR-V e: FCEV at USD 459 monthly with USD 15,000 hydrogen refueling credits, marking the first production plug-in fuel-cell vehicle available for consumer leasing in the United States through 12 California dealerships.

- January 2024: Uber intensified EV driver incentives by offering up to USD 2,000 for Tesla purchases and sharing trip data with Tesla to identify charging infrastructure needs, demonstrating the platform economy’s role in accelerating commercial adoption.

United States Electric Vehicle Leasing Market Report Scope

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| Individual Customers |

| Corporate Fleets |

| Government Agencies |

| Ride-Sharing & Delivery Platforms |

| Short-Term (Less than 12 months) |

| Mid-Term (1–3 years) |

| Long-Term (More than 3 years) |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Propulsion Type | Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles | |

| Fuel-Cell Electric Vehicles | |

| By End User | Individual Customers |

| Corporate Fleets | |

| Government Agencies | |

| Ride-Sharing & Delivery Platforms | |

| By Duration | Short-Term (Less than 12 months) |

| Mid-Term (1–3 years) | |

| Long-Term (More than 3 years) |

Key Questions Answered in the Report

How large is the United States electric vehicle leasing market today?

The sector reached a United States electric vehicle leasing market size of USD 13.17 billion in 2025 and is projected to nearly double by 2030.

What is the expected growth rate through 2030?

The market is forecast to expand at a 15.37% CAGR, driven by tax credits, falling battery prices, and growing commercial demand.

Which vehicle category grows fastest in leasing?

Commercial vans and trucks are set for a 15.51% CAGR because high mileage unlocks maximum operating savings.

How do federal incentives affect monthly lease payments?

The USD 7,500 commercial-vehicle credit often trims USD 200–250 from monthly payments, making many EVs cheaper to lease than comparable gasoline models.

What risks could slow leasing adoption?

Rising interest rates, limited rural charging, and potential state mileage taxes can raise costs and dampen fleet economics.

Which companies lead in EV leasing?

Tesla Financial Services, GM Financial, and Ford Motor Credit are notable leaders, supported by captive financing and strategic rate subsidies.

Page last updated on: