Japan Electric Vehicle Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

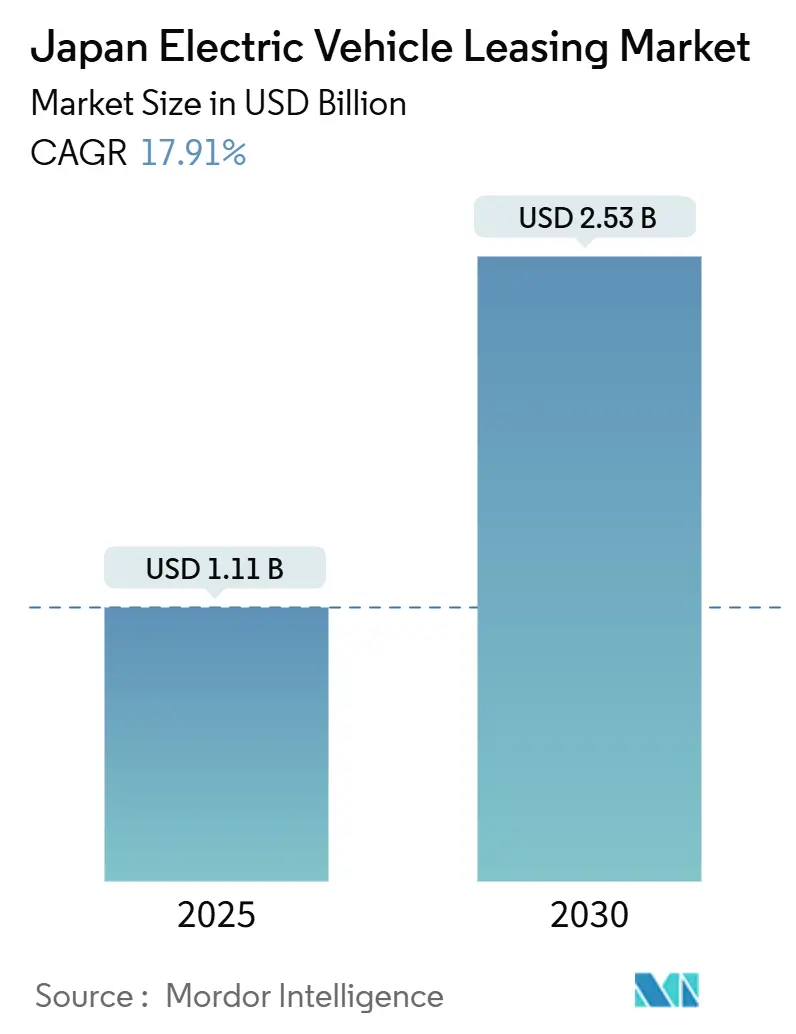

| Market Size (2025) | USD 1.11 Billion |

| Market Size (2030) | USD 2.53 Billion |

| Growth Rate (2025 - 2030) | 17.91% CAGR |

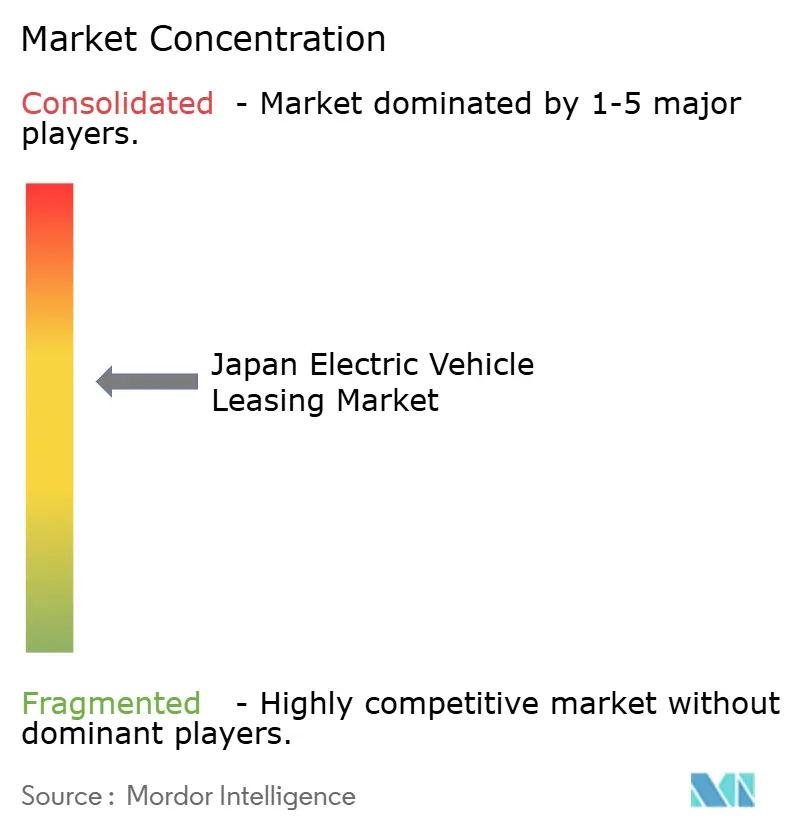

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Electric Vehicle Leasing Market Analysis by Mordor Intelligence

The Japan electric vehicle leasing market recorded a market size of USD 1.11 billion in 2025 and is forecast to reach USD 2.53 billion by 2030, expanding at a 17.91% CAGR between 2025 and 2030. The market’s momentum stems from Green Transformation investment policies that channel GX Economy Transition Bond proceeds toward corporate electrification incentives, while rising ESG mandates convert fleet budgets from capital expenditure to predictable operating spending. Accelerating public- and private-sector charging rollouts, falling total cost of ownership for high-mileage applications, and the emergence of battery-as-a-service leasing all reinforce demand. Competitive opportunities are widening as ride-sharing and delivery platforms scale, hydrogen infrastructure spending attracts fuel-cell fleets, and data-driven residual-value tools lower depreciation risk. Long-term growth prospects are further supported by domestic OEM consolidation that promises shared development costs, streamlined supply chains, and greater product variety for lessees.

Key Report Takeaways

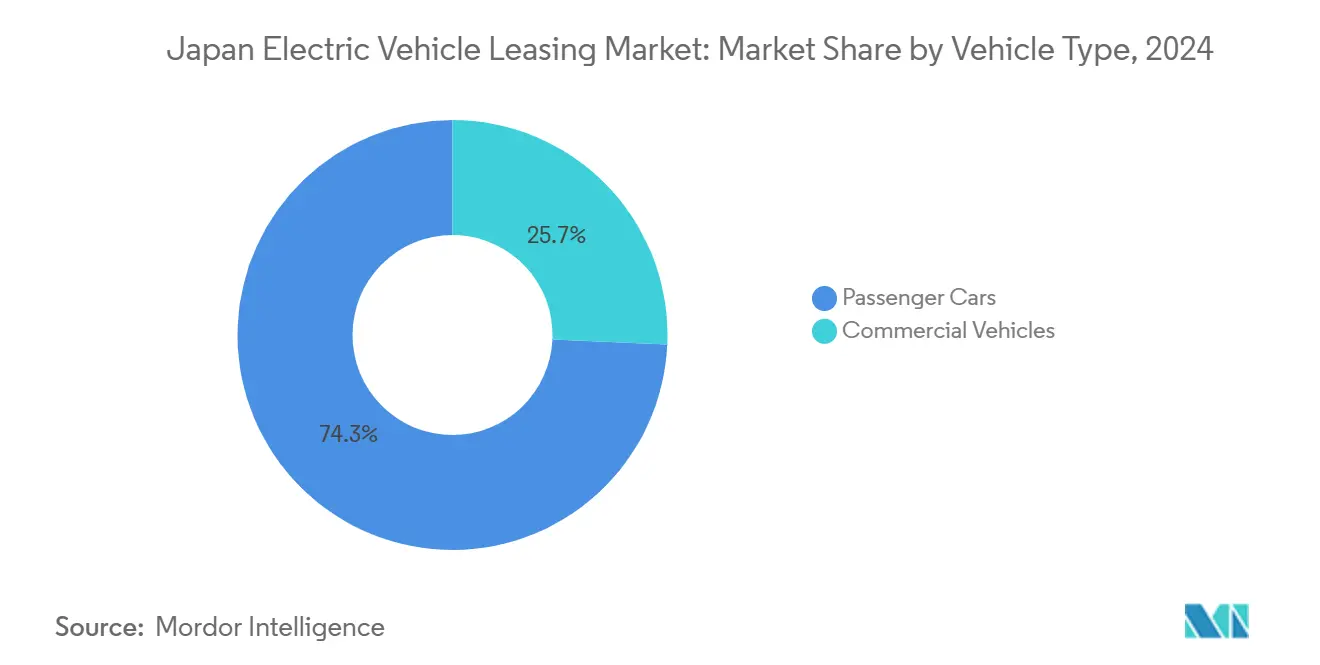

- By vehicle type, Passenger Cars led with a 74.25% share of the Japan electric vehicle leasing market in 2024, while Commercial Vehicles are projected to expand at a 19.09% CAGR between 2025 and 2030.

- By propulsion type, Battery Electric Vehicles led with a 66.33% share of the Japan electric vehicle leasing market in 2024; Fuel-Cell Electric Vehicles are projected to expand at a 23.93% CAGR between 2025 and 2030.

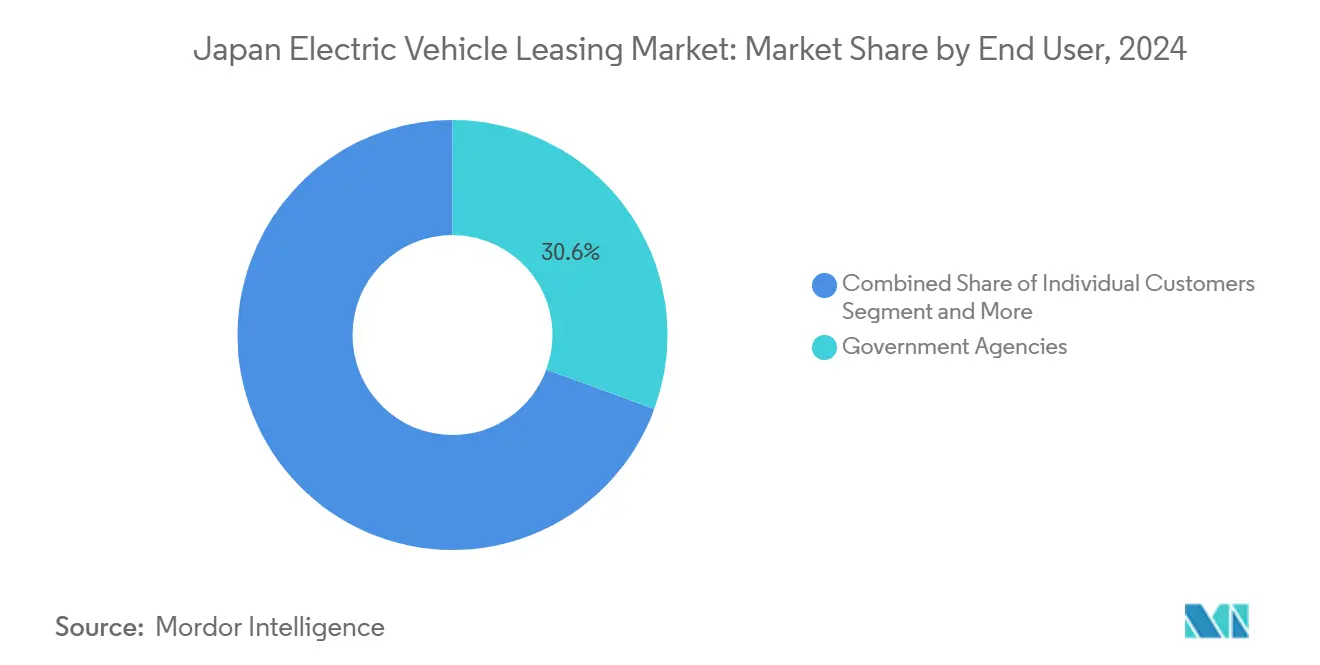

- By end user, Government Agencies held 30.55% of the Japan electric vehicle leasing market share in 2024, while Ride-Sharing and Delivery Platforms are advancing at a 20.24% CAGR through 2030.

- By lease duration, Long-Term contracts captured a 34.81% share of the Japan electric vehicle leasing market in 2024, although Short-Term contracts are growing at a 19.64% CAGR to 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Japan representing one among them. The global report on electric vehicle leasing market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Japan Electric Vehicle Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate ESG Drives Fleet Electrification | +4.1% | Nationwide corporate headquarters regions | Short term (≤ 2 years) |

| EV Cost-of-Ownership Falling Versus ICE | +3.5% | Nationwide high-mileage segments | Long term (≥ 4 years) |

| Government Incentives for EV Leases | +3.2% | National: Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| OEM Battery-Health Analytics Lower Risk | +2.9% | High-volume leasing markets | Medium term (2-4 years) |

| Charging Infrastructure Expanding | +2.8% | Urban centers, highway corridors | Medium term (2-4 years) |

| V2G Pilots Enable Revenue-Sharing Leases | +1.6% | Tokyo pilots, other cities in pipeline | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate ESG Targets Accelerating Fleet Electrification

Large employers translate net-zero pledges into binding vehicle-replacement schedules, prompting bulk lease contracts that guarantee step-wise fleet conversion. Chugai Pharmaceutical plans to cut fleet fuel use by 75% by 2030 through electric leasing, and financial institutions are replicating the model to strengthen integrated reporting credibility. OEM joint ventures deliver turnkey offerings that bundle charging access, telematics, and service, enabling procurement managers to demonstrate rapid emissions progress without one-time capital outlays. This virtuous cycle sustains long-term lease demand across passenger and commercial vehicle segments.

Falling EV Total Cost-of-Ownership vs. ICE Vehicles

Battery price declines, preferential electricity tariffs, and reduced maintenance jointly lower lifecycle costs, especially for vehicles logging more than 40,000 km annually. ALTNA’s battery-as-a-service plan separates the most depreciating asset from the chassis, allowing lessees to pay only for energy throughput and residual battery capacity. Flexible early-exit features introduced by Joycal appeal to households wary of technology obsolescence, yet still lock in lower kilometer-based costs than comparable gasoline models.

Government Subsidies and Tax Incentives for EV Leases

Japan’s Green Transformation road map earmarks GX Economy Transition Bond proceeds for decarbonizing transport, with preferential depreciation, registration-tax rebates, and interest-rate subsidies that specifically reward operational-lease structures. Tokyo metropolitan programs add condominium charger grants that remove urban adoption bottlenecks. Together, these incentives compress effective monthly lease payments, widen the addressable corporate base, and align with 2050 carbon-neutrality goals while preserving domestic manufacturing jobs [1]Ministry of Economy, Trade and Industry, “Zero Emission Vehicle Subsidy Programs,” meti.go.jp.

OEM Battery-Health Analytics Lowering Residual-Value Risk

Lessors historically added high-risk premiums to cover uncertain battery resale values. New cloud-based diagnostics partnered by ORIX, EVolity, and Panasonic provide real-time state-of-health scoring, which underpins guaranteed buy-back programs. Reliable data narrows valuation spreads at lease end and unlocks secondary stationary-storage uses that lift residual proceeds, feeding back into competitive monthly pricing [2]Panasonic Corp., “Battery Health Analytics Partnership Announcement,” panasonic.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain EV Residual Values | -2.7% | Secondary vehicle markets nationwide | Medium term (2-4 years) |

| Limited Private-Charger Installation | -2.1% | Urban centers, particularly Tokyo and Osaka metropolitan areas | Short term (≤ 2 years) |

| Import-Driven Delivery Volatility | -1.9% | Major ports and inland distribution hubs | Short term (≤ 2 years) |

| Conservative Consumer Finance Culture | -1.4% | National, stronger impact in rural and traditional markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uncertain EV Residual Values and Higher Depreciation Risk

Battery degradation variance produces wide resale-price spreads, prompting lessors to inflate security deposits or monthly charges. Standardized diagnostics from ORIX and partner suppliers are addressing the gap, but the current five-year depreciation curve remains steeper than for internal-combustion counterparts. Insurance carriers now underwrite degradation guarantees, yet full residual-value normalization is unlikely until post-2027, when secondary-life stationary storage demand scales [3]ORIX Corp., “Battery Diagnostics Service Launch,” orix.co.jp.

Limited Private-Charger Installation in Multi-Unit Dwellings

A significant proportion of households in Tokyo and Osaka choose to reside in condominiums or rental apartments, where parking spaces are shared or detached from individual ownership, making charger retrofits subject to association votes and complex electrical upgrades. Even when national subsidies cover up to 50% of hardware costs, building-management boards often reject installations that could increase maintenance fees or reduce visitor parking capacity, slowing the approval cycle to 18 months or longer. This bottleneck raises range anxiety for potential lessees who lack reliable overnight charging, leading leasing firms to incorporate higher risk premiums into monthly payments. Fleet operators that house vehicles in apartment blocks face additional logistical hurdles, such as staggered charging schedules that extend vehicle downtime and erode productivity. Until streamlined permitting processes and standardized load-sharing panels become widespread, limited charger availability in multi-unit dwellings will continue to dampen near-term lease growth in densely populated cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Corporates Propel Commercial Growth

Commercial vehicles are projected to grow at a 19.09% CAGR to 2030, while passenger cars retained a 74.25% share in 2024. Corporate decarbonization targets push logistics fleets toward electric vans and trucks, and FamilyMart’s 12.8% CO₂ reduction highlights how route optimization multiplies sustainability gains for lessees. Battery-as-a-service contracts remove upfront pack costs, aligning payments with energy throughput and creating second-life grid-storage value streams that improve the Japan electric vehicle leasing market size economics for high-mileage users.

Passenger-car leasing expands as younger drivers favor access over ownership and embrace transparent, usage-based billing. Joycal’s NORIDOKI MINI and Seven Max FREE plans demonstrate how penalty-free exits and mid-term upgrades counter technology-obsolescence fears. Urban charger density and condominium-subsidy programs reduce home-charging barriers, reinforcing passenger-car demand even as commercial segments capture the highest CAGR within the Japan electric vehicle leasing market.

By Propulsion Type: Hydrogen Picks Up Pace

Battery electric vehicles still hold 66.33% of 2024 volume thanks to mature charging networks and falling battery prices. Residual-value analytics partnerships between ORIX, EVolity, and Panasonic standardize state-of-health data, permitting lessors to sharpen end-of-term valuations. Plug-in hybrids taper as range anxiety fades, while V2G-enabled BEVs earn grid-capacity income that can be shared between lessors and lessees, enhancing total-cost-of-ownership advantages.

Fuel-cell electric vehicles post the fastest 23.93% CAGR because government hydrogen-station grants shrink refueling downtime for heavy payload routes. The Honda-Nissan merger targets shared stack and software platforms that will lower component costs and broaden FCEV model availability for fleet lessors, ensuring a differentiated option alongside BEVs within the Japan electric vehicle leasing market share mix.

By End User: Policy Leads, Platforms Scale

Government agencies commanded 30.55% of the Japan electric vehicle leasing market share in 2024 after ministries locked in zero-emission fleet rotations through long-term contracts. Procurement guidelines favor predictable operating-expense structures, allowing agencies to hit carbon-neutral milestones without capital-budget spikes and to publicize progress in annual sustainability reports.

Ride-sharing and delivery platforms are growing at a 20.24% CAGR, catalyzed by April 2024 legislation that lets taxi licensees manage app-based ride-sharing. Operators pick short-to-mid-term leases with kilometer-indexed billing to flex fleets up or down in real time. Corporate fleets remain the second-largest slice, and individual consumers increasingly opt for bundled insurance-and-maintenance packages that simplify budgeting and minimize ownership risk.

By Duration: Flexibility Gains Favor

Long-term contracts (>3 years) still hold 34.81% of the Japan electric vehicle leasing market size because agencies and blue-chip corporates need multi-year cost certainty. These users prize fixed monthly payments that mirror depreciation schedules and shield budgets from fuel-price volatility, especially for high-mileage commercial vans.

Long-term contracts (3 years) still hold 34.81% of the Japan electric vehicle leasing market size because agencies and blue-chip corporates need multi-year cost certainty. These users prize fixed monthly payments that mirror depreciation schedules and shield budgets from fuel-price volatility, especially for high-mileage commercial vans.h seasonal demand swings. Mid-term contracts (1-3 years) bridge the gap by offering tech refresh options without constant renegotiation.

Geography Analysis

Metropolitan corridors—Tokyo, Osaka, and Nagoya—dominate adoption because dense charger networks, condominium-subsidy schemes, and corporate headquarters clusters converge to create critical mass. Park24’s Rail & Car Share hubs integrate rail access with leased EVs, widening commuter reach and supporting passenger-car utilization at scale. Coastal prefectures also benefit from nearby import terminals that streamline vehicle intake, yet they must manage higher exposure to shipping delays that can ripple into lease scheduling.

Rural prefectures lag due to sparse charging and lower fleet densities, factors that elevate operational-risk premiums baked into lease pricing. Government mobility programs now fund community EV pools that target medical-care and education access, seeding future demand once infrastructure arrives. Leasing companies explore mini-hub models with solar-assisted slow chargers to bridge the gap and test viability in low-population areas before committing larger assets.

Domestic OEM production realignment aims to create regional manufacturing nodes that, post-2027, could rebalance market weight toward Kyushu and Tohoku as localized supply stabilizes delivery windows and trims logistics costs. These new clusters are projected to shorten dealer-to-customer lead times, lower inbound freight emissions, and foster local vendor ecosystems that can service leased fleets more efficiently. The resulting geographic dispersion may gradually narrow the adoption gap between urban and non-urban markets.

Mordor Intelligence provides coverage of the electric vehicle leasing market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India, South Korea, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

Incumbent finance giants leverage scale to negotiate favorable OEM pricing while layering analytics tools to reduce residual-risk buffers. ORIX integrates battery-health scoring with telematics to refine asset-valuation curves, and Toyota Financial Services’ KINTO bundles insurance, maintenance, and seasonal tire storage in a single fee that resonates with risk-averse households. Sumitomo Mitsui Auto Service cross-sells solar and battery-storage leases to depot operators, reinforcing sticky customer relationships and unlocking bundled-energy revenue.

Disruptors carve niches through flexible contract structures and energy-market linkages that incumbents cannot replicate quickly. ALTNA retains battery ownership to monetize second-life grid opportunities, allowing upfront chassis lease rates to undercut traditional offers. Telemetry-rich newcomers craft pay-as-you-drive models that align cost with gig-economy revenue rhythms, and software-defined fleet-management dashboards offer lessees real-time ESG reporting that simplifies compliance.

Consolidation trends abroad—such as ALD Automotive merging with LeasePlan—signal intensifying pressure for Japanese players to scale or specialize without diluting service quality. Domestic alliances between automakers and leasing houses now prioritize vehicle-to-grid readiness so fleets can earn capacity-market revenue. The competitive field therefore hinges on who can blend asset-financing efficiency, battery-health transparency, and energy-services expertise while navigating Japan’s stringent consumer-protection and data-privacy regulations.

Japan Electric Vehicle Leasing Industry Leaders

ORIX Auto Corporation

Sumitomo Mitsui Auto Service Co., Ltd.

Nippon Car Solutions Co., Ltd.

Tokyo Century Corp. (Nippon Rent-A-Car)

Toyota Financial Services Corp. (KINTO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Joycal Japan launched the Seven Max FREE flexible car-leasing plan that permits penalty-free termination after 25 months, enhancing consumer flexibility while preserving predictable payments.

- November 2024: JA Mitsui Leasing and Fujitsu began trials with vehicles from Japan Agricultural Cooperatives to speed commercial EV adoption across farming regions.

- June 2024: Honda and Mitsubishi established ALTNA Co. Ltd., a 50/50 venture to advance EV leasing models and second-life battery storage applications.

Japan Electric Vehicle Leasing Market Report Scope

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| Individual Customers |

| Corporate Fleets |

| Government Agencies |

| Ride-Sharing and Delivery Platforms |

| Short-Term (Less than 12 months) |

| Mid-Term (1–3 years) |

| Long-Term (More than 3 years) |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Propulsion Type | Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles | |

| Fuel-Cell Electric Vehicles | |

| By End User | Individual Customers |

| Corporate Fleets | |

| Government Agencies | |

| Ride-Sharing and Delivery Platforms | |

| By Duration | Short-Term (Less than 12 months) |

| Mid-Term (1–3 years) | |

| Long-Term (More than 3 years) |

Key Questions Answered in the Report

How big is the Japan electric vehicle leasing market in 2025?

The market stands at USD 1.11 billion in 2025 and is set to grow rapidly to USD 2.53 billion by 2030.

What CAGR is expected for Japanese EV leasing between 2025 and 2030?

A strong 17.91% CAGR is forecast as incentives, infrastructure, and ESG policies converge.

Which end-user group is growing fastest in Japanese EV leasing?

Ride-sharing and delivery platforms lead with a 20.24% CAGR through 2030.

How are short-term leases affecting market dynamics?

Flexible under-12-month contracts are expanding at 19.64% CAGR, meeting demand for technology agility and balance-sheet efficiency.

Page last updated on: