India Electric Vehicle Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

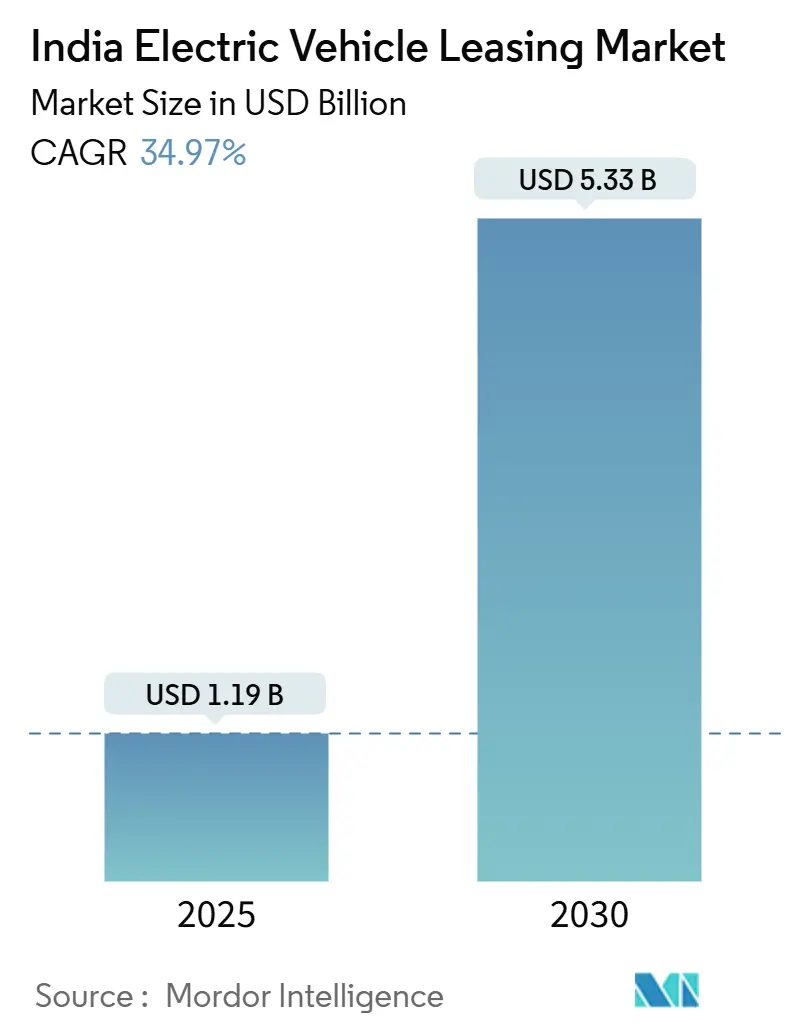

| Market Size (2025) | USD 1.19 Billion |

| Market Size (2030) | USD 5.33 Billion |

| Growth Rate (2025 - 2030) | 34.97% CAGR |

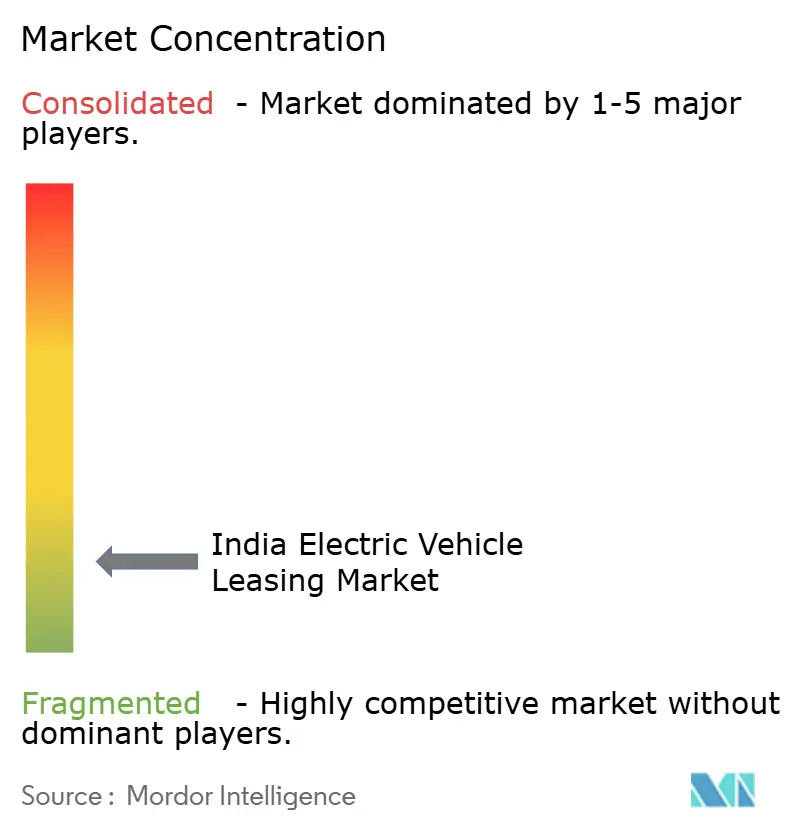

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Electric Vehicle Leasing Market Analysis by Mordor Intelligence

The India electric vehicle leasing market reached USD 1.19 billion in 2025 and is forecast to climb to USD 5.33 billion by 2030, translating into a 34.97% CAGR; this trajectory underscores a swift scaling of the India electric vehicle leasing market size alongside robust demand growth. Portfolio expansion is being propelled by government incentive realignment, widening corporate ESG mandates, and innovative battery-as-a-service models that compress lifetime costs. Leasing companies are capitalizing on falling cell prices, improving charging density in metropolitan corridors, and streamlined GST treatment that removes historical tax distortions. Competitive intensity remains moderate yet rising, with traditional lessors defending share against digital-first entrants that bundle fleet analytics, charging access, and residual-value guarantees. A tightening credit environment and selective lender appetites introduce financing friction, but structured risk-sharing pools and OEM-linked supply contracts partially offset funding constraints.

Key Report Takeaways

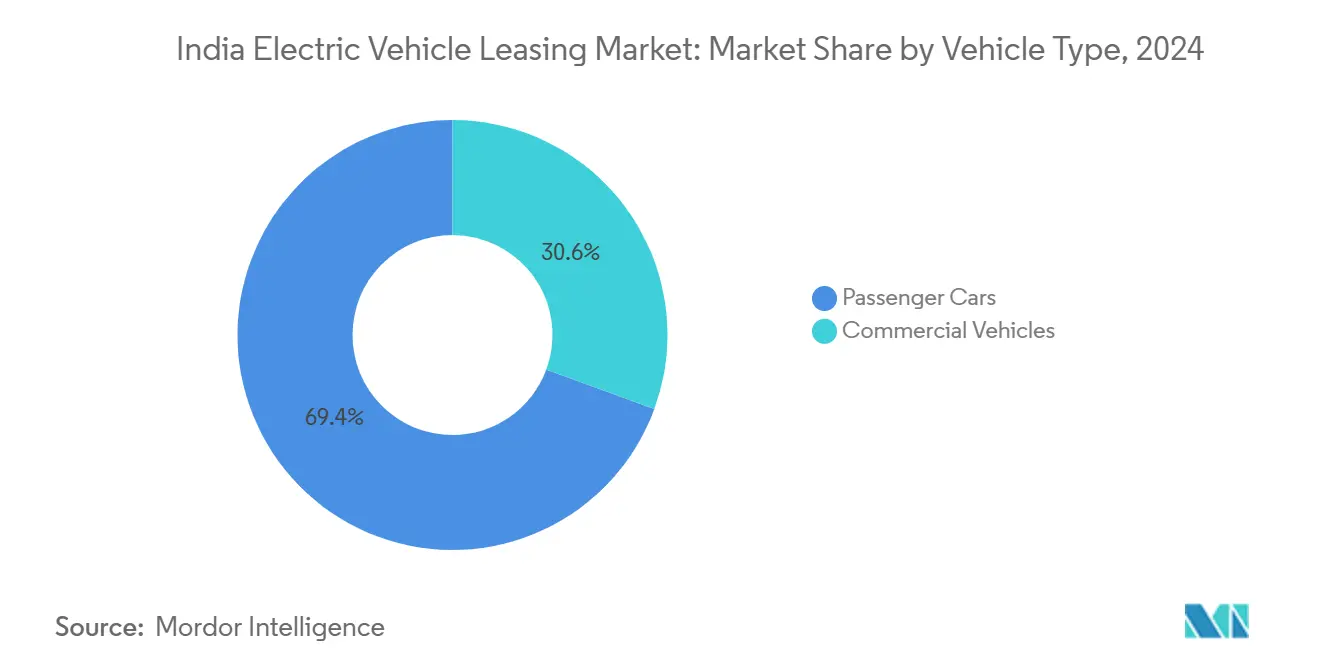

- By vehicle type, passenger cars held 69.36% of the India electric vehicle leasing market share in 2024, while commercial vehicles are forecast to post the fastest 37.18% CAGR through 2030.

- By propulsion, battery electric vehicles accounted for 84.15% of the India electric vehicle leasing market size in 2024 and will advance at a 39.64% CAGR to 2030.

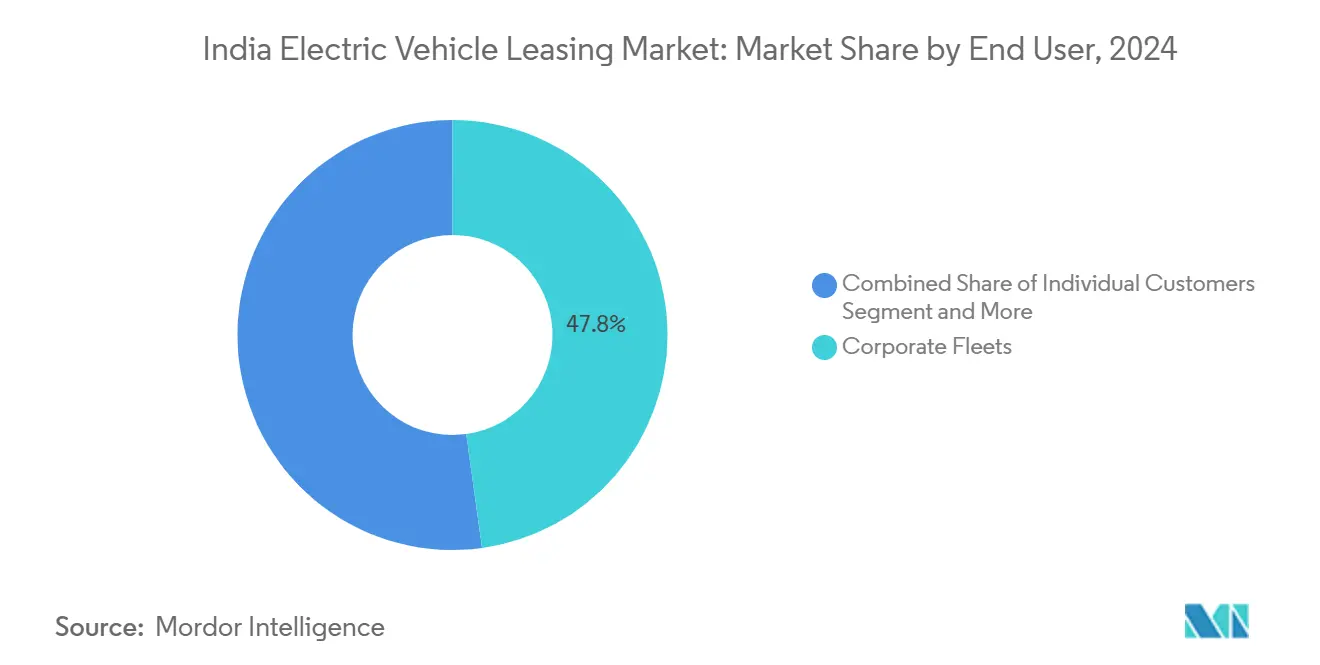

- By end user, corporate fleets commanded 47.82% revenue in 2024, whereas ride-sharing and delivery platforms are projected to record a 35.82% CAGR through 2030.

- By duration, mid-term (1-3 year) contracts made up 52.75% of demand in 2024; long-term leases (above 3 years) exhibit the quickest 35.41% CAGR to 2030.

India contributes to a system defined not by any single country or region but by the interaction of many. The global electric vehicle leasing market data by Mordor Intelligence represents that combined structure.

India Electric Vehicle Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FAME-II and PM E-DRIVE Incentive Alignment | +8.2% | National; Delhi-NCR, Mumbai, Bengaluru | Medium term (2-4 years) |

| Battery Subscription and Swapping Lowers Fleet TCO | +7.5% | Urban hubs; expanding Tier-2 cities | Long term (≥ 4 years) |

| Corporate ESG-linked Fleet Decarbonization Mandates | +6.8% | Metropolitan corporate clusters | Short term (≤ 2 years) |

| OEM-backed Ride-Hailing Supply Contracts | +4.9% | Urban mobility corridors | Medium term (2-4 years) |

| GST Parity on Lease Rentals vs Bank Loans | +4.3% | National | Short term (≤ 2 years) |

| Digital EV Marketplaces Boost Residual Value | +3.7% | Tier-1 with Tier-2 expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing FAME-II and PM-eDrive Incentive Alignment

The policy hand-off from FAME-II to PM E-DRIVE reallocates INR 10,900 crore toward leasing-friendly vehicle types and earmarks INR 2,000 crore for 72,100 fast chargers, directly lowering range-anxiety premiums for lessors [1]Ministry of Heavy Industries, “Scheme Guidelines for PM E-DRIVE,” mhi.gov.in. Corporate buyers gain smoother cash flows through an e-voucher subsidy mechanism, while phased localization rules stabilize supply chains and boost residual-value predictability. The sharpened emphasis on commercial categories nudges procurement toward vans, pickups, and three-wheelers, deepening the India electric vehicle leasing market’s commercial mix.

Battery Subscription and Swapping Lowering TCO for Fleets

Battery-as-a-service programs cut capital outlays by up to 40% versus combustion equivalents, as demonstrated by Vidyut’s INR 2.5 per-kilometer rental offering through its tie-up with JSW MG Motor. Swapping networks, such as SUN Mobility, deliver 3-5 minute turnaround, sustaining high-utilization duty cycles that suit logistics and ride-hail fleets. Standardized pack formats are emerging, enabling cross-OEM interoperability and strengthening uptime guarantees embedded in lease contracts.

Corporate "ESG-Linked" Fleet Decarbonization Mandates

Over 390,000 vehicles are pledged for electrification by EV100 signatories in India, converting ESG goals into binding procurement pipelines [2]The Climate Group, “EV100 Progress Update 2025,” theclimategroup.org. In November 2025, Delhi's new regulations for commercial fleets underscore a growing demand for sustainable practices. Lessors are evolving into sustainability allies, offering real-time emissions dashboards. These tools not only enhance corporate reporting by providing accurate and timely data but also strengthen contract renewals by aligning with clients' environmental goals and compliance requirements.

OEM-Backed Ride-Hailing Supply Contracts (e.g., Uber 25k EV Plan)

Tata Motors and Uber have finalized a framework deal for XPRES-T sedans. Meanwhile, BYD has signed a global supply agreement with Uber, committing to deliver 100,000 units. These agreements guarantee substantial volumes and often come with attractive captive-finance leases, which provide financial flexibility to Uber and its partners. These deals usually include platform-specific telematics and maintenance packages, which are critical in creating significant entry barriers for competitors. These packages are tailored to meet the operational needs of ride-hailing platforms, ensuring seamless integration and efficient fleet management. This dynamic particularly benefits lessors who collaborate with OEMs to co-develop software stacks. By working closely with OEM partners, lessors can ensure that the software solutions are optimized for the platform's requirements, enhancing operational efficiency and strengthening their competitive positioning in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Credit Cost and Limited Refinancing Avenues | -5.8% | National; stronger in Tier-2/3 | Medium term (2-4 years) |

| Public Fast-charging Shortfall versus Demand | -4.2% | High-density urban centers | Short term (≤ 2 years) |

| Lender Wariness Post-BluSmart Default | -3.9% | Nationwide; Delhi-NCR focus | Short term (≤ 2 years) |

| Green Plate Resale Infrastructure Lacking | -2.1% | Tier-2 and rural markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Credit and Limited Refinancing Avenues

Electric car loans carry 8.5-9.5% rates and two-wheelers 18-22%, reflecting ongoing concerns about battery life and resale values. The Asian Development Bank proposes an INR 25 billion loss pool and an INR 4.5 billion guarantee facility to unlock cheaper capital [3]Asian Development Bank, “Accelerating E-Mobility Financing in India,” adb.org. Until such risk-sharing tools scale, lessors must hold thicker equity cushions, constraining fleet growth.

Patchy Public Fast-Charging Uptime (17% Faulty)

Only about 12,100 public chargers serve a fleet that needs 1.32 million points by 2030, signaling a pronounced supply gap. Sparse intercity coverage forces lessors to concentrate deployments in three metros, limiting geographic diversification and elevating routing risk premiums in lease quotes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Gain Velocity

Commercial vehicles contribute a rapidly widening share of the India electric vehicle leasing market, rising at a 37.18% CAGR despite passenger cars still capturing 69.36% of volume in 2024. The India electric vehicle leasing market size for vans, pickups, and three-wheelers is scaling on operational economics—predictable routes and centralized depots let fleets exploit lower running expenses. Delhi’s 2025 clean-fleet mandate accelerates replacement cycles, positioning commercial leasing as a compliance pathway. Battery-swap ecosystems further sharpen uptime, letting logistics players sustain near-ICE rhythms. Concurrently, passenger-car leasing absorbs corporate ESG demand but lags in retail adoption because charging density outside metros remains patchy.

Longer term, product launches such as Switch Mobility’s e-LCVs add breadth and pay-per-kilometer battery rentals temper capital hurdles, narrowing the cost delta with combustion peers. As residual-value models mature, financiers are expected to push multiproduct portfolios that balance predictable commercial cash flows with higher-margin passenger-car contracts.

By Propulsion Type: Battery Electric Vehicles Sustain Momentum

Battery electric vehicles commanded an 84.15% share of the India electric vehicle leasing market in 2024 and are set to advance at a 39.64% CAGR through 2030, reinforcing their position as the technology of choice for fleet operators. The India electric vehicle leasing market size for plug-in hybrid and fuel-cell formats remains limited, largely because their dual-fuel complexity and scarce refueling infrastructure raise residual-value uncertainty. Government policy alignment, notably the PM E-DRIVE incentive’s focus on BEVs and the Production-Linked Incentive for domestic cell manufacturing, continues to narrow cost gaps with internal-combustion alternatives. Lessors benefit from this concentration, since unified propulsion simplifies maintenance contracts and charger partnerships while letting them price uptime guarantees more aggressively.

Ongoing battery-as-a-service pilots further cement BEV economics by stripping out the single largest capital component and alleviating degradation risk. Honda and Mitsubishi’s ALTNA venture illustrates how specialized battery leasing services can extend useful life cycles and enable longer tenors without inflating monthly rentals. Standardized battery packs and expanding fast-charging corridors reduce range-anxiety premiums, letting leasing companies market BEV fleets as functionally equivalent to combustion vehicles in high-utilization duty cycles. As charge-point operators densify urban and freight corridors, the India electric vehicle leasing market share for BEVs is expected to edge higher, pushing hybrids and fuel-cells further toward niche status.

By End User: Platform Economies Accelerate Adoption

Corporate fleets held 47.82% of the Indian electric vehicle leasing market share in 2024, reflecting board-level ESG mandates and clear total-cost advantages when vehicles clock high daily mileage. These programs convert sustainability targets into binding procurement schedules, allowing lessors to lock in multiyear volume contracts and securitize cash flows at competitive spreads. Ride-sharing and delivery platforms—propelled by Uber’s 25,000-vehicle roadmap and Zomato’s push for 100% electric deliveries—are scaling rapidly, leveraging predictable routes, centralized maintenance, and data-rich telematics to maximize asset utilization. Government and individual segments remain smaller but provide reputational lift and policy validation that flow through to commercial demand.

Platform operators increasingly insist on bundled offerings that fold insurance, charging, and battery analytics into a single monthly fee, shifting evaluation criteria from headline rental rates to guaranteed uptime. Leasing firms respond by striking OEM supply contracts and deploying battery-swap tie-ins that cut dwell times to minutes, a critical factor for gig-economy drivers paid per trip. As the digitally used EV marketplaces mature and certify battery health, residual-value risk diminishes, encouraging more aggressive lease structures for app-based fleets. Collectively, these dynamics are carving out a clear hierarchy in the India electric vehicle leasing market size: corporates anchor base demand, platforms drive incremental growth, and smaller segments fill out geographic whitespace.

By Duration: Longer Tenors Signal Rising Confidence

Leases of 1-3 years (mid-term) controlled 52.75% of volume in 2024, balancing depreciation visibility with operational flexibility for fleet managers navigating fast-moving technology cycles. Nevertheless, contracts exceeding 3 years (long-term) are expanding at 35.41% CAGR as battery warranties lengthen and real-world performance data dispel longevity doubts. The India electric vehicle leasing market size tied to long-term agreements benefits from smoother amortization schedules, enabling lessors to quote lower monthly outlays and still protect internal rates of return. Mid-term tenors remain essential for corporates piloting electrification, but the risk premium baked into shorter durations is gradually shrinking as charging infrastructure reliability improves.

OEM-backed programs such as Kia Subscribe, which spans 12-36 months and bundles maintenance with roadside assistance, exemplify the hybrid flexibility customers now expect. Battery health analytics and standardized resale channels further ease concerns about technology obsolescence, letting leasing companies extend warranties and embed guaranteed buyback clauses. As residual-value forecasting improves, insurers are willing to underwrite longer coverage, reducing capital charges for lessors and translating to sharper customer pricing. This virtuous cycle is poised to tilt share toward multi-year contracts, reinforcing the India electric vehicle leasing market share held by providers able to finance and service vehicles over extended horizons.

Geography Analysis

Delhi-NCR, Mumbai, and Bengaluru anchor more than two-thirds of lease originations owing to higher charger density, corporate HQ clustering, and proactive state incentives. Delhi’s subsidy stack and 2025 commercial-fleet mandate catalyze demand spikes, while Mumbai’s financial-services concentration funnels ESG budgets toward electrified employee transport. Bengaluru’s tech ecosystem fosters early-adopter fleets, with companies like Flipkart booking multi-thousand-unit commitments that amplify local charger utilization.

Tier-2 metros—Pune, Hyderabad, and Chennai—form the second wave. Automotive manufacturing legacies supply after-sales talent and accelerate infrastructure rollouts. Alt Mobility’s expansion across 30 cities illustrates how demand radiates outward from franchise charging partnerships and standardized battery packs. Nonetheless, charger-per-vehicle ratios remain stretched, compelling lessors to cluster deployments along freight corridors that guarantee turnaround.

Semi-urban and rural districts lag because public charging is slow, and RTO familiarity with green-plate workflows is limited. The INR 2,000 crore PM E-DRIVE charger fund is earmarked to extend fast charging to highway nodes, a move expected to unlock intercity freight leasing by the late decade. Until then, geographic skew towards metropolitan strongholds will persist, concentrating competitive battles in a few high-density pockets.

The electric vehicle leasing market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe. This is complemented by country-specific insights for Japan, South Korea, and United States, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Competition sits at a middle-fragmented stage: legacy lessors, bank-backed captives, and venture-funded specialists jostle for fleet share against a backdrop of nascent regulation. ORIX Auto Infrastructure Services leverages decades-long OEM ties and nationwide workshops to provide cradle-to-grave fleet management, anchoring its multi-segment portfolio. ALD Automotive complements global purchasing power with India-specific analytics to underwrite battery health and resale. Alt Mobility, a digital-native entrant, bundles telematics, uptime guarantees, and battery-swap access to court high-utilization ride-hail operators.

The BluSmart distress event reshuffled asset ownership, letting acquisitive rivals pick up vehicles at a discount and reinforcing the premium on governance standards. Lenders have tightened covenants, giving well-capitalized lessors an edge. Simultaneously, infrastructure owners—utilities and charge-point operators—are partnering with leasing firms to lock in offtake and build integrated mobility-as-a-service bundles. Macquarie’s USD 1.5 billion platform exemplifies cross-asset financing muscle marshaled to scale both vehicles and chargers.

Strategic collaboration is growing: Tata Motors aligns captive finance with Uber supply contracts, while OEMs increasingly embed embedded-finance APIs into dealer CRMs to accelerate lease approvals. Technology—battery analytics, AI-based residual-value engines, and blockchain provenance—now underpins competitive moats as much as cost of funds. Given low switching friction, customer stickiness hinges on value-added services rather than headline rentals.

India Electric Vehicle Leasing Industry Leaders

Ayvens (ALD Automotive and LeasePlan)

ORIX Auto Infrastructure Services

Tata Capital Leasing

Alt Mobility

Lithium Urban Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Alt Mobility secured growth capital from Beyond Capital Ventures to scale its fleet to 30,000 vehicles and USD 100 million assets under management by March 2027, up from 13,000 vehicles across 30 cities.

- November 2024: Switch Mobility signed an MoU with Vertelo, aiming to deploy 1,000 electric vehicles nationwide over the next 3-5 years through tailored leasing packages.

- October 2024: Alt Mobility entered the commercial four-wheeler passenger segment, targeting employee transport, ride-hail, and tourism operators with bundled lifecycle management.

- July 2024: Kia launched a lease for the EV6 in India at INR 1.29 lakh per month, including insurance, maintenance, pickup-and-drop, and 24×7 roadside assistance.

India Electric Vehicle Leasing Market Report Scope

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| Individual Customers |

| Corporate Fleets |

| Government Agencies |

| Ride-Sharing and Delivery Platforms |

| Short-Term (Less than 12 months) |

| Mid-Term (1–3 years) |

| Long-Term (More than 3 years) |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Propulsion Type | Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles | |

| Fuel-Cell Electric Vehicles | |

| By End User | Individual Customers |

| Corporate Fleets | |

| Government Agencies | |

| Ride-Sharing and Delivery Platforms | |

| By Duration | Short-Term (Less than 12 months) |

| Mid-Term (1–3 years) | |

| Long-Term (More than 3 years) |

Key Questions Answered in the Report

How big is the India electric vehicle leasing market in 2025, and where is it heading?

The market stands at USD 1.19 billion in 2025 and is projected to reach USD 5.33 billion by 2030, growing at a 34.97% CAGR.

Which vehicle category will grow fastest in electric leasing?

Commercial vehicles are set to expand at a 37.18% CAGR through 2030, outpacing passenger cars.

What makes battery electric vehicles dominant in leasing portfolios?

BEVs offer lower maintenance, simpler drivetrains, and benefit from policy incentives, resulting in an 84.15% share and 39.64% CAGR growth.

Why are ride-sharing platforms critical for future leasing demand?

High utilization, predictable routes, and large ESG commitments drive ride-sharing and delivery fleets to a 35.82% CAGR by 2030.

Page last updated on: