South Korea Electric Vehicle Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

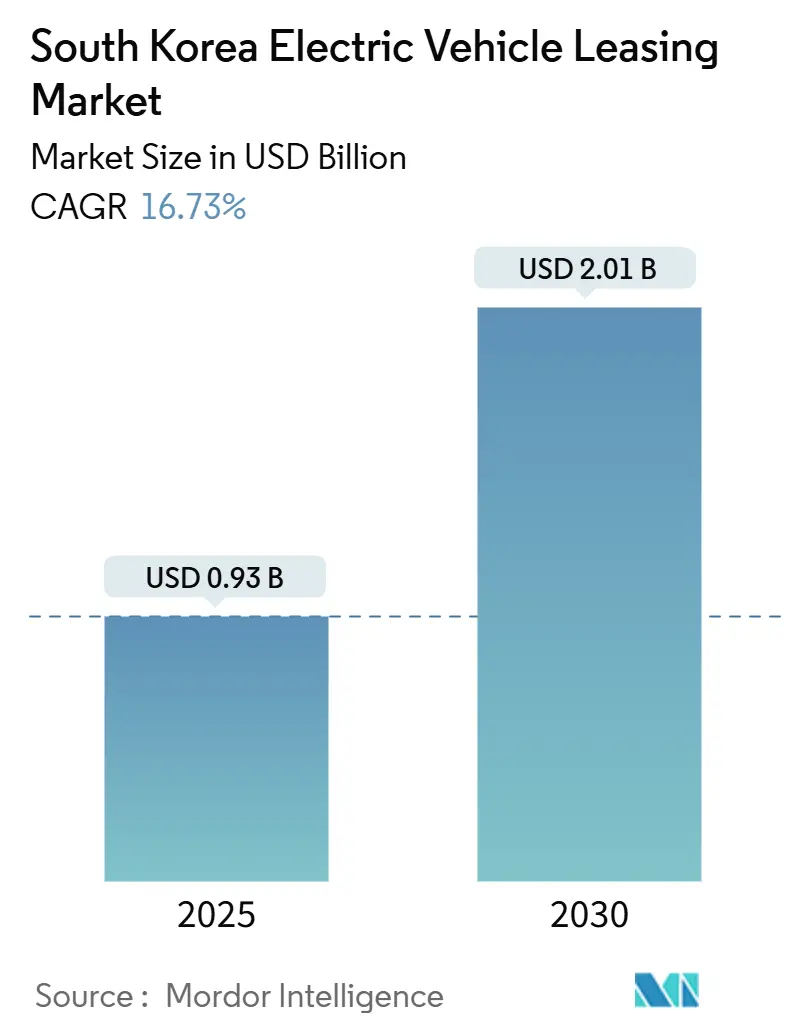

| Market Size (2025) | USD 0.93 Billion |

| Market Size (2030) | USD 2.01 Billion |

| Growth Rate (2025 - 2030) | 16.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Electric Vehicle Leasing Market Analysis by Mordor Intelligence

The South Korea Electric Vehicle Leasing Market size is estimated at USD 0.93 billion in 2025, and is expected to reach USD 2.01 billion by 2030, at a CAGR of 16.73% during the forecast period (2025-2030). Aggressive central-government subsidies, a dense urban fast-charging grid, and battery-residual-value guarantees are converging to accelerate adoption, allowing lessees to bypass enormous upfront costs and battery-degradation risks. Hyundai Capital’s penetration rose from 2019 to 2021, with customers aged 20-30 doubling their share over the same span, underscoring the appeal of flexible access models to younger drivers. Rapid infrastructure rollout and multiple public charging points as of January 2025 have cut the national EV-to-charger ratio to 1.7, reducing range anxiety for retail and fleet users. Captive-finance products that fold 10-year battery residuals into monthly payments now price many leased EVs below gasoline equivalents, reinforcing momentum despite cooling retail demand in the broader auto sector.

Key Report Takeaways

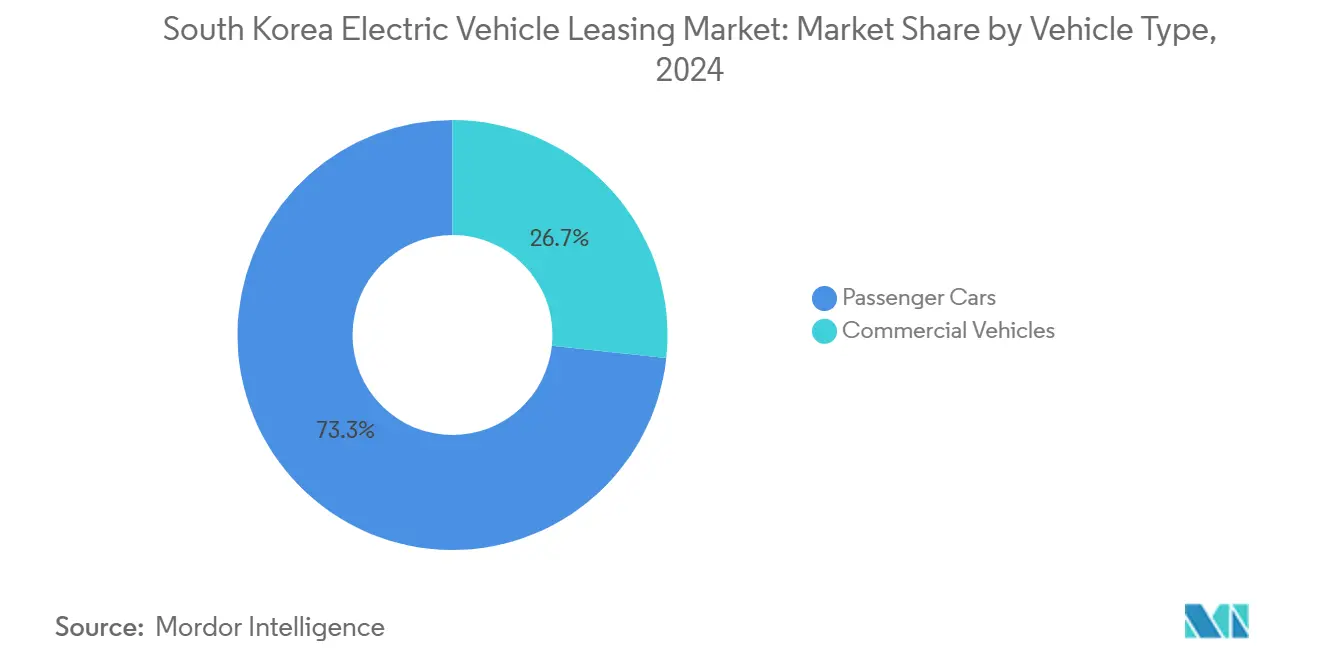

- By vehicle type, passenger cars held 73.28% of the South Korea electric vehicle leasing market share in 2024, while commercial vehicles are advancing at a 16.81% CAGR through 2030.

- By propulsion, battery electric vehicles accounted for 86.14% of the South Korea electric vehicle leasing market in 2024; fuel-cell models register the fastest 16.88% CAGR to 2030.

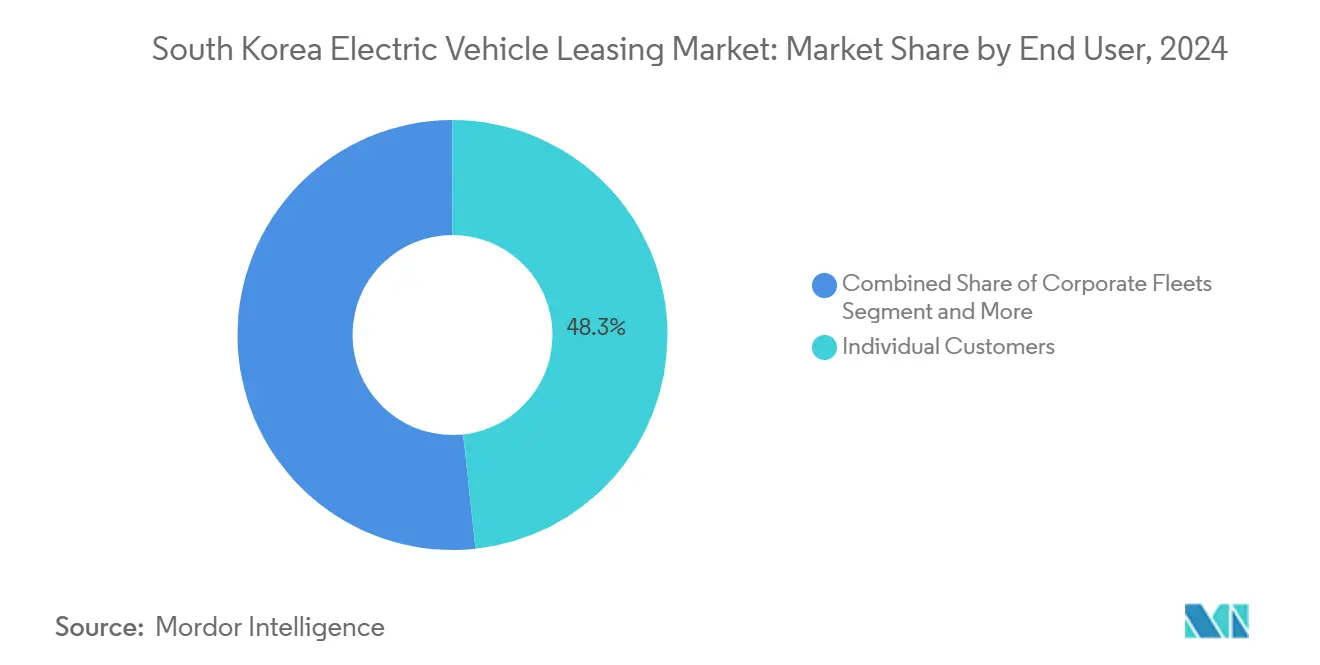

- By end user, individual drivers represented 48.29% of 2024 demand, whereas ride-sharing and delivery platforms are accelerating at a 16.94% CAGR.

- By lease duration, mid-term contracts (1-3 years) captured 55.16% of the 2024 South Korea electric vehicle leasing market size, but short-term options (<12 months) posted a 16.97% CAGR.

Competitive positioning in South korea includes both locally based firms and those operating across multiple regions. The market landscape in the global electric vehicle leasing industry research shows how these players are arranged internationally.

South Korea Electric Vehicle Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government EV Purchase | +3.2% | National, concentrated in Seoul metropolitan area | Medium term (2-4 years) |

| Rapid Build-Out Of Nationwide Fast-Charging Network | +2.8% | National, priority in urban centers | Short term (≤ 2 years) |

| OEM Captive Finance Arms Bundling Low-Apr EV Leases | +2.4% | National, stronger in corporate segments | Short term (≤ 2 years) |

| Tax Incentives And Zero-Emission Zones | +2.1% | Seoul, Busan metropolitan areas | Medium term (2-4 years) |

| Battery Residual-Value Guarantees | +1.8% | National, early adoption in premium segments | Long term (≥ 4 years) |

| Software-Defined Vehicles Enabling OTA Upgrades | +1.4% | National, tech-forward demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government EV Purchase & Battery-Lease Subsidies

Maximum purchase aid of KRW is 6.5 million for locally produced EVs priced below KRW 55 million, now coupled with expanded corporate discounts covering up to 80% of fleet costs, directly lowering lease outlays for businesses. Hyundai Capital’s Battery Care Lease layers these incentives onto a 60-month contract that embeds a 10-year residual guarantee, cutting monthly payments beneath gasoline equivalents for the Casper Electric. The Ministry of Trade, Industry, and Energy program supporting battery-material localization is trimming upstream costs that ultimately filter into lower leases[1]“Battery Material Localization Initiative,” Ministry of Trade, Industry and Energy, motie.go.kr . Foreign investors establishing Korean leasing ventures can obtain cash grants covering three-fifths of capex alongside seven-year tax holidays, widening capital access.

Rapid Build-Out Of Nationwide Fast-Charging Network

Public chargers expanded by roughly 100,000 annually since 2021, bringing the installed base to 405,000 by January 2025 and achieving an EV-to-charger ratio of 1.7, the tightest in the OECD. The 2025 central budget allocates for rapid units and smart slow chargers—up around two-fifths on 2024—which concentrates capacity at logistics depots and shopping districts favored by lessees. Chaevi’s commercial launch of 400 kW units in 2024 trims around four-fifths of charge times, making short-term leases viable for delivery fleets[2]“Launch of 400 kW Ultra-Fast Charger,” Chaevi, chaevi.co.kr. PlugLink’s May 2025 purchase of Hanwha Solutions’ charging portfolio expands its network past 30,000 stations, enabling bundled charger-plus-vehicle lease offers. The Megawatt Charging System program, targeting 2028 heavy-duty deployment, further lifts the commercial leasing outlook.

OEM Captive Finance Arms Bundling Low-Apr EV Leases

Hyundai Capital’s Battery Care Lease provides fixed annual mileage, remote battery-health telemetry, and guaranteed repurchase, leveraging data unavailable to stand-alone lessors. Genesis Finance extends similar low-APR packages to premium buyers, while Kia’s e-Life bundles charging credits and resale guarantees into PV5 leases, reinforcing captive-finance control over customer lifetime value. SK Rent-a-Car counters with three-fifths off Tesla Model 3 rates, showing how independent players react to captive pressure. This financing innovation is boosting adoption by roughly 2.4 percentage points.

Tax Incentives & Zero-Emission Zones In Seoul, Busan

Seoul’s zero-emission zones restrict ICE entry and impose a four-fifths battery-charge cap for indoor parking, nudging operators toward managed fleet leases that centralize compliance monitoring[3]“Zero-Emission Zone Ordinance,” Seoul Metropolitan Government, seoul.go.kr . A reduced consumption tax through June 2025 offers immediate cost relief to leasing firms purchasing fleet vehicles. Busan mirrors policy with hydrogen-bus quotas that intersect with fuel-cell leasing demand, as 1,000 units are scheduled by 2027. Lane-priority proposals for EVs on expressways could slice delivery times, elevating commercial lease value propositions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cooling Retail Demand | -2.3% | National, concentrated in premium segments | Medium term (2-4 years) |

| Elevated EV Insurance Premiums | -1.9% | National, higher impact in urban areas | Short term (≤ 2 years) |

| Critical-Mineral Supply Constraints | -1.5% | National, supply chain dependent regions | Long term (≥ 4 years) |

| Over-Installation Of Low-Utilisation Public Chargers | -1.2% | Urban centers, early infrastructure deployment areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cooling Retail Demand & Falling Used-EV Prices

Tesla sold only one unit nationwide in January 2024, and overall EV registrations dropped slightly in H1 2024, signaling demand fatigue. Hyundai paused Ioniq 5 output as inventories swelled, while EV sales fell drastically year-over-year, underscoring structural weakness in retail appetite. Used-EV listings surged exponentially after safety scares, driving residual values downward—directly undermining leasing balance-sheet assumptions. Battery suppliers mirror the slump: SK On’s more than half of revenue slide in 2024 speaks to upstream stress that constrains price flexibility.

Elevated EV Insurance Premiums

Average annual EV insurance for gasoline cars is driven by repair bills that average fairly, and battery replacements have increased exponentially. Loss ratios hit around four-fifths in past years, prompting insurers to hike rates and forcing lessors to absorb or pass on costs. Samsung Fire & Marine is piloting EV-specific products, but actuarial data remain thin, keeping premiums high. High-profile incidents—such as the Mercedes-Benz EQE parking-garage fire—have triggered safety rules that cap charge level to 80% in Seoul-run facilities, feeding insurer risk models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Acceleration

Commercial vehicles remain the fastest-growing slice, tracking a 16.81% CAGR, even though passenger cars dominated the 2024 South Korea electric vehicle leasing market share at 73.28%. Seoul’s plan to convert multiple buses to hydrogen by 2027 under a Hyundai-KD Transportation-SK E&S pact translates into predictable multi-year fleet contracts. SOCAR’s corporate program with KEPCO replaces owned vans with shared EVs, offering three-fifths weekday discounts, underlining the cost advantage over self-managed assets. OEM focus is pivoting: Kia’s PV5, slated for H2 2025 launch, provides modular Cargo and Chassis Cab variants, blurring lines between passenger and light-commercial to capture urban-delivery demand. Subsidies that now cover up to 80% of corporate EV costs multiply commercial viability.

Passenger cars, while slowing, remain the bedrock of the South Korean electric vehicle leasing market. Mid-term contracts suit household budgeting, locking predictable payments at below-ICE totals thanks to residual-value guarantees. As chip shortages ease, some buyers migrate back to ownership, but OTA-upgradable models keep leases relevant by delivering continual feature refreshes. Overall, the South Korean electric vehicle leasing market size for passenger cars is projected to maintain double-digit growth even as commercial categories sprint ahead.

By Propulsion Type: Hydrogen Emerges Despite Battery Dominance

Battery electric vehicles captured 86.14% of the 2024 South Korean electric vehicle leasing market, reflecting mature charging networks and a deep OEM lineup. Leasing economics benefit from falling cell costs. Upcoming models promising a 900 km range in 2026 will further stretch BEV competitiveness. Government mandates that tie maximum subsidies to vehicle-to-load capability also favor BEVs, whose hardware readily supports bidirectional charging.

Fuel-cell EVs, while niche, log the quickest 16.88% CAGR to 2030, propelled by heavy-duty use cases. April 2024 saw the Incheon Gajwa liquefied-hydrogen station open with 120 kg-per-hour throughput—enough for 120 buses daily—boosting confidence in fleet leasing economics. Plans for 280 hydrogen stations by 2030 signal infrastructure readiness that mitigates range-anxiety disadvantages. Busan’s hydrogen-bus rollout dovetails with these targets, pushing commercial lessors to secure early mover slots despite higher fuel costs, downtime savings from five-minute fills versus DC fast charging tipping the total-cost balance for high-utilization operators.

By End User: Platforms Accelerate Beyond Individual Adoption

Ride-sharing and delivery platforms are expanding at a 16.94% CAGR through 2030, though individuals still accounted for 48.29% of 2024 demand in the South Korean electric vehicle leasing market. SOCAR has installed exclusive “Socar Zones” at KEPCO sites, giving corporate clients guaranteed access and bundled power tariffs. A Seoul pilot showing e-bike couriers cutting delivery costs by more than one-tenth versus trucks underscores the economics favoring electrified fleets. Platforms also value short-term contracts that match seasonal demand patterns, pushing lessors to develop month-to-month packages.

Individual adopters gravitate toward mid-term leases, balancing affordability and flexibility. The eco-friendly vehicle cohort outsold ICE models for the first time in May 2025, indicating mainstream inflection. Battery-care guarantees are especially persuasive for households wary of depreciation. OTA upgradeability further reduces perceived obsolescence risk, letting drivers refresh features during the term rather than swapping cars. Subsidy rules that grade OEM after-sales service quality encourage established lessors to showcase robust support, reinforcing consumer trust.

By Lease Duration: Flexibility Drives Short-Term Growth

Short-term contracts below 12 months post the highest 16.97% CAGR, capturing customers who want trial access during tech churn and resale uncertainty. SK Rent-a-Car’s three-fifths discounted Tesla Model 3 campaign exemplifies how rental hybrid models foster rapid uptake among undecided buyers. OTA-enabled feature upgrades reduce lock-in; users can experience evolving software without committing to multi-year depreciation.

Mid-term leases retain 55.16% of the 2024 South Korea electric vehicle leasing market share by aligning payment schedules with typical three-year household budgeting cycles. Captive lessors tune residual values precisely, leveraging proprietary battery-health analytics. Long-term contracts beyond three years face headwinds from rapid model cycles, yet SDV roadmaps may extend asset life by decoupling hardware from feature evolution. Fleet operators, prioritizing fixed-cost visibility, continue to sign four-to-five-year terms despite tech obsolescence risk, creating a balanced portfolio for lessors.

Geography Analysis

Seoul metro remains the epicenter of the South Korea electric vehicle leasing market, absorbing a disproportionate share of fast-charger budget and hosting the nation’s only zero-emission zone policy to date. The city’s ambition to place 400,000 EVs on roads by 2026 assures dense utilization for leasing fleets stationed in satellite Gyeonggi cities. High-rise parking regulations that limit charging above four-fifths favor professional fleet management over individual ownership, further anchoring lease growth.

Busan follows with a hydrogen-bus deployment that dovetails with the fastest-growing fuel-cell lease segment. The port city’s logistics concentration and ongoing zero-emission zone design bolster demand among last-mile operators intrigued by quick hydrogen refuel times. Incheon, home to Korea’s first liquefied-hydrogen station, positions itself as a strategic pivot for fuel-cell buses serving airport routes and coastal freight, widening geographic spread.

Secondary cities such as Daegu and Daejeon benefit from OEM manufacturing clusters and provincial incentives tied to job creation. Ulsan, hosting Hyundai’s central plant, sees employee lease programs that bundle payroll deductions, lifting penetration among factory workers. Rural regions lag in charger density, but government grants offset up to half of installation costs for village co-ops, hinting at future uptake. Overall, the South Korean electric vehicle leasing market exhibits spatial diffusion outward from the capital while retaining a Seoul-centric core.

Mordor Intelligence tracks the electric vehicle leasing market across other major regions such as Europe, with additional country-level coverage spanning Japan, India, and United States, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The market shows moderate concentration: captive finance arms of Hyundai, Kia, and Genesis control roughly three-fifths of active contracts, while top five players together hold nearly four-fifths share. Hyundai Capital differentiates through battery-health telemetry and guaranteed buy-backs, reinforcing brand stickiness. Lotte Rental and SK Rent-a-Car expand aggressively via promotional pricing and bundled insurance, challenging captives on cost rather than tech.

Platform-based entrants such as SOCAR and Kakao Mobility shift competition toward service layers—dynamic routing, shared charging reservations, and integrated payment wallets. Infrastructure operators like PlugLink are vertically integrating by offering charger-plus-vehicle subscription bundles, leveraging 30,000-unit networks to claim gatekeeper economics. Token-based financing pilots from Korea ST Trading aim to securitize charger cash flows, potentially lowering capex costs for smaller lessors.

Software competence is becoming a key competitive divider, as OEMs with proprietary SDV stacks can deliver OTA updates that enhance residuals, while independents must license platforms, increasing costs. Regulatory requirements linking subsidy eligibility to after-sales service further advantage incumbents with nationwide workshops. Nonetheless, niche specialists exploiting hydrogen-commercial segments or subscription-based infotainment may peel share from mainstream players.

South Korea Electric Vehicle Leasing Industry Leaders

Lotte Rental

SK Rent-a-Car

Hyundai Capital

KB Capital

Shinhan Capital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PlugLink acquired Hanwha Solutions’ EV-charging division, adding 14,000 units to surpass 30,000 chargers nationwide.

- February 2025: Kia unveiled the PV5, a modular Platform Beyond Vehicle for Korean and European deliveries in H2 2025.

- September 2024: Hyundai Motor and Kia initiated a four-year project with Hyundai Steel and EcoPro BM to localize lithium-iron-phosphate cathode production.

South Korea Electric Vehicle Leasing Market Report Scope

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Individual Customers |

| Corporate Fleets |

| Government Agencies |

| Ride-Sharing & Delivery Platforms |

| Short-Term (< 12 months) |

| Mid-Term (1–3 years) |

| Long-Term (> 3 years) |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Propulsion Type | Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) | |

| Fuel-Cell Electric Vehicles (FCEV) | |

| By End User | Individual Customers |

| Corporate Fleets | |

| Government Agencies | |

| Ride-Sharing & Delivery Platforms | |

| By Lease Duration | Short-Term (< 12 months) |

| Mid-Term (1–3 years) | |

| Long-Term (> 3 years) |

Key Questions Answered in the Report

What is the current value of the South Korean electric vehicle leasing market?

The market is valued at USD 0.93 billion in 2025 and is projected to reach USD 2.01 billion by 2030.

How fast is the market expected to grow?

It is forecast to expand at a 16.73% CAGR through 2030, driven by subsidies, charging density, and innovative leasing models.

Which vehicle segment is growing the fastest?

Commercial vehicles show the highest growth, posting a 16.81% CAGR due to fleet electrification mandates and cost advantages.

Why are fuel-cell electric vehicles gaining ground?

Despite a small current volume, the government plans for 280 hydrogen stations and dedicated bus programs are pushing fuel-cell models to a 16.88% CAGR.

What role do software-defined vehicles play in leasing?

OTA upgrades keep vehicles technologically current during the lease term, boosting residual values and lessee satisfaction.

How concentrated is the competitive landscape?

The top five lessors hold about four-fifths of the market, indicating moderate concentration with room for niche entrants focusing on service differentiation.

Page last updated on: