Europe Electric Vehicle Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

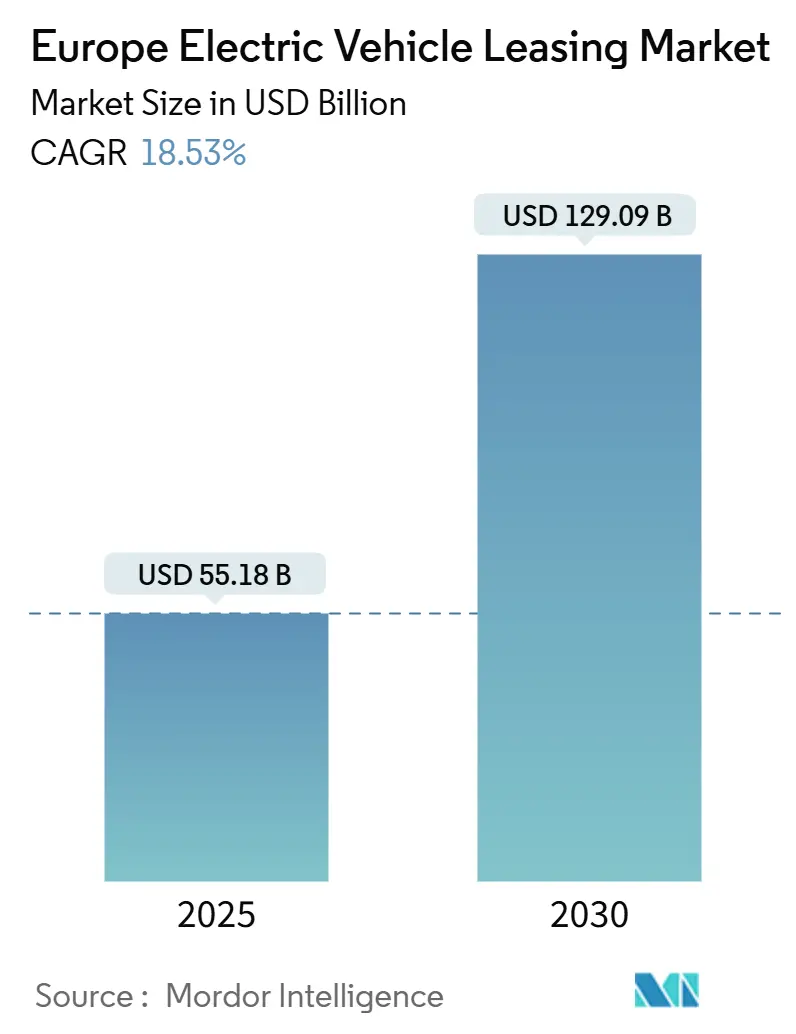

| Market Size (2025) | USD 55.18 Billion |

| Market Size (2030) | USD 129.09 Billion |

| Growth Rate (2025 - 2030) | 18.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electric Vehicle Leasing Market Analysis by Mordor Intelligence

The European Electric Vehicle Leasing Market size is estimated at USD 55.18 billion in 2025, and is expected to reach USD 129.09 billion by 2030, at a CAGR of 18.53% during the forecast period (2025-2030). Steady policy backing, corporate sustainability mandates, and fast-growing public-charging networks have cemented leasing as the dominant acquisition route for battery-powered transport across the region. Volkswagen Financial Services confirmed that leasing accounts for over half of all new electric-vehicle registrations, underscoring a structural preference for off-balance-sheet financing that de-risks business residual-value exposure. Product differentiation now rests on flexible contract lengths, embedded charging packages, and battery-health transparency, which lower the total ownership costs for fleet operators. Heightened consolidation, led by the ALD–LeasePlan tie-up, concentrates buying power and accelerates digital innovation in risk analytics. Headwinds revolve around subsidy rollbacks and volatile used-EV pricing; however, offsetting measures such as buy-back guarantees and the forthcoming EU Battery Passport offer clear pathways to steadier residual-value forecasts.

Key Report Takeaways

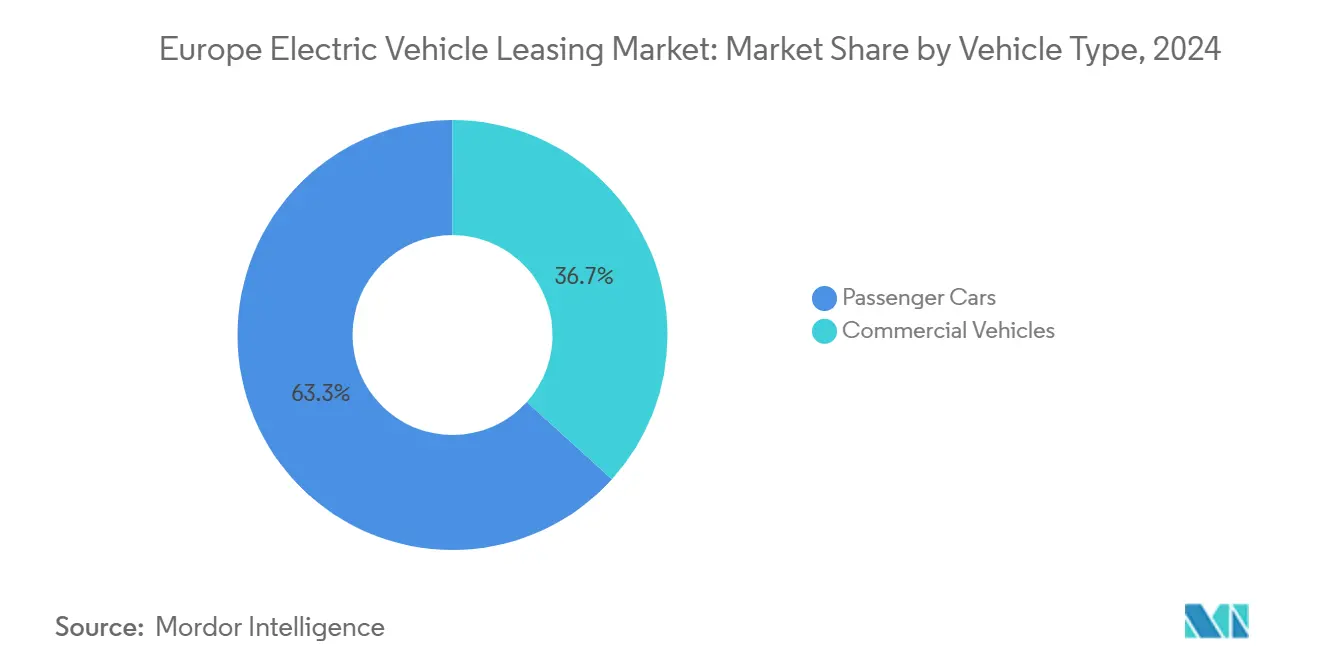

- By vehicle type, passenger cars accounted for 63.27% share of the European electric vehicle leasing market size in 2024; commercial vehicles are projected to rise at an 18.88% CAGR to 2030.

- By propulsion type, battery electric vehicles dominated with 72.16% share of the European electric vehicle leasing market size in 2024, whereas fuel-cell electric vehicles are advancing at an 18.93% CAGR through 2030.

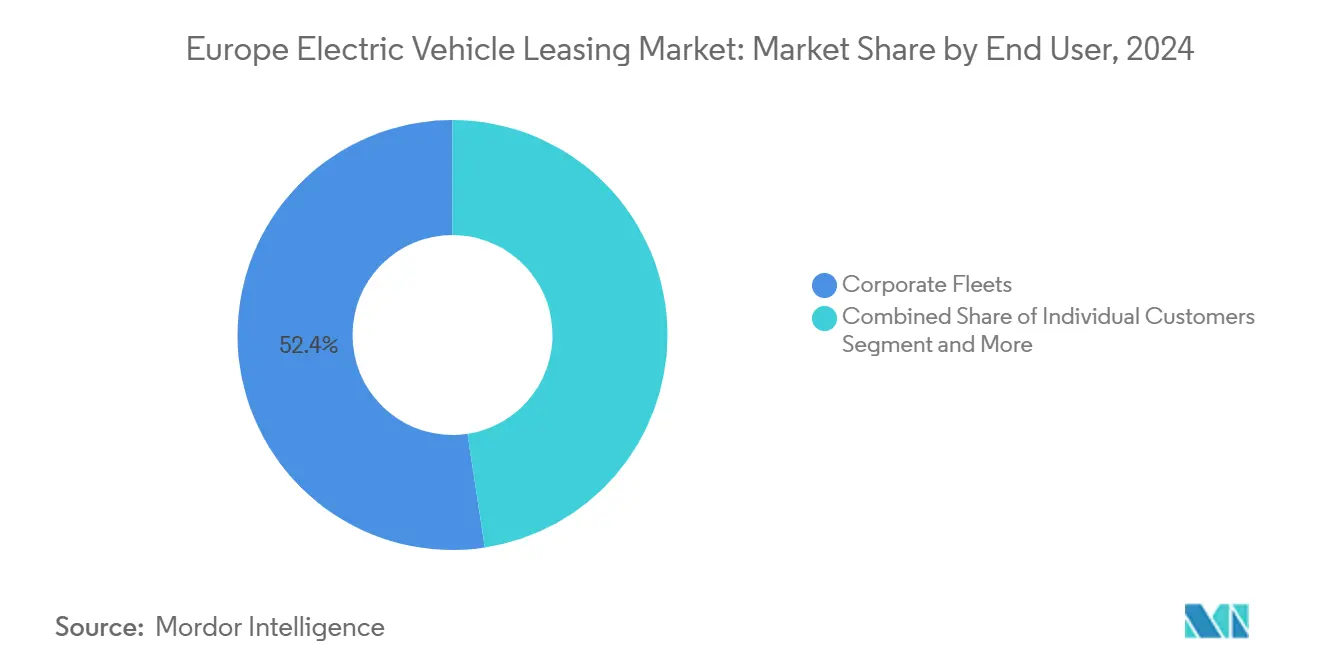

- By end user, corporate fleets retained 52.37% of the European electric vehicle leasing market share in 2024, while ride-sharing and delivery platforms are expanding at a 19.04% CAGR to 2030.

- By duration, mid-term leases (1-3 years) commanded 48.75% of the European electric vehicle leasing market size in 2024, while short-term contracts under 12 months are growing fastest at an 18.94% CAGR through 2030.

- By geography, Germany led with 26.17% of the European electric vehicle leasing market share in 2024; France is on course for the highest 18.71% CAGR to 2030.

Proportional positioning is established by comparing regional contributions against the global total, including that of Europe. The electric vehicle leasing market share in our global report expresses these relative weights.

Europe Electric Vehicle Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate Sustainability-Driven Fleet Electrification | +4.1% | Global, strongest in Germany, France, UK | Long term (≥ 4 years) |

| Fiscal Incentives and Bik Tax Advantages | +3.2% | UK, Germany, Netherlands, Belgium | Medium term (2-4 years) |

| Telematics-Driven Residual-Value Optimisation | +2.3% | Global, led by Nordic markets | Medium term (2-4 years) |

| OEM Battery-Health Certification Platforms | +1.9% | EU-wide, strongest in Germany, France | Medium term (2-4 years) |

| Social-Leasing Programmes | +1.8% | France, Germany, expanding to Italy, Spain | Short term (≤ 2 years) |

| FCEV Pilot Lease Schemes | +0.7% | Germany, Netherlands, Ireland, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate Sustainability-Driven Fleet Electrification

Environmental, Social, and Governance commitments now dictate procurement. A coalition of leasing and mobility firms has lobbied the European Commission for binding targets to obligate large fleets to buy 100% zero-emission vehicles by 2030[1]“Corporate fleet electrification targets,” Transport & Environment, transportenvironment.org . Around one-fifths of company-car registrations in the United Kingdom were electric in 2023, and corporate buyers generated three-quarters of all domestic EV sales. Arval and BYD have struck supply agreements that pair vehicle deliveries with advisory services, showing how leasing companies are positioning themselves as full-service electrification partners. As fleet cars typically defleet after three to four years, they funnel a healthy supply of used EVs into the secondary market, thereby improving affordability for private households.

Fiscal Incentives & Bik Tax Advantages For EV Leases

Persistent tax relief propels the European electric vehicle leasing market by lowering effective monthly outlays for business users. The United Kingdom has locked Benefit-in-Kind on zero-emission company cars at a decent rate for fiscal 2025–26, moving up just six points over the next four years, which anchors multi-year lease planning[2] “Benefit-in-kind rates for company cars,” GOV.UK, gov.uk. Germany’s revised framework lifts the price cap for favorable company-car taxation to around a lakh EUR and permits two-fifths first-year depreciation, a boon for premium electric models. Belgium’s acquisition grants and the Netherlands’ BPM exemptions create parallel boosts. Because lease providers capture these fiscal gains directly, they can pass them on via lower rentals, making leasing structurally more attractive than outright purchase.

Telematics-Driven Residual-Value Optimisation

The European electric vehicle leasing industry increasingly relies on real-time battery data to underwrite depreciation risk. Black Book’s Battery Adjusted Values, the first valuation tool that layers state-of-charge and degradation metrics onto pricing algorithms, shows that transparent battery health can lift used-vehicle proceeds[3]“Battery Adjusted Values,” Black Book, blackbook.com . Parliamentary studies in the UK found three-fifths of consumers hesitant to buy used EVs because of battery-life anxiety, validating the need for objective data. Leasing firms are tying telematics feeds into predictive maintenance regimes, thereby sharpening their disposal strategies and improving profitability.

OEM Battery-Health Certification Platforms

Starting January 2026, the EU Battery Passport will assign a digital ID to every traction battery over 2 kWh, logging performance and lifecycle footprint[4]“Battery Passport Regulation,” European Commission, europa.eu. Many OEMs are racing to build commercial certification ecosystems around this mandate. Extended warranties and standardized health checks should narrow valuation bands at lease end, encouraging more aggressive residual-value assumptions in the European electric vehicle leasing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy-Withdrawal Shock | -4.1% | Germany, Netherlands, reducing in France | Short term (≤ 2 years) |

| Volatile BEV Residual Values | -3.4% | Global, particularly Germany, UK, France | Medium term (2-4 years) |

| Public-Charging Infrastructure Gaps | -2.8% | Rural areas across EU, strongest impact in Eastern Europe | Short term (≤ 2 years) |

| Battery-Recycling Fee Escalation Risk | -1.2% | EU-wide, strongest in Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subsidy-Withdrawal Shock In Key EU Markets

Germany’s abrupt halt to the Umweltbonus in December 2023 triggered around two-fifths of the slump in EV registrations by mid-2024. France trimmed corporate incentives and paused its social-leasing budget, while the Netherlands dialed back plug-in hybrid support. OEMs responded with price discounts of up to EUR 10,000, which compresses lease profitability and complicates residual-value forecasts. A clear, long-term subsidy roadmap is vital for demand stability in the European electric vehicle leasing market.

Volatile BEV Residual Values & Price Erosion

OEM price cuts, most visibly by Tesla, have shaken the used-EV market. Leasing leaders Ayvens and Arval now negotiate buy-back guarantees to cushion depreciation. Demand for residual-value insurance rises, while financial institutions reassess EV risk exposure. Hertz’s decision to offload 20,000 EVs in the United States underscores global fragility. Until secondary prices stabilize, lease rates will stay above diesel equivalents in several high-volume markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Scale Rapidly

Commercial vehicles captured a smaller slice of Europe's electric vehicle leasing market than passenger cars in 2024, yet their 18.88% CAGR to 2030 outpaces all other groups. Lease structures match predictable delivery routes, centralized charging depots, and stringent corporate CO₂ targets, making electrification economically rational for logistics operators. Passenger cars maintain a 63.27% share due to entrenched corporate-car benefit schemes in Germany, the UK, and France. However, growth moderates as premium segments mature and OEMs pivot production toward crossovers and vans.

Commercial operators value flexibility and residual-value certainty, which leasing satisfies via variable-term contracts and guaranteed maintenance. High-utilization duty cycles amplify fuel savings versus diesel, shortening payback periods. Conversely, passenger-car leasing pivots toward subscription offerings that bundle insurance and charging access. As subscription contracts rarely exceed 12 months, they will reinforce the trend toward shorter lease tenors and more frequent fleet refresh.

By Propulsion Type: FCEV Momentum Builds

Battery electric vehicles held a 72.16% share of the European electric vehicle leasing market in 2024, underpinned by dense charging grids in Northern Europe and manufacturer portfolio breadth. Ayvens disclosed that BEV deliveries climbed around two-fifths of its intake over the past year, confirming mainstream acceptance. Fuel-cell electric vehicles, while nascent, register the fastest 18.93% CAGR through 2030, leveraging superior range and refueling speed for long-haul freight. Government grants in Ireland and Germany underwrite pilot fleets, lowering the total cost of ownership to parity with diesel on specific routes. Plug-in hybrids face shrinking policy support as Brussels pushes for pure-zero-emission compliance, limiting their future lease share.

Infrastructure remains the swing factor. BEV success springs from home-charging availability and a critical mass of 350 kW fast chargers along motorways. FCEV growth depends on hydrogen station density, projected to exceed 2,000 EU sites by 2030 under current plans. As refueling networks expand, leasing companies will likely offer mixed BEV-FCEV portfolios to optimize duty cycles across use cases.

By End User: Platform Operators Uplift Demand

Corporate fleets controlled 52.37% of the European electric vehicle leasing market in 2024, shaped by stringent ESG scorecards and fleet-wide CO₂ ceilings. Ride-sharing and last-mile delivery platforms are scaling faster at a 19.04% CAGR as electric drivelines slash per-kilometer energy costs and satisfy city low-emission-zone rules. Uber’s European Green Future program subsidizes electric-vehicle rentals for drivers, while courier groups like DPD roll out depot-based charging partnerships that dovetail with lease packages.

Individual consumers benefited from France’s social-leasing pilot, revealing significant pent-up demand at monthly payments under EUR 100. When the scheme is reinstated in 2025, uptake should broaden markedly. Government-agency procurement remains steady but slower, constrained by public-tender cycles and budget scrutiny. Nevertheless, national zero-emission vehicle mandates for municipal fleets should ensure long-term volume visibility.

By Duration: Short-term Contract Surge

Mid-term leases still accounted for 48.75% of the European electric vehicle leasing market size in 2024, but sub-12-month contracts are growing fastest at 18.94% CAGR. Rapid battery-tech upgrades and residual-value uncertainty drive customers toward flexibility. Short tenors let businesses trial electric vans without full depreciation risk, while digital-native consumers appreciate the ability to switch models annually. Lease providers counterbalance shorter revenue tails by bundling charging subscriptions and maintenance upsells, widening per-unit margin.

Long-term leases remain relevant for cost-sensitive SMEs that prize lower monthly outgoings. Yet the overall mix heads toward variable-term solutions, coinciding with the broader shift from ownership to usership across European mobility culture.

Geography Analysis

Germany held a 26.17% share of the European electric vehicle leasing market in 2024, driven by its domestic OEM base and deep corporate car culture. Terminating the Umweltbonus led to a sharp decline in registrations, but new tax incentives for company cars, combined with a moderate price ceiling, are helping to stabilize demand. BMW will launch NEUE KLASSE production in late 2025, aiming to capture over half of BEV sales by 2030. Volkswagen Financial Services also reports that BEV contracts now exceed those for diesel among new fleet deals, highlighting a structural shift.

France posts the region’s fastest 18.71% CAGR through 2030, driven by the high-profile rollout of social leasing and continued ecological incentives for new BEVs. Domestic OEM conglomerate Stellantis offers a local sourcing advantage, while an expanding charging grid underpins consumer confidence. The government intends to reopen the social scheme in 2025, fueling extended momentum.

The United Kingdom benefits from enduring Benefit-in-Kind rates on zero-emission company cars and the statutory ZEV sales mandate. Leasing penetration already tops three-fifths of corporate registrations. Italy and Spain each employ eco-incentive pools encouraging adoption, although infrastructure gaps linger outside metropolitan centers. Nordic markets continue to lead per-capita uptake, whereas much of Eastern Europe trails due to limited purchasing power and sparse public charging. EU cohesion funding earmarked for e-mobility infrastructure aims to narrow this divide over the next decade.

Mordor Intelligence examines the electric vehicle leasing market across diverse other regional markets as well, offering granular country-level perspectives for Japan, India, United States, and South Korea and more.

Competitive Landscape

The top seven lessors now supervise two-fifths of the vehicles and generate a fairly decent profit margin, reflecting efficient capital recycling and scale buying. The ALD–LeasePlan merger formed Ayvens with several vehicle parks across multiple countries and a EUR 440 million annual synergy target by 2026. Alphabet reported more than two-fifths of its 2025 contract intake is electric, evidencing a pivot toward zero-emission portfolios. Technology investment focuses on AI-driven pricing, battery-health analytics, and mobile-first customer journeys.

White-space growth lies in national social-leasing tenders, hydrogen truck pilot contracts, and turnkey charging-lease bundles. Disruptors such as Onto and Finn offer subscription-only models that prioritize month-to-month flexibility. Incumbents respond by launching variable-term products and integrating telematics platforms that couple predictive maintenance with carbon-reporting dashboards.

OEM tie-ups are pivotal; Arval’s deal with BYD secures supply, while SIXT’s Stellantis agreement locks price and residual-value protection. Market concentration is climbing but remains moderate, presenting ongoing entry opportunities for niche specialists.

Europe Electric Vehicle Leasing Industry Leaders

LeasePlan

Arval

Ayvens

Volkswagen Financial Services

Sixt Leasing

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BMW Group is set to unveil its Neue Klasse technology platform, aiming to support around 40 new or refreshed models by 2027. This move is strategically designed to rival Chinese firms and position BMW as a frontrunner in fully electric vehicles.

- February 2025: Transport & Environment urged the European Commission to mandate 100% zero-emission corporate fleets by 2030 and heavy-vehicle electrification by 2035.

- January 2025: Volkswagen, in partnership with Volkswagen Financial Services, has launched a special leasing initiative dubbed "Drive electric – drive ID.3." Starting now, private customers and select commercial lessees can access the all-electric ID.3 models, Pro and Pro S, at notably reduced monthly rates. This enticing offer extends to the exclusive GOAL special-edition models as well.

Europe Electric Vehicle Leasing Market Report Scope

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Individual Customers |

| Corporate Fleets |

| Government Agencies |

| Ride-Sharing & Delivery Platforms |

| Short-Term (< 12 months) |

| Mid-Term (1–3 years) |

| Long-Term (> 3 years) |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Rest of Europe |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Propulsion Type | Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) | |

| Fuel-Cell Electric Vehicles (FCEV) | |

| By End User | Individual Customers |

| Corporate Fleets | |

| Government Agencies | |

| Ride-Sharing & Delivery Platforms | |

| By Duration | Short-Term (< 12 months) |

| Mid-Term (1–3 years) | |

| Long-Term (> 3 years) | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the European electric vehicle leasing market in 2025?

The European electric vehicle leasing market stood at USD 55.18 billion in 2025 and is projected to reach USD 129.09 billion by 2030.

What is the forecast growth rate for electric-vehicle leasing in Europe?

The market is set to expand at an 18.53% CAGR between 2025 and 2030.

Which country leads the regional leasing volume?

Germany led with a 26.17% share of total contracts in 2024, aided by a strong domestic OEM base and tax incentives for company cars.

Which segment is growing fastest by propulsion?

Fuel-cell electric vehicles show the highest 18.93% CAGR through 2030 owing to their suitability for long-haul and heavy-duty use cases.

Why are short-term lease contracts gaining favor?

Rapid battery-technology cycles and residual-value uncertainty push many fleets and consumers toward contracts shorter than 12 months, which are expanding at an 18.94% CAGR.

Page last updated on: