United States Electronic Health Records Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

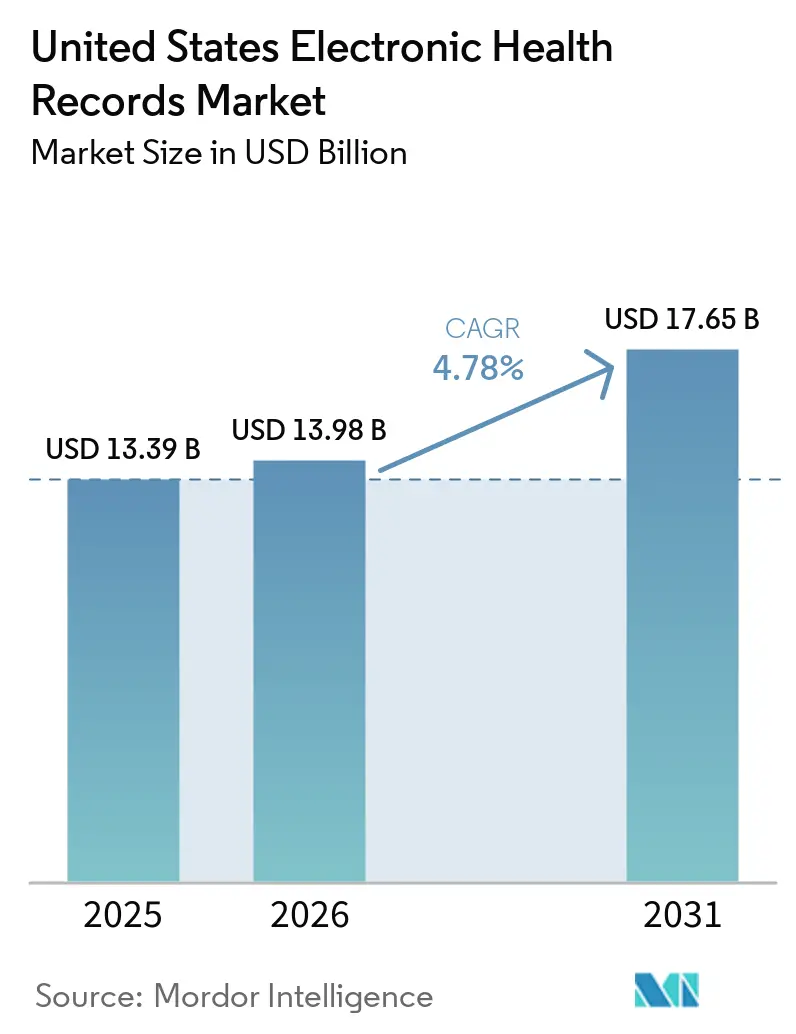

| Base Year Market Size (2025) | USD 13.39 Billion |

| Market Size (2026) | USD 13.98 Billion |

| Market Size (2031) | USD 17.65 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

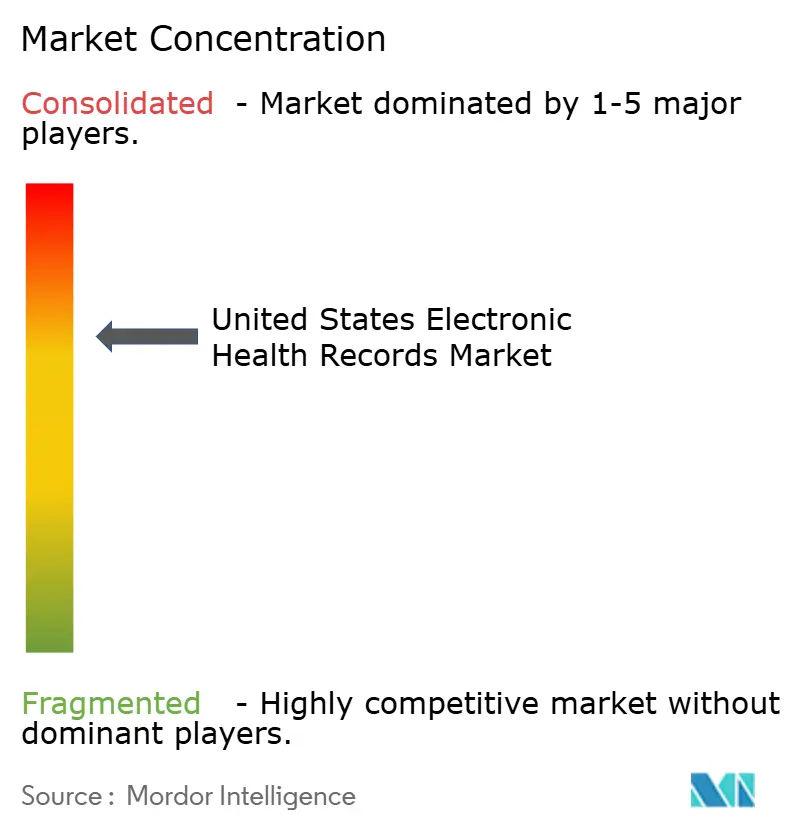

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Electronic Health Records Market Analysis by Mordor Intelligence

The United States Electronic Health Records Market size was valued at USD 13.39 billion in 2025 and is estimated to grow from USD 13.98 billion in 2026 to reach USD 17.65 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031).

The United States electronic health records market is being pushed by federal interoperability deadlines, payer and provider pressure to automate prior authorization, and a wider move toward cloud delivery that supports faster updates and lower infrastructure burden. TEFCA has already moved interoperability into day-to-day operating reality, with health record exchange volumes rising sharply and national connectivity now spanning tens of thousands of participant and subparticipant locations, which makes exchange readiness a practical buying requirement for large provider organizations. The CMS prior authorization rule and the ONC certification roadmap are also compressing vendor timelines, so providers are increasingly favoring platforms that can show active compliance plans rather than promising future upgrades. At the same time, ambient documentation and workflow automation are changing what buyers expect from the United States electronic health records market, since documentation support is now being judged alongside interoperability, uptime, and reimbursement workflow support. This is why vendor gains in the United States electronic health records market are coming less from first-time adoption and more from replacements and upgrades among providers that no longer want to stay on platforms that are behind on certification, cloud readiness, or embedded automation.

Key Report Takeaways

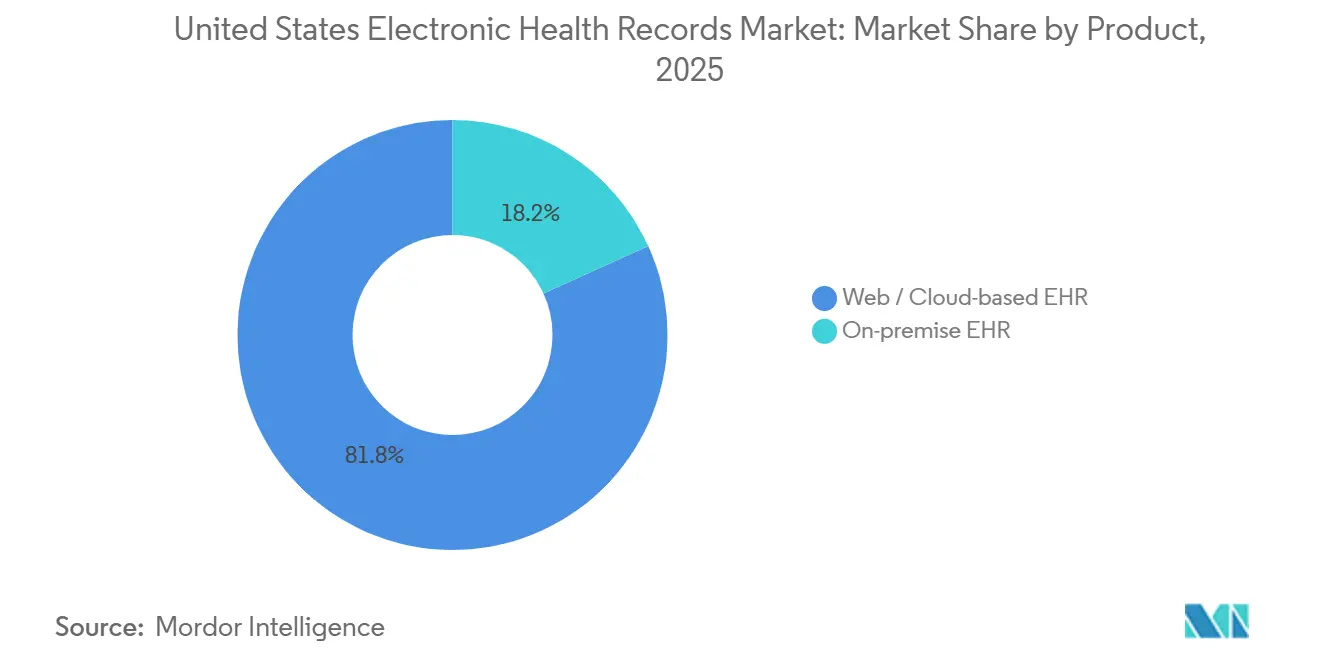

- By product, web/cloud-based EHR held 81.79% share of the United States electronic health records market size in 2025, and the same segment is projected to expand at a 6.3% CAGR through 2031.

- By type, acute EHR held 45.23% of the United States electronic health records market share in 2025, while post-acute EHR is forecast to record the highest CAGR at 6.07% through 2031.

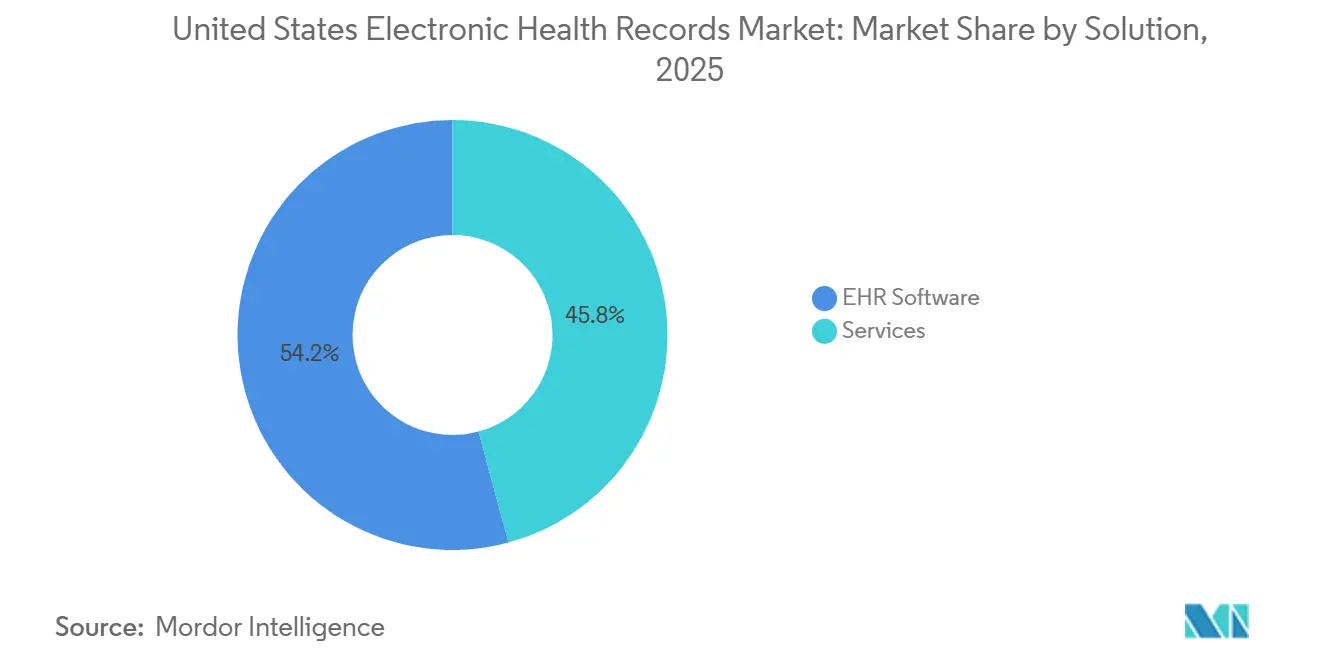

- By solution, EHR software accounted for 54.23% of the United States electronic health records market size in 2025, while services are projected to grow fastest at a 6.78% CAGR through 2031.

- By end use, hospitals held 52.71% of the United States electronic health records market share in 2025, while ambulatory surgical centers are expected to expand at a 7.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Electronic Health Records Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Interoperability And Prior-Authorization Mandates | +1.5% | National, compliance pressure highest in Medicare Advantage and Medicaid managed-care states such as Texas, California, Florida, and New York | Short term (≤ 2 years) |

| Cloud And Web-Based Migration Economics | +1.2% | National, fastest in large integrated delivery networks in the Northeast and West Coast | Medium term (2-4 years) |

| Outpatient Care Expansion And Multisite Coordination Needs | +0.8% | National, most pronounced in Sun Belt states where ASC expansion is fastest | Medium term (2-4 years) |

| AI-Enabled Documentation And Workflow Automation | +0.9% | National, fastest adoption in academic medical centers and large ambulatory groups | Short term (≤ 2 years) to Medium term (2-4 years) |

| TEFCA Network Effects Favor Exchange-Ready Platforms | +0.7% | National, rural and critical access hospitals in the Midwest and Southeast are gaining access parity | Medium term (2-4 years) |

| USCDI And Certification Roadmap-Driven Upgrade Cycles | +0.5% | National, compliance burden highest for small practices and rural hospitals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Federal Interoperability and Prior-Authorization Mandates

The United States electronic health records market is moving through a certification reset as USCDI v1 expired on January 1, 2026, and ONC requirements moved the active baseline to newer data standards. USCDI v3 expanded the required structured data set well beyond the earlier version, adding fields such as social determinants of health and insurance data that force vendors to rework data architecture, testing, and exchange workflows.[1]U.S. Department of Health and Human Services, “HTI-4 Final Rule, Overview Fact Sheet,” HealthIT, healthit.gov ONC then published USCDI v6 in July 2025 and released draft USCDI v7 on January 29, 2026, which keeps the United States electronic health records market on an annual upgrade cycle instead of allowing vendors to treat compliance as a one-time exercise. CMS has added a second deadline through the Interoperability and Prior Authorization Final Rule, with Prior Authorization APIs required to go live on January 1, 2027, which shortens development windows for every certified vendor serving affected workflows. HHS also stated that the HTI-4 Final Rule is expected to generate USD 19.2 billion in administrative savings over 10 years by allowing providers to manage prior authorization more fully inside certified systems, which raises the operating value of compliance-ready platforms. As a result, platform selection in the United States electronic health records market is now closely tied to whether a vendor can show an active certification roadmap, not just a stable installed base.

Cloud And Web-Based Migration Economics

Cloud migration has become a practical operating decision in the United States electronic health records market because providers now have visible examples of cost savings, performance gains, and simpler upgrade paths after moving major EHR workloads off local infrastructure. Microsoft stated in March 2026 that Epic deployments on Azure delivered strong financial returns for migrating organizations, which helped shift cloud discussions from IT modernization into board-level capital planning.[2]Microsoft, “Delivering More Cost-Efficient Healthcare with Epic on Azure,” Microsoft in Business, microsoft.com Microsoft also said Franciscan Health saved USD 45 million over 5 years after its Azure migration, while cutting infrastructure costs by one-third and improving application response time by 50%, which gives providers a concrete case for moving away from older hosting models. That matters because cloud delivery converts large hardware cycles into steadier operating expenses and makes it easier to support analytics, API exposure, and ongoing compliance upgrades from a common environment. It also supports the direction of the United States electronic health records market, where interoperability, certification updates, and AI features all require more frequent product changes than many on-premise footprints were designed to handle. The commercial logic is therefore reinforcing the policy logic, which is why cloud delivery leads on both scale and growth in this market.

Outpatient Care Expansion and Multisite Coordination Needs

The United States electronic health records market is also being shaped by a steady move of care delivery into ambulatory and multisite settings, where disconnected records create scheduling, billing, and care-transition friction that operators increasingly want to remove. The Ambulatory Surgery Center Association reported that EHR adoption in ASCs reached 76% in 2025, up from 55% in 2021, which shows that digital record use has moved well beyond early-stage uptake in this setting. The same association also noted that many of the remaining paper-based centers still plan to delay adoption until regulations force action, which leaves a meaningful pool of delayed demand still in the market. Consolidation is a major trigger because private equity owners and health systems often standardize platforms after acquisitions, and that can override the prior preference to stay on paper or on a narrow local workflow. MEDITECH’s June 2025 deployment across all 132 Willis Knighton clinics showed how large organizations are replacing multiple systems with a single record environment to improve coordination across ambulatory and acute care. Vendors that offer perioperative, anesthesia, scheduling, and billing workflows inside broader ambulatory platforms are therefore gaining momentum in the United States electronic health records market, because buyers want fewer interfaces and less local customization.

AI-Enabled Documentation and Workflow Automation

AI-enabled documentation is becoming a real buying issue in the United States electronic health records market because providers now expect the EHR to reduce documentation time rather than simply store the finished note. Oracle said in March 2026 that its Clinical AI Agent had already saved more than 200,000 physician hours and had expanded from ambulatory settings into inpatient and emergency department workflows across the United States.[3]Oracle Corporation, “Oracle Health Clinical AI Agent Helps Emergency and Inpatient Doctors Spend More Time on Patient Care,” Oracle, oracle.com athenahealth then moved in a different but equally important direction by launching athenaAmbient at no extra charge to more than 170,000 clinicians, which signaled that ambient documentation is starting to shift from paid add-on toward bundled platform capability. Mayo Clinic and Abridge expanded that logic further in May 2026 by announcing an ambient documentation program for nursing workflows, which widened AI automation beyond physician charting into one of the largest documentation burdens in the care setting. These moves matter because embedded AI becomes more valuable when it connects directly to billing, charge capture, and authorization workflows that already sit inside the platform. That raises switching friction in the United States electronic health records market, since providers may prefer a single vendor that can combine documentation support, compliance updates, and financial workflow tools in one product stack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity, Ransomware, And Privacy Exposure | -0.6% | National, with disproportionate impact on smaller health systems and rural hospitals with limited IT security capacity | Short term (≤ 2 years) to Medium term (2-4 years) |

| High Switching Costs And Implementation Disruption | -0.5% | National, most acute in Epic-dominated markets in the Northeast and West | Long term (≥ 4 years) |

| Uneven API And FHIR Readiness Across Smaller Providers | -0.4% | Rural and underserved areas in the Midwest, Appalachia, and the Mountain West | Medium term (2-4 years) |

| Vendor Lock-In From Concentrated Platform Ecosystems | -0.3% | National, most acute in large health system markets with enterprise-wide Epic deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity, Ransomware, and Privacy Exposure

Cybersecurity remains the clearest downside risk in the United States electronic health records market because the financial and operational impact of an incident can move quickly from IT recovery into care delivery and executive oversight. IBM reported average healthcare breach recovery costs of USD 7.42 million per incident in 2025, which kept healthcare at the highest cost level among critical infrastructure sectors. The American Hospital Association also reported in its 2025 year-in-review that more than 90% of breached health records were taken from systems outside the core EHR, including clearinghouses, revenue cycle systems, and third-party connectors, which means risk now sits across the broader application network rather than inside the record alone. That raises the difficulty of vendor selection because health systems must assess the security posture of API partners and adjacent workflow tools, not only the main EHR application. It also explains why HIPAA compliance and SOC 2 Type II controls are now basic contract expectations rather than points of product differentiation. For the United States electronic health records market, that security burden can slow purchase decisions, extend implementation review cycles, and raise the cost of platform expansion into more connected workflows.

High Switching Costs and Implementation Disruption

High switching costs remain a structural drag on the United States electronic health records market because providers often stay with a weak-fit platform rather than absorb the disruption of a large migration. This is especially true for hospital systems where the EHR is tied into revenue cycle tools, analytics, staffing, prior authorization, and now documentation support, which makes replacement a full operating model change instead of a software swap. Direct migration budgets can run into the multi-million-dollar range for large organizations, and the larger burden often comes from training, workflow redesign, data conversion, and temporary productivity loss during and after go-live. That burden has reduced the number of organizations willing to make replacement decisions quickly, even when policy deadlines are increasing the pressure to modernize. In practice, this means the United States electronic health records market still rewards incumbents that can keep clients current on compliance without forcing a disruptive rip-and-replace event. It also means challengers need a sharper value case than they did in earlier adoption cycles, since they are now asking providers to trade known pain for a costly transition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cloud Consolidation Reshapes the Deployment Baseline

Web/cloud-based EHR held 81.79% of the United States electronic health records market size in 2025 and is also forecast to post the fastest CAGR at 6.30% through 2031. That combination shows that the United States electronic health records market is not splitting between equal deployment models, but is moving more firmly toward cloud as the default operating base. The shift is reinforced by federal interoperability and certification demands, since frequent standards updates and API requirements are easier to manage in environments built for continuous releases. It is also reinforced by provider economics, because cloud-hosted records can reduce local infrastructure burden and simplify performance upgrades across large clinical networks.

On-premise EHR accounted for the remaining 18.21% in 2025, which shows that a smaller but durable installed base still remains in the United States electronic health records market. That base is concentrated in organizations with tighter control requirements, older infrastructure decisions, or slower capital planning cycles, including some rural and public-sector settings. Even so, the product roadmap balance has shifted toward web and cloud delivery because TEFCA participation, API exposure, and embedded automation all favor platforms that can be updated more quickly across distributed users. This leaves on-premise vendors under pressure to defend existing contracts while cloud-first vendors capture a larger share of upgrade and replacement activity in the United States electronic health records industry.

By Type: Post-Acute Growth Exposes Care Coordination Gaps

Acute EHR led the type mix with 45.23% in 2025, while post-acute EHR is expected to record the fastest CAGR at 6.07% through 2031. Acute care still anchors the United States electronic health records market because hospitals remain the center of large enterprise contracts, major integration budgets, and the strictest interoperability demands. Post-acute growth is rising because patient acuity in skilled nursing and home health settings is increasing, and providers in those settings need better continuity of records as transitions from hospital care become more clinically complex. The result is a broader push for the United States electronic health records market to support the full care path rather than only the hospital stay.

Ambulatory EHR remains a large middle layer in this structure because care volume continues to move out of inpatient settings and into physician offices, specialty clinics, and multisite organizations. eClinicalWorks’ March 2025 integration with the PointClickCare marketplace showed how ambulatory vendors are trying to close the long-standing record gap between physician workflows and long-term or post-acute settings. That kind of connection matters because weak handoffs across care settings can hurt documentation quality, follow-up planning, and reimbursement continuity. Vendors with stronger post-acute and ambulatory bridge tools are therefore better positioned in the United States electronic health records industry than vendors that still treat those settings as side markets.

By Solution: Services Growth Signals a Market Maturity Transition

EHR software held 54.23% of the United States electronic health records market size in 2025, while services are forecast to grow fastest at a 6.78% CAGR through 2031. That pattern suggests the United States electronic health records market has moved deeper into an implementation and optimization phase, where providers are spending not only on software licenses but also on migration, integration, training, and compliance support. The current rule set helps explain this shift because USCDI upgrades, TEFCA connectivity, prior authorization APIs, and AI workflow deployment all require skills that many provider organizations do not keep in-house. In other words, software remains the core spend line, but services are rising faster because the operating environment around the software has become more demanding.

Cloud-based software remains the strongest part of the solution mix because the main vendors are aligning product development, data exchange, and AI tools around cloud infrastructure rather than around legacy local deployments. Epic’s Azure path and Oracle Health’s OCI strategy both reflect that direction, even though they come from different competitive positions inside the market. On-premise software continues to generate maintenance and support revenue, but the center of product investment is moving elsewhere. That leaves services as the connecting layer that helps providers modernize without breaking clinical and financial workflows across the United States electronic health records market.

By End Use: Ambulatory Surgical Centers Are the Fastest-Growing Demand Cohort

Hospitals accounted for 52.71% of the United States electronic health records market size in 2025, while ambulatory surgical centers are forecast to expand at the fastest CAGR of 7.67% through 2031. Hospitals remain the largest end-user group because they anchor enterprise-scale deployments, complex interoperability needs, and the highest degree of platform integration across clinical and financial operations. Even so, the fastest incremental demand in the United States electronic health records market is shifting toward ASCs as procedure volumes continue to move away from hospital outpatient departments. The cost and compliance balance in these facilities is changing, which is making digital records harder to postpone.

ASCA reported that 76% of ASCs were already using an EHR in 2025, but many of the remaining paper-based centers still cited cost as the main barrier, which leaves a delayed adoption pool that can be activated by ownership changes or tighter regulation. Physician offices and specialty clinics remain highly contested because they represent large contract opportunities for ambulatory vendors and care-delivery organizations that operate across multiple states. athenahealth’s January 2026 deployment across all 350 CenterWell Senior Primary Care and Conviva Care Center locations in 15 states showed how a single ambulatory contract can shape regional positioning for a vendor. Diagnostic centers are still the smallest end-user segment, but they are becoming more important as integrated records are increasingly expected across referral, imaging, and value-based care workflows. This keeps end-user demand broad in the United States electronic health records market, even while hospitals continue to dominate revenue.

Geography Analysis

The United States electronic health records market sits inside one national regulatory framework, but adoption intensity and vendor concentration still vary by region. The Northeast has the densest concentration of large academic health systems and remains one of the strongest enterprise acute care zones for interoperability-driven purchasing. Health information exchange capacity was already mature in several states before TEFCA, which means the region entered the national framework with a stronger foundation for broad exchange participation. ONC reported in 2025 that 5 out of 10 hospitals already involved in national networks were participating in TEFCA, compared with 1 in 10 among hospitals that had not previously joined those networks, which shows how earlier exchange maturity is shaping current regional readiness.

The South and the Sun Belt are the fastest-moving areas for new-site ambulatory and ASC activity in the United States electronic health records market. Population growth, ongoing outpatient expansion, and multisite provider strategies are giving these states a higher pace of practical deployment decisions than many slower-growth regions. That is why vendors with ASC-specific workflows, lower-complexity implementations, and strong ambulatory sales teams are directing added effort toward Texas, Florida, Arizona, and Georgia. These areas are less defined by a single dominant enterprise replacement cycle and more by continuous site additions, network affiliations, and portfolio standardization. The Midwest shows a split pattern, with large integrated systems operating mature exchange and EHR environments, while many smaller community hospitals still face slower modernization paths.

Rural hospitals and critical access hospitals, especially in the Midwest, Appalachia, and the Mountain West, face the most persistent barriers in the United States electronic health records market. Budget limits, smaller IT teams, and weaker API readiness make certification and interoperability upgrades harder to manage in these geographies. TEFCA’s spread to more than 83,000 participant and subparticipant locations has improved the baseline opportunity for exchange, but local execution still depends on funding, vendor support, and technical capacity. This is why rural-focused acquisitions and support models are gaining strategic value, since the next phase of growth will depend partly on bringing smaller providers into more modern and secure record environments.

Competitive Landscape

The United States electronic health records market is highly concentrated in acute care and more open in ambulatory and post-acute settings. Epic Systems, Oracle Health, and MEDITECH together account for 90% of acute care deployments, which keeps the top end of the market tightly controlled even though competition remains active below that level. In practice, that means the acute segment rewards scale, implementation depth, and long-term interoperability execution more than aggressive price competition. It also means winning or losing a few large health system accounts can quickly change the tone of competition across the United States electronic health records market.

Oracle Health is trying to reset its position through product and infrastructure moves rather than through incremental sales tactics. Oracle expanded Clinical AI Agent into inpatient and emergency workflows in March 2026 and continued to tie that strategy to Oracle Cloud Infrastructure, which gives it a combined pitch around automation and hosting. Oracle also secured a major CMS cloud contract in February 2026, which strengthened its public-sector reference base ahead of its planned AI-native acute care launch. Epic has benefited from the same broad market conditions from the other side, since the current cycle favors vendors that can pair cloud hosting, certification continuity, and exchange readiness in a familiar enterprise model. MEDITECH remains relevant by extending Expanse across broad ambulatory footprints, which helps defend its position among systems looking for a unified record across care settings.

Competition becomes more fluid once the market moves beyond the largest acute care organizations. athenahealth has leaned on AI partnerships and large ambulatory deployments, including its Dragon Copilot integration and its CenterWell rollout, to strengthen its value proposition around clinician workflow and multisite physician operations. ModMed’s April 2026 acquisition of Bonsai Health shows how specialty vendors are pushing beyond documentation and into patient engagement and front-office automation. PointClickCare is doing something similar in post-acute care through Discharge Intel, its next-generation EHR for practice groups, and the expansion of Chart Advisor, which deepens its role in acute-to-post-acute transitions. This leaves the United States electronic health records market with a concentrated acute core and a more varied outer layer where workflow fit, AI packaging, and lower-friction implementation can still move share.

United States Electronic Health Records Industry Leaders

athenahealth

eClinicalWorks

Epic Systems Corporation

Oracle Health

PointClickCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: PointClickCare expands Chart Advisor to Senior Living. PointClickCare announced the upcoming availability of Chart Advisor to Senior Living communities, extending its AI-powered risk identification and documentation quality tool from skilled nursing into assisted living. The expansion broadens PointClickCare's addressable market within post-acute EHR and deepens its position ahead of competing LTPAC platforms.

- April 2026: IKS Health agrees to acquire TruBridge. Inventurus Knowledge Solutions (IKS Health) announced a definitive agreement to acquire TruBridge (NASDAQ: TBRG), a healthcare technology provider focused on rural and community hospitals. The combined entity will serve more than 2,000 healthcare organizations and 150,000+ clinicians with AI-driven EHR and revenue cycle management capabilities, representing a significant consolidation in the rural hospital EHR segment.

- April 2026: ModMed acquires Bonsai Health. Specialty EHR vendor ModMed, backed by Clearlake Capital, acquired Bonsai Health, an agentic AI patient engagement platform with capabilities including automated patient reactivation and AI-driven self-scheduling. The acquisition integrates front-office automation across ModMed's approximately 50,000-provider specialty network.

- April 2026: PointClickCare and AIDA Healthcare partner on care transitions. PointClickCare and AIDA Healthcare announced a strategic partnership to optimize referral management and care transitions between acute and post-acute settings, directly targeting one of the highest-friction data handoff points in the U.S. care continuum.

United States Electronic Health Records Market Report Scope

The United States Electronic Health Records (EHR) market is defined as the industry encompassing digital systems that securely document, store, share, and analyze patient health information across healthcare providers. It includes software platforms and services that enable interoperability, clinical decision support, patient engagement, and compliance with U.S. regulations such as HIPAA and the HITECH Act.

The United States Electronic Health Records (EHR) Market Report defines the market as segmented across several dimensions. By product, it includes both web/cloud-based EHR systems and on-premise EHR solutions. By type, the market is categorized into acute EHR, ambulatory EHR, and post-acute EHR. In terms of solution, it covers EHR software as well as services that support implementation, maintenance, and optimization. Finally, by end use, the market encompasses hospitals, physician offices and specialty clinics, ambulatory surgical centers, and diagnostic centers. Market forecasts are provided in terms of value (USD), reflecting the financial scope and growth potential of these segments.

| Web / Cloud-based EHR |

| On-premise EHR |

| Acute EHR |

| Ambulatory EHR |

| Post-acute EHR |

| EHR Software | Cloud-based |

| On-premise | |

| Services | Consulting |

| Implementation & Integration | |

| Support & Maintenance |

| Hospitals |

| Physician Offices and Specialty Clinics |

| Ambulatory Surgical Centers |

| Diagnostic Centers |

| By Product | Web / Cloud-based EHR | |

| On-premise EHR | ||

| By Type | Acute EHR | |

| Ambulatory EHR | ||

| Post-acute EHR | ||

| By Solution | EHR Software | Cloud-based |

| On-premise | ||

| Services | Consulting | |

| Implementation & Integration | ||

| Support & Maintenance | ||

| By End Use | Hospitals | |

| Physician Offices and Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Diagnostic Centers | ||

Key Questions Answered in the Report

What is the current size of the United States electronic health records space?

It stands at USD 13.98 billion in 2026 and is forecast to reach USD 17.65 billion by 2031, growing at a 4.78% CAGR over 2026-2031.

Which product category leads deployment today?

Web and cloud-based EHR leads with 81.79% share in 2025 and also posts the fastest projected growth at 6.30% through 2031.

Why are interoperability rules affecting vendor competition so strongly?

ONC certification updates, TEFCA connectivity, and the CMS prior authorization rule have made compliance readiness a direct buying criterion for providers.

Which end-user group is expanding fastest?

Ambulatory surgical centers are the fastest-growing end-user group, with a projected 7.67% CAGR through 2031, even though hospitals remain the largest revenue base.

Why are services growing faster than software?

Providers need more help with cloud migration, certification changes, API work, AI deployment, and workflow redesign, so services are projected to grow at 6.78% through 2031.

Page last updated on: