United States Healthcare Payer Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

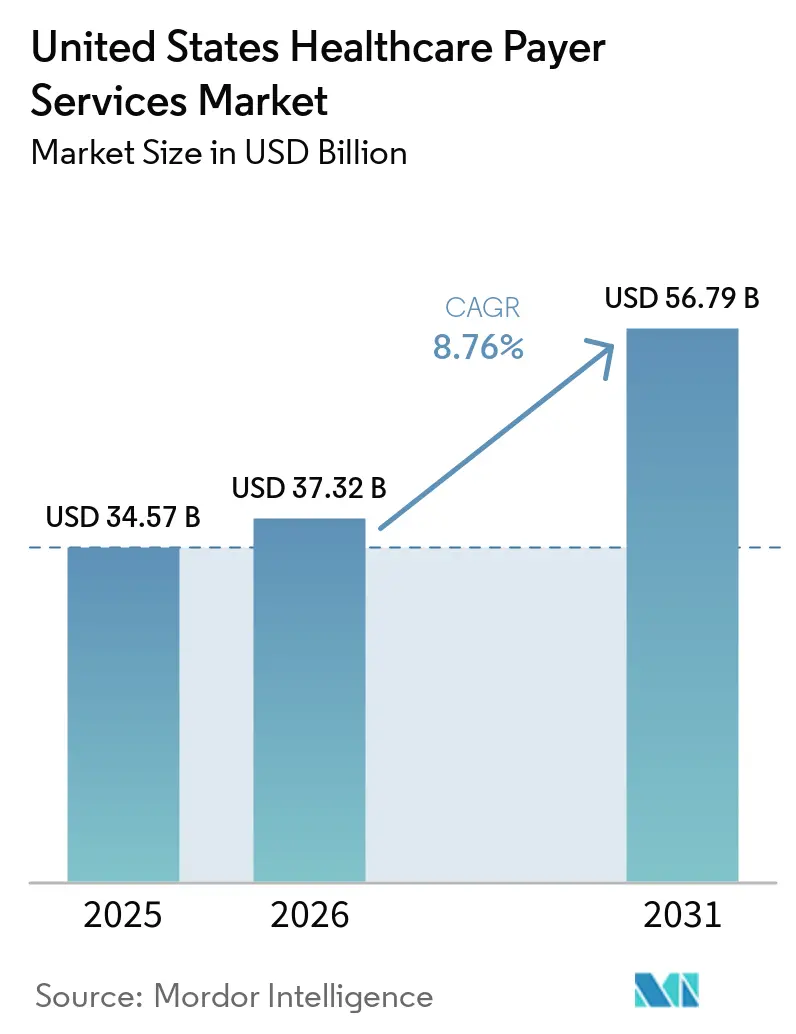

| Base Year Market Size (2025) | USD 34.57 Billion |

| Market Size (2026) | USD 37.32 Billion |

| Market Size (2031) | USD 56.79 Billion |

| Growth Rate (2026 - 2031) | 8.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Healthcare Payer Services Market Analysis by Mordor Intelligence

The United States Healthcare Payer Services Market size is projected to expand from USD 34.57 billion in 2025 and USD 37.32 billion in 2026 to USD 56.79 billion by 2031, registering a CAGR of 8.76% between 2026 to 2031.

The United States healthcare payer services market is expanding because payers are outsourcing more claims, IT, analytics, and administrative work as manual operations become harder to sustain under tighter margins and rising compliance demands. Administrative automation still has a large untapped savings pool, which keeps outsourcing relevant for both routine and exception-heavy workflows across the payer operating model. The compliance calendar is also turning technology modernization into a near-term revenue stream for service vendors, especially around interoperability, prior authorization, and clinical documentation exchange requirements. The market is also moving into a more outcome-based phase because payers now expect vendors to show faster claims handling, cleaner workflows, and better control of administrative leakage, rather than just offering labor at scale. As production AI moves into live claims environments, the United States healthcare payer services market is shifting from pilot-led experimentation toward contracts tied more closely to measurable operating performance.

Key Report Takeaways

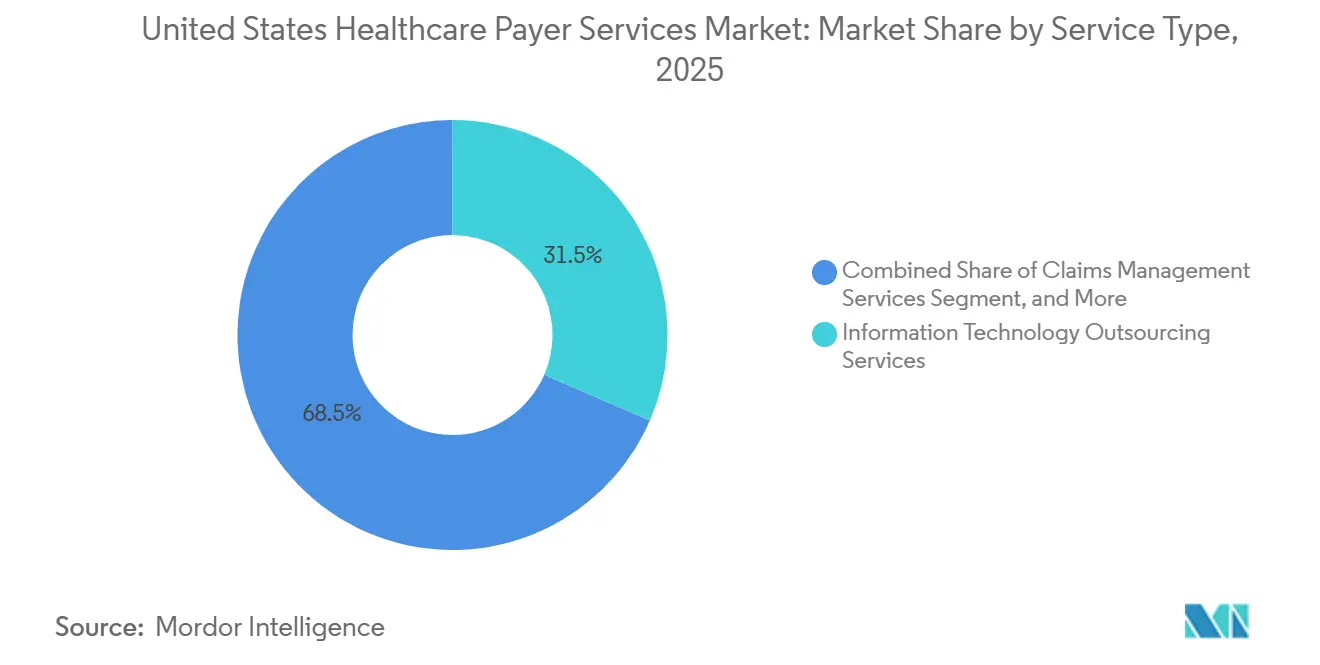

- By service type, information technology outsourcing services led with 31.48% revenue share in 2025, while knowledge process outsourcing services are forecast to expand at a 9.36% CAGR through 2031.

- By application, health insurance held 51.17% of the United States healthcare payer services market share in 2025, while managed care recorded the highest projected CAGR at 10.29% through 2031.

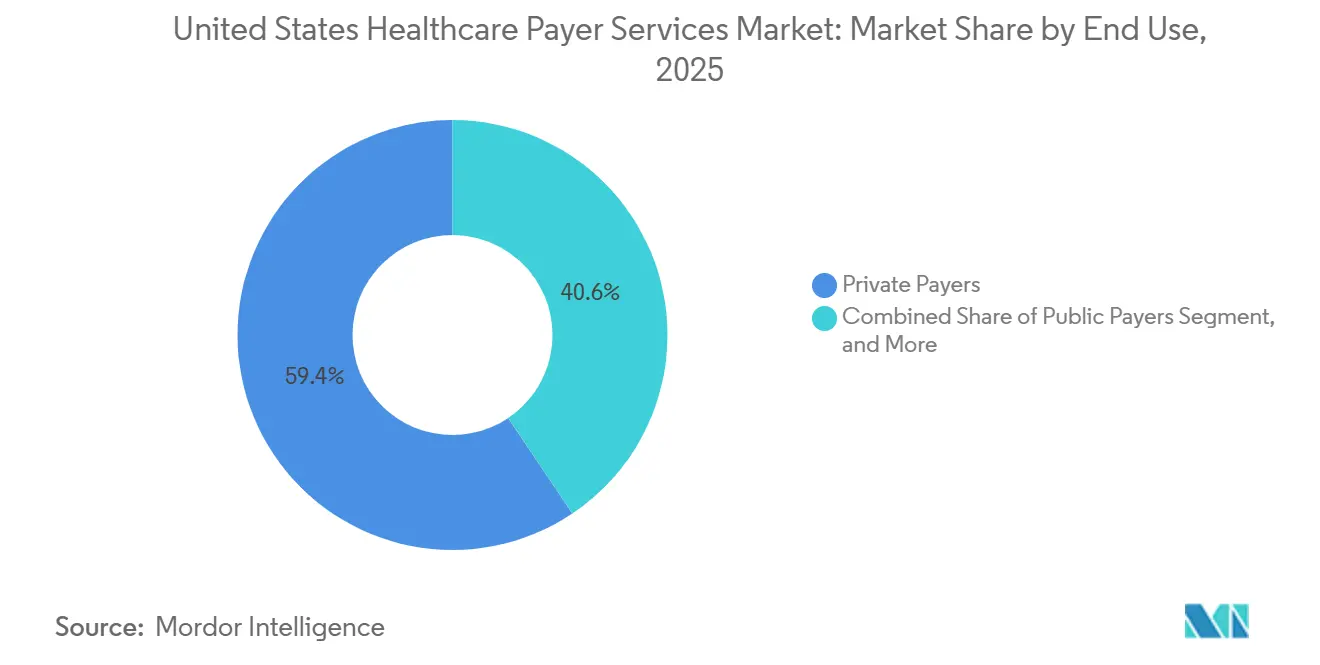

- By end use, private payers accounted for 59.42% share of the United States healthcare payer services market size in 2025, while public payers are advancing at a 9.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Healthcare Payer Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Claims Automation Demand | +2.8% | National, with concentrated impact in high-volume MA markets, Florida, Texas, Ohio | Short term (≤ 2 years) |

| Value-Based Care Contracting Complexity | +2.1% | National, early gains in Massachusetts, Minnesota, Oregon, California | Medium term (2-4 years) |

| Interoperability-Driven Administrative Workload | +1.5% | National, compliance front-loaded in CMS-regulated plan states | Short term (≤ 2 years) |

| AI-Based Payment Integrity Expansion | +1.6% | National, with spill-over to self-insured employer markets in Midwest and Northeast | Medium term (2-4 years) |

| Payer Margin Compression From Low-Mix Administrative Leakage | +1.2% | National, most acute in MA-heavy southeastern and south-central markets | Short term (≤ 2 years) |

| Rapid Rise In Prior Authorization Exception Volumes | +1.0% | National, particularly Medicare Advantage and Medicaid managed care segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Claims Automation Demand: Manual Adjudication Costs Reach Systemic Levels

The United States healthcare payer services market is benefiting from the fact that administrative work is still too expensive to leave inside fragmented and partly manual payer systems. CAQH reported that electronic transaction processing helped the U.S. healthcare system avoid USD 258 billion in administrative costs in 2024, while another USD 21 billion in annual savings remains available through deeper automation of manual and partially manual workflows. That gap matters because denied, pended, and exception-heavy claims still create repeat touches, longer cycle times, and avoidable labor costs that payers increasingly prefer to shift to specialist operating partners. Once those rework loops are moved outside the health plan, vendors can spread workflow investments across many clients, which makes automation economics easier to justify than they are inside a single payer. Aetna stated in May 2026 that its Claims Automation Model reduced processing time for complex claims by more than 20%, which gives the market a visible example of how production AI can lower turnaround time in a live payer setting. As more plans look for the same result, the United States healthcare payer services market is seeing stronger demand for vendors that can combine claims operations, workflow rules, exception handling, and AI-based resolution inside one delivery model.

Value-Based Care Contracting Complexity: Outsourced Analytics Becoming Non-Negotiable

The United States healthcare payer services market is also being pulled forward by value-based care because those contracts are much harder to reconcile than fee-for-service arrangements. AJMC noted that traditional payment infrastructure, including claims adjudication and billing systems, remains structurally misaligned with value-based reimbursement mechanics for self-insured employers and related arrangements.[1]American Journal of Managed Care, “Legal Issues in Value-Based Care Contracts for Self-Insured Employers,” AJMC, ajmc.com NASCO also pointed to fragmented payer environments where attribution, engagement, claims, and reporting data sit across multiple systems without a single source of truth, which raises the administrative burden around contract measurement and settlement. In that setting, external analytics and KPO partners become less of an optional add-on and more of an operating necessity because they can centralize performance measurement, actuarial work, and contract-level reporting that internal teams struggle to coordinate. This is one reason the United States healthcare payer services market is shifting toward longer and deeper vendor relationships, since payers increasingly need outside partners that stay embedded across recurring reporting cycles and not just isolated project windows. The same dynamic also supports higher-value outsourcing because plans are buying analytical judgment, reporting continuity, and data handling discipline, not just low-cost processing capacity.

Interoperability-Driven Administrative Workload: Compliance Spending Converted to Services Revenue

The United States healthcare payer services market is receiving a strong near-term push from the regulatory timetable tied to interoperability and prior authorization modernization. The CMS-0057-F rule moved payer compliance work into a fixed execution window with initial milestones beginning in January 2026 and full API requirements due in January 2027, which makes internal delays harder to absorb than they were under earlier mandates. That timetable is layered on top of the CMS claims attachments final rule, which became effective in May 2026, sets a 2028 compliance deadline, and is expected to generate USD 781 million in annual savings from moving clinical documentation exchange away from fax-based processes.[2]CMS, “CMS Claims Attachments Rule Sets 2028 Deadline,” HFMA, hfma.org When these requirements land together, technology spending stops being a discretionary upgrade and becomes operational compliance spending, which directly supports IT outsourcing, implementation services, workflow redesign, and ongoing managed support. It also changes vendor selection because payers now need production-ready environments that can handle FHIR-based exchange, documentation standards, and reporting demands under live deadlines, rather than consultants that only advise on program design. That is why the United States healthcare payer services market is seeing compliance-led demand translate quickly into service revenue, especially for firms already positioned around payer IT modernization.

AI-Based Payment Integrity Expansion: Shift From Recovery to Prevention Reorders the Market

The United States healthcare payer services market is also being reshaped by a broader move to place AI earlier in the claim and payment workflow. Once claims automation tools begin working in production, the same logic extends into coding review, payment accuracy checks, and exception routing because payers want errors identified before they become expensive downstream rework. Aetna’s May 2026 update showed that AI can already deliver measurable throughput gains in complex claims environments, which strengthens the case for wider deployment across adjacent payment integrity tasks. Vendors that can connect adjudication, review rules, documentation checks, and case escalation in one operating framework are gaining an advantage because payers increasingly want fewer handoffs across separate providers. This shifts contract value toward vendors with integrated workflow design, data handling, and model governance rather than vendors that only offer stand-alone recovery services. Over time, that should keep the United States healthcare payer services market tilted toward platform-based delivery where the commercial value comes from preventing avoidable leakage early and documenting that improvement clearly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HIPAA And CMS Compliance Burden | -0.9% | National, with concentration in federally regulated plan types, Medicare, Medicaid, ACA marketplace | Short term (≤ 2 years) |

| Cybersecurity And Breach Exposure | -0.8% | National, vendor-concentration risk highest in Southeast and Mid-Atlantic outsourcing hubs | Medium term (2-4 years) |

| Legacy Core System Integration Friction | -0.7% | National, most acute in regional Blues plans and Medicaid-heavy states with aging infrastructure | Long term (≥ 4 years) |

| Contract Governance And Transition Leakage In Outsourced Operations | -0.5% | National, with above-average exposure in large multi-vendor commercial payer engagements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Breach Exposure: Third-Party Vendor Concentration Creates Systemic Risk

Cybersecurity is a real brake on the United States healthcare payer services market because the scale of outsourcing can also concentrate operational exposure within a smaller number of critical vendors. When one service provider sits across claims, member data, or administrative interfaces for many payer clients, a single failure can affect multiple contracts at the same time and force payers to reassess vendor concentration risk. That risk is now influencing procurement design, since plans want stronger audit rights, clearer accountability language, and better evidence that outside partners can protect PHI in complex production settings. Security spending therefore rises for both buyers and vendors, which can slow contract decisions even while it raises demand for providers with mature control environments. The result is a narrower effective vendor pool, because not every outsourcing provider can absorb the cost of security architecture, monitoring, testing, and governance required for payer-grade operations. This keeps the United States healthcare payer services market growing, but it also makes vendor qualification slower and more demanding than a standard cost-led outsourcing cycle.

Legacy Core System Integration Friction: A Drag Measured in Decades, Not Quarters

Legacy platform complexity remains another restraint because many payers still depend on core systems built for older adjudication models and not for modern interoperability, analytics, or cloud-native workflows. Those environments often require long modernization programs before new outsourced services can produce clean and repeatable returns, which stretches timelines and complicates budget approvals. The issue is not simply technical age, because old claims, eligibility, and reporting systems are deeply tied to plan-specific processes, historical data structures, and regulatory controls that cannot be replaced quickly. Even when vendors provide translation layers, connectors, and migration support, the surrounding operating model still has to be redesigned over several years, which slows the pace at which payers can fully externalize complex work. This creates a mixed effect for the United States healthcare payer services market, since legacy friction generates steady demand for IT partners while delaying the speed at which payers capture the full economic benefit of those engagements. It also helps explain why large transformation contracts increasingly include phased milestones, hybrid operations, and longer transition periods before the highest-value work is moved outside the plan.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: IT Outsourcing Anchors Revenue as KPO Accelerates

Information Technology Outsourcing Services held 31.48% of the United States healthcare payer services market share in 2025, which kept it as the largest service category by a clear margin. That lead reflects how much payer operating stability now depends on outside support for cloud migration, platform modernization, cybersecurity controls, API enablement, and integration work that internal teams often cannot complete at the required pace. In the United States healthcare payer services industry, ITO also carries a strategic role because it sits underneath many other outsourced functions, including claims workflow redesign, member servicing tools, reporting architecture, and prior authorization systems. The service line remains closely tied to regulatory execution, since payers need technical delivery partners that can move compliance programs from policy interpretation into operational systems. Even if adjacent categories grow faster over the next few years, ITO should continue to anchor revenue because most payer transformation programs still begin with systems, interfaces, security, and workflow infrastructure rather than with stand-alone labor contracts.

Knowledge Process Outsourcing Services is projected to expand at a 9.36% CAGR from 2026 to 2031, making it the fastest-growing service type in the United States healthcare payer services market. Its growth is linked to payer demand for actuarial support, risk adjustment work, forecasting, contract measurement, and value-based care reporting that require specialized analytical skills and stronger data handling than general BPO models usually provide. NASCO’s observation that health plans still operate across fragmented data environments helps explain why KPO vendors are moving closer to payer decision cycles and not just supporting back-office analysis. Claims Management Services remains central because it supports high-volume workflow transfer, while payment integrity and fraud-related work are gaining more attention as payers look for earlier intervention inside the claims life cycle. Business Process Outsourcing Services and Analytics Services are also benefiting from contracts that now include measurable expectations around turnaround time, rework reduction, and administrative accuracy. That means the United States healthcare payer services market is gradually rewarding providers that can connect operational delivery with analytical depth, rather than keeping those functions in separate vendor silos.

By Application: Health Insurance Dominates but Managed Care Disrupts the Equilibrium

Health Insurance accounted for 51.17% of the United States healthcare payer services market size in 2025, which reflects the breadth of administrative work attached to commercial, individual, and ACA marketplace lines. This part of the market carries heavy and recurring demand for enrollment, provider data, credentialing, utilization management, billing support, and multi-state compliance tasks that are well suited to external operating partners. The scale of those workflows keeps outsourcing penetration high because large national carriers and regional plans both need flexible capacity without carrying all delivery costs internally. The segment also benefits from continuous pressure to simplify member experience while keeping administrative expense under control, which pushes plans toward shared-service models and more automated vendor-led workflows. For that reason, Health Insurance remains the largest application base in the United States healthcare payer services market, even as newer growth pools emerge elsewhere.

Managed Care is forecast to grow at a 10.29% CAGR through 2031, making it the fastest-growing application segment. That acceleration comes from the administrative intensity of risk-bearing arrangements, where prior authorization, utilization review, provider coordination, and performance reporting create heavier service needs than many traditional fee-for-service settings. KFF reported that Medicare Advantage insurers made nearly 53 million prior authorization determinations in 2024, up from 49.8 million in 2023, which illustrates the rising workload flowing into managed care administration. As that volume rises, plans need outside support not only for transaction handling but also for audit trails, appeals support, provider communication, and workflow design that can keep pace with tighter reporting expectations. Public Programs and Life Insurance still contribute smaller revenue pools, but they offer stable demand where service vendors can build long-duration operating roles around specialized compliance requirements. This is why the United States healthcare payer services market is seeing managed care act as the main growth disruptor inside the application mix, even while Health Insurance remains the revenue core.

By End Use: Private Payers Anchor the Market as Public Payer Growth Accelerates

Private Payers represented 59.42% of the market in 2025, which made them the largest end-use group across the United States healthcare payer services market. Commercial insurers, Blues plans, and employer-related administrators continue to absorb the largest share of outsourced claims, IT, analytics, and member-facing service work because they operate across multiple lines with large and recurring administrative volumes. In the US healthcare payer services industry, this group also tends to move earlier on automation because member retention, service quality, and administrative efficiency all affect competitive positioning more directly. The next stage of outsourcing in this segment is likely to be more platform-embedded than labor-led, as claims routing, call center support, and exception handling become increasingly tied to AI-enabled workflow tools. Aetna’s deployment of CAM is one example of how private payer operations are moving toward production AI within live claims environments. That combination of scale, competition, and technology investment should keep private payers as the main spending base for the United States healthcare payer services market over the medium term.

Public Payers are projected to grow at a 9.07% CAGR from 2026 to 2031, which makes them the fastest-growing end-use segment. Their growth is tied to Medicaid eligibility processing needs, changing CMS requirements, and the broader push to modernize public program administration under tighter visibility and compliance expectations. KFF Health News reported that states are paying firms such as Deloitte, Accenture, and Optum to support eligibility systems as they respond to federal policy changes, which shows how outsourcing demand is extending into state-administered public workflows. This part of the market is more concentrated around large contractors because public payers often require scale, contract history, security credentials, and complex delivery capabilities that smaller vendors cannot easily provide. Employer-Sponsored Plans remain meaningful but slower growing, since self-insured employers continue to examine value-based structures while still relying on older fee-for-service claims infrastructure in many arrangements. The result is that the United States healthcare payer services market is anchored by private payer spending today, while public payer demand is becoming a larger growth engine as government program administration becomes more digital and more outsourced.

Geography Analysis

Regional demand within the United States healthcare payer services market is strongest in the Southeast, where large Medicare Advantage and Medicaid managed care populations create sustained need for outsourced claims, enrollment, prior authorization, and member administration services. Florida and Texas stand out because both states combine large insured populations with heavy managed care activity, which raises transaction density and makes scalable operating partners more attractive to payers. These markets also support larger delivery ecosystems, including payer operations teams, IT modernization programs, and hybrid labor models linked to nearshore support structures. As a result, the United States healthcare payer services market tends to see some of its most immediate operational demand in southeastern and south-central states, where payers cannot easily absorb rising volumes with internal teams alone. This regional concentration is especially visible when compliance work and claims processing growth happen at the same time.

The Northeast serves a different role because it functions as the commercial insurance administration hub for the country, with a high concentration of employer-sponsored plan activity, specialty insurance operations, and multi-state compliance needs. Massachusetts remains important because value-based care infrastructure is more mature there than in many other states, which supports stronger demand for KPO, analytics, and contract measurement support. AJMC’s discussion of the legal and operational complexity around value-based contracts for self-insured employers aligns with why northeastern payers often need more specialized analytical and reporting support. The Midwest, including Ohio, Illinois, Indiana, and Michigan, remains tied closely to large employer-sponsored exposures and to Blues plan modernization programs that are still working through core platform upgrades and interoperability preparation. This gives the region a medium-term demand profile, where current spending is often focused first on system modernization and workflow readiness before the highest-value external services are expanded more broadly.

The Western U.S. has a more digital-first payer profile, especially in California and Washington, where integrated models, technology-oriented operating cultures, and earlier movement on data exchange create a different outsourcing mix. In these states, demand is often centered on IT integration, data governance, member-facing digital workflows, and faster support for changing prior authorization and transparency expectations. California is especially relevant because state-level requirements often move quickly and can act as an early signal for broader operating changes that later spread through the national payer environment. Mountain and Plains states carry lower absolute volume, but they are still important to the United States healthcare payer services market because smaller regional payers in these areas are more likely to adopt BPaaS and specialized outsourcing models when internal scale is too limited for large capital investment.

Competitive Landscape

The United States healthcare payer services market remains moderately concentrated. These firms compete across overlapping service areas, but the basis of competition is shifting away from pure labor scale and toward platform depth, integration capability, domain expertise, and the ability to deliver measurable operating outcomes. Large vendors have an advantage in payer transformation programs because they can combine consulting, implementation, managed services, analytics, and compliance support under one contract. Mid-market specialists still matter because they can move faster in targeted niches such as member engagement, payment integrity, utilization management, and workflow redesign for smaller plans. That balance keeps the United States healthcare payer services market competitive, even though a relatively small group of vendors still shapes the largest deals.

Technology execution is now the clearest differentiator because payers want evidence that automation tools can work safely in production and not just in controlled pilot settings. Aetna’s May 2026 launch of its Claims Automation Model gave the market a concrete example of production AI tied to better processing speed, which raises the standard that vendors must meet when they position AI-led claims solutions. Genpact’s acquisition of XponentL Data in June 2025 showed a similar pattern, where vendors are buying data engineering and domain AI capabilities to deepen their healthcare and life sciences delivery stack. Accenture Federal Services also expanded its public-sector payer-adjacent position in February 2026 when it was selected to support the VA Electronic Health Record Modernization program, a large digital transformation engagement tied to health administration at a national scale. These moves show that the United States healthcare payer services market is rewarding vendors that can combine data infrastructure, AI, and complex program delivery in the same commercial offering.

Competition is also widening down-market because small and mid-sized payers need the same compliance and modernization capabilities as national plans, but often lack the staff and capital to build them internally. Cognizant highlighted its expansion into small and mid-sized payer clients in March 2026, which points to a meaningful opportunity outside the largest national accounts. Conduent’s 2025 10-K also acknowledged intensifying competition from Genpact, Wipro, and EXL, reinforcing that established vendors are defending share against rivals that now offer similar platform-oriented operating models. Overall, the United States healthcare payer services market is becoming harder to win through scale alone because buyers increasingly evaluate vendors on security discipline, implementation certainty, workflow intelligence, and their ability to improve administrative performance without disrupting core payer operations.

United States Healthcare Payer Services Industry Leaders

Accenture plc

Centene Corporation

CVS Health

IBM Corporation

UnitedHealth Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CVS Health's Aetna deployed its Claims Automation Model (CAM), an AI agent platform that reduced complex claims processing time by more than 20%, with the tool integrating eligibility, coverage, member, and provider data to automate resolutions and recommend next-best actions. This deployment marks a shift from augmentation to production AI in claims workflows for a top-5 US insurer.

- March 2026: CommonSpirit Health and Humana reached a three-year national Medicare Advantage contract, reestablishing in-network access across CommonSpirit's 24-state footprint, including Colorado and Texas, ending nearly a year of negotiations that had disrupted MA member access in multiple markets.

- March 2026: CMS issued a final rule establishing the first HIPAA-adopted national standards for the electronic exchange of clinical documentation attachments, effective May 26, 2026, with a 2028 compliance deadline and estimated annual savings of USD 781 million. This rule directly expands the IT and BPO outsourcing mandate for payers still relying on fax-based documentation submission.

- February 2026: Accenture Federal Services was selected to support the VA Electronic Health Record Modernization (EHRM) program under a 4.5-year contract, covering digital transformation services for more than 9 million veterans and representing a significant public payer IT outsourcing engagement.

United States Healthcare Payer Services Market Report Scope

The United States Healthcare Payer Services Market comprises the administrative, operational, and financial services outsourced by organizations that finance or reimburse healthcare costs, such as private insurance companies, government agencies, and employers. Its primary purpose is to streamline claims processing, member management, billing, and fraud detection to reduce operational costs.

The United States healthcare payer services market is segmented across several dimensions. By service type, it includes Claims Management Services, Billing and Payment Services, Fraud Detection and Payment Integrity Services, Analytics Services, Knowledge Process Outsourcing Services, Information Technology Outsourcing Services, and Business Process Outsourcing Services. By application, the market is divided into Health Insurance, Life Insurance, Managed Care, and Public Programs. Finally, by end use, the segmentation covers Private Payers, Public Payers, and Employer-Sponsored Plans.

| Claims Management Services |

| Billing and Payment Services |

| Fraud Detection and Payment Integrity Services |

| Analytics Services |

| Knowledge Process Outsourcing Services |

| Information Technology Outsourcing Services |

| Business Process Outsourcing Services |

| Health Insurance |

| Life Insurance |

| Managed Care |

| Public Programs |

| Private Payers |

| Public Payers |

| Employer-Sponsored Plans |

| By Service Type | Claims Management Services |

| Billing and Payment Services | |

| Fraud Detection and Payment Integrity Services | |

| Analytics Services | |

| Knowledge Process Outsourcing Services | |

| Information Technology Outsourcing Services | |

| Business Process Outsourcing Services | |

| By Application | Health Insurance |

| Life Insurance | |

| Managed Care | |

| Public Programs | |

| By End Use | Private Payers |

| Public Payers | |

| Employer-Sponsored Plans |

Key Questions Answered in the Report

What is the 2031 value of the United States healthcare payer services space?

The United States healthcare payer services market is projected to reach USD 56.79 billion by 2031, rising from USD 34.57 billion in 2025 at an 8.76% CAGR from 2026 to 2031.

Which service category leads revenue generation?

Information Technology Outsourcing Services leads the mix with 31.48% share in 2025 because payers still rely heavily on outside partners for modernization, integration, compliance, and cybersecurity support.

Which application area is expanding the fastest?

Managed Care is the fastest-growing application segment, with a projected 10.29% CAGR through 2031, supported by rising prior authorization and risk-bearing administrative workload.

Why are payers outsourcing more operations now?

Payers are outsourcing more because administrative automation still has a large savings opportunity, while interoperability mandates, prior authorization rules, and complex value-based contracts are increasing internal workload.

What is changing in vendor competition?

Competition is moving toward platform-led contracts where vendors are expected to prove faster claims handling, better workflow control, stronger security, and production-ready AI rather than only offering low-cost labor.

Which end-user group offers the strongest growth outlook?

Public Payers show the fastest end-use growth at 9.07% CAGR through 2031 as states and public programs invest in eligibility systems, compliance workflows, and digital administration support.

Page last updated on: