U.S. Healthcare IT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

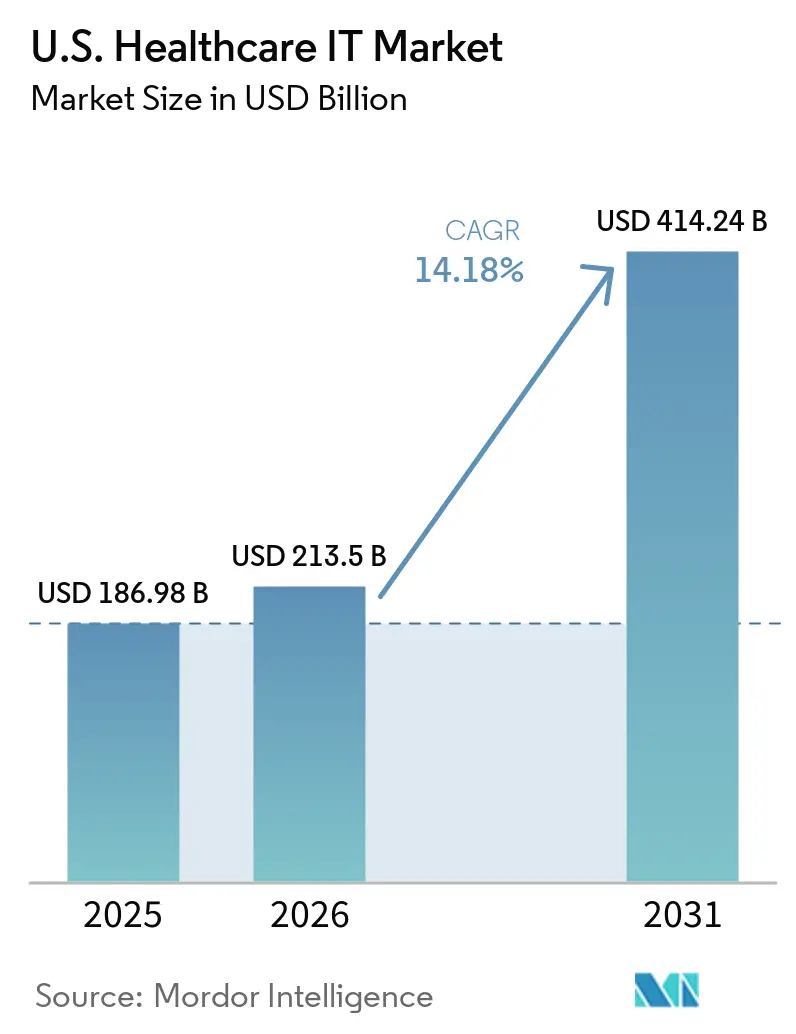

| Base Year Market Size (2025) | USD 186.98 Billion |

| Market Size (2026) | USD 213.5 Billion |

| Market Size (2031) | USD 414.24 Billion |

| Growth Rate (2026 - 2031) | 14.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Healthcare IT Market Analysis by Mordor Intelligence

The U.S. Healthcare IT Market size is expected to increase from USD 186.98 billion in 2025 to USD 213.5 billion in 2026 and reach USD 414.24 billion by 2031, growing at a CAGR of 14.18% over 2026-2031.

Federal regulations are driving rapid digitization in the United States Healthcare IT market, with strict deadlines for interoperability, prior authorization, and data exchange among payers, providers, and software developers. Providers are increasingly adopting AI-driven automation to address documentation challenges, improve throughput, and control labor costs as profit margins remain under pressure. Fragmented care delivery continues to prioritize investments in interoperability, workflow orchestration, and patient access tools, particularly for seamless data exchange across hospitals, physician groups, payers, and post-acute settings. The shift to value-based reimbursement models and growing digital-first patient expectations are fueling demand for analytics, care gap closure, and engagement platforms that integrate directly into existing workflows.

Key Report Takeaways

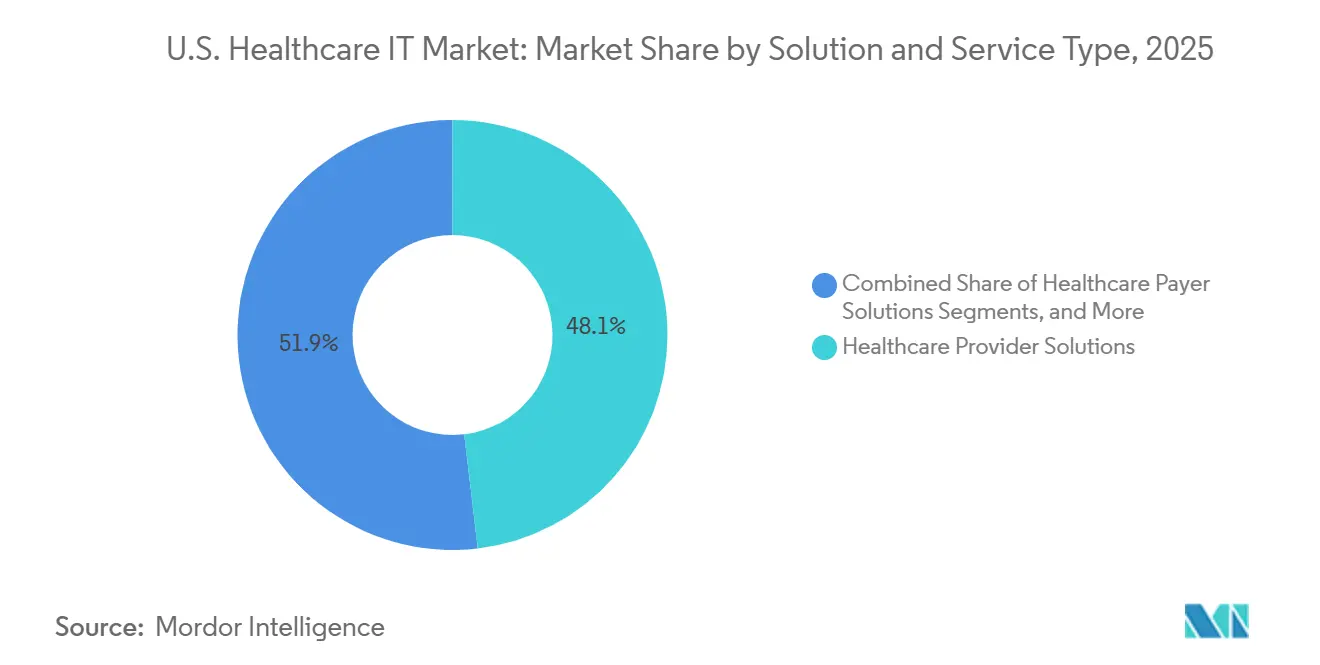

- By solution and service type, healthcare provider solutions held 48.12% of the U.S. healthcare IT market share in 2025, while healthcare payer solutions are projected to expand at a 15.20% CAGR through 2031.

- By component, services accounted for 71.7% of the U.S. healthcare IT market size in 2025, while software and platforms are forecast to grow at a 15.99% CAGR through 2031.

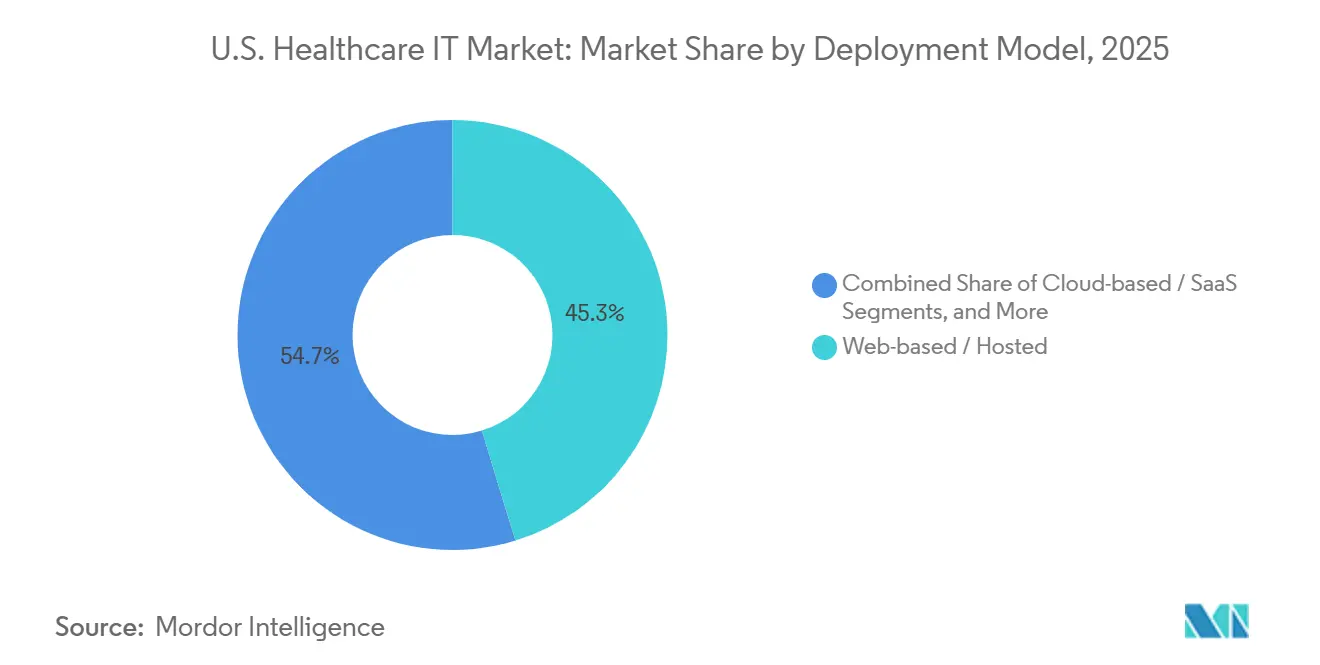

- By deployment model, web-based or hosted deployments held 45.27% share in 2025, while cloud-based or saas deployments are projected to advance at a 14.34% CAGR through 2031.

- By end user, healthcare providers commanded 68.45% share in 2025, while life sciences and research organizations are projected to register a 15.25% CAGR through 2031.

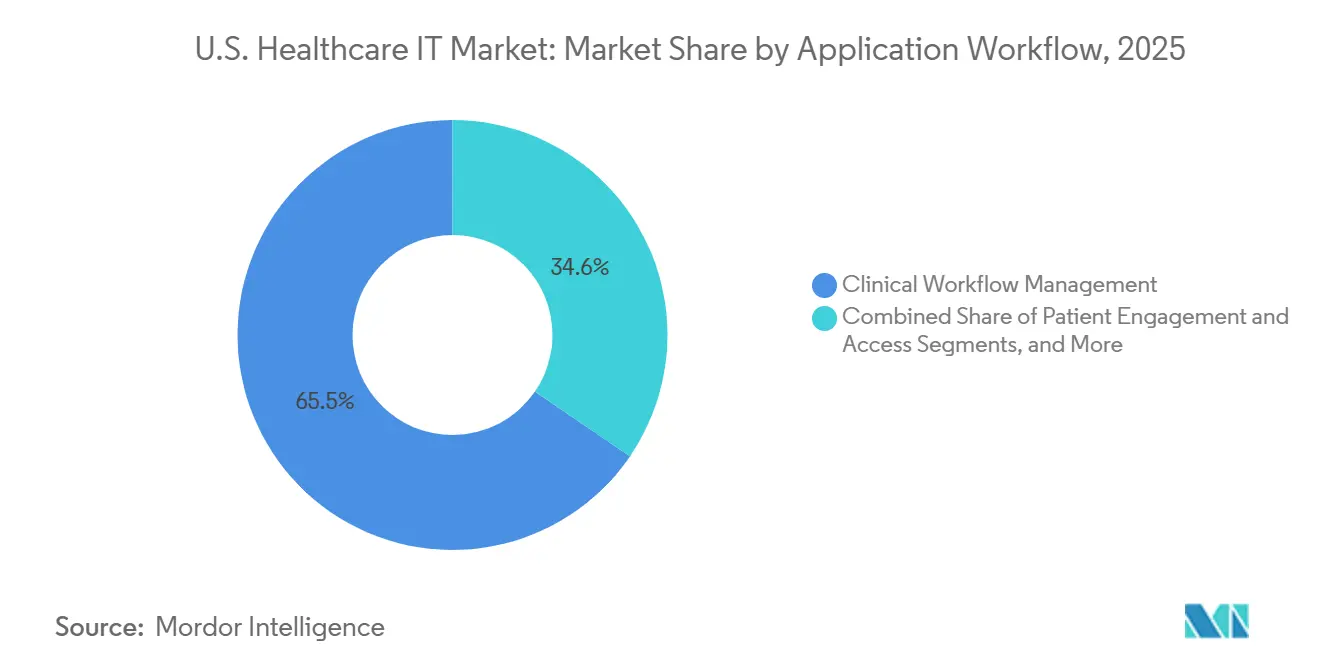

- By application, clinical workflow management captured 65.45% share in 2025, while patient engagement and access are forecast to grow at a 14.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Healthcare IT Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-enabled clinical and administrative workflow automation | +4.2% | US-wide, highest adoption in large IDNs and academic medical centers | Short term (≤ 2 years) |

| Interoperability and information-blocking compliance mandates | +3.0% | US-wide, driven by CMS and ONC federal mandates | Medium term (2-4 years) |

| Shift to value-based care and population health analytics | +2.5% | US-wide, most advanced in states with high Medicare Advantage penetration | Medium term (2-4 years) |

| Continued digitization of provider workflows and patient access | +2.2% | US-wide, with accelerated pace in ambulatory and post-acute settings | Short term (≤ 2 years) |

| Electronic prior authorization and payer api buildout | +1.8% | US-wide, mandated for all CMS-regulated payers under CMS-0057-F | Medium term (2-4 years) |

| Data-liquidity buildout across post-acute and behavioral settings | +1.4% | US-wide, with early deployment in community mental health and skilled nursing networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Clinical and Administrative Workflow Automation

In the United States Healthcare IT market, health systems are prioritizing AI-driven solutions like ambient AI scribing and agentic orchestration to achieve measurable workflow improvements in clinical and administrative systems. Oracle Health introduced its Clinical AI Agent in March 2026, reporting significant physician time savings and reduced documentation efforts. As these capabilities integrate into enterprise EHRs, standalone tools face pricing pressures, while vendors with established platforms gain an advantage by linking automation to broader contracts. Regulatory momentum, such as HHS's HTI-5 proposed rule, further emphasizes the compliance value of AI-enabled data access.

Interoperability and Information-Blocking Compliance Mandates

Interoperability compliance in the United States Healthcare IT market has transitioned from a strategic goal to an operational necessity, with financial and certification penalties for non-compliance. HHS and OIG announced active enforcement of information-blocking penalties, while the HTI-5 proposal tightened exceptions and required legacy API updates for broader data exchange. This urgency drives sustained spending on TEFCA connectivity, FHIR upgrades, and interoperability middleware throughout the forecast period.

Shift to Value-Based Care and Population Health Analytics

The shift to value-based reimbursement in the United States Healthcare IT market is increasing demand for tools that enhance risk capture, care gap management, and quality reporting. Inovalon’s Integrated Care Gap Closure, launched in October 2025, embeds analytics into EHR workflows, improving real-time decision-making. Life sciences organizations are also leveraging these tools for real-world data access and trial recruitment, creating new revenue streams beyond traditional provider software budgets.

Electronic Prior Authorization and Payer API Buildout

Electronic prior authorization is a key growth driver in the United States Healthcare IT market, with compliance deadlines accelerating investments in API infrastructure and automation. CMS mandates require payers to meet expedited and standard request timelines by January 2026, with full FHIR-based API deployment by January 2027.[1]Office of the National Coordinator for Health Information Technology, “Enforcement Alert,” HealthIT.gov, healthit.gov These regulations are expected to generate significant cost savings while driving a multi-year implementation wave, keeping this segment active despite tightening provider budgets.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cybersecurity and privacy burden | -2.5% | US-wide, US records the highest per-incident breach cost globally | Short term (≤ 2 years) |

| High implementation cost and legacy integration complexity | -2.0% | US-wide, most acute among critical-access hospitals and community health systems | Medium term (2-4 years) |

| Ai governance and workflow-level liability concerns | -1.2% | US-wide, with emerging FDA, ONC, and state-level AI oversight frameworks | Medium term (2-4 years) |

| Sensitive-data consent complexity in specialty care exchange | -0.8% | US-wide, particularly in behavioral health and substance use disorder care settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Privacy Burden

Cybersecurity challenges continue to restrain the United States Healthcare IT market as new APIs, cloud connections, and AI tools expand the attack surface organizations must manage. The average cost of a healthcare data breach reached USD 7.42 million in 2025, highlighting the financial impact. Cyber incidents, such as the Change Healthcare breach affecting 192.7 million individuals, demonstrate how third-party disruptions can compromise claims, payments, and care access.[2]Centers for Medicare & Medicaid Services, “CMS Finalizes Rule to Expand Access to Health Information and Improve the Prior Authorization Process,” CMS Newsroom, cms.govThese challenges force health systems to prioritize spending on monitoring, identity controls, and incident response, slowing the adoption of new applications. Additionally, AI adoption adds governance complexities, further impacting market expansion.

High Implementation Cost and Legacy Integration Complexity

High implementation costs and legacy system integration complexities hinder the United States Healthcare IT market, particularly in organizations with limited budgets and significant technical debt. Many still operate outdated interfaces and fragmented systems that are difficult to migrate to modern cloud environments. Even with subscription-based software models, costs related to workflow redesign, interface rebuilding, and staff training remain substantial. Smaller providers and rural systems face the greatest burden, as multi-year contracts often rely on operating budgets. While proposed regulatory changes could reduce compliance costs starting in 2027, current integration challenges will persist throughout the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution & Service Type: Payer IT Acceleration Redraws the Revenue Mix

In 2025, Healthcare Provider Solutions accounted for 48.12% of the United States Healthcare IT market, driven by investments in clinical information systems, EHR platforms, revenue cycle tools, and patient-facing applications. Core clinical systems remain essential for documentation, orders, prescribing, and operational coordination, with updates focusing on AI integration, workflow redesign, cloud transitions, and interoperability.

Healthcare Payer Solutions is the fastest-growing segment, with a forecast CAGR of 15.20% through 2031, fueled by tools for prior authorization, care management, fraud analytics, and payment integrity. Federal compliance requirements are driving payer-side investments, aligning them with provider workflows.

By Component: Services Revenue Leads While Software Platforms Accelerate Fastest

In 2025, services dominated the United States Healthcare IT market with a 71.7% share, reflecting reliance on outsourcing, managed services, consulting, and revenue cycle operations. Large health systems prefer service-intensive models to manage infrastructure, cybersecurity, cloud migrations, and workflow transformations, ensuring operational risk is shared with external partners.

Software and Platforms, growing at a CAGR of 15.99% through 2031, are driven by AI-enabled EHRs, cloud analytics, and interoperability middleware. Buyers are increasing software investments to automate documentation, enhance patient access, and streamline workflows. Despite rapid software growth, services remain critical for integration, change management, and training, maintaining their role as the largest revenue contributor.

By Deployment Model: Cloud Momentum Builds Against Installed-Base Inertia

In 2025, web-based or hosted deployments accounted for 45.27% of the United States Healthcare IT market, reflecting a shift from on-premises systems during earlier EHR modernization cycles. Hybrid deployment models are prevalent, balancing modern analytics and AI tools with the need for continuity in legacy systems.

Cloud-based or SaaS deployment, with a forecast CAGR of 14.34% through 2031, is gaining traction due to its scalability, rapid updates, and alignment with subscription models. However, migration remains gradual due to complexities in transitioning core clinical data and workflows, ensuring a prolonged hybrid phase before cloud dominance.

By End User: Provider Dominance Holds While Life Sciences Broadens Demand

In 2025, Healthcare Providers held 68.45% of the United States Healthcare IT market, driven by spending across acute care, ambulatory care, post-acute settings, and behavioral health. Providers focus on layering AI and automation tools onto existing EHR platforms to address immediate challenges while maintaining enterprise systems.

Life Sciences and Research Organizations, growing at a CAGR of 15.25% through 2031, are increasing investments in real-world data platforms, AI-driven recruitment, and patient identification tools. Research entities seek integrated provider workflows for patient access and evidence, while payers accelerate investments to meet federal compliance deadlines.

By Application / Workflow: Clinical Automation Leads While Engagement Scales Faster

In 2025, Clinical Workflow Management captured 65.45% of the United States Healthcare IT market, encompassing scheduling, documentation, order management, and care coordination. Integrated clinical platforms are evolving with AI to enhance operational efficiency and reduce administrative burdens.

Patient Engagement and Access, with a forecast CAGR of 14.90% through 2031, is growing rapidly due to demand for digital-first interactions and tools like patient portals, telehealth coordination, and remote monitoring. These applications improve access, streamline workflows, and reduce administrative workloads, complementing the dominance of clinical systems.

Geography Analysis

In 2026, the United States Healthcare IT market was valued at USD 213.50 billion, with projections reaching USD 414.34 billion by 2031. This growth is driven by federal policies and national vendor strategies. Key regulations, including CMS-0057-F, the ONC's 21st Century Cures Act enforcement, and TEFCA expansion, are shaping demand. By January 2026, payers must meet prior authorization deadlines, and full FHIR-based API deployment is required by January 2027. These mandates necessitate investments in payer systems, provider workflows, middleware, and compliance services. Security remains a priority due to rising costs from cyber incidents.

Regional adoption in the United States is influenced by provider system size, payer mix, and state-level policies. Large integrated delivery networks in the Northeast, Mid-Atlantic, and West Coast dominate enterprise EHR, analytics, and outsourcing contracts due to their complex operations. In contrast, community health systems in the South and rural Midwest represent growth opportunities for ambulatory EHRs, revenue cycle services, and population health tools. States like California, Texas, New York, and Florida, with significant managed Medicaid populations, drive payer-side investments alongside Medicaid modernization and API requirements.

Behavioral health and post-acute care settings remain under-digitized compared to acute care and physician enterprises. Expanding data liquidity in community mental health and skilled nursing networks is becoming critical as interoperability expectations grow. State mental health IT mandates and expanded telemental health reimbursements post-COVID are narrowing the gap, though implementation varies. The United States Healthcare IT market reflects nationwide demand with varying adoption rates based on scale, funding, and readiness.

Competitive Landscape

In the United States Healthcare IT market, the platform layer is moderately concentrated, while point solutions remain fragmented, creating varied competitive conditions across product categories. By early 2026, Epic Systems held a 43.7% share of the United States acute care hospital market and managed 56.9% of hospital beds. Epic's dominance is reinforced by its bundling strategy, integrating features like ambient documentation and population health into its platform, making it challenging for smaller AI vendors to secure large-scale contracts unless they address niche areas. Oracle Health is focusing on voice-enabled clinical workflows and payer-provider data exchange, with its Clinical AI Agent widely available since March 2026.

In revenue cycle management, buyers prioritize denial prevention, claim performance, automation depth, and integration quality over clinical breadth. Waystar expanded its collaboration with Google Cloud in March 2026, integrating Gemini models into its autonomous revenue cycle platform. The company reported that AltitudeAI prevented over USD 15 billion in denied claims within its first year, emphasizing the importance of financial outcomes in vendor selection. R1 RCM and Optum remain key competitors, as large providers seek partners capable of combining software, services, and operational expertise at scale.

Opportunities are strongest in behavioral health IT, post-acute informatics, and specialty workflow automation, where vendors like Netsmart Technologies and TruBridge have established significant positions. These niches are likely to attract acquisition interest as larger platforms aim to expand into community mental health and critical-access hospital environments. Federal API compliance is a critical factor, as vendors unable to deliver FHIR-ready connectivity by 2027 will face reduced appeal to payers and providers. The United States Healthcare IT market increasingly rewards vendors that combine established relationships with compliance, workflow improvements, and reliable execution.

U.S. Healthcare IT Industry Leaders

Epic Systems Corporation

Oracle Corporation

Koninklijke Philips N.V.

GE HealthCare

eClinicalWorks LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CMS launched the Early Adopters initiative to expedite electronic prior authorization solutions ahead of the January 2027 API compliance deadline.

- April 2026: CMS proposed extending electronic prior authorization to pharmaceutical benefits, with compliance set for October 2027 and a shift to FHIR-based standards.

- April 2026: ONC and OIG updated their enforcement alert, emphasizing that obstructing automation technologies like agentic AI could incur penalties under the 21st Century Cures Act.

- March 2026: Oracle Health introduced its Clinical AI Agent nationwide, saving over 200,000 physician documentation hours and reducing ambulatory documentation time by 41% for AtlantiCare.

- March 2026: Waystar expanded its collaboration with Google Cloud, integrating Gemini models and preventing over USD 15 billion in denied claims within a year.

U.S. Healthcare IT Market Report Scope

As per scope of the report, U.S. Healthcare IT refers to the hardware, software, and networking systems used across the American medical industry to compile, store, analyze, and share health information. It connects patients, healthcare providers, and insurance payers to improve patient safety, streamline workflows, and ensure regulatory compliance.

The U.S. Healthcare IT market is segmented by solution & service type, component, deployment model, end-user, and application/workflow. By solution & service type, the market includes healthcare provider solutions, healthcare payer solutions, and healthcare IT outsourcing and managed services. By component, the market is segmented into software and platforms, hardware, devices, infrastructure, and services. By deployment model, the market is segmented into on-premises, web-based/hosted, cloud-based/SaaS, and hybrid. By end-user, the market is segmented into healthcare providers, healthcare payers, life sciences and research organizations, government and public health agencies, and employers, purchasers, and TPAs. By application/workflow, the market is segmented into clinical workflow management, financial and administrative workflow, patient engagement and access, data exchange, analytics and intelligence, and imaging, diagnostics and departmental informatics. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Healthcare Provider Solutions | Clinical Information Systems | EHR / EMR Systems |

| Computerized Provider Order Entry Systems | ||

| Clinical Decision Support Systems | ||

| e-Prescribing Systems | ||

| Medication Administration / Pharmacy Information Systems | ||

| Laboratory Information Systems | ||

| Radiology Information Systems / PACS / VNA | ||

| Cardiology Information Systems | ||

| Other Specialty Departmental Systems | ||

| Non-clinical Provider Solutions | Revenue Cycle Management | |

| Practice Management | ||

| Scheduling and Patient Flow Management | ||

| Workforce Management | ||

| Claims, Billing and Payment Collection | ||

| Patient-Facing and Virtual Care Solutions | Patient Portals | |

| Telehealth / Virtual Care Platforms | ||

| Remote Patient Monitoring Platforms | ||

| Digital Front Door / Self-scheduling / Contact Center Tools | ||

| Data, Analytics and Interoperability Solutions | Health Information Exchange | |

| Population Health Management | ||

| Care Management Platforms | ||

| Clinical Data Repositories / Data Platforms | ||

| Interoperability / FHIR / API Management | ||

| AI-enabled Documentation, Coding and Workflow Automation | ||

| Healthcare Payer Solutions | Claims Management | |

| Care Management | ||

| Fraud, Waste and Abuse Analytics | ||

| Utilization Management / Prior Authorization | ||

| Member Engagement / CRM | ||

| Payment Integrity, Risk Adjustment and Quality Analytics | ||

| Healthcare IT Outsourcing and Managed Services | Revenue Cycle Outsourcing | |

| IT Consulting and Implementation | ||

| Managed Infrastructure, Cloud and Security Services | ||

| Application Management and Support | ||

| Clinical Documentation and Coding Outsourcing | ||

| Software and Platforms |

| Hardware, Devices and Infrastructure |

| Services |

| On-premises |

| Web-based / Hosted |

| Cloud-based / SaaS |

| Hybrid |

| Healthcare Providers |

| Healthcare Payers |

| Life Sciences and Research Organizations |

| Government and Public Health Agencies |

| Employers, Purchasers and TPAs |

| Clinical Workflow Management |

| Financial and Administrative Workflow |

| Patient Engagement and Access |

| Data Exchange, Analytics and Intelligence |

| Imaging, Diagnostics and Departmental Informatics |

| By Solution & Service Type | Healthcare Provider Solutions | Clinical Information Systems | EHR / EMR Systems |

| Computerized Provider Order Entry Systems | |||

| Clinical Decision Support Systems | |||

| e-Prescribing Systems | |||

| Medication Administration / Pharmacy Information Systems | |||

| Laboratory Information Systems | |||

| Radiology Information Systems / PACS / VNA | |||

| Cardiology Information Systems | |||

| Other Specialty Departmental Systems | |||

| Non-clinical Provider Solutions | Revenue Cycle Management | ||

| Practice Management | |||

| Scheduling and Patient Flow Management | |||

| Workforce Management | |||

| Claims, Billing and Payment Collection | |||

| Patient-Facing and Virtual Care Solutions | Patient Portals | ||

| Telehealth / Virtual Care Platforms | |||

| Remote Patient Monitoring Platforms | |||

| Digital Front Door / Self-scheduling / Contact Center Tools | |||

| Data, Analytics and Interoperability Solutions | Health Information Exchange | ||

| Population Health Management | |||

| Care Management Platforms | |||

| Clinical Data Repositories / Data Platforms | |||

| Interoperability / FHIR / API Management | |||

| AI-enabled Documentation, Coding and Workflow Automation | |||

| Healthcare Payer Solutions | Claims Management | ||

| Care Management | |||

| Fraud, Waste and Abuse Analytics | |||

| Utilization Management / Prior Authorization | |||

| Member Engagement / CRM | |||

| Payment Integrity, Risk Adjustment and Quality Analytics | |||

| Healthcare IT Outsourcing and Managed Services | Revenue Cycle Outsourcing | ||

| IT Consulting and Implementation | |||

| Managed Infrastructure, Cloud and Security Services | |||

| Application Management and Support | |||

| Clinical Documentation and Coding Outsourcing | |||

| By Component | Software and Platforms | ||

| Hardware, Devices and Infrastructure | |||

| Services | |||

| By Deployment Model | On-premises | ||

| Web-based / Hosted | |||

| Cloud-based / SaaS | |||

| Hybrid | |||

| By End User | Healthcare Providers | ||

| Healthcare Payers | |||

| Life Sciences and Research Organizations | |||

| Government and Public Health Agencies | |||

| Employers, Purchasers and TPAs | |||

| By Application / Workflow | Clinical Workflow Management | ||

| Financial and Administrative Workflow | |||

| Patient Engagement and Access | |||

| Data Exchange, Analytics and Intelligence | |||

| Imaging, Diagnostics and Departmental Informatics | |||

Key Questions Answered in the Report

What is the current value of the US healthcare IT sector in 2026?

The US Healthcare IT market stands at USD 213.50 billion in 2026 and is projected to reach USD 414.34 billion by 2031 at a 14.18% CAGR.

What is driving growth in healthcare IT spending in the United States?

The main growth drivers are federal interoperability and prior authorization mandates, AI-enabled workflow automation, value-based care analytics, and continued digitization of patient access and provider workflows.

Which solution category leads revenue in US healthcare IT?

Healthcare Provider Solutions led with 48.12% share in 2025, supported by broad spending on EHRs, clinical information systems, revenue cycle tools, and patient-facing applications.

Which area is expanding fastest over the forecast period?

Healthcare Payer Solutions is the fastest-growing solution category at a 15.20% CAGR, while Software and Platforms is the fastest-growing component at 15.99% CAGR.

Why is electronic prior authorization important for vendors and buyers?

CMS compliance deadlines require faster payer responses from January 2026 and full FHIR-based Prior Authorization APIs by January 2027, which is pushing new spending across payer platforms, EHR connectors, and workflow automation tools.

What is the biggest risk slowing digital expansion in this space?

Cybersecurity remains the main restraint because breach exposure, third-party vulnerability, AI governance, and compliance spending divert budget away from new product rollouts and delay some implementations.

Page last updated on: