United States Connected Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

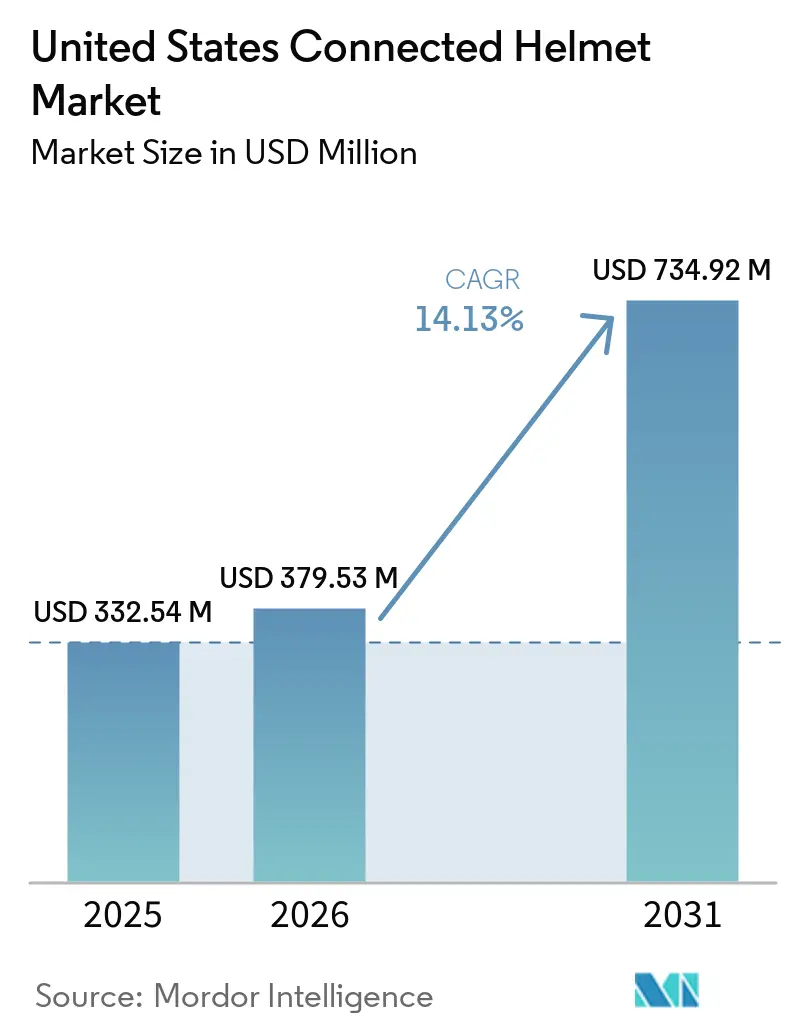

| Base Year Market Size (2025) | USD 332.54 Million |

| Market Size (2026) | USD 379.53 Million |

| Market Size (2031) | USD 734.92 Million |

| Growth Rate (2026 - 2031) | 14.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Connected Helmet Market Analysis by Mordor Intelligence

The United States connected helmet market size is projected to grow from USD 332.54 million in 2025 to USD 379.53 million in 2026 and is forecast to reach USD 734.92 million by 2031, growing at a CAGR of 14.13% from 2026 to 2031. Under the Infrastructure Investment and Jobs Act (IIJA), regulatory advancements, coupled with increased V2X roadside-unit density and city-level mandates for gig-worker safety, are transforming helmets from mere protective gear into active participants in cooperative perception. The National Highway Traffic Safety Administration's (NHTSA) decision to withdraw proposed amendments to FMVSS 218 showcases a flexible federal oversight, allowing manufacturers to integrate antennas and edge modules without the looming risk of recertification. Demand from fleet operators is surging, as evidenced by pilots from DoorDash, Uber Eats, and Amazon logistics, which highlight a tangible drop in injury claims thanks to features that expedite EMS dispatch during crashes. With e-commerce commanding a significant share of the channel, it's clear that today's digital-savvy riders prioritize researching firmware, battery longevity, and over-the-air update capabilities before making a purchase.

Key Report Takeaways

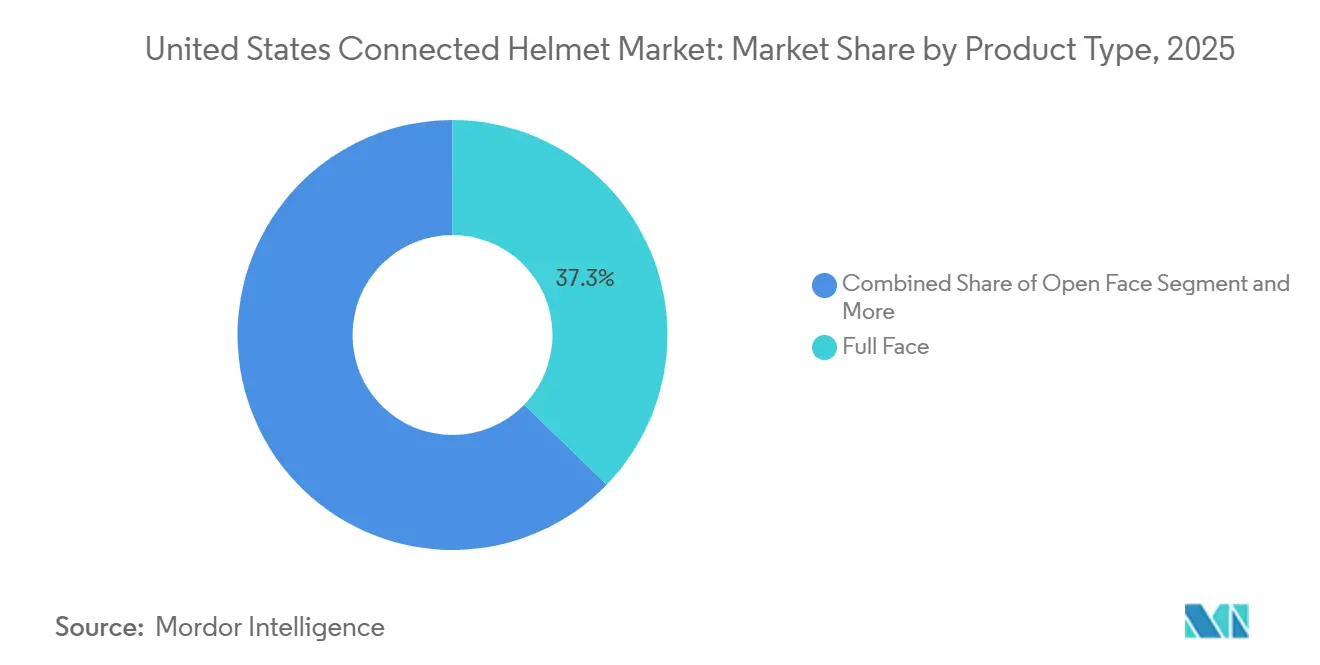

- By product type, full-face models held 37.26% of the United States connected helmet market share in 2025, while HUD-integrated helmets are forecast to grow at a 14.67% CAGR through 2031.

- By technology level, integrated audio systems accounted for a 33.19% of the United States connected helmet market share in 2025; ADAS sensor suites posted the fastest growth rate at a 14.34% CAGR through 2031.

- By end user, individual riders accounted for 55.22% of the United States connected helmet market share in 2025, yet fleet and delivery operators expanded at a 14.61% CAGR under municipal mandates.

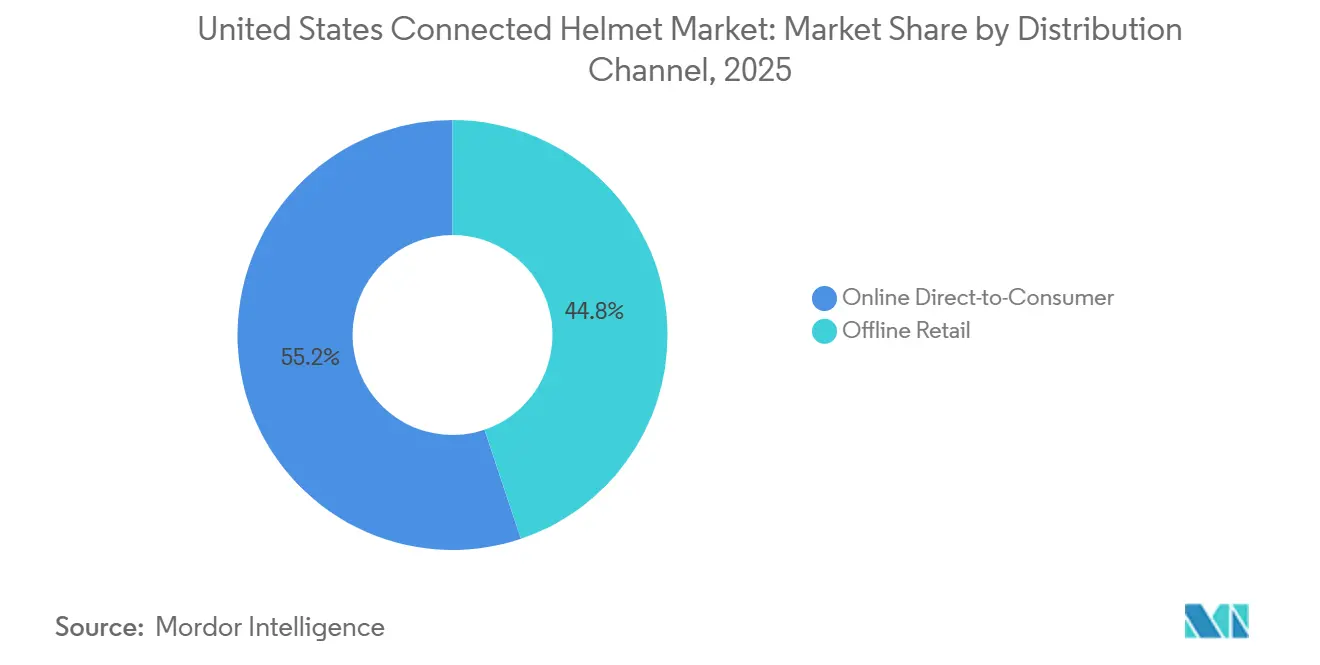

- By distribution, online direct-to-consumer platforms captured 55.17% of the United States connected helmet market share in 2025 and are projected to grow at a 14.72% CAGR through 2031.

- By price range, premium helmets priced above USD 600 accounted for 47.18% of the United States connected helmet market share in 2025; the mid-range tier grew fastest at a 14.47% CAGR, helped by insurance-linked discounts.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with United states being one of the contributors. Our global connected helmet market size represents that cumulative total.

United States Connected Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent DOT-Compliant Safety Mandates | +3.2% | National, with early enforcement in California, New York, Texas | Medium term (2-4 years) |

| Expansion of Direct-To-Consumer E-Commerce Channels | +2.8% | National, concentrated in urban markets | Short term (≤ 2 years) |

| Integration of V2X Chips | +2.5% | IIJA pilot regions: Arizona, Texas, Utah expanding nationally | Long term (≥ 4 years) |

| Micromobility Fleet Operators | +2.1% | Urban centers: NYC, SF, LA, Seattle, Austin | Short term (≤ 2 years) |

| Insurance-Premium Discounts for Verified Connected-Helmet Use | +1.9% | National, with early adoption in high-risk metropolitan areas | Medium term (2-4 years) |

| Federal IIJA Roadside V2X Pilots | +1.8% | Multi-state corridors, Connected West Project coverage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent DOT-Compliant Safety Mandates In U.S. States

Several states have enacted universal motorcycle helmet laws. In response, OEMs are embedding connected verification methods, such as NFC tags, enabling roadside officers to easily verify DOT compliance[1]“Helmet Use Laws by State,” Insurance Institute for Highway Safety, iihs.org. The decision to halt liner-thickness screenings eliminated immediate certification hurdles. This change enables brands to integrate sensors without requiring new FMVSS tests [2]“Notice of Withdrawal of FMVSS 218 NPRM,” National Highway Traffic Safety Administration, nhtsa.gov. While voluntary Snell standards introduce oblique-impact metrics, premium helmets already tout these as a marketing edge. Enforcement varies: California employs random checkpoints, while other states are more lenient. This discrepancy drives the adoption of geofenced firmware, ensuring proof of compliance is uploaded in stricter areas. As the industry anticipates future biomechanical mandates, R&D teams feel the pressure to balance shell energy dispersion with rising electronic density.

Expansion of Direct-To-Consumer E-Commerce Channels

Online portals are revolutionizing the buying experience by combining detailed listings, real-time stock visibility, and instant firmware downloads, making it hard for physical dealerships to compete. Forcite's configurator, which offers shell sizing and LED previews, has successfully reduced return rates linked to sizing issues. Younger riders are increasingly drawn to unboxing videos, Reddit AMAs, and YouTube reviews featured on product pages, creating a feedback loop that enhances conversion rates. However, these robust digital footprints can serve as evidence in liability lawsuits. To counter this, brands are turning to third-party validations, backing up claims such as "crash notification." Additionally, analytics from payment gateways are being harnessed to forecast demand, streamlining just-in-time production of carbon shells and subsequently reducing working capital needs.

Integration of V2X Chips Enabling Group-Riding Networks

Funded by the IIJA, corridors now host numerous intersection RSUs and VRU-warning sites. This development underscores the evolving role of helmets, positioning them as nodes for communication among vulnerable road users rather than merely serving as intercoms between riders. Sena’s Wave Intercom showcases a seamless transition from cellular to Mesh technology, ensuring consistent connectivity even during 5G coverage gaps [3]“Wave Intercom Technical Sheet,” Sena Technologies, sena.com. However, with SAE J2945/8 still in flux, helmet chipsets must incorporate field-upgradable radios. Tests conducted in Manhattan and Los Angeles reveal packet delays when devices cluster within a limited radius, underscoring the urgent need for edge congestion-control algorithms. Pioneering users are navigating firmware complexities, reaping the rewards of roadway alerts that were once the exclusive domain of car dashboards.

Insurance-Premium Discounts For Verified Connected-Helmet Use

Allianz Partners and Cosmo Connected introduced an embedded accident policy at EUR 9.99 monthly, exchanging verified impact data and GPS traces for immediate claim adjudication. Early enrollees report one-tenth of annual premium savings, offsetting as much as one-fifth of a premium helmet’s purchase cost within three years. U.S. carriers test similar telematics-based discounts in Chicago, Los Angeles, and Miami, focusing on high-risk age brackets under 30. Insurtech platforms integrate helmet APIs to verify active ride sessions, rewarding continuous use rather than mere ownership. These incentives accelerate replacement cycles as riders seek compliant models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost | -2.4% | National, particularly affecting price-sensitive rural markets | Short term (≤ 2 years) |

| Limited Battery Life | -1.8% | Western states with extensive touring routes | Medium term (2-4 years) |

| Bluetooth/Wi-Fi Spectrum Congestion | -1.6% | Dense metropolitan areas: NYC, LA, SF, Chicago | Short term (≤ 2 years) |

| Data-Privacy Liability Concerns | -1.3% | National, concentrated in GDPR-conscious enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Helmets

Connected helmets, priced between a range for Sena’s Phantom and Schuberth’s E2 Carbon, command a premium over DOT-approved shells that already meet legal requirements. Shoei’s GT-Air 3 Smart is tailored for riders of high-end touring bikes, sidelining budget commuters. Lifecycle costs, including battery replacements and emergency service subscriptions, increase the annual outlay. While insurer discounts can offset the price over time, adoption hinges on riders’ willingness to share location data. In states lacking helmet laws, some buyers forgo helmets entirely, exacerbating the price gap.

Limited Battery Life For Long-Distance Touring

Forcite's MK1S lasts only a few hours on a charge when its camera is recording continuously. This falls significantly short of the durations typical for rides on western highways. While Sena offers a "Safe Power Mode" that allows users to tether to a power bank, using cables compromises overall ergonomics. Off-road enthusiasts experience even shorter usage periods; the dust-proof seals, designed to protect, inadvertently trap heat, leading to quicker degradation of lithium packs. Research prototypes experimenting with wind-turbine vents deliver minimal additional power, which is inadequate for edge AI demands. As the industry awaits the arrival of higher-density battery cells, long-haul users are left with two choices: carry spare helmets or sacrifice continuous recording.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Full-Face Leads as HUD Adoption Rises

Full-face helmets accounted for 37.26% of the United States connected helmet market share in 2025, benefiting riders who emphasize wind noise reduction at highway speeds. The segment evolves as OEMs embed recesses for V2X antennas without adding drag. HUD-equipped models expand at a 14.67% CAGR, supported by Shoei’s GT-Air 3 Smart that projects FHD navigation cues three meters ahead of the rider’s line of sight, yielding 32% quicker reaction times in simulator trials. Modular flip-ups attract adventure riders who need chin-bar flexibility, while LIVALL pioneers open-face designs with bone-conduction speakers that avoid blocking ear canals.

Touring enthusiasts still favor carbon-fiber shells for weight savings. Still, mid-range fiberglass builds from Sena’s Specter show that mesh intercom and Safe Power Mode can coexist with aggressive pricing. Off-road helmets now include LED floods for night trails, broadening use cases beyond paved roads. Regulatory cap-on-projection height forces hidden camera modules inside EPS liners, so brands patent energy-dispersion channels to route impact forces around electronics.

By Technology Level: Audio Foundation, ADAS Upswing

Integrated audio accounted for 33.19% of the United States connected helmet market share in 2025, propelled by rider-to-rider mesh compatibility. Yet ADAS sensor suites, apart from audio, see a 14.34% CAGR as insurers reward eCall functionality. In the coming years, the U.S. market for helmets equipped with ADAS features is poised for rapid expansion. Shoei's HUD, utilizing Sony's OLEDoS micro-display, boasts high brightness - a feature previously exclusive to automotive clusters. Forcite integrates GPS, video, and LED navigation halos into its platform but grapples with battery-drain issues, prompting OEMs to consider swappable cell trays.

As Bluetooth modules become ubiquitous, the emphasis shifts to software innovations that leverage AI to filter out wind noise and seamlessly connect to cloud services. While multi-band antennas address V2X and LTE fallback needs, they introduce additional tuning challenges. With SAE nearing the finalization of cooperative-perception payloads, the importance of firmware roadmaps rivals that of shell materials, underscoring the growing stakes in interoperability.

By End User: Individual Riders Dominate While Fleet Delivery Accelerates

Individual riders contributed 55.22% of the United States connected helmet market share in 2025, yet their growth lags fleets’ 14.61% CAGR. The United States' connected helmet market size is tied to the scale of delivery services, as New York City’s 2025 ordinance compels app firms to log device details. DoorDash pilots report 20% cut in claim payouts where crash detection verifies impact vectors. Passenger adoption stays niche; group-ride apps like Sena’s Wave give pillions an easy on-ramp, but infrequent usage dampens ROI.

Fleets demand dashboards aggregating wear-time and GPS breadcrumbs, pushing vendors into SaaS territory. Privacy clauses add friction but also enable tiered pricing: workers who opt into full telemetry unlock higher medical-coverage caps, a stick-and-carrot tactic that gig platforms are now testing.

By Distribution Channel: Online DTC Becomes Primary Path to Market

Online cornered 55.17% of the United States connected helmet market share in 2025 and grew at a 14.72% CAGR through 2031. Search-engine visibility around “best mesh intercom helmet” directs traffic straight to brand pages with AR sizing tools. Offline dealerships still serve distress purchases after a crash, but limited floor space for multiple shell-tech combos hampers turnover. Seven-day evaluation return windows online mimic the fit assurance once unique to stores. Marketplaces also bundle firmware auto-update memberships, deepening recurring revenue.

By Price Range: Premium Tier Sets the Pace

Premium units above USD 600 accounted for 47.18% of the United States connected helmet market share in 2025, thanks to carbon shells and integrated HUDs. Yet the mid-range at USD 400–600 posts a 14.47% CAGR as Quin’s crash-chip retrofits lower the barrier to entry. The United States connected helmet market size for mid-range tiers benefits from insurer discounts that neutralize the upfront premium over three years. Economy models remain scarce because material and battery costs leave thin margins, though entry SKUs with Bluetooth-only kits may seed upgrades later via clip-on LiDAR pods.

Geography Analysis

California’s universal helmet law, its dense rider base, and its early telematics insurance trial make it the single largest slice of the United States connected helmet market revenue. Texas and Florida trail but have partial laws that temper immediate uptake; riders over 21 may ride without helmets, cutting addressable head counts. Western corridor states—Utah, Colorado, Wyoming—benefit from IIJA RSU buildouts, enabling helmets to receive roadside LiDAR alerts years before the nationwide rollout.

Northeastern states, including New York, New Jersey, and Massachusetts, show higher per-capita helmet use, offering fertile ground for HUD adoption once price curves ease. Midwest touring culture values Sena’s unlimited-range cellular intercom more than LiDAR alerts, so feature prioritization varies by zip code. Data-privacy legislation maps onto adoption: stringent CCPA in California raises compliance spend yet also clarifies rules, encouraging larger fleets to pilot smart gear. States lacking clear statutes face slower telematics penetration as legal teams advise caution.

Future spread hinges on Phase 2 V2X deployments slated for 2028–2030 that will fill geographic gaps. Once edge certificates interoperate across corridors, OEMs expect helmet firmware to switch RSU profiles automatically, making the technology seamless for interstate touring.

Coverage of the connected helmet market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for South Korea, China, Japan, and India, each shaped by local operating conditions.

Competitive Landscape

Moderate market concentration sees the top five brands accounting for a significant share of combined revenue. Sena's greenfield factory marks a bold move into vertical integration, pairing Mesh radios with composite shell molding and setting an aggressive MSRP. This move directly challenges legacy OEMs, many of whom still rely on third-party intercom vendors. GoPro's acquisition of Forcite not only enhances its portfolio but also positions content-capture services as a lucrative add-on. Subscribers of Forcite helmets might soon enjoy discounted rates on GoPro's cloud storage. Meanwhile, Shoei, with its patented optics, cements its leadership in HUD technology, and Schuberth, with its focus on carbon craftsmanship, targets the ultra-premium market.

LIVALL's innovative AI taillight and camera duo carve out a niche in fleet compliance. At the same time, Quin's chip-licensing strategy broadens crash-detection capabilities across various helmet brands, all with minimal increase in BOM. However, entering this market isn't easy; challenges include navigating SCMS certificate management and the expensive DOT testing required for each shell size. As spectrum congestion becomes a pressing issue, R&D efforts are pivoting towards beam-forming antennas and edge filtering, with a notable surge in patents related to dynamic channel selection. Yet, the industry's Achilles' heel remains battery technology. Brands forging partnerships with solid-state battery suppliers could secure a significant advantage in the future.

United States Connected Helmet Industry Leaders

Sena Technologies Inc.

Vista Outdoor

HJC Helmets

Jarvish Inc.

LIVALL Tech Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: At CES 2026, LIVALL introduced its AI Visual Smart Taillight (VG1) and the VGH10 helmet, both featuring multi-sensor fusion, 120-degree HD video, and bi-directional hazard alerts. The VG1 taillight is designed to enhance road safety by providing real-time hazard detection and alerts. At the same time, the VGH10 helmet integrates advanced AI to enhance protection and situational awareness for cyclists.

- February 2025: Sena Technologies introduced the Phantom full-face smart helmet with integrated comms and adaptive illumination from its new high-tech plant.

United States Connected Helmet Market Report Scope

The United States connected helmet market report is segmented by product type (full face, modular/flip-up, open face, half helmet, off-road/ motocross), technology level (bluetooth-only, integrated audio/comms, and HUD/AR display, crash detection and ecall, ADAS sensor suite, and multi feature), end user (individual rider, passenger, and fleet/delivery), distribution channel (offline retail and online direct-to-consumer), and price range (economy, mid-range, and premium). The market forecasts are provided in terms of value (USD).

| Full Face |

| Modular / Flip-up |

| Open Face |

| Half Helmet |

| Off-road / Motocross |

| Smart HUD-Integrated |

| Bluetooth-Only |

| Integrated Audio / Comms |

| HUD / AR Display |

| Crash Detection & eCall |

| ADAS Sensor Suite |

| Multi-Feature (All-in-One) |

| Individual Rider |

| Passenger |

| Fleet / Delivery |

| Offline Retail |

| Online Direct-to-Consumer |

| Economy |

| Mid-Range |

| Premium |

| By Product Type | Full Face |

| Modular / Flip-up | |

| Open Face | |

| Half Helmet | |

| Off-road / Motocross | |

| Smart HUD-Integrated | |

| By Technology Level | Bluetooth-Only |

| Integrated Audio / Comms | |

| HUD / AR Display | |

| Crash Detection & eCall | |

| ADAS Sensor Suite | |

| Multi-Feature (All-in-One) | |

| By End User | Individual Rider |

| Passenger | |

| Fleet / Delivery | |

| By Distribution Channel | Offline Retail |

| Online Direct-to-Consumer | |

| By Price Range | Economy |

| Mid-Range | |

| Premium |

Key Questions Answered in the Report

How large will U.S. spending on connected helmets be by 2031?

United States connected helmet market size is forecast to reach USD 734.92 million by 2031, advancing at a 14.13% CAGR from 2026.

Which product style leads sales?

Full-face helmets commanded 37.26% United States connected helmet market share in 2025, reflecting strong demand from touring and sport-bike riders.

What technology segment is growing fastest?

Helmets with ADAS sensor suites, including crash detection and V2X radios, are projected to expand at a 14.34% CAGR through 2031.

Will battery life improvements unlock new customer groups?

Yes, adoption among long-distance touring riders should accelerate once next-generation cells push continuous camera runtime beyond 8–10 hours.

How do privacy laws affect connected-helmet roll-outs?

CCPA and similar statutes require opt-in consent and breach notifications, adding compliance costs that slow deployments for smaller fleets.

Page last updated on: