HUD Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

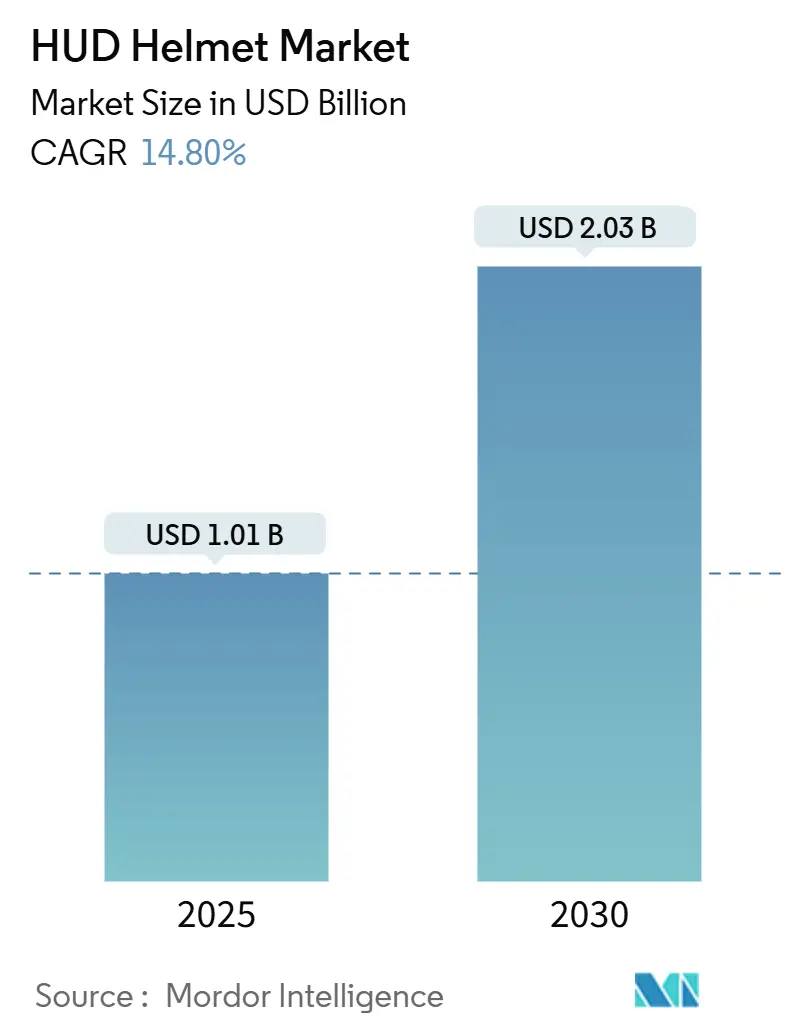

| Market Size (2025) | USD 1.01 Billion |

| Market Size (2030) | USD 2.03 Billion |

| Growth Rate (2025 - 2030) | 14.80% CAGR |

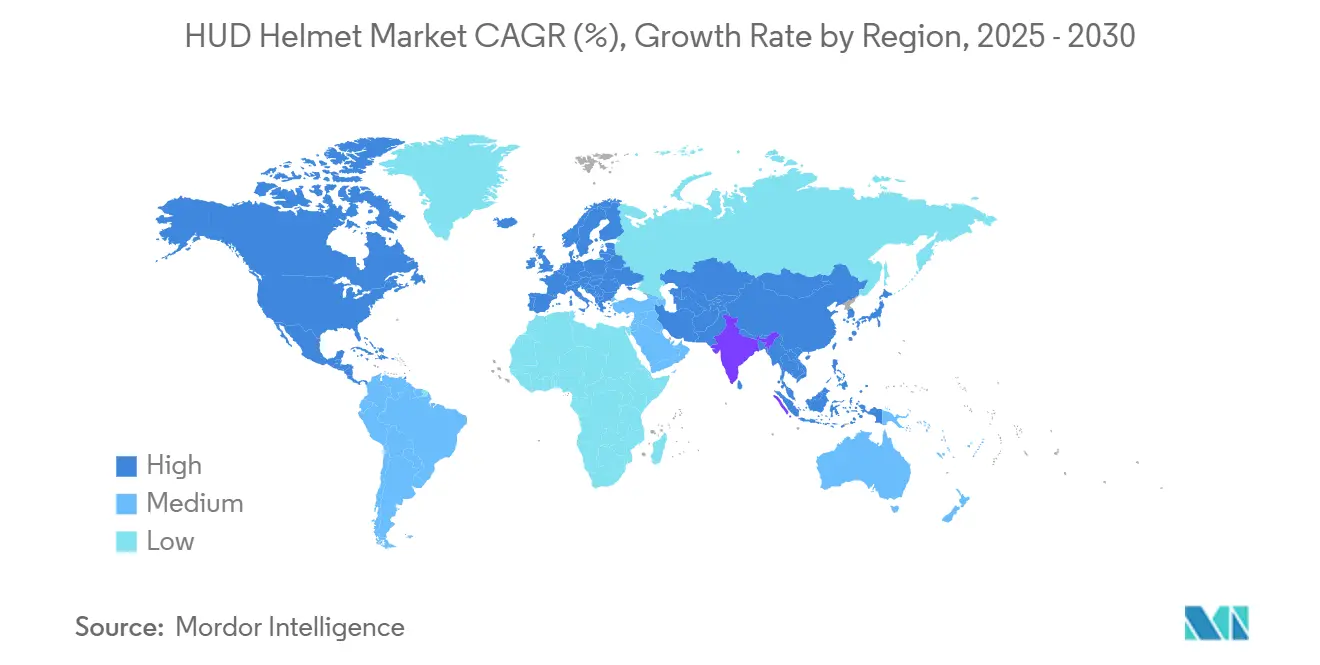

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

HUD Helmet Market Analysis by Mordor Intelligence

The HUD helmet market size stands at USD 1.01 billion in 2025 and is predicted to reach USD 2.03 billion by 2030, reflecting a 14.80% CAGR during the forecast period. This market growth phase aligns with rapid micro-OLED cost declines, stronger military validation, and the anticipated 2025 UNECE visor-display harmonization that removes long-standing regulatory uncertainty. Demand rises as insurers translate telematics data into lower premiums, while electric-scooter OEMs embed smart helmets into vehicle bundles to differentiate their offerings. Segment momentum also benefits from urban Vision Zero grants that treat connected protective gear as critical infrastructure and Asia-Pacific manufacturing clusters that keep component prices falling.

Key Report Takeaways

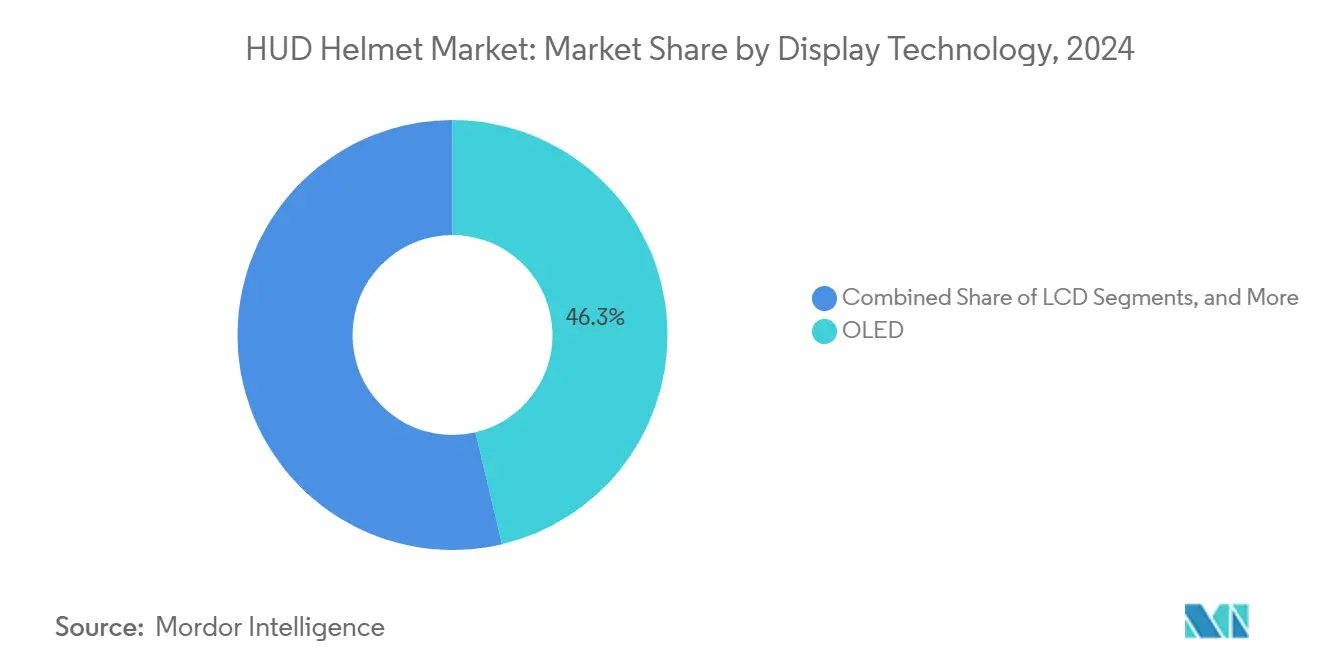

- By display technology, OLED captured 46.27% share of the HUD helmet market in 2024 and is advancing at a 22.94% CAGR through 2030.

- By connectivity, embedded solutions held a 54.12% share of the HUD helmet market in 2024, and are expected to grow at a CAGR of 24.36% through 2030.

- By helmet type, full-face models led with 62.71% share of the HUD helmet market in 2024; modular helmets are projected to expand at 27.48% CAGR to 2030.

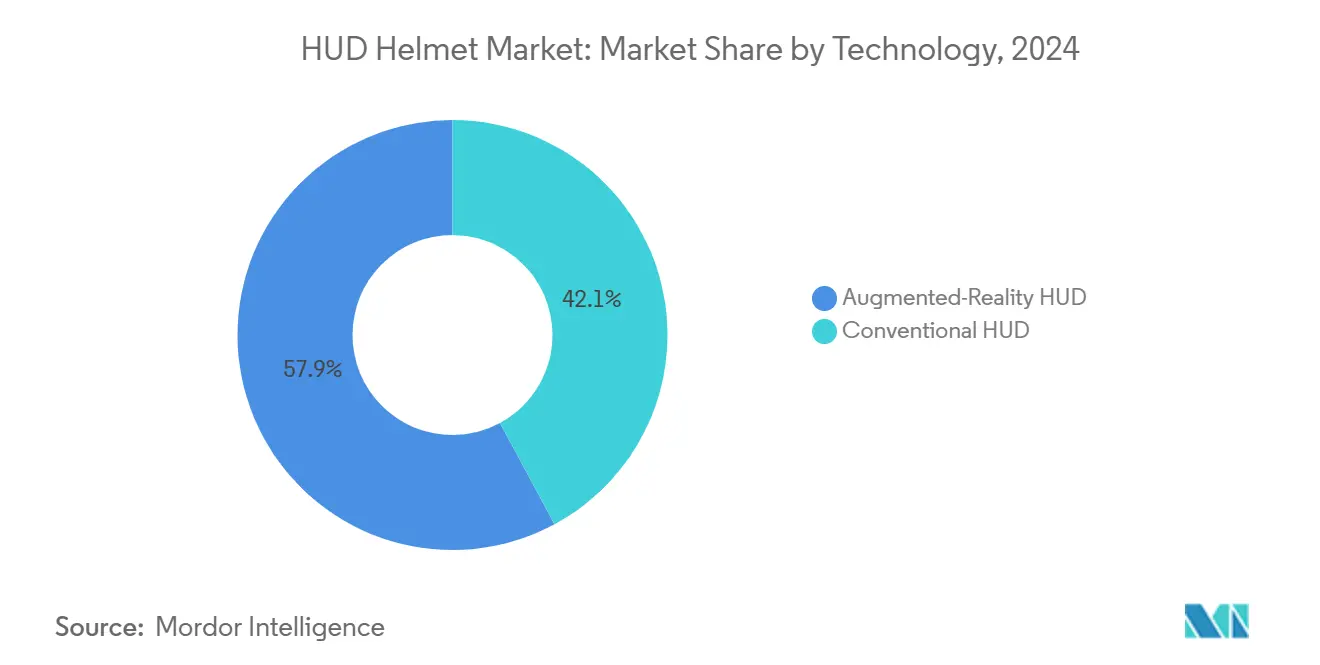

- By technology, augmented-reality HUDs had a 57.86% share of the HUD helmet market in 2024 and are poised to rise at a 29.62% CAGR during the forecast window.

- By user type, professional riders represented 54.88% of demand in 2024, whereas amateur adoption is growing at 18.47% CAGR during the forecast period.

- By application, navigation and route guidance commanded a 37.19% share of the HUD helmet market in 2024; performance monitoring is the fastest riser at 25.68% CAGR through 2030.

- By geography, Europe led with a 32.34% share of the HUD helmet market in 2024, while Asia-Pacific is the fastest-growing region with a 19.84% CAGR through 2030.

Global HUD Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Decline in Micro-OLED Cost Structure | +3.2% | Global, concentrated in Asia-Pacific manufacturing | Medium term (2-4 years) |

| Post-2025 UNECE Visor-Display Safety Harmonisation | +2.8% | Europe and countries adopting UNECE standards | Long term (≥ 4 years) |

| Rising Connected-Two-Wheeler Insurance Discounts | +2.1% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| E-Commerce Bundling by EV-Scooter OEMs | +1.9% | Asia-Pacific core, spill-over to urban centers globally | Medium term (2-4 years) |

| Urban "Vision-Zero" Funding for Smart-PPE | +1.7% | North America, Europe, select Asia-Pacific cities | Long term (≥ 4 years) |

| Military Off-Budget AR-Training Programmes | +1.5% | North America, Europe, select defense markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline In Micro-OLED Cost Structure

Manufacturing cost reductions in micro-OLED displays stem from Samsung Display and LG Display scaling production for VR headsets, creating spillover benefits for motorcycle HUD applications. Transitioning from silicon-based to glass substrates reduces material costs while improving brightness and contrast ratios essential for outdoor visibility. EyeLights leveraged these advances and launched their second-generation EyeRide HUD via Kickstarter in June 2024, demonstrating commercial viability at consumer price points. However, supply chain concentration in South Korea and Taiwan creates vulnerability to geopolitical disruptions that could reverse cost trends. Integrating micro-OLED technology into motorcycle helmets requires specialized optical systems and thermal management solutions that add complexity beyond the display component.

Post-2025 UNECE Visor-Display Safety Harmonization

The UNECE Regulation No. 22.06, effective January 2022, mandated testing of authorized accessories, including intercom systems and display devices, to ensure they do not degrade helmet performance during impact scenarios[1]"Proposal for Supplement 2 to the 06 series of amendments to UN Regulation No. 22 (Protective helmets)," Economic Commission for Europe, unece.org. This regulatory framework extends beyond traditional safety metrics, including rotational acceleration testing at -20°C and angled impacts at 45°, creating stringent certification requirements for HUD-equipped helmets. The regulation's global adoption accelerates through 2025 as countries align with European standards, creating market access barriers for non-compliant products. ECE 22.06 certification now requires testing helmet accessories as integrated systems rather than standalone components, fundamentally changing product development cycles. Manufacturers must demonstrate that HUD mounting systems, wiring harnesses, and battery modules maintain helmet integrity under standardized impact conditions, driving innovation in breakaway mounting systems and flexible electronics integration.

Rising Connected-Two-Wheeler Insurance Discounts

Insurance providers increasingly offer premium discounts for motorcycles equipped with connected safety devices, with Allianz Partners partnering with Cosmo Connected to embed telematics data collection in smart helmets[2]"Allianz Partners and Cosmo Connected have entered into a global strategic partnership," Allianz, allianz-partners.com. These programs typically provide 5% to 15% premium reductions for riders demonstrating safe behavior through helmet-mounted sensors and GPS tracking. The insurance industry's shift toward usage-based models creates direct financial incentives for HUD adoption, particularly among commercial delivery fleets and ride-sharing operators. However, privacy concerns regarding continuous location tracking and behavioral monitoring may limit adoption among recreational riders. Integrating crash detection algorithms and emergency response features positions smart helmets as risk mitigation tools rather than mere convenience accessories, aligning insurer interests with rider safety outcomes.

E-Commerce Bundling By EV-Scooter OEMs

Electric scooter manufacturers increasingly bundle smart helmets with vehicle purchases to create integrated mobility ecosystems. Ather Energy launched its Halo smart helmet series in July 2024, designed explicitly for scooter integration. This bundling strategy addresses regulatory requirements in markets like India, where helmet usage is mandatory, while creating differentiated value propositions for premium electric vehicles. The Ather Halo bit, priced at INR 12,999 (USD 147)[3]Sutanu Guha, " Ather HALO Smart Helmets Launched," ACKO Drive, ackodrive.com, demonstrates how OEMs subsidize smart helmet costs to drive ecosystem adoption and recurring revenue through connected services. Chinese manufacturers, including NIU and Gogoro, pursue similar strategies, leveraging helmet connectivity for vehicle diagnostics, theft protection, and rider behavior analytics. However, helmet replacement cycles of 3-5 years misalign with faster vehicle upgrade patterns, creating inventory management challenges for OEMs. The success of bundling strategies depends on seamless integration between helmet and vehicle systems, requiring standardized communication protocols that remain fragmented across manufacturers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Visor-Fog and Glare Defects | -2.4% | Global, particularly humid/cold climate regions | Short term (≤ 2 years) |

| Fragmented Battery-Pack Standards | -1.8% | Global, affecting interoperability | Medium term (2-4 years) |

| Consumer Privacy Push-Back on Eye-Tracking | -1.6% | Europe, North America (GDPR regions) | Long term (≥ 4 years) |

| Trade-War Optical-Component Tariffs | -1.3% | North America, affecting import costs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Visor-Fog And Glare Defects

Anti-fog coating technologies struggle with the thermal dynamics created by HUD displays, which generate localized heat that disrupts traditional moisture management systems. VISIODRY and InnoSense FogGo coatings demonstrate effectiveness in standard helmet applications but require reformulation for HUD integration scenarios. The optical interference between anti-fog treatments and HUD projection systems creates ghosting effects that degrade display clarity, particularly in bright sunlight conditions. Temperature differentials between the rider's face and ambient conditions exacerbate these issues in markets with extreme climate variations. Advanced solutions, including electrically heated visors and active ventilation systems, add cost and complexity while reducing battery life, creating trade-offs that limit mass market adoption.

Fragmented Battery-Pack Standards

The absence of standardized battery interfaces across innovative helmet manufacturers creates ecosystem fragmentation, inhibiting interoperability and increasing consumer replacement costs. Current implementations range from proprietary USB-C variants to custom magnetic charging systems, preventing cross-brand compatibility and creating vendor lock-in scenarios. Flexible lithium-polymer batteries suitable for helmet integration face 500-1500 mAh capacity constraints, limiting operational duration to 8-14 hours depending on HUD brightness and connectivity features. The International Electrotechnical Commission's TC 21 standards for secondary batteries do not address helmet-mounted power systems' unique form factors and safety requirements, leaving manufacturers to develop proprietary solutions. Battery placement within helmet structures must balance weight distribution, crash safety, and thermal management requirements while complying with impact protection standards. Energy harvesting technologies, including solar cells and kinetic generators, remain insufficient for continuous HUD operation, requiring hybrid approaches that increase system complexity and cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Display Technology: OLED Dominance Accelerates Innovation

OLED technology holds a 46.27% share of the HUD helmet market in 2024 and leads growth at 22.94% CAGR through 2030, driven by superior contrast ratios and power efficiency compared to alternative display technologies. The technology's ability to achieve black levels and wide viewing angles proves essential for outdoor visibility conditions where traditional LCDs struggle with sunlight readability. LCOS (Liquid Crystal on Silicon) maintains a specialized niche for high-resolution applications but faces cost disadvantages that limit adoption to premium segments. LCD technology persists in budget-oriented products but suffers from thickness and power consumption limitations that conflict with helmet weight distribution requirements. LED-based displays occupy a minimal market share due to resolution constraints and limited color reproduction capabilities.

Manufacturing advances in micro-OLED production, particularly Samsung's transition to glass substrates, reduce component costs significantly while improving brightness output for enhanced outdoor visibility. Integrating OLED displays requires specialized optical combiners and thermal management systems that add complexity but enable features like variable transparency and augmented reality overlays. Supply chain concentration in South Korea and Taiwan creates geographic risk factors that manufacturers address through diversification strategies and inventory buffers.

By Connectivity: Embedded Solutions Drive Integration

Embedded connectivity solutions dominated with 54.12% share of the HUD helmet market in 2024 and are witnessing growth at 24.36% CAGR through 2030, reflecting the industry's shift toward integrated rather than tethered architectures. This preference stems from rider safety concerns about cable management and the desire for seamless operation without smartphone dependency. Embedded systems incorporate cellular modems, GPS receivers, and Bluetooth radios within the helmet structure, enabling direct communication with emergency services and navigation platforms. The approach eliminates single points of failure associated with tethered connections while providing superior weather resistance and crash survivability.

Tethered solutions maintain relevance in cost-sensitive segments and retrofit applications where existing helmet investments require preservation. However, cable routing through helmet ventilation systems creates comfort and safety compromises that limit long-term viability. The transition toward embedded connectivity aligns with insurance industry requirements for tamper-resistant telematics data collection and emergency response automation. Battery life considerations favor embedded designs that optimize power management across integrated subsystems rather than supporting external charging requirements.

By Helmet Type: Modular Designs Reshape Traditional Categories

Full-face helmets hold a 62.71% share of the HUD helmet market in 2024 due to superior protection characteristics and optimal HUD integration space. Still, modular designs will surge at 27.48% CAGR through 2030 as urban mobility patterns prioritize versatility over maximum protection. The modular category's growth reflects changing rider demographics and use cases, particularly among delivery professionals and commuters who require frequent helmet removal for customer interaction. Modular helmets accommodate HUD systems through flip-up chin bars that provide access to display components for maintenance and adjustment without compromising the primary protection shell.

Open-face and half-shell designs face integration challenges due to limited mounting space and reduced structural support for HUD components. However, these categories benefit from aftermarket solutions like the Ather Halo bit, which attaches to existing helmets without modification. The ECE 22.06 regulation's emphasis on accessory compatibility testing favors modular designs that accommodate HUD systems while maintaining certification compliance across multiple configurations.

By Technology: AR HUD Transforms Riding Experience

Augmented-reality HUD technology held a 57.86% share of the HUD helmet market in 2024. It achieves the highest growth rate, at 29.62% CAGR through 2030, fundamentally transforming motorcycle navigation and safety systems beyond conventional display paradigms. AR integration enables real-time overlay of navigation instructions, hazard warnings, and vehicle telemetry onto the rider's field of view without requiring visual focus shifts that compromise road awareness.

Conventional HUD systems maintain relevance in cost-sensitive applications and retrofit scenarios but lack the contextual awareness capabilities that define next-generation riding assistance. The integration of AR technology requires advanced sensor fusion combining GPS, IMU, and camera inputs to achieve accurate overlay registration in dynamic riding conditions. Processing requirements for real-time AR rendering drive power consumption that challenges current battery technologies, creating trade-offs between functionality and operational duration that manufacturers address through selective feature activation and intelligent power management algorithms.

By User Type: Professional Adoption Drives Market Maturation

Professional users held 54.88% share of the HUD helmet market in 2024, reflecting early adoption by delivery services, law enforcement, and commercial transportation operators who justify HUD investments through operational efficiency gains and safety improvements. These users prioritize reliability, durability, and integration with fleet management systems over consumer-oriented features like entertainment and social connectivity. Professional adoption creates reference cases and validation that accelerate amateur segment growth at 18.47% CAGR through 2030 as technology costs decline and feature sets expand.

Amateur users increasingly embrace HUD technology for recreational riding and daily commuting applications, driven by smartphone integration capabilities and gamification features that enhance the riding experience. Social features, including rider-to-rider communication and group navigation coordination, emerge as key differentiators for amateur adoption, requiring mesh networking capabilities that extend beyond traditional Bluetooth limitations.

By Application: Performance Monitoring Emerges as Growth Leader

Navigation and route guidance applications dominated with a 37.19% share of the HUD helmet market in 2024, leveraging established GPS infrastructure and rider familiarity with smartphone-based navigation systems. However, performance monitoring achieves the highest growth rate at 25.68% CAGR through 2030 as riders increasingly demand real-time feedback on speed, lean angle, braking force, and engine parameters that enhance safety and riding skill development. This application category benefits from integration with motorcycle CAN bus systems and aftermarket sensor networks that provide comprehensive vehicle telemetry without requiring smartphone connectivity.

Safety alerts maintain steady adoption through integration with vehicle-to-vehicle (V2V) communication systems and infrastructure-based warning networks deployed in urban environments. Communication and media applications serve recreational users but face adoption barriers related to audio quality in high-noise environments and battery consumption from continuous streaming. The convergence of multiple applications within a single HUD system creates value propositions that justify premium pricing while addressing diverse user requirements across professional and amateur segments.

Geography Analysis

Europe maintains market leadership with a 32.34% share of the HUD helmet market in 2024, anchored by stringent ECE 22.06 regulations that mandate compatibility testing for helmet accessories and create barriers for non-compliant products. The region's regulatory framework drives innovation in integrated HUD systems that meet safety standards while enabling advanced functionality, with companies like Schuberth and SHOEI investing heavily in R&D to maintain competitive advantages. Germany leads adoption through automotive industry crossover technologies and premium motorcycle manufacturing, while France and Italy contribute through fashion-conscious design integration that appeals to style-oriented riders. The region's mature insurance markets increasingly offer premium discounts for connected safety devices, creating direct financial incentives for HUD adoption among professional and recreational users.

Asia-Pacific is the fastest-growing region, with a 19.84% CAGR through 2030, driven by electric scooter OEM bundling strategies and massive urban mobility transitions in China and India. Japan's technological leadership in display manufacturing and South Korea's OLED production capabilities provide regional supply chain advantages that reduce component costs and accelerate innovation cycles.

North America holds a significant market share through early adoption by law enforcement and military applications. However, trade tensions create cost pressures through tariffs on optical components from Mexico and Canada, forcing manufacturers to restructure supply chains and potentially relocate production. The region's insurance industry leadership in usage-based pricing models creates favorable conditions for connected helmet adoption. At the same time, urban Vision Zero initiatives in cities like Minneapolis provide public funding for smart PPE deployment that includes motorcycle safety technologies.

Competitive Landscape

The HUD helmet market exhibits moderate fragmentation with established helmet manufacturers competing against specialized technology companies through distinct strategic approaches that reflect different core competencies and market positioning. Traditional helmet manufacturers like BMW Motorrad, SHOEI, and Schuberth leverage brand recognition and safety certification expertise to integrate HUD technology into premium product lines, while technology specialists, including NUVIZ, DigiLens, and JARVISH, focus on innovation and feature differentiation to capture early adopter segments. The January 2024 GoPro acquisition of Forcite for an undisclosed amount signals strategic consolidation toward integrated camera-HUD ecosystems that combine action sports heritage with safety technology. This convergence creates white-space opportunities for companies that can bridge traditional safety engineering with consumer electronics capabilities, particularly in battery management, thermal design, and optical integration.

Competitive dynamics increasingly favor vertical integration as companies seek to control critical components and reduce dependency on fragmented supply chains affected by trade tensions and component shortages. Technology differentiation focuses on power management, with companies like Exeger partnering with Cosonic to develop solar-powered smart helmets that address battery life limitations through energy harvesting integration.

HUD Helmet Industry Leaders

-

DigiLens Inc.

-

NUVIZ Inc.

-

JARVISH Inc.

-

Shoei Co., Ltd

-

BMW of North America, LLC (BMW Motorcycle)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Exeger and Cosonic introduced solar-powered smart helmets for two-wheel riders in China. These helmets utilize Powerfoyle photovoltaic technology to provide continuous power for HUD systems, significantly reducing dependence on external charging infrastructure.

- February 2024: GoPro completed the acquisition of Forcite Helmet Systems, an Australian manufacturer of connected motorcycle helmets featuring HUD displays, chin-mounted cameras, and Bluetooth connectivity. The company plans to develop GoPro-branded helmet lines and partner with established manufacturers.

Global HUD Helmet Market Report Scope

| Organic Light Emitting Diode (OLED) |

| Liquid Crystal on Silicon (LCOS) |

| Liquid Crystal Display (LCD) |

| Light-Emitting Diode (LED) |

| Tethered |

| Embedded |

| Full Face |

| Open Face |

| Modular |

| Half Shell |

| Conventional HUD |

| Augmented-Reality HUD |

| Professional |

| Amateur |

| Navigation and Route Guidance |

| Safety Alerts |

| Performance Monitoring |

| Communication and Media |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Display Technology | Organic Light Emitting Diode (OLED) | |

| Liquid Crystal on Silicon (LCOS) | ||

| Liquid Crystal Display (LCD) | ||

| Light-Emitting Diode (LED) | ||

| By Connectivity | Tethered | |

| Embedded | ||

| By Helmet Type | Full Face | |

| Open Face | ||

| Modular | ||

| Half Shell | ||

| By Technology | Conventional HUD | |

| Augmented-Reality HUD | ||

| By User Type | Professional | |

| Amateur | ||

| By Application | Navigation and Route Guidance | |

| Safety Alerts | ||

| Performance Monitoring | ||

| Communication and Media | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the HUD helmet market in 2025?

The motorcycle helmet HUD market size is USD 1.01 billion in 2025 and will double to USD 2.03 billion by 2030.

What is the forecast CAGR for motorcycle helmet HUD products?

The compound annual growth rate is projected at 14.8% between 2025 and 2030.

Which display technology dominates motorcycle HUD helmets?

OLED leads with 46.27% market share in 2024 and grows faster than any rival technology.

Why are insurers interested in HUD-equipped helmets?

Connected helmets supply telematics that support 5–15% premium discounts, driving fleet and commuter adoption.

Which region is the fastest-growing for motorcycle HUD helmets?

Asia-Pacific is expanding at 19.84% CAGR, fueled by electric scooter OEM bundling strategies.

What technical issue most limits adoption today?

Persistent visor-fog and glare defects remain the top restraint, cutting visibility and raising warranty costs.

Page last updated on: