Japan Connected Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

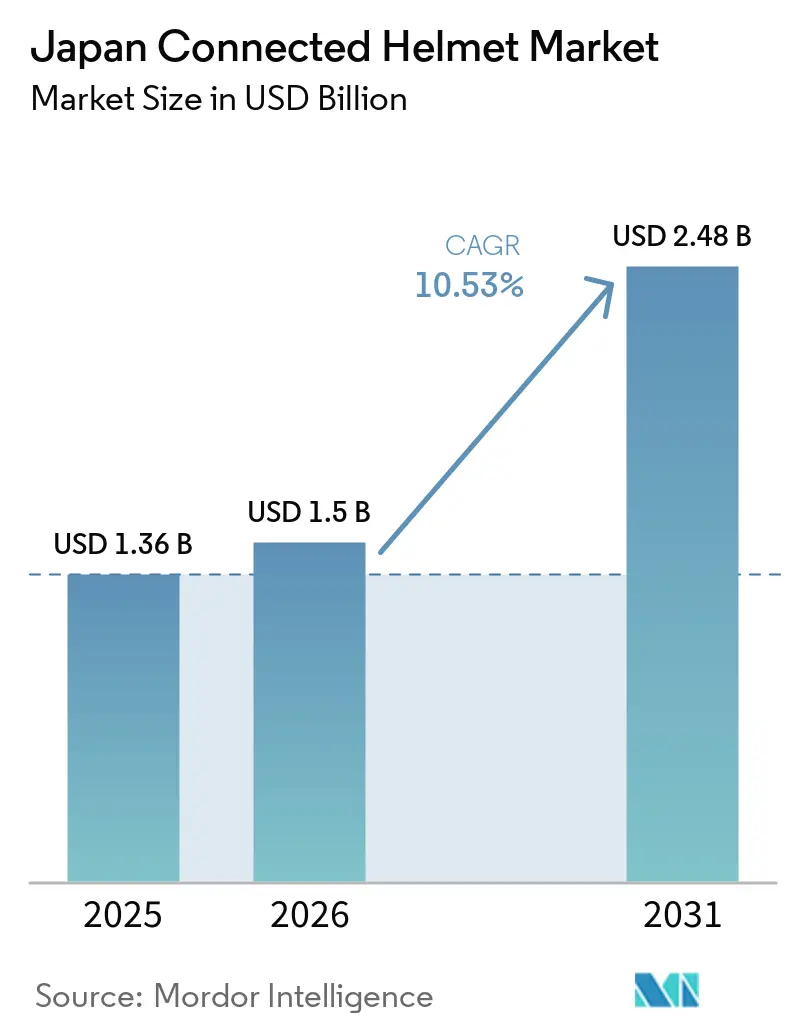

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 10.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Connected Helmet Market Analysis by Mordor Intelligence

The Japan-connected helmet market size is expected to increase from USD 1.36 billion in 2025 to USD 1.50 billion in 2026 and reach USD 2.48 billion by 2031, growing at a CAGR of 10.53% over 2026-2031. Three pivotal forces are reshaping the demand landscape: government-supported V2X infrastructure emerging on expressways, a growing cohort of tech-savvy riders emphasizing safety, and OEM subscription bundles that tie connected helmets to profitable after-sales revenues. Although full-face designs dominate sales, smart HUD-integrated variants are swiftly catching up, driven by plummeting microdisplay prices and the standardization of crash-detection modules. Offline retail accounts for a significant share of revenue, driven by Japanese riders' preference for professional fittings. However, direct-to-consumer platforms are witnessing substantial growth, fueled by tech-savvy consumers embracing virtual sizing tools. Geographically, Kanto leads, benefiting from Tokyo's early V2X roll-out, while Chubu, capitalizing on Nagoya's automotive corridor for OEM pilots, boasts the fastest growth.

Key Report Takeaways

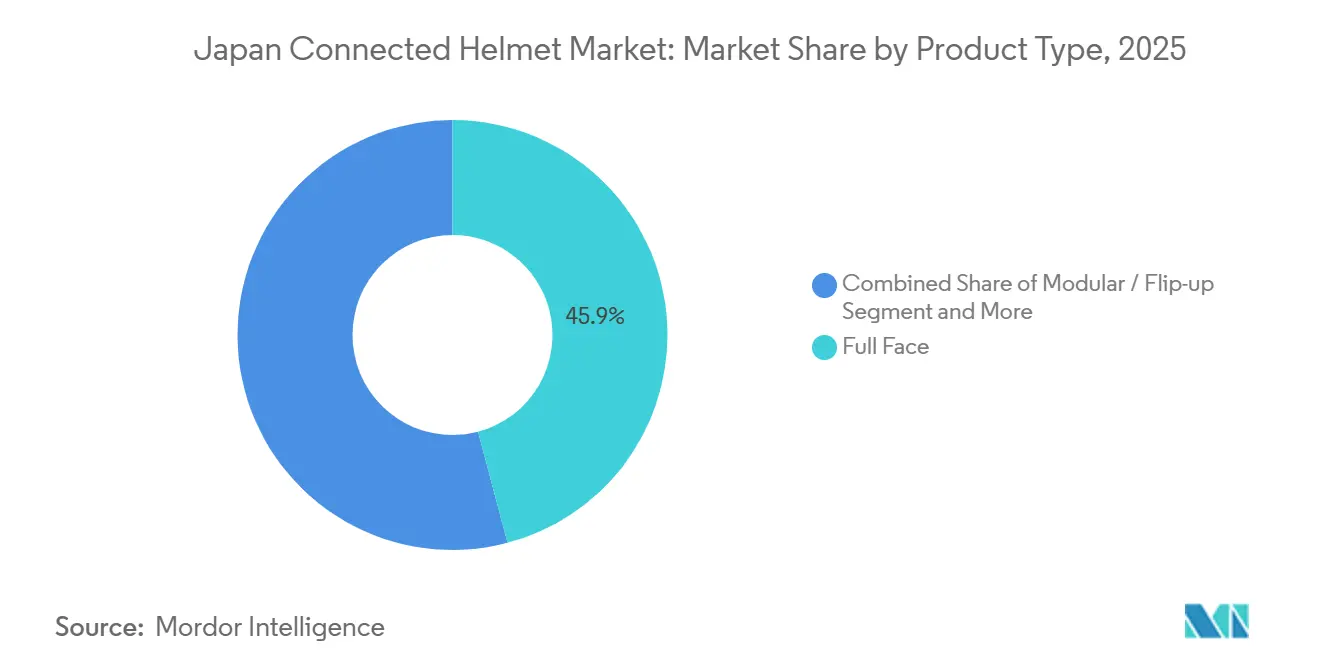

- By product type, full-face helmets led with a 45.88% revenue share in 2025, while smart HUD-integrated variants are projected to record the fastest 12.49% CAGR through 2031.

- By connectivity tier, integrated audio/communications accounted for 41.22% of the Japan connected helmet market share in 2025, whereas ADAS sensor-suite configurations are forecast to grow at 13.22% CAGR through 2031.

- By end user, individual riders accounted for 66.67% of the market in 2025, whereas the fleet and delivery segment is anticipated to grow at a 12.39% CAGR during the forecast period.

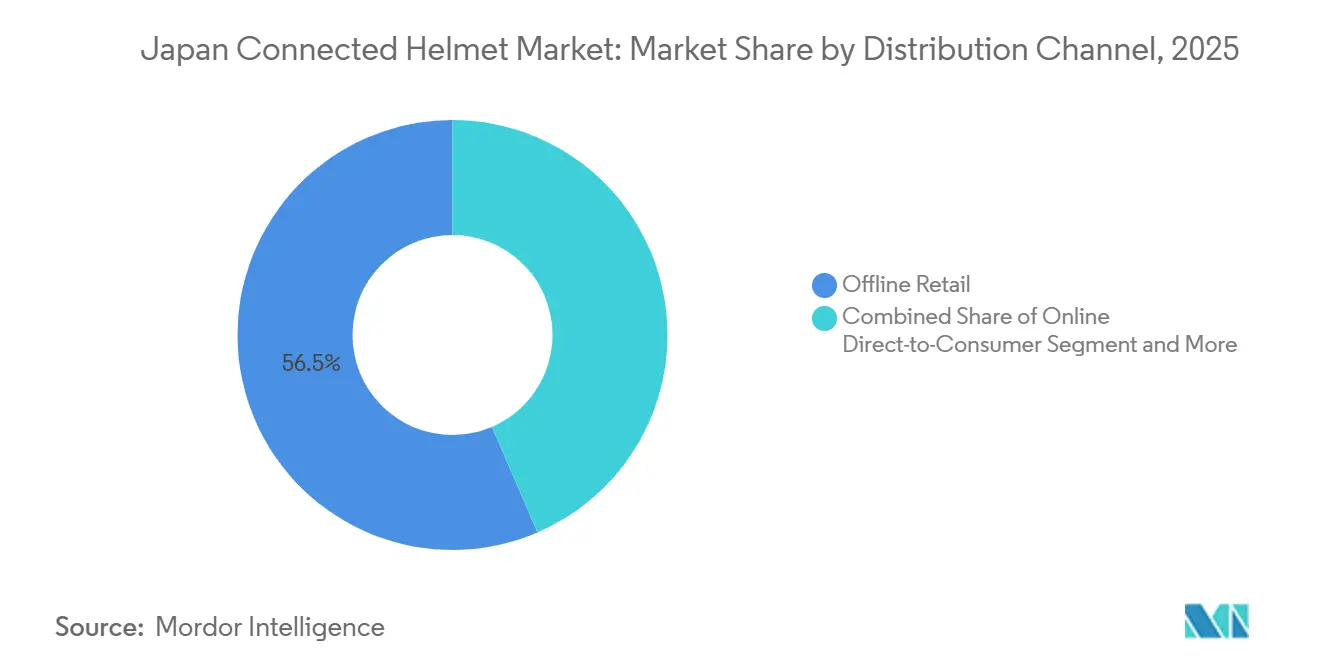

- By distribution channel, offline retail captured 56.46% revenue in 2025, while online direct-to-consumer sales are on track for a 15.01% CAGR over the same period.

- By price range, mid-range helmets held 46.88% share in 2025, and premium models are priced and expanding at 13.72% CAGR toward 2031.

- By geography, Kanto accounted for 35.91% of 2025 revenue, and Chubu is expected to post the fastest 11.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Japan includes both locally based firms and those operating across multiple regions. The market landscape in the global connected helmet industry research shows how these players are arranged internationally.

Japan Connected Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G/4G LTE-V2X Roll-out | +2.8% | Kanto, Kansai, Chubu | Medium term (2-4 years) |

| "Smart-helmet as a Service" | +2.1% | Kanto, Kansai | Short term (≤ 2 years) |

| Premium Touring and Adventure Bike Sales | +1.9% | Kanto, Chubu, Kyushu | Medium term (2-4 years) |

| Standards for In-helmet Electronics | +1.7% | All Prefectures | Short term (≤ 2 years) |

| Insurance Discounts for IoT-verified Helmets | +1.2% | Kanto, Kansai | Medium term (2-4 years) |

| Group-riding Social Networks | +0.8% | Kanto, Kansai, Chubu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Roll-out of 5G/4G LTE-V2X Along Japan’s Expressways

The Ministry of Internal Affairs and Communications initiated the installation of roadside units on the Shin-Tomei Expressway. This advancement enables helmets to receive real-time hazard warnings without connecting to a smartphone. With plans to expand to the Tomei, Meishin, and Chugoku corridors, manufacturers will establish a nationwide H2I backbone. This shift is steering competition towards V2X-native chipsets. Delivery fleets stand to gain significantly by receiving lane-closure alerts earlier than GPS navigation, thereby reducing the risk of rear-end collisions. However, a disparity remains: secondary roads, still dependent on a 4G fallback, experience added latency. Consequently, a two-tier market has emerged: metropolitan riders are leaning towards V2X-ready helmets, while their rural counterparts prefer Bluetooth-only models.

OEM-Backed “Smart-helmet-as-a-Service” Bundles

Shoei unveiled the GT-Air 3 Smart, featuring an OLED heads-up display, available for financing alongside motorcycle loans [1]“GT-Air 3 Smart Launch,”, Shoei Co. Ltd., shoei.com. By shifting from one-time sales to recurring fee bundles, OEMs gain valuable telemetry insights for product design. However, this strategy poses a risk of channel conflict with aftermarket dealers. While older riders lean towards outright ownership, commuters are gravitating towards pay-per-feature tiers, significantly reducing their upfront costs. Early adopters are predominantly found in Kanto and Kansai, regions where dealerships are equipped to manage fittings and firmware updates. Conversely, in rural prefectures, limited dealer networks hinder subscription adoption, presenting a potential avenue for virtual onboarding and mail-in fitting services.

Rise in Premium Touring and Adventure Bike Sales Among 40-plus Riders

Even as overall motorcycle sales softened, registrations of higher-capacity bikes rose, highlighting a trend of discretionary spending among riders in the older age group. These discerning buyers prioritize features like quiet linings, long-lasting batteries, and modular visors. This demand has enabled premium helmets, often priced higher, to capture a larger market share. In response, brands like Shoei and Arai have integrated advanced features such as speaker cavities and infrared-cut shields. Meanwhile, OGK Kabuto’s KAMUI-5 has introduced a flip-up convenience, catering to touring routes in Hokkaido’s national parks. Given that touring riders spend extended hours on expressways, helmets equipped with swappable batteries and weatherproof USB-C ports have become more popular than standard commuter models. To effectively reach this demographic, brands have set up pop-up showrooms at summer rallies, compensating for Hokkaido's sparse retail landscape.

Mandatory Use of PSC/SG Standards for In-helmet Electronics from 2026

Japan has mandated that embedded electronics, including battery packs, HUD modules, and radios, must pass stringent impact tests to ensure they don't compromise shell integrity. This move, extending PSC and SG marks, effectively sidelines low-cost imports that previously retrofitted untested electronics. As a result, the market is increasingly dominated by firms boasting in-house crash labs. While start-ups grapple with significant test fees per model, established players can spread these costs over larger volumes. Fleet operators now insist on PSC/SG helmets for insurance coverage, and Uber Eats has begun rejecting riders if their selfie-verification app fails to recognize the SG logo on their headgear. This short-term supply contraction has not only boosted average selling prices but also accelerated the industry's pivot towards premium certified units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Li-ion Battery Packs Cost | -1.8% | Coastal Prefectures (Kanagawa, Chiba, Shizuoka) | Medium term (2-4 years) |

| RF Spectrum Congestion | -1.4% | Tokyo Metropolitan Area | Short term (≤ 2 years) |

| Fragmented Prefectural Privacy Rules | -1.1% | All Prefectures | Long term (≥ 4 years) |

| Limited Consumer Awareness | -0.9% | Rural Prefectures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Replacement Cost of Li-ion Battery Packs in Humid Coastal Regions

In Pacific prefectures, the salty air corrodes charging contacts, significantly reducing battery life. With replacement modules costing more, the total cost of ownership exceeds that of non-connected helmets. While manufacturers haven't introduced swap programs, coastal riders are either delaying upgrades or opting for Bluetooth-only shells with user-replaceable modules. Concerns over safety prevent consumers from using third-party batteries without PSC marks, effectively tying them to expensive OEM parts. This financial burden is hindering the adoption of premium helmets in Okinawa and Shizuoka, even though riding conditions are quite inviting.

RF Spectrum Congestion for Bluetooth 5.x in Dense Tokyo Corridors

Wi-Fi and IoT devices have saturated the GHz band. As a result, along Shibuya’s main roads, the intercom range shrinks significantly during peak hours. While dual-band radios can address this dropout issue, they increase the bill of materials. Meanwhile, some delivery fleets are opting for LTE-based VoIP headsets. These headsets offer a latency trade-off for the near-instant audio. Riders, however, find this latency acceptable only at urban speeds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Full-Face Dominance Drives Smart Integration

Full face designs held 45.88% of the Japanese connected helmet market share in 2025 because Shoei and Arai dominate premium safety certification. Smart HUD-integrated models, led by Shoei’s GT-Air 3 Smart, are forecast at a 12.49% CAGR, reflecting falling micro-display prices and PSC-compliant battery packs.

Modular and flip-up shells attract touring riders who prioritize easy donning, while open-face and half helmets stay below 15% because limited surface area constrains electronics placement. Off-road helmets add action-camera mounts but struggle to fit six-hour batteries without exceeding weight targets. The segment’s inflection lies in retrofit kits: CrossHelmet’s X1-NKD ships without electronics and lets buyers snap in HUD and sensor pods later, shifting revenue toward upgrade accessories.

By Connectivity and Feature Level: ADAS Sensors Accelerate Safety Evolution

Integrated audio/comms accounted for 41.22% of the Japan-connected helmet market in 2025, yet ADAS sensor-suite models grew at a 13.22% CAGR as delivery fleets chase telematics-verified safety bonuses. Uber Eats mandates SG-marked helmets with visual verification, steering couriers toward radar-equipped shells that trigger app unlock only when worn.

HUD/AR helmets remain premium at USD 1,100-1,800, and all-in-one units face reliability issues due to short battery life. Crash-detection and eCall capabilities gain policy support, with Japan’s transport ministry studying mandatory eCall by 2028. Manufacturers, therefore, release mid-priced helmets that pair basic Bluetooth intercom with accelerometer-based crash alerts to balance cost and compliance.

By End User: Fleet Adoption Accelerates Commercial Integration

Individual riders commanded 66.67% share in 2025, but fleet and delivery services expanded at 12.39% CAGR on the back of insurance discounts and compliance dashboards. Riders in full-time delivery require helmets rated for daily six-hour use and all-weather charging ports, driving distinct SKUs that omit HUD but add GPS tracking.

Passenger helmets remain marginal because tandem riding is uncommon, reducing the incentive to add rear-camera feeds. Age demographics reinforce the split: older touring riders pay for quiet linings and long-life batteries, whereas younger couriers accept lighter Bluetooth-only lids to keep initial costs down.

By Distribution Channel: Online Growth Challenges Traditional Retail

In 2025, offline retail held a dominant 56.46% market share, driven by Japanese consumers' preference for professional sizing. Meanwhile, online direct-to-consumer sales surged at a 15.01% CAGR, buoyed by incentives like free size-exchange programs and the option for installment payments.

OEM accessory bundles create a hybrid path; premium bike buyers roll a JPY 150,000 (approximately USD 982) helmet into vehicle loans at dealerships. Virtual head-scans and augmented-reality try-ons lower return rates but remain less precise than in-store fitting, keeping brick-and-mortar relevant in rural prefectures where broadband is slower.

By Price Range: Premium Segment Drives Innovation Investment

Mid-range helmets captured 46.88% revenue, anchoring mainstream penetration, whereas premium SKUs are expected to grow 13.72% annually by offering carbon-fiber shells, AR-optics, and AI noise cancellation. Manufacturers funnel premium margins back into fundamental research on micro-LED projection, solid-state batteries, and biometric sensing. Consequently, features once exclusive to USD 1,000-plus helmets migrate downward each model year, progressively democratizing advanced safety.

Economy units remain vital for price-conscious commuters but typically employ removable accessory brackets rather than factory-embedded electronics, carving out a low-cost entry ramp into the Japan-connected helmet market. Economy helmets prioritize basic safety compliance, mid-range products introduce essential smart features, and Premium offerings lead with innovative advancements. This pricing hierarchy enables manufacturers to cater to varied customer demands, all while ensuring robust margins on their advanced products, bolstering brand differentiation and market positioning.

Geography Analysis

Kanto generated 35.91% of 2025 revenue, buoyed by Tokyo’s early V2X deployment and dense dealership network. While Kansai is the second-largest region, it shows a cultural reluctance: Osaka's adoption of bicycle helmets lags behind Tokyo's. This sentiment extends to connected gear as well.

Chubu, bolstered by Nagoya's robust automotive supply chain and the Japan Alps' scenic touring routes favoring long-range mesh intercoms, is set to lead regional growth with an impressive 11.57% CAGR through 2031. Meanwhile, in Kyushu and Okinawa, rising humidity escalates battery-replacement costs, though these regions collectively represent only a minor segment of the market.

Due to limited V2X coverage and a lack of awareness of retail curtailment, Hokkaido, Tohoku, Chugoku, and Shikoku collectively account for a minor share. To address this, brands are turning to mobile demo trucks and promoting online sales with free returns. However, these efforts have yet to close the adoption gap behind Kanto. Additionally, the fragmented nature of prefectural privacy complicates national roll-outs. For instance, firmware adjustments are necessary to switch data-logging features as riders move between lenient and strict jurisdictions, thereby increasing maintenance costs.

Mordor Intelligence tracks the connected helmet market across other major regions such as Europe, with additional country-level coverage spanning South Korea, China, United States, and India, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Market concentration remains moderate. Together, Shoei and Arai command a significant share of the global premium segment, using that trust to introduce connected variants without compromising core safety standards. OGK Kabuto carves out a niche by partnering with Uber Eats, ensuring that only SG-marked helmets are accepted for orders.

CrossHelmet stands out with its HUD model, certified by both SG and DOT, priced at a premium. However, its reliance on crowdfunding for capital restricts its production scale [2]“PSC/SG Certification Announcement,”, CrossHelmet Inc., Crosshelmet.com. Meanwhile, LIVALL has introduced an AI Visual Smart Helmet that uses automotive radar and prices it significantly lower than competitors, all while adhering to compliance standards. This move hints at a broader cost deflation trend linked to car supply chains.

Local players, especially Japanese firms, are leading the patent race, with a keen focus on optics and battery thermal control. Moreover, strategic collaborations are bolstering their positions: Shoei has partnered with EyeLights for micro-displays, and Yamaha has partnered with Gachaco for swappable battery kiosks, thereby fortifying their production expertise and after-sales services.

Japan Connected Helmet Industry Leaders

Shoei Co., Ltd.

Arai Helmet Ltd.

Sena Technologies Inc.

OGK Kabuto Co., Ltd.

HJC Helmets

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sena released the Phantom full-face helmet with integrated AI noise reduction, 5-mode rear brake light, and pre-installed cloud-sync firmware.

- January 2025: OGK Kabuto introduced the Ryuki System helmet featuring an aerodynamic “wake stabilizer” and dual-band mesh intercom.

Japan Connected Helmet Market Report Scope

The Japan connected helmet market report is segmented by product type (full face, modular/flip-up, open face, half helmet, off-road/ motocross), connectivity and feature level (bluetooth-only, integrated audio/comms, and HUD/AR display, crash detection and ecall, ADAS sensor suite, and multi feature), end user (individual rider, passenger, and fleet/delivery), distribution channel (offline retail, online direct-to-consumer, and OEM Accessory Bundles), and price range (economy, mid-range, and premium) and by region (Kanto, Kansai, Chubu, Kyushu and Okinawa, Hokkaido and Tohoku, Chugoku, and Shikoku). The market forecasts are provided in terms of value (USD) and volume in units.

| Full Face |

| Modular / Flip-up |

| Open Face |

| Half Helmet |

| Off-road / Motocross |

| Smart HUD-Integrated |

| Bluetooth-Only |

| Integrated Audio / Comms |

| HUD / AR Display |

| Crash Detection and eCall |

| ADAS Sensor Suite |

| Multi-Feature (All-in-One) |

| Individual Rider |

| Passenger |

| Fleet / Delivery |

| Offline Retail |

| Online Direct-to-Consumer |

| OEM Accessory Bundles |

| Economy |

| Mid-Range |

| Premium |

| Kanto |

| Kansai |

| Chubu |

| Kyushu and Okinawa |

| Hokkaido and Tohoku |

| Chugoku |

| Shikoku |

| By Product Type | Full Face |

| Modular / Flip-up | |

| Open Face | |

| Half Helmet | |

| Off-road / Motocross | |

| Smart HUD-Integrated | |

| By Connectivity and Feature Level | Bluetooth-Only |

| Integrated Audio / Comms | |

| HUD / AR Display | |

| Crash Detection and eCall | |

| ADAS Sensor Suite | |

| Multi-Feature (All-in-One) | |

| By End User | Individual Rider |

| Passenger | |

| Fleet / Delivery | |

| By Distribution Channel | Offline Retail |

| Online Direct-to-Consumer | |

| OEM Accessory Bundles | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Region | Kanto |

| Kansai | |

| Chubu | |

| Kyushu and Okinawa | |

| Hokkaido and Tohoku | |

| Chugoku | |

| Shikoku |

Key Questions Answered in the Report

How large will the Japan connected helmet market be by 2031?

It is projected to reach USD 2.48 billion by 2031, expanding at a 10.53% CAGR from 2026 to 2031.

Which product type holds the biggest share today?

Full face helmets lead with 45.88% of 2025 revenue because they dominate premium safety certification.

What is the fastest-growing connectivity tier?

ADAS sensor-suite helmets are forecast at a 13.22% CAGR as delivery fleets adopt telematics-verified safety equipment.

Why does Kanto dominate regional sales?

Tokyo’s early V2X infrastructure, dense motorcycle dealer network and safety-focused consumer culture give Kanto 35.91% of 2025 revenue.

What regulatory change will most influence adoption by 2026?

PSC/SG certification for in-helmet electronics becomes mandatory in 2026, raising product-quality standards and encouraging premium purchases.

Page last updated on: