Connected Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

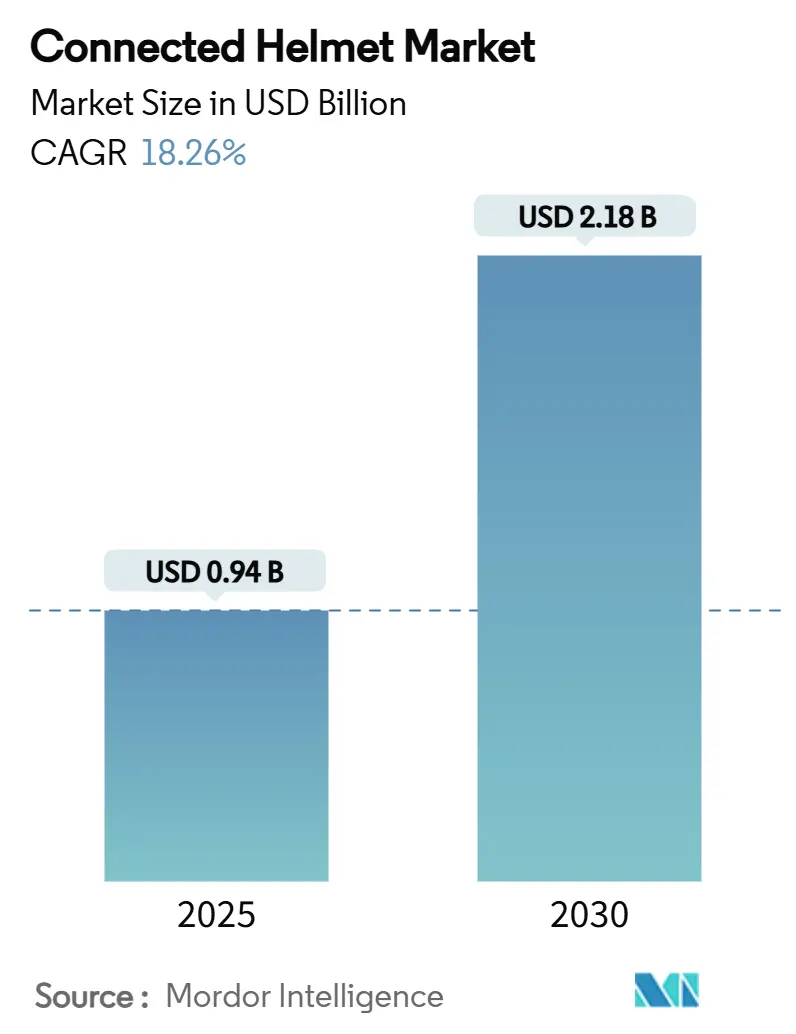

| Market Size (2025) | USD 0.94 Billion |

| Market Size (2030) | USD 2.18 Billion |

| Growth Rate (2025 - 2030) | 18.26% CAGR |

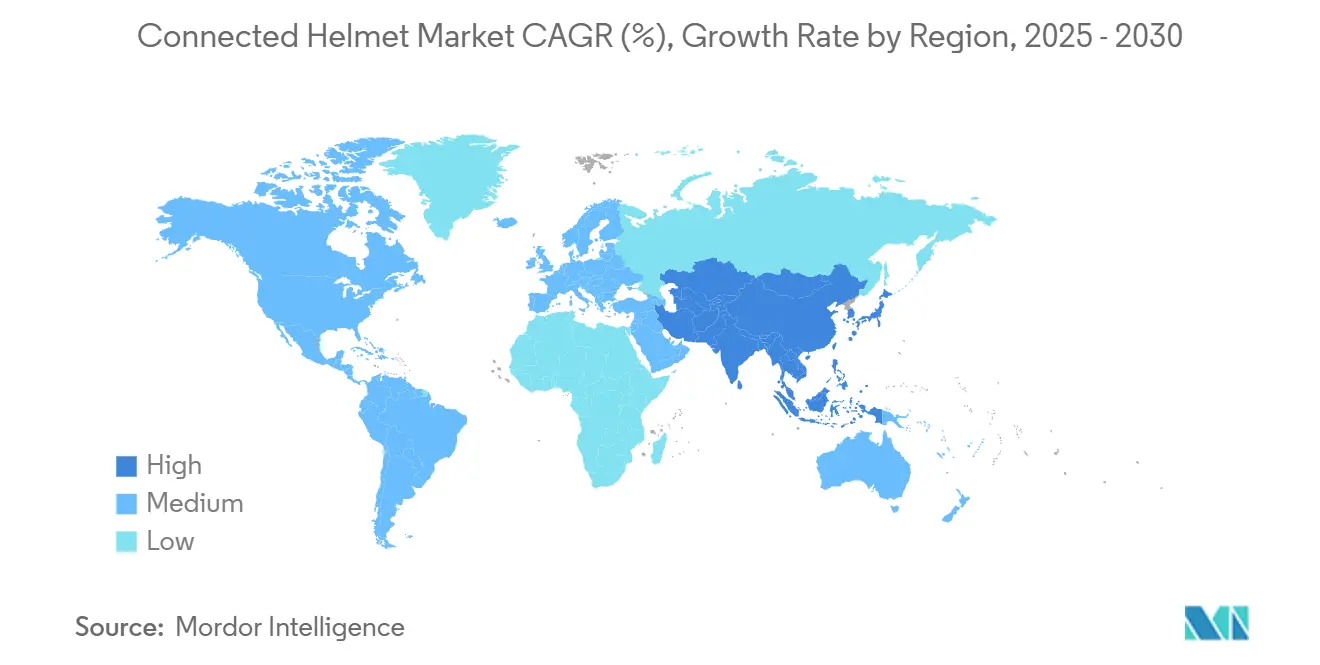

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

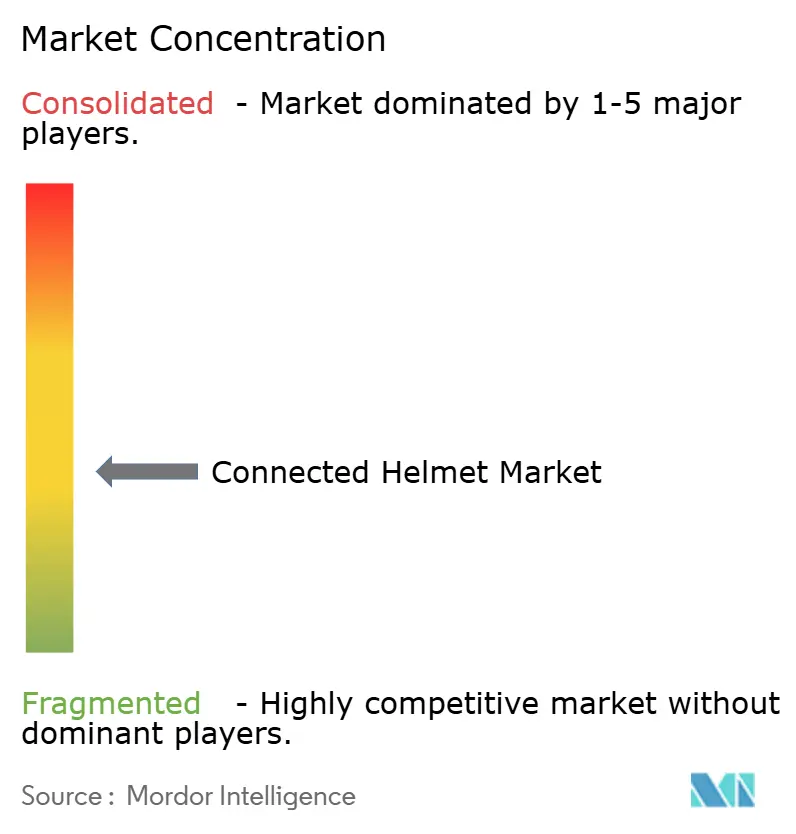

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Helmet Market Analysis by Mordor Intelligence

The connected helmet market size stands at USD 0.94 billion in 2025 and is forecast to expand to USD 2.18 billion by 2030, translating into an 18.26% CAGR. Asia-Pacific leads today, propelled by motorcycle-centric urban mobility, rapid 5G rollouts, and government safety mandates that collectively create outsized demand for smart protective gear. Regulatory bodies in Europe and North America amplify momentum through e-call requirements and labeling updates, while premium consumer preferences in these regions underpin healthy replacement cycles. Partnerships between incumbent helmet brands and technology firms accelerate feature integration, whereas start-ups laud fast product iterations and direct-to-consumer models to capture early adopters. Heightened interest from insurers, delivery platforms, and ride-sharing operators further broadens the use-case spectrum, positioning the connected helmet market for sustained double-digit expansion.

Key Report Takeaways

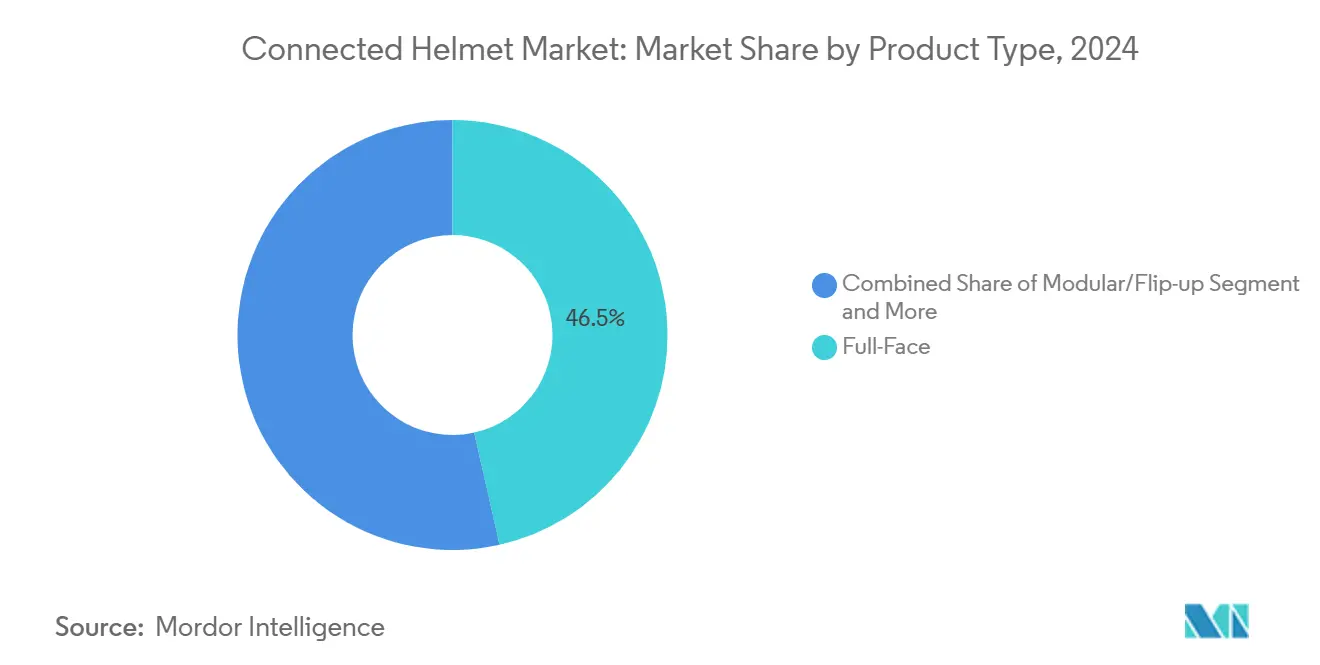

- By product type, full-face models commanded 46.51% of 2024 revenue, while HUD-integrated/AR helmets are advancing at a 19.12% CAGR through 2030.

- By end-user, individual riders contributed 69.33% of 2024 demand, whereas commercial fleet and delivery users are accelerating at an 18.78% CAGR to 2030.

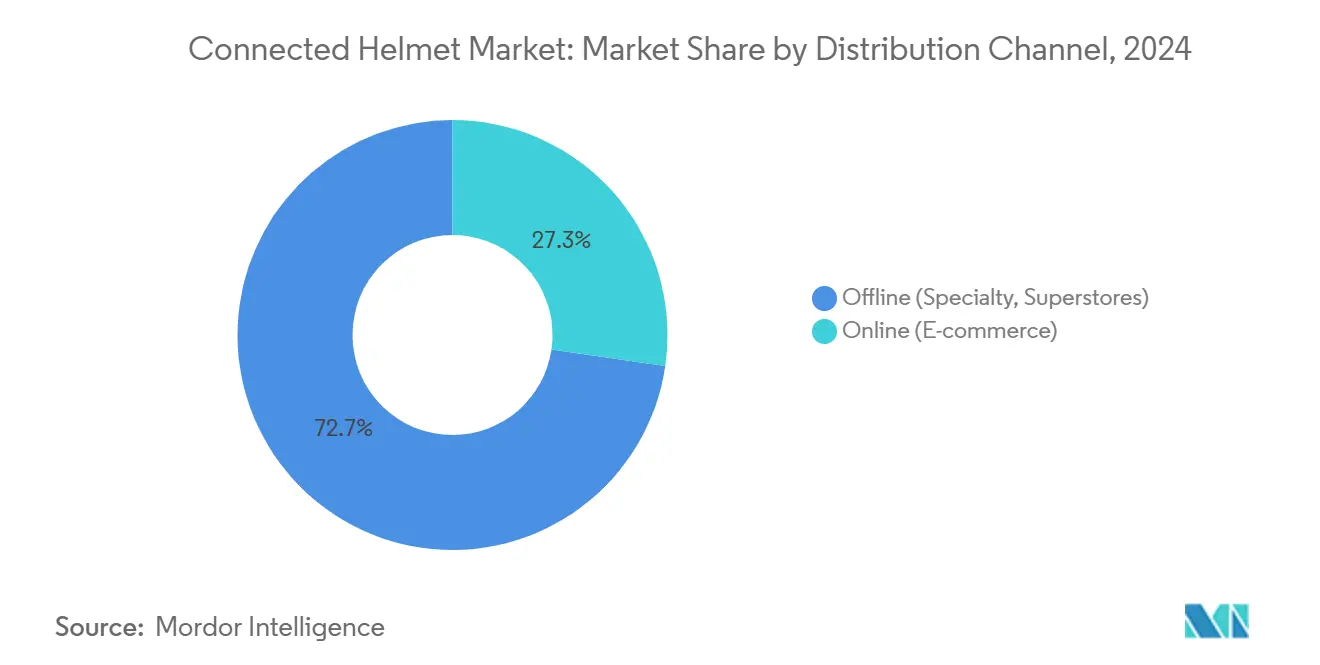

- By distribution channel, offline retail retained 72.65% of 2024 sales; online channels are growing fastest at a 20.13% CAGR to 2030.

- By connectivity technology, Bluetooth-only solutions held 55.41% of 2024 revenue, and 5G plus C-V2X platforms are set to grow at a 26.15% CAGR through 2030.

- Asia-Pacific represented 47.26% of 2024 revenue and is forecast to post a 19.65% CAGR to 2030.

Global Connected Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Rollout Enabling Low-Latency V2X | +3.5% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Mandatory E-Call & Crash Alerts | +3.2% | Europe, North America, and expanding to APAC | Medium term (2-4 years) |

| AR-HUD Navigation Integration | +2.9% | North America, Europe, premium APAC markets | Long term (≥ 4 years) |

| Motorcycle ADAS Adoption Growth | +2.8% | Global, early uptake in developed markets | Long term (≥ 4 years) |

| Fleet Safety Programmes for Ride-Sharing & Delivery | +2.1% | Global urban centers, chiefly APAC and North America | Short term (≤ 2 years) |

| Telematics-Based Insurance Discounts | +1.8% | Europe, North America, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Rollout Enabling Low-latency V2X

Telstra’s 5G helmet prototype streams hazard data straight from roadside units, demonstrating sub-10 millisecond latency suitable for crash-avoidance scenarios [1]Telstra Corporation, “Telstra Builds 5G Bike Helmet Prototype,” telstra.com.au. Academic work on 6G envisions reflective metasurfaces that boost signal quality for moving riders, extending safety envelopes even in dense urban canyons.

Mandatory E-call and Crash-notification Mandates

European Union rules now require motorcycles to support automatic emergency calling, prompting helmet makers to embed e-call-ready electronics that relay crash data to first responders within seconds. The National Highway Traffic Safety Administration has mirrored labeling changes to accommodate such electronics in the United States, impacting 3.6 million helmets per year. As 43 nations align under UN Regulation No. 22, compliant connected helmets gain uniform access to global markets[2]United Nations Economic Commission for Europe, “UN Regulation No. 22—Protective Helmets,” unece.org.

Integration of AR-HUDs for Real-time Navigation

TILSBERK’s swappable HUD module adds 12-hour battery life and four display modes, proving the everyday viability of augmented overlays. MOTOEYE’s rear-camera-assisted system widens riders’ field of view to 240 degrees, virtually eliminating blind spots and setting new benchmarks for situational awareness. Premium hobbies thus catalyze trickle-down innovation for mass-market models.

Growing Adoption of Motorcycle ADAS Platforms

The Connected Motorcycle Consortium confirms that riders often overlook dashboard alerts, making helmet-level warnings essential. Automakers testing V2M systems report blind-spot collision risk reductions after integrating Qualcomm-powered C-V2X chips into prototype bikes. When helmets display these alerts in riders’ line of sight, ADAS effectiveness multiplies, reinforcing demand for integrated solutions.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost vs. Standard Helmets | -2.8% | Global, notably price-sensitive APAC | Short term (≤ 2 years) |

| Short Battery Life & Thermal Issues | -2.1% | Global, especially hot-climate regions | Medium term (2-4 years) |

| No Interoperability Standards | -1.9% | Global, fragmented across regions | Long term (≥ 4 years) |

| Privacy & Cybersecurity Risks | -1.6% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High ASP versus Conventional Helmets

Smart helmets can cost three to five times more than basic certified models. Sena’s USD 599 premium Impulse unit illustrates the affordability gap for riders in emerging economies [3]Sena Technologies, “Impulse Modular Smart Helmet,” sena.com. United Nations research finds cost is the primary barrier to quality helmet uptake, suggesting connected variants will diffuse gradually in low-income regions.

Limited Battery Life and Thermal Management

Feher’s thermoelectric-cooled helmet keeps interior temperatures up to 18 degrees cooler yet adds weight and needs external power, underscoring design compromises. Field tests show most smart helmets require recharging after four to six hours; extended battery packs alleviate range anxiety but add bulk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Full-Face Dominance Meets AR Innovation

Full-face designs generated 46.51% of 2024 revenue because their rigid shells safely house microphones, cameras, and antenna arrays without compromising impact performance, giving them the largest connected helmet market share. Growth now pivots to HUD-integrated and AR variants that promise hands-free navigation and enhanced situational awareness, sprinting ahead at a 19.12% CAGR as early adopters absorb premium pricing. Manufacturers combine carbon-fiber shells with miniaturized optics to maintain weight parity with standard lids, easing adoption among commuter and touring segments. Start-ups employ direct-to-consumer channels to bypass retail mark-ups, nudging average selling prices lower while still preserving margins through software add-ons. Over the forecast period, modular and flip-up hybrids are expected to bridge the gap between traditional touring comfort and HUD functionality, offering a mid-tier price point that opens the connected helmet market to value-conscious buyers.

Second-generation AR systems introduce multi-color waveguides that project speed, navigation, and ADAS warnings directly onto riders’ lines of sight, cutting eye-off-road time. Vendors stress swappable battery modules and OTA firmware updates to extend product lifecycles, aligning with sustainability mandates in Europe and parts of Asia. Off-road and adventure sub-segments benefit from satellite tracking and emergency beacons that operate beyond cellular footprints, making connected helmet market size gains even in sparsely populated geographies. Patent filings around cooling fabrics and lightweight antennas indicate a pipeline of incremental upgrades that can be layered onto existing shell molds, encouraging OEMs to iterate rapidly. These dynamics preserve full-face dominance yet carve out meaningful opportunity for HUD-centric disruptors.

By End-User: Individual Riders Drive Volume, Fleets Accelerate Growth

Individual owners accounted for 69.33% of 2024-unit shipments, underpinning the bulk of the connected helmet market revenue. They value Bluetooth calls, music streaming, and crash alerts that integrate seamlessly with smartphones. Social media communities amplify word-of-mouth adoption as riders post ride telemetry dashboards and AR viewpoints, nudging peers toward similar upgrades. Meanwhile, commercial fleets—food delivery, courier, and ride-hail operators—are scaling rapidly at an 18.78% CAGR by bundling helmets into onboarding kits. Corporations leverage real-time dashboards to monitor rider speed violations and rest breaks, meeting occupational-health compliance and reducing insurance premiums. Certain city regulators now require proof of compliant headgear for platform licensing, further tilting demand toward connected models.

Passengers represent an emerging niche as brands release smaller shell sizes with synchronized intercom pairing. Safety-minded parents purchase these for teenage pillion riders, an underserved demographic with high accident exposure. For enterprise buyers, cloud APIs stream anonymized telemetry into dispatch systems for live route optimization. Subscription-based analytics unlock recurring revenue that cushions hardware margin erosion as commoditization looms. Combined, these end-user patterns diversify the connected helmet industry and insulate it against single-segment demand shocks.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Brick-and-mortar specialists and big-box outlets retained a 72.65% share in 2024 because consumers still prioritize physical fit checks before purchase. Certified staff explain ECE 22.06 or DOT compliance and demonstrate firmware updates in-store, promoting trust among first-time buyers. Yet online channels are registering the strongest momentum with a 20.13% CAGR, supported by 360-degree sizing apps and hassle-free return logistics. Manufacturers benefit from direct consumer feedback loops that accelerate product refinement while eliminating distributor margins, allowing competitive pricing without eroding profitability. Live-stream shopping events in China and Southeast Asia showcase connected helmet features to millions simultaneously, condensing the awareness-to-purchase cycle.

Digital platforms bundle accessory upsells—action cameras, PTT buttons, and spare visors—lifting average order value. Secure payment gateways and localized warehousing curb delivery times to under 48 hours in key metros. As mixed-reality try-on experiences mature, virtual storefronts will further erode offline dominance, especially for tech-centric consumer segments that are comfortable purchasing safety equipment online. Nonetheless, servicing and firmware upgrades still draw foot traffic to physical outlets, preserving a hybrid sales model.

By Connectivity Technology: Bluetooth Leads, 5G Transforms Future

Bluetooth-only architectures captured 55.41% revenue in 2024 as they sufficiently handle voice, music, and short-range intercom. Bluetooth 5.0’s low-energy profile also eases battery pressure, a critical pain point in hot climates. Cellular-enabled variants add e-SIM modules for always-on crash alerts but incur data fees that dampen adoption in cost-sensitive regions. The 5G and C-V2X cohort, however, commands the fastest runway at a 26.15% CAGR because ultra-low latency supports safety-critical V2X alerts and cloud-AI hazard prediction. Early pilot corridors in South Korea, Japan, and parts of Western Europe showcase over-the-air firmware patches that continuously improve detection algorithms without hardware swaps, future-proofing investments.

Standards groups are converging on hybrid stacks that fuse Bluetooth for rider-to-rider chat with C-V2X for infrastructure messages, reducing module duplication and power drain. Ultra-wideband chips in development promise centimeter-level positioning that can warn riders of dooring hazards in dense traffic. Such innovations widen the connected helmet market size as legacy Bluetooth owners upgrade to multi-band models. The long-term outlook features cloud-native helmets that offload compute-intensive vision processing to edge servers, trimming on-board CPU needs and heat output, thus addressing restraint-level thermal concerns.

Geography Analysis

Asia-Pacific delivered the largest connected helmet market size, accounting for 47.26% of global revenue in 2024 and advancing at a forecast 19.65% CAGR through 2030. India and China represent twin growth engines where two-wheelers dominate daily commutes; government subsidy programs for BIS-certified or CCC-certified smart helmets accelerate the transition from non-standard lids. Local telcos integrate 5G modules in traffic lights across Tier-1 cities, enabling real-time V2X alerts that bolster consumer confidence. Japanese OEMs co-develop proprietary mesh intercoms that integrate seamlessly with domestically popular touring bikes, further embedding connectivity within riding culture. Subsidized insurance premiums for riders who share telematics tighten the value loop, ensuring continued uptake.

North America ranks second by value, underpinned by high average selling prices and a strong after-market customization culture. Federal labeling revisions accommodate electronics without undermining crash standards, giving manufacturers a clear route to compliance. Nationwide 5G coverage allows helmets to tap into cellular V2X feeds, a capability leveraged heavily by touring enthusiasts traversing interstate corridors. Motorsports’ influence remains significant; AMA Supercross partnerships showcase flagship models with carbon shells and adaptive noise cancelation to television audiences, translating racing credibility into street sales. Snowmobile and ATV riders also embrace smart helmets for remote SOS beacons, broadening seasonal demand profiles.

Europe holds a mature yet innovation-friendly environment shaped by ECE 22.06. Governmental Vision Zero road-safety strategies underscore technology adoption, making connected helmets a strategic pillar in wider mobility ecosystems. Urban congestion-charging zones in cities like London and Stockholm discount fees for riders using certified smart helmets that prove compliance, effectively monetizing safe behavior. The bloc’s robust GDPR framework, however, necessitates edge encryption and clear opt-in protocols, nudging product design toward privacy-by-default architectures. Beyond the Big 3 regions, South America and Middle East-Africa yield nascent opportunities as delivery-platform proliferation forces corporate buyers to prioritize rider welfare; multilateral development banks fund pilot projects that bundle helmets into road-safety loans, setting the stage for future scaling.

Mordor Intelligence provides coverage of the connected helmet market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to South Korea, United States, China, Japan, and India incorporating local coverage and market participation, as required.

Competitive Landscape

Competitive intensity is moderate, with the presence of both major players and niche specialists. Traditional brands such as Shoei and Schuberth lean on decades-old safety reputations while licensing mesh intercom modules from Cardo and Sena to keep pace with feature expectations. Start-ups like Forcite and LIVALL differentiate through over-the-air software upgrades, eye-tracking HUDs, and community ride-sharing dashboards, capturing tech-savvy early adopters. GoPro’s 2024 acquisition of Forcite underscores a rising wave of consolidation as electronics giants seek hardware platforms for their content ecosystems. Post-merger, GoPro leverages its sensor and battery IP to boost operating time by 30% without weight penalties, raising the performance bar.

Insurers increasingly partner with OEMs to embed white-label coverage, creating stickier customer relationships and incremental revenue. Supply-chain localization trends push Asian manufacturers to establish final-assembly plants in Europe and North America, avoiding tariff uncertainty and reducing shipping emissions.

Patent filings around dynamic tint visors and graphene-based antennas hint at defensive IP wars that could raise entry barriers for latecomers. The market’s moderate fragmentation also spurs cross-licensing deals that shorten time-to-market for advanced features. Overall, strategic collaborations, M&A activity, and software-driven value capture define the connected helmet industry’s competitive playbook through 2030.

Connected Helmet Industry Leaders

Shoei Co. Ltd.

Sena Technologies

Schuberth GmbH

Forcite Helmet Systems (GoPro, Inc.)

Jarvish Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: GoPro and AGV unveiled a co-branded smart helmet that marries action-camera electronics with premium Italian shell construction.

- March 2025: Cardo Systems and Schuberth released the SC EDGE plug-and-play comms unit, extending Mesh functionality to multiple Schuberth models.

- February 2025: Sena launched the Phantom full-face helmet featuring AI noise cancellation, Harman/Kardon audio, and four-zone illumination.

- January 2025: Intelligent Cranium Helmets debuted an AI-based model at CES, offering 240-degree vision and automatic emergency alerts.

Global Connected Helmet Market Report Scope

| Full-Face |

| Modular/Flip-up |

| Open-Face/Half |

| Off-road/Adventure |

| HUD-Integrated/AR |

| Rider (Individual) |

| Passenger |

| Commercial Fleet and Delivery |

| Offline (Specialty, Superstores) |

| Online (E-commerce) |

| Bluetooth-Only |

| Cellular/4G-LTE |

| 5G and C-V2X |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Full-Face | |

| Modular/Flip-up | ||

| Open-Face/Half | ||

| Off-road/Adventure | ||

| HUD-Integrated/AR | ||

| By End-user | Rider (Individual) | |

| Passenger | ||

| Commercial Fleet and Delivery | ||

| By Distribution Channel | Offline (Specialty, Superstores) | |

| Online (E-commerce) | ||

| By Connectivity Technology | Bluetooth-Only | |

| Cellular/4G-LTE | ||

| 5G and C-V2X | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the connected helmet market in 2025?

The connected helmet market size is USD 0.94 billion in 2025.

What is the growth outlook through 2030?

Revenue is projected to reach USD 2.18 billion by 2030, implying an 18.26% CAGR.

Which region leads to current demand?

Asia-Pacific accounts for 47.26% of global 2024 revenue and posts the fastest 19.65% CAGR.

Which product segment is expanding the quickest?

HUD-integrated/AR helmets are forecast to grow at a 19.12% CAGR through 2030.

Page last updated on: