Europe Connected Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

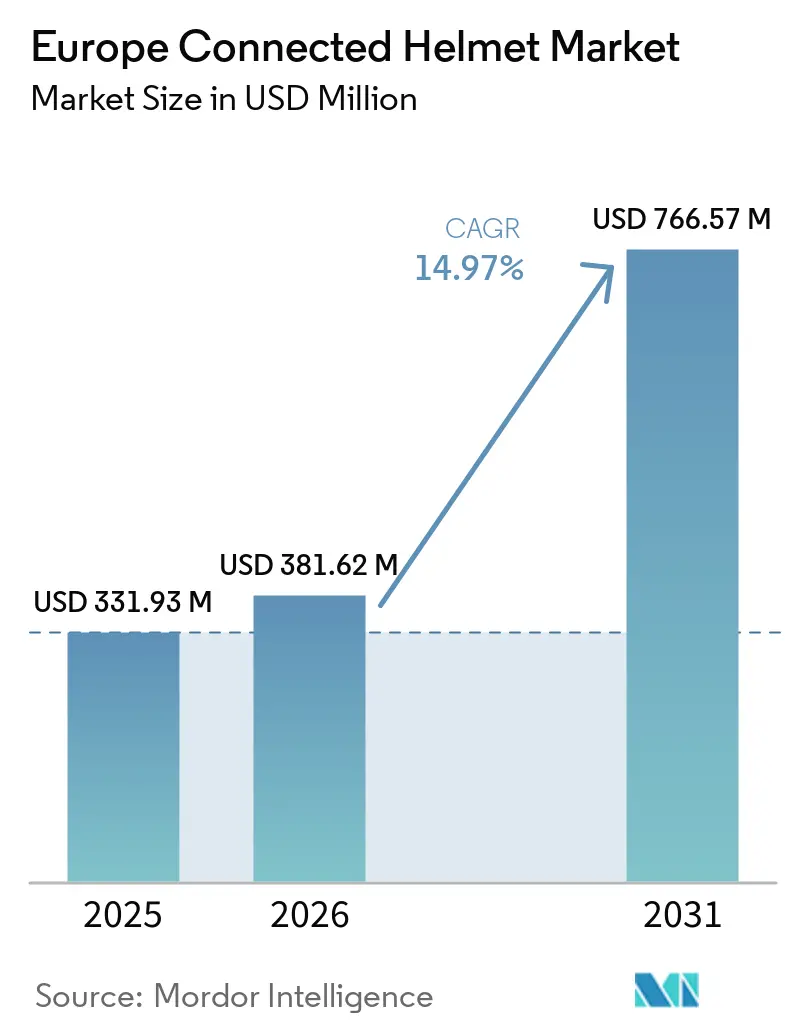

| Base Year Market Size (2025) | USD 331.93 Million |

| Market Size (2026) | USD 381.62 Million |

| Market Size (2031) | USD 766.57 Million |

| Growth Rate (2026 - 2031) | 14.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Connected Helmet Market Analysis by Mordor Intelligence

The Europe-connected helmet market size is projected to grow from USD 331.93 million in 2025 to USD 381.62 million in 2026, and is forecast to reach USD 766.57 million by 2031, growing at a CAGR of 14.97% from 2026 to 2031. In Europe, riders are shifting from traditional head protection to advanced, data-driven devices. These modern helmets not only detect crashes but also offer features like turn-by-turn navigation, group intercom, and automatic eCall. All these functionalities are certified under the new Universal Accessory (UA) pathway. The stringent UA testing now integrates the Bluetooth unit with the helmet’s rotational-impact protocol. As a result, only fully integrated systems achieve seamless homologation. Major German insurers, including Allianz Partners, ERGO, and Harley-Davidson Insurance Services, are boosting the adoption of these helmets. They're offering premium discounts for users of verified connected helmets or telematics sensors. Additionally, a parallel expansion of 5G-V2X corridors along the TEN-T network, supported by funding from the EU and Member States, is ensuring robust helmet-to-vehicle communications. Meanwhile, private-equity recapitalizations and data platforms driven by OEMs are intensifying consolidation pressures. This scenario is pushing established helmet brands to make a tough choice: invest in costly UA certification or risk being sidelined in the aftermarket [1]“2025 Motorcycle Registration Statistics,” ACEM, acem.eu.

Key Report Takeaways

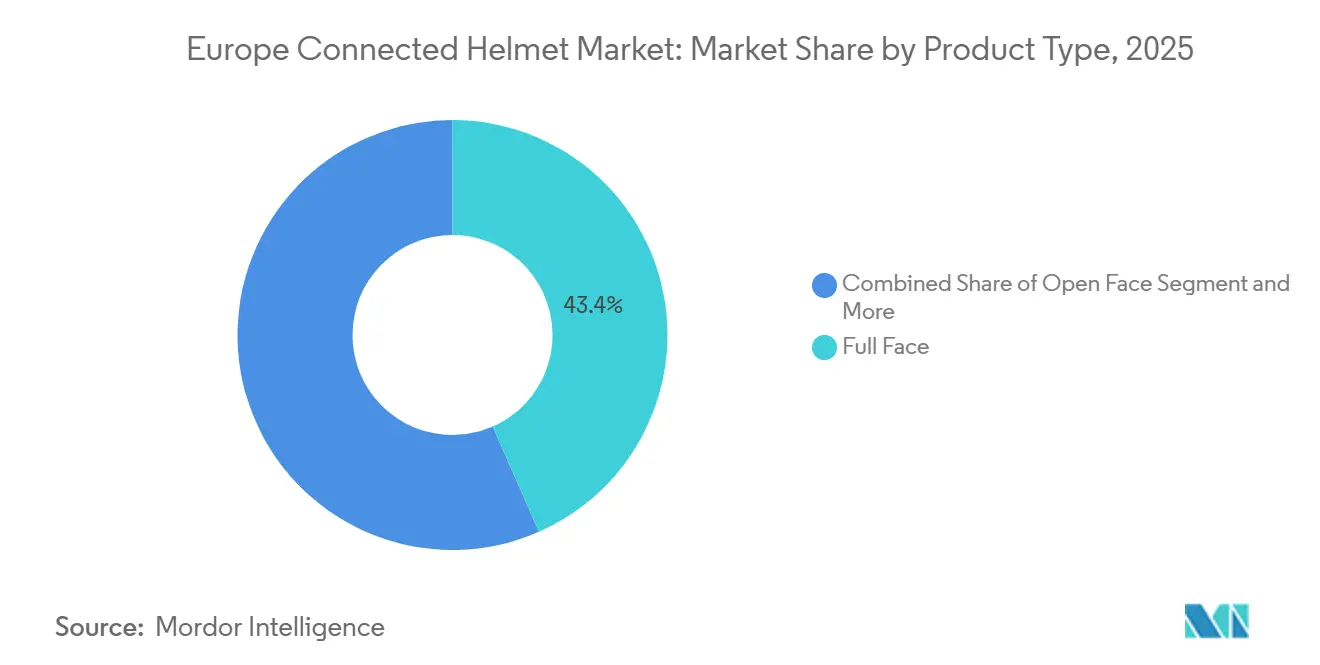

- By product type, full-face helmets accounted for 43.41% of the Europe-connected helmet market size in 2025, while smart HUD-integrated models are forecast to expand at a 15.15% CAGR through 2031.

- By technology level, integrated audio/comms systems captured 37.23% of the Europe-connected helmet market size in 2025, whereas ADAS sensor-suit helmet systems are projected to grow at a 15.03% CAGR through 2031.

- By end user, individual riders accounted for 65.11% of the helmet market in Europe in 2025. Yet, fleet and delivery applications are expected to grow at a 15.07% CAGR over the forecast period.

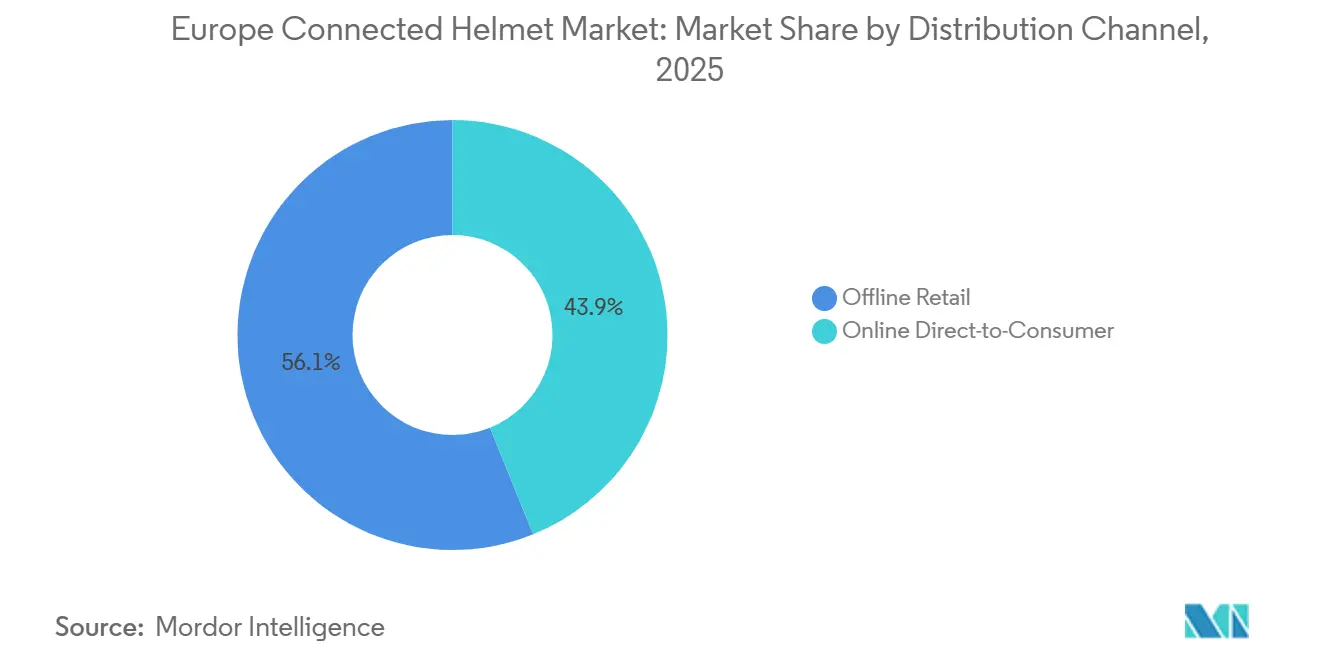

- By distribution channel, offline retail accounted for 56.12% of the Europe-connected helmet market size in 2025, while online direct-to-consumer sales are poised to grow at a 15.21% CAGR through 2031.

- By price range, mid-range helmets priced EUR 200–500 accounted for 44.16% of the Europe-connected helmet market size in 2025, whereas premium models above EUR 500 are set to grow at a 15.26% CAGR through 2031.

- By geography, Germany led the Europe-connected helmet market with 27.23% of the market share in 2025, but the United Kingdom is projected to record the fastest CAGR of 15.11% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global connected helmet market data by Mordor Intelligence represents that combined structure.

Europe Connected Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Motorcycle ADAS | +2.8% | Central and Northern Europe, UK leading | Long term (≥ 4 years) |

| EU Regulation 2025/555 Mandating E-Call Integration | +2.5% | EU-wide, with early adoption in Germany, France | Medium term (2-4 years) |

| Growth In Premium Touring Culture | +1.9% | Germany, Austria, Switzerland, Nordics | Long term (≥ 4 years) |

| Insurance-Premium Discounts | +1.2% | UK, Netherlands, France | Short term (≤ 2 years) |

| 5G-V2X Corridor Build-Out Along TEN-T Routes | +1.1% | Cross-border corridors, major highways | Medium term (2-4 years) |

| OEM Bundling Of Subscription-Based Rider-Data Services | +0.8% | Germany, UK, premium markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Motorcycle ADAS and Hud-Enabled Helmets

Head-up display technology is evolving from a motorsport novelty to a touring essential. Shoei’s GT-Air Smart, developed in collaboration with EyeLights and Sony, enhances rider reaction times by projecting navigation cues directly into their line of sight [2]“GT-Air 3 Smart Technical Sheet,” Shoei Co. Ltd., Shoei, shoei-helmets.com. Schuberth’s C5 ANC features active noise cancellation, helping to reduce fatigue on extended Alpine journeys. Meanwhile, TVS’s prototype showcased at EICMA offers spatially anchored AR guidance, but its limited battery life highlights energy density as a looming engineering challenge[3]“EICMA 2025 AR Helmet Presentation,” TVS Motor Company, tvsmotor.com. German riders, accustomed to high-mileage treks across the Alps, appreciate these fatigue-reducing features and are ready to invest in premium HUD units. As HUD modules find their way into mid-priced helmets, the European connected helmet market is poised for broader price-tier penetration, all while maintaining UA certification standards.

EU Regulation 2025/555 Mandating E-Call Integration

The updated eCall regulations will transition emergency signaling to packet-switched networks. While eCall remains optional for motorcycles, helmet manufacturers are proactively adapting to meet the demands of insurers and fleet purchasers. BMW Motorrad has introduced a vehicle-mounted eCall system that significantly reduces response times, yet it does not incorporate a helmet. Quin Design and LIVALL, by integrating crash sensors into the helmet shell, maintain oversight of rider data and ensure their continued relevance in the aftermarket. Thus, the European connected helmet market hinges on determining which platform—be it a vehicle, a helmet, or a wearable—will first gain consumers' trust and insurers' endorsement.

Growth in Premium Touring Culture Across Central and Northern Europe

In the wake of the pandemic, there's been a surge in demand for long-distance tours, primarily through the scenic Alps and Nordic routes. Nowadays, riders are seeking helmets equipped with Bluetooth mesh chat, real-time weather updates, and turn-by-turn mapping designed to support their 10-hour journeys. These advanced helmets enhance safety and improve the overall riding experience by seamlessly integrating technology. In response, manufacturers customize battery packs to endure sub-zero temperatures, while waterproof pogo-pin connectors ensure audio clarity, even in sleet. Additionally, the ability of touring groups to communicate peer-to-peer enhances perceived value; for instance, an eight-rider convoy can stay connected even when cell service drops in remote mountain passes. This connectivity fosters community and ensures coordination, making group tours more enjoyable and efficient.

Insurance-Premium Discounts For Verified Connected-Helmet Use

In Germany, riders can significantly reduce their annual Harley-Davidson insurance costs by installing a RideLink sensor that activates the eCall feature. Meanwhile, in France, consumers are opting for Cosmo Connected’s bundle, which includes a helmet light, a crash sensor, and an Allianz insurance policy, all available through a single online checkout. VIGO, with its usage-based insurance cover, made its debut in Slovenia and Croatia and swiftly captured market share. This success underscores the viability of hardware-subsidized models in regions sensitive to pricing. As underwriting data increasingly support the notion of reduced crash severity, actuaries are expanding discount tiers. Consequently, it's not just motorcycle registrations but the economics of insurance that are driving sales in Europe's burgeoning connected helmet market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost | -1.8% | Price-sensitive markets, Southern Europe | Short term (≤ 2 years) |

| Limited Battery Life | -1.4% | Northern Europe, Alpine regions | Medium term (2-4 years) |

| GDPR-Driven Data-Privacy Hurdles | -1.2% | EU-wide, with stricter enforcement in Germany, France | Long term (≥ 4 years) |

| Fragmented Certification Add-Ons | -0.9% | Cross-border markets, varying by member state adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Helmets

Connected helmet models are roughly quadruple that of a plain polycarbonate lid, creating sticker shock in markets where average annual motorcycle spend is under a minimal budget. Southern European cities, where low-capacity scooters dominate, display the steepest price elasticity, stalling volume adoption. Providers attempt to soften the blow via buy-now-pay-later plans, yet interest costs partially offset savings from potential insurance rebates, muting conversion. Until electronics costs align with large-scale automotive supply chains, premium segmentation will continue to polarize the connected helmet market.

GDPR-Driven Data-Privacy Hurdles for Crash Telemetry

Article 25 of the GDPR mandates data minimization and explicit consent, requiring that helmets incorporate opt-in toggles and process data on-device. Forcite's transfer of GPS and biometric data to overseas servers activates Standard Contractual Clauses, putting smaller brands under the scrutiny of compliance audits. The EU Data Act expands portability rights to encompass "connected products," which likely includes smart helmets. Consequently, manufacturers must establish robust consent mechanisms ahead of the enforcement deadline. Brands prioritizing privacy by design stand to gain favor with German and Dutch fleets, who perceive GDPR fines as a significant threat to their existence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Full Face Dominance Drives Safety Integration

Full-face models secured 43.41% of the Europe-connected helmet market size in 2025, by balancing aerodynamics, quiet interiors, and ECE 22.06 compliance. The Europe-connected helmet market for smart HUD units is set to outgrow every other category at a 15.15% CAGR to 2031, as nano-OLED modules reach sunlight-readable 3,000 nits and sub-50-gram optics. Shoei’s GT-Air 3 Smart exemplifies the trend, combining Full HD projection with long-lasting batteries to cater to all-day tourers. While open-face and half helmets remain favored for Mediterranean scooter rides, they now face rising certification costs, narrowing the price gap with entry-level full-face models.

Touring riders who appreciate modular helmets for their ability to lift the chin bar during refueling are now benefiting from Cardo’s integration of Mesh technology. This enhancement enables private group communication between multiple riders over long distances, effectively addressing communication challenges in Alpine tunnels. Meanwhile, off-road niches are thriving, as Quin-equipped O’Neal dirt helmets transmit crash data to emergency applications across European nations. Consequently, the European helmet market is divided between premium HUD models and Bluetooth-only full-face variants. Manufacturers adept at bridging both price points are strategically positioned to safeguard both volume and profit margins.

By Technology Level: ADAS Integration Accelerates Safety Evolution

Integrated audio/comms accounted for 37.23% of the Europe-connected helmet market in 2025, as Bluetooth is now table stakes. Cardo and Sena’s latest chipsets deliver 1.6 km of range and automatically switch between Mesh and Bluetooth modes, ensuring backward compatibility while future-proofing firmware updates. Yet ADAS-sensor helmets—gyros, accelerometers, eCall, and V2X—are scaling at 15.03% CAGR to 2031 as insurers demand real-time risk scoring. BMW's Com P1 GS seamlessly integrates crash detection into a module, which conveniently attaches to the GS Carbon shell.

While HUD/AR helmets come with a hefty price tag, they still face challenges with energy density. For instance, TVS's prototype reveals that the battery provides only a limited runtime in continuous AR mode. Designers of all-in-one helmets aspire to achieve the trifecta: UA-certified crash detection, HUD, and V2X functionalities within a single shell. However, as of now, only Midland's BT Mini and BTR1 Advanced have successfully passed UA's rotational tests. As the European market for connected helmets evolves, there's a growing trend towards a modular approach—combining helmets with certified clip-ons—potentially overshadowing the all-in-one super-helmets. This shift may persist until advancements in battery chemistry and a reduction in certification costs align.

By End User: Fleet Applications Drive Commercial Adoption

Individual enthusiasts accounted for 65.11% of the Europe-connected helmet market in 2025, driven by demand for music streaming, group chat, and eCall reassurance. Fleet couriers in London, Paris, and Milan are the fastest-rising cohort, with a 15.07% CAGR, propelled by municipal safety charters that highlight a disproportionate share of motorcycle fatalities relative to the kilometers they ride. In a move echoing the Allianz-Cosmo models in France, Deliveroo, Uber Eats, and Glovo are piloting subsidy schemes that enable riders to lease a connected helmet at a minimal monthly cost.

While passenger helmets play a secondary role, they still benefit from technological advancements. The market for connected helmets in Europe, specifically for fleet-delivery applications, stands poised for significant growth. This projection hinges on three pivotal factors: insurer discounts, platform mandates that embed these helmets into rider contracts, and city licensing reforms that link commercial moped permits to this advanced safety gear.

By Distribution Channel: Digital Transformation Reshapes Sales

Offline held 56.12% of the Europe-connected helmet market size in 2025 because customers still want expert fitting for a safety-critical product. Yet insurer-bundled web stores are posting 15.21% CAGR as riders click to renew policies and receive a subsidized helmet or sensor by mail. Cosmo Connected has crafted a seamless digital journey that bypasses traditional dealer interactions, showcasing the potential of frictionless e-commerce in a domain typically reliant on hands-on trials.

While premium full-face helmets may remain anchored to showrooms due to the intricacies of carbon-fiber shell sizing, the European market for connected helmets is embracing an omnichannel strategy. Features like virtual 3-D fitting applications, a return policy, and the option for dealers to pick up online orders are facilitating smoother conversions across diverse age and income groups.

By Price Range: Premium Segment Drives Innovation

Mid-range EUR 200–500 helmets accounted for 44.16% of the Europe-connected helmet market size in 2025, offering ECE 22.06 compliance and Bluetooth for commuting use. Premium tiers above EUR 500 are slated for a 15.26% CAGR as affluent tourers justify the cost of ANC, HUD, and 10-hour batteries. Schuberth's C5 ANC and Shoei's GT-Air 3 Smart are targeting riders who cover significant distances annually.

Helmets in the economy segment face margin pressures due to rising tooling costs from UA certification. By segmenting their offerings—HUD flagship models, crash-sensor mid-range, and Bluetooth entry-level—manufacturers can dominate the European connected helmet market without undermining their premium sales.

Geography Analysis

Germany accounted for 27.23% of the Europe-connected helmet market in 2025, even though, after Euro 5+ pre-buy distortions, new bike registrations plummeted significantly. With a mature parc, the focus has shifted from first-time purchases to upgrades. In Germany, the size of the connected helmet market is now more influenced by insurer outreach than by motorcycle sales volume, especially as RideLink and ERGO cut premiums substantially for eCall users. Additionally, OEMs are playing a pivotal role in shaping this demand; for instance, BMW is integrating rider data into its ConnectedRide subscriptions through factory-fitted Intelligent Emergency Call, effectively sidelining third-party helmet manufacturers.

The United Kingdom is projected to grow at a 15.11% CAGR through 2031, driven by Transport for London's road-safety charter, which highlights a stark reality: motorcycles account for a significant share of road fatalities, even though they represent a small share of road traffic. In response, delivery platforms face mounting public pressure to enforce the use of connected gear. This push could see the popularity of affordable crash-sensor helmets surge in the coming years. Spain stands out with unique growth in motorcycle registrations, thanks to its year-round riding-friendly weather. However, a keen price sensitivity curbs the adoption of Heads-Up Displays (HUDs) until insurers begin offering hardware subsidies, especially in regions south of the Pyrenees.

Both France and Italy, despite witnessing declines in unit sales, boast extensive installed bases that drive retrofit sales. A notable example is Allianz Partners in France, which offers a helmet-and-insurance bundle at an affordable price, setting a precedent for mid-income regions. Meanwhile, Northern Italy's Alpine corridor continues to see robust demand for premium touring helmets, with brands like Shoei and Schuberth commanding high prices. The Rest-of-Europe, encompassing Austria, Switzerland, Benelux, and the Nordics, naturally gravitates towards the premium segment. Here, affluent riders value HUD navigation for cross-border tours, especially when navigating unfamiliar languages. Overall, the demand for connected helmets in Europe is more closely tied to factors such as insurance telematics density, the maturity of touring culture, and urban fleet mandates, rather than just raw motorcycle sales, prompting a shift in commercial strategies across the continent.

The connected helmet market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for South Korea, United States, China, Japan, and India, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

While no brand commands a dominant market share, strategic maneuvers indicate potential consolidation. Dainese recently underwent a significant recapitalization, injecting substantial funds into its operations while reducing its debt burden. This move positions Dainese to integrate its D-Air airbag telemetry with helmet data, creating a unified safety system. Meanwhile, GoPro, following its acquisition of Forcite, has partnered with AGV. Together, they are combining video capture and crash sensors into a single helmet, targeting creators who seek both footage and claims evidence under one subscription. BMW Motorrad is leveraging its OEM status with its ConnectedRide suite—featuring Com U1, Com P1 GS, and Smartglasses. By preloading connected services trials at the point of sale, BMW effectively sidelines third-party helmets that do not meet UA certification requirements or enable in-dash integration.

Opportunities are emerging in fleet helmets that offer basic eCall features and UA-certified clip-on modules. These modules, designed to avoid shell replacements, are bundled with insurance and available as mail-order upgrades. Quin Design, supported by its stake in Mips, is expanding into motocross and MTB. This development suggests that the European connected helmet industry could soon foster adjacent sports sub-segments. Legacy brands, such as Ducati, KTM, and Triumph, that observe BMW’s direct-bundle strategy must act quickly—those that delay UA testing risk being relegated to low-margin aftermarket channels. The European connected helmet market is increasingly favoring brands that navigate regulatory challenges efficiently, establish partnerships to reduce rider costs, and integrate seamlessly with OEM dashboards.

Europe Connected Helmet Industry Leaders

Dainese SpA

Sena Technologies, Inc.

Schuberth GmbH

Shoei Co., Ltd.

LIVALL Tech Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: At EICMA 2025, SENA debuted its latest innovation: the Specter modular smart helmet. Tailored for touring enthusiasts, the Specter boasts cutting-edge technology and features ideal for long-distance rides. Merging connectivity, comfort, and safety, the Specter underscores SENA's commitment to advancing smart helmet technology.

- November 2025: At Milan's EICMA exhibition, Swiss startup Aegis Rider and Indian two-wheeler giant TVS Motor Company have launched an augmented-reality helmet that showcases cutting-edge heads-up display technology.

Europe Connected Helmet Market Report Scope

The Europe connected helmet market report is segmented by product type (full face, modular/flip-up, open face, half helmet, off-road/ motocross), technology level (bluetooth-only, integrated audio/comms, and HUD/AR display, crash detection and ecall, ADAS sensor suite, and multi feature), end user (individual rider, passenger, and fleet/delivery), distribution channel (offline retail and online direct-to-consumer), and price range (economy, mid-range, and premium) and country. The market forecasts are provided in terms of value (USD).

| Full Face |

| Modular / Flip-up |

| Open Face |

| Half Helmet |

| Off-road / Motocross |

| Smart HUD-Integrated |

| Bluetooth-Only |

| Integrated Audio / Comms |

| HUD / AR Display |

| Crash Detection & eCall |

| ADAS Sensor Suite |

| Multi-Feature (All-in-One) |

| Individual Rider |

| Passenger |

| Fleet / Delivery |

| Offline Retail |

| Online Direct-to-Consumer |

| Economy |

| Mid-Range |

| Premium |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Product Type | Full Face |

| Modular / Flip-up | |

| Open Face | |

| Half Helmet | |

| Off-road / Motocross | |

| Smart HUD-Integrated | |

| By Technology Level | Bluetooth-Only |

| Integrated Audio / Comms | |

| HUD / AR Display | |

| Crash Detection & eCall | |

| ADAS Sensor Suite | |

| Multi-Feature (All-in-One) | |

| By End User | Individual Rider |

| Passenger | |

| Fleet / Delivery | |

| By Distribution Channel | Offline Retail |

| Online Direct-to-Consumer | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe connected helmet market in 2031?

It is expected to reach USD 766.57 million by 2031, advancing at a 14.97% CAGR between 2026 and 2031.

Which product category is growing fastest?

Smart HUD-integrated full-face helmets are forecast to post the highest 15.15% CAGR through 2031.

How are insurers influencing helmet adoption?

Premium discounts up to 60% for verified eCall or telematics use are pushing rapid uptake, especially in Germany, France, and the UK.

Why do delivery fleets matter for future sales?

Urban couriers face safety mandates and can generate double-digit CAGR demand as connected helmets lower liability and speed emergency response.

What technological feature is expected to grow the most?

ADAS Sensor Suite integration leads with a 15.03% CAGR, reflecting demand for predictive safety functions.

Page last updated on: