China Connected Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

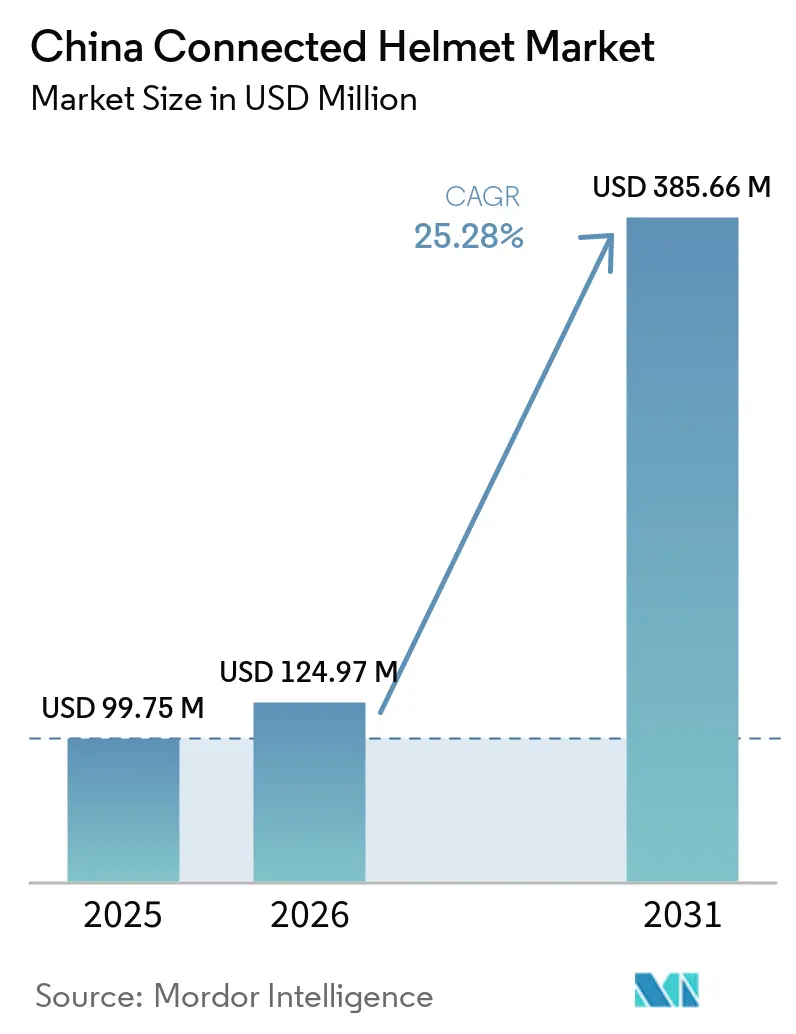

| Base Year Market Size (2025) | USD 99.75 Million |

| Market Size (2026) | USD 124.97 Million |

| Market Size (2031) | USD 385.66 Million |

| Growth Rate (2026 - 2031) | 25.28% CAGR |

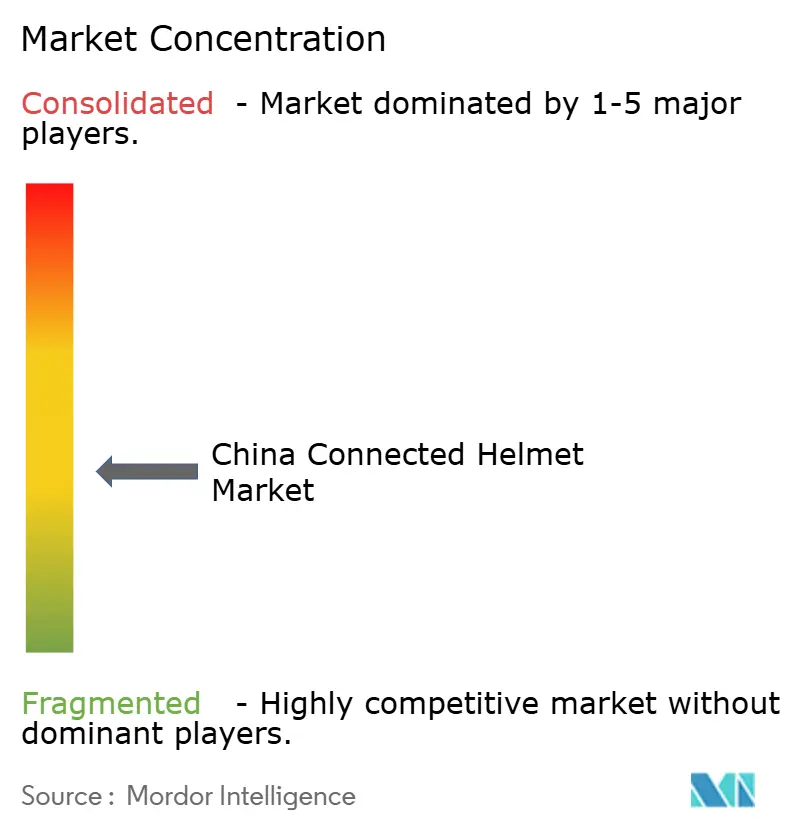

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Connected Helmet Market Analysis by Mordor Intelligence

The China-connected helmet market size is projected to be USD 99.75 million in 2025, USD 124.97 million in 2026, and reach USD 385.66 million by 2031, growing at a CAGR of 25.28% from 2026 to 2031. Food-delivery giants are ramping up bulk purchases, tighter enforcement is taking hold in metropolitan areas, and consumers are increasingly gravitating towards premium motorcycles. In this evolving landscape, platform operators are now viewing helmets not just as safety gear but as telematics nodes, a move that reduces liability and opens doors to insurance rebates. Meanwhile, regulators are broadening their compliance net, extending it from motorcycles to encompass the nation's vast fleet of e-bikes. Domestic manufacturers are riding the wave of policy support from the "Made in China" initiative. However, challenges loom large: the proliferation of counterfeits and a fragmented Bluetooth ecosystem are stalling seamless adoption. Yet, there's a silver lining: manufacturers who can roll out PIPL-compliant, ADAS-ready models priced competitively stand poised to attract a new wave of riders, moving beyond mere passive protection.

Key Report Takeaways

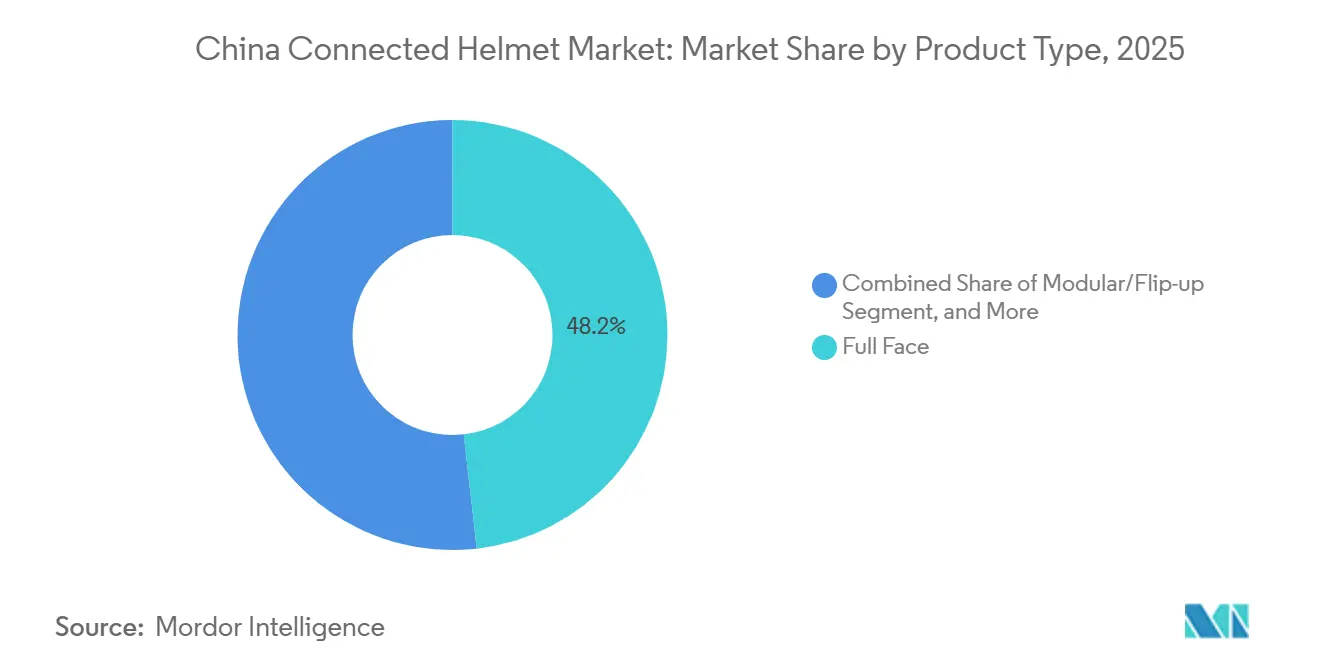

- By product type, full face helmets accounted for 48.15% of revenue in 2025, while smart HUD-integrated variants are forecast to post a 26.25% CAGR through 2031.

- By technology level, Bluetooth-only models commanded 47.33% of the China connected helmet market share in 2025, whereas ADAS sensor suite configurations are projected to advance at a 26.87% CAGR to 2031.

- By end user, individual riders accounted for 84.25% of 2025 demand, while the fleet/delivery segment is expected to grow at a 26.36% CAGR through 2031 as Meituan scales telematics mandates.

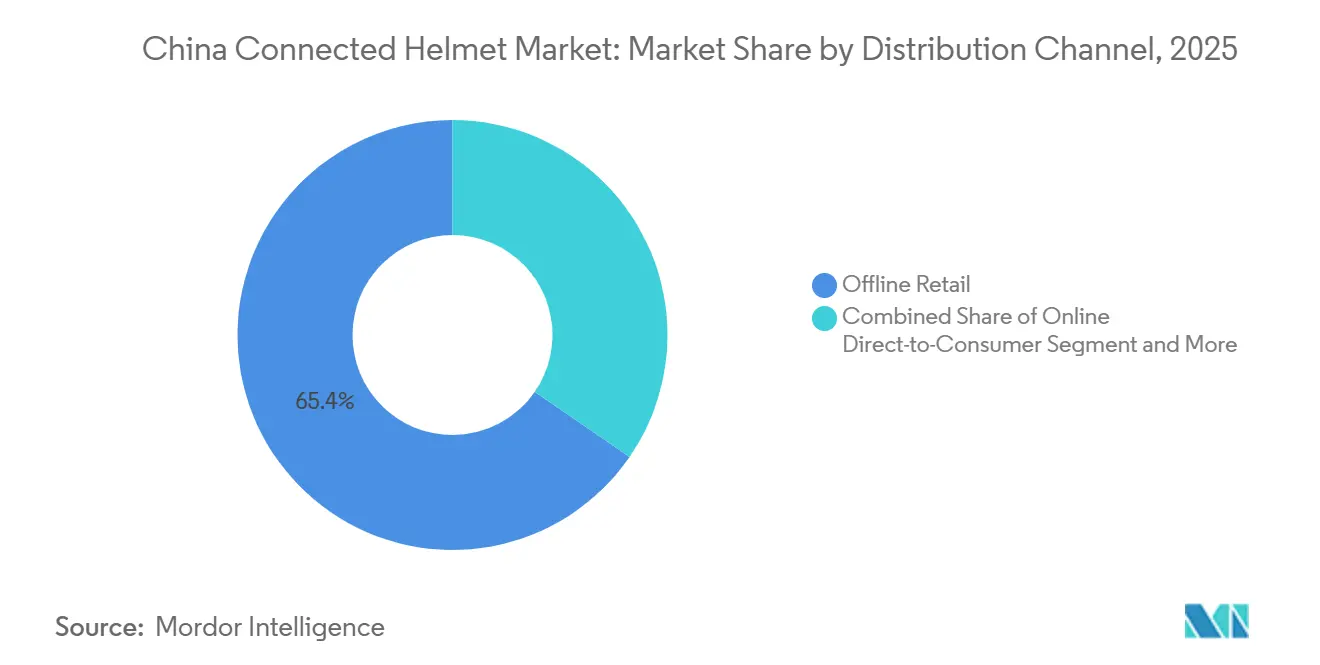

- By distribution channel, offline retail retained a 65.36% share in 2025, while online direct-to-consumer channels are on track for a 25.95% CAGR, powered by e-commerce integrations on Tmall and JD.com.

- By price range, mid-range helmets priced USD 200-500 captured 51.18% share in 2025, while the premium tier above USD 500 is projected to accelerate at a 26.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of China. The connected helmet market share in our global report expresses these relative weights.

China Connected Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Helmet-Wear Enforcement and “One Helmet-One Belt” | +4.2% | Tier-1 and Tier-2 urban clusters | Short term (≤ 2 years) |

| Food-Delivery Platforms’ Bulk Telematics Buys | +4.1% | High-density delivery zones, expanding to Tier-3 cities | Medium term (2-4 years) |

| Premium Motorcycle Registration Surge | +3.8% | Beijing, Shanghai, Guangzhou, Shenzhen, key Tier-2 cities | Medium term (2-4 years) |

| “Made in China 2025” IoT Incentives | +3.5% | Guangdong, Jiangsu, Zhejiang manufacturing hubs | Long term (≥ 4 years) |

| WeChat Mini-Program Integration | +2.9% | Digitally mature provinces nationwide | Medium term (2-4 years) |

| Insurance Rebates for Safe-Riding Telematics | +2.7% | Pilot programs in major metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Helmet-Wear Enforcement and “One Helmet-One Belt” Campaign

Beijing has expanded its helmet law to cover e-bike riders, raising fines to encourage compliance among the nation's vast e-bike community. This move aims to address safety concerns as the number of e-bike users grows [1]“Notice on Mandatory Helmet Use for E-Bikes,”, Beijing Municipal Government, beijing.gov.cn. While helmet use has risen in some cities, most riders still choose basic models. In Yinchuan, local authorities have adopted NFC technology in shared helmets, rendering bikes inoperable unless the rider wears a compliant helmet. This shift favors brands that provide certified helmets with crucial connectivity features. Suppliers are adjusting to this changing scenario, exploring innovative designs and technologies to meet the rising demand for compliant helmets.

Food-Delivery Platforms Bulk-Adopting Telematics Helmets

Meituan had shipped a significant number of connected helmets, demonstrating the dominance of platform economics over traditional retail channels. Ele.me introduced its AI helmet X3, featuring "Xiao E" indoor navigation, which was initially rolled out in multiple malls and is planned for further expansion[2]“Launch of AI Helmet X3,”, Ele.me, ele.me. These helmets come equipped with crash-detection sensors that automatically alert dispatchers. This feature aligns with insurance rebates, offering premium discounts for riders verified as safe. Such bulk procurement not only locks riders into proprietary ecosystems but also accelerates innovation cycles and heightens entry barriers for newcomers.

Surge in Premium Motorcycle Registrations in Tier-1 and Tier-2 Cities

Premium motorcycle registrations grew significantly, with BMW Motorrad leading the market in China [3]“China Sales Report 2024,”, BMW Motorrad, bmw-motorrad.com. In cities like Beijing, Shanghai, and Chengdu, riders are elevating helmets to lifestyle status, investing in features like HUD overlays, rear-camera feeds, and CAN bus integration. TVS introduced its latest offering, the Aegis Rider Vision, featuring binocular micro-OLED displays and a robust battery. As disposable incomes rise, the trend of premium penetration extends beyond motorcycles, reaching into the realm of connected safety gear.

“Made in China 2025” Incentives for IoT and Smart Wearables

Domestic innovators meeting indigenous-innovation criteria are rewarded with tax holidays, R&D subsidies, and fast-track procurement access. LIVALL, boasting numerous patents and alignment with Huawei's HarmonyOS, achieved significant sales on VMALL within a short period. Clusters in Shenzhen, Hangzhou, and Foshan enable helmet manufacturers to co-locate with suppliers of Bluetooth technology, batteries, and injection molding, significantly shortening the lead time from concept to market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Sensitivity Among Commuters | -2.8% | Tier-3 cities and rural areas | Short term (≤ 2 years) |

| Counterfeit/Low-Quality Knock-Offs | -2.1% | Lower-tier cities and online marketplaces | Medium term (2-4 years) |

| Inconsistent Bluetooth Support on Android Forks | -1.9% | Nationwide across device ecosystems | Medium term (2-4 years) |

| Data-Localization and PIPL Compliance Hurdles | -1.7% | Heightened impact on cross-border cloud services | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity Among Commuter Motorcyclists and E-bike Users

On e-commerce platforms, certified mid-priced helmets reign supreme. In contrast, lower-priced units, even though they do not pass the required tests, dominate livestream sales. While counterfeit smart helmets are slightly underpriced compared tostill bear the full cost their authentic counterparts, many commuters view the connectivity feature as non-essential. Lab tests revealed that all low-end helmets tested failed to meet stability standards. Although platform subsidies provide some relief to riders, individual buyers continue to bear the entire expense, hindering widespread adoption.

Prevalence of Counterfeit/Low-Quality Smart-Helmet Knock-offs

In a sweeping crackdown across various regions, authorities seized counterfeit helmets and fraudulent labels. Inspections in pivotal areas revealed alarming failure rates in energy-absorption tests, raising significant safety concerns. Although e-commerce platforms are working to eliminate counterfeit listings, the lag in enforcement is eroding consumer trust and exerting pressure on legitimate manufacturers committed to certification. This situation highlights the urgent need for stricter enforcement and collaboration between regulatory bodies and online marketplaces to safeguard consumer safety and support compliant manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Integration Drives Premium Shift

Full Face models retained 48.15% of the China-connected helmet market share in 2025, as riders value full-coverage protection compatible with aftermarket Bluetooth kits. HUD-Integrated variants, although niche, are forecast to grow at a 26.25% CAGR, eclipsing the broader China-connected helmet market. As premium adopters in China increasingly seek heads-up navigation and rear-view feeds, the market for HUD-integrated helmets is poised for rapid expansion. However, the growth prospects for modular and open-face styles are being curtailed by stricter impact-absorption tests mandated by Beijing's regulations.

Demonstrating its technical viability, HUD technology is making inroads into automotive displays, as evidenced by XPENG's virtual windshield. Brands offering ECE-certified HUD helmets at competitive prices stand to attract aspirational riders, especially those upgrading to higher-value machines. While Full Face units will dominate in volume due to their compliance with standards and alignment with riders' habits, the revenue growth is skewing towards HUD-enabled models. These not only command higher average selling prices (ASPs) but also offer subscription-based software add-ons, enhancing their appeal.

By Technology Level: ADAS Integration Accelerates Safety Evolution

Bluetooth-Only helmets held 47.33% share in 2025, reflecting low entry prices of USD 50-150. ADAS Sensor Suites are set to deliver a 26.87% CAGR, outperforming the China connected helmet market by 1.6 percentage points and lifting its size over the forecast period. Telematics-ready ADAS systems bundle crash detection, eCall, and speed alerts, unlocking insurer rebates and shifting value creation from hardware margins to data services.

Ele.me’s X3 illustrates the leap from appeal to tech-reactive crash alerts to predictive navigation inside malls. Yet fragmented Android Bluetooth stacks force vendors to juggle compatibility layers, raising support costs. Mesh-networked Bluetooth 5.3 chips in EJEAS X10 improve group-ride audio, but backward-compatibility gaps persist. Multi-feature helmets that combine HUD, ADAS, and mesh audio court tech enthusiasts but risk overwhelming casual commuters with feature fatigue.

By End User: Fleet Applications Drive Commercial Adoption

Individual Riders accounted for 84.25% of demand in 2025, yet fleet adoption, led by Meituan, delivered a 26.36% CAGR through 2031, outpacing the overall China connected helmet market. The China-connected helmet market for delivery fleets is expanding as platforms subsidize hardware and recoup costs through reduced accidents. Dispatch dashboards now receive crash-detection telemetry, enabling quicker responses and lower insurance costs.

While individual riders continue to drive sales volume, fleet buyers prioritize durability, IPX6 waterproofing, and easy firmware updates over mere aesthetics. However, it's the needs of these fleets that are shaping industry roadmaps: vendors are integrating on-device encryption and NFC rider IDs to meet employer safety audit standards. Despite their potential, passenger helmets have found limited traction, as ride-hailing apps predominantly lean towards four-wheel solutions in bustling urban centers.

By Distribution Channel: Digital Commerce Transforms Purchasing Patterns

Offline Retail captured 65.36% share in 2025 because touch-and-feel evaluation remains critical for safety gear. However, Online Direct-to-Consumer channels are slated for a 25.95% CAGR as Tmall and JD.com livestreams pair helmet flash sales with motorcycle accessory bundles. Virtual try-ons and one-hour urban deliveries that tackle fit and immediacy concerns are driving a surge in online sales of helmets linked to China.

Counterfeit products remain a major issue in e-commerce. A raid uncovered a store dealing with counterfeit units. While platforms are now using AI image-matching to identify and remove suspicious listings, gaps in enforcement have led to consumer skepticism. Outside of premium motorcycle brands, OEM bundling is still in its infancy. This is largely due to ambiguous liability issues; until standards are established to clarify responsibilities, growth is expected to be driven by either specialized brick-and-mortar stores or flagship stores managed by platforms.

By Price Range: Premium Segment Drives Technology Adoption

Mid-range USD 200-500 models cornered 51.18% of the market in 2025, balancing features and affordability for urban commuters. The Premium segment above USD 500 will expand at 26.66% CAGR, nearly matching the fastest technology tier, as Tier-1 incomes climb and riders equate helmets with status. Rising premium motorcycle sales filter directly into high-spec helmet demand, lifting average selling prices across the China-connected helmet market.

Economy segments below USD 200 face double jeopardy: tightening standards and counterfeit dilution. Provincial tests show failure rates up to 20% for energy absorption. Mid-Range makers are deleting under-performing SKUs in the crowded USD 200-300 band to focus either on sub-USD 150 commuter lines or HUD-equipped models above USD 400, clarifying brand hierarchies.

Geography Analysis

In China, affluent riders in Tier-1 cities like Beijing, Shanghai, Guangzhou, and Shenzhen are driving a significant portion of the premium revenue in the helmet market, particularly for HUD and ADAS variants. BMW Motorrad's sales growth underscores the strong demand for high-performance bikes and their associated connected gear. A law enacted in Beijing mandates helmet use for e-bike riders, establishing a compliance baseline that favors certified vendors.

In Tier-2 cities such as Hangzhou, Chengdu, and Wuhan, rising incomes are fostering a burgeoning motorcycle culture. Hangzhou, home to several LIVALL supply-chain partners, benefits from shorter iteration loops and reduced logistics costs. While these cities enforce regulations similar to those of their Tier-1 counterparts, they enjoy a premium market without the traffic congestion seen in Beijing.

In Tier-3 cities and rural areas, price sensitivity is evident, with units priced below RMB 60 accounting for the majority of livestream sales. Quality issues highlighted in audits from Shanghai and Shandong have led to mistrust, stalling the shift to connected upgrades. However, initiatives like Yinchuan's NFC-gated shared e-bikes demonstrate that smaller cities can cultivate a demand for affordable connected helmets.

Coastal provinces, due to their proximity to clusters in Shenzhen, Hangzhou, and Foshan, enjoy advantages such as swift restocking and easy access to components. In contrast, inland areas face higher freight costs, leading them to prefer offline dealers focused on slower-moving stock. The "One Helmet, One Belt" initiative boosted usage in targeted areas, yet rural compliance lags behind urban standards. This regional diversity necessitates strategies like tiered pricing, dialect-specific voice assistants, and localized marketing to tap into the next wave of riders.

Mordor Intelligence examines the connected helmet market across diverse other regional markets as well, including Europe, while also offering granular country-level perspectives for India, South Korea, United States, and Japan and more.

Competitive Landscape

China's helmet market shows moderate fragmentation. Domestic players like LIVALL, Smart4U, CNELL, and FreedConn compete with international premium brands such as BMW Motorrad, Sena, and Jarvish. They also face competition from established helmet manufacturers such as HJC and Shoei. LIVALL's collaboration with Huawei's HarmonyOS Connect led to impressive sales on VMALL, achieved within a short period of the product's launch. This underscores the significant influence of super-app ecosystems in the market. FreedConn, on the other hand, capitalizes on certifications from CE, FCC, and ISO, allowing it to cater to export markets through white-label contracts.

Strategic approaches vary across the board. Some brands are integrating their products with platforms like WeChat or HarmonyOS, embedding helmets into the daily routines of super-app users. In contrast, other brands are focusing on proprietary mesh networks and innovations in heads-up displays (HUD). There's a notable gap in the market for insurance-validated telematics priced under a specific threshold, presenting an opportunity for new entrants, especially those collaborating with Ping An. However, potential newcomers face hurdles, notably the costs associated with GB 811-2010 and ECE 22.06 certifications, as well as the need for data architectures compliant with the Personal Information Protection Law (PIPL).

Current technological advancements are heavily focused on AI-driven voice assistants, indoor navigation systems, and camera-based Advanced Driver-Assistance Systems (ADAS). LIVALL is set to unveil its AI Visual Smart Helmet, which will incorporate computer-vision hazard detection atop traditional Bluetooth functionalities. Meanwhile, Jarvish is targeting a niche market, offering helmets with carbon-fiber shells powered by Qualcomm's Snapdragon technology. The fight against counterfeiting is crucial: consistent enforcement not only strengthens brand equity for legitimate manufacturers but also deters fleeting imitators.

China Connected Helmet Industry Leaders

HJC Helmets

Shoei Co., Ltd.

LS2 Helmets (Foshan)

LIVALL Tech Co., Ltd.

YEMA Helmet Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Beijing has enforced mandatory helmet rules for e-bike riders, extending the GB 811-2010 standards citywide. This regulation aims to enhance rider safety and reduce the risk of head injuries in accidents. The GB 811-2010 standards specify the technical requirements for helmets, including impact resistance and durability, ensuring a higher level of protection for users.

- January 2025: Exeger partnered with Cosonic to debut a solar-powered, self-charging smart helmet optimized for China’s urban courier fleet.

China Connected Helmet Market Report Scope

The China-connected helmet market report is segmented by product type (full face, modular/flip-up, open face, half helmet, off-road/ motocross, and smart HUD-integrated), technology level (Bluetooth-only, integrated audio/comms, HUD/AR display, crash detection and ecall, ADAS sensor suite, and multi-feature (All-in-One)), end user (individual rider, passenger, and fleet/delivery), distribution channel (offline retail, online direct-to-consumer, and OEM Accessory Bundles), and price range (economy, mid-range, and premium). The market forecasts are provided in terms of value (USD) and volume in units.

| Full Face |

| Modular/Flip-up |

| Open Face |

| Half Helmet |

| Off-road/Motocross |

| Smart HUD-Integrated |

| Bluetooth-Only |

| Integrated Audio/Comms |

| HUD/AR Display |

| Crash Detection and eCall |

| ADAS Sensor Suite |

| Multi-Feature (All-in-One) |

| Individual Rider |

| Passenger |

| Fleet/Delivery |

| Offline Retail |

| Online Direct-to-Consumer |

| OEM Accessory Bundles |

| Economy (Below USD 200) |

| Mid-Range (USD 200 - USD 500) |

| Premium (Above USD 500) |

| By Product Type | Full Face |

| Modular/Flip-up | |

| Open Face | |

| Half Helmet | |

| Off-road/Motocross | |

| Smart HUD-Integrated | |

| By Technology Level | Bluetooth-Only |

| Integrated Audio/Comms | |

| HUD/AR Display | |

| Crash Detection and eCall | |

| ADAS Sensor Suite | |

| Multi-Feature (All-in-One) | |

| By End User | Individual Rider |

| Passenger | |

| Fleet/Delivery | |

| By Distribution Channel | Offline Retail |

| Online Direct-to-Consumer | |

| OEM Accessory Bundles | |

| By Price Range | Economy (Below USD 200) |

| Mid-Range (USD 200 - USD 500) | |

| Premium (Above USD 500) |

Key Questions Answered in the Report

How large will the China connected helmet market be by 2031?

It is forecast to reach USD 385.66 million, expanding at a 25.28% CAGR from 2026 to 2031.

Which helmet technology is growing fastest in China?

ADAS Sensor Suite configurations are projected to log the highest 26.87% CAGR through 2031 as insurers reward telematics-verified safe riding.

Why are food-delivery platforms important for helmet demand?

Meituan and Ele.me treat helmets as fleet-management tools, having already deployed more than 1 million smart units that reduce liability and qualify riders for insurance rebates.

How do China’s data laws affect foreign helmet brands?

PIPL requires local data storage, forcing overseas brands to invest in domestic cloud infrastructure and redesign products for on-device analytics.

Page last updated on: