South Korea Connected Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

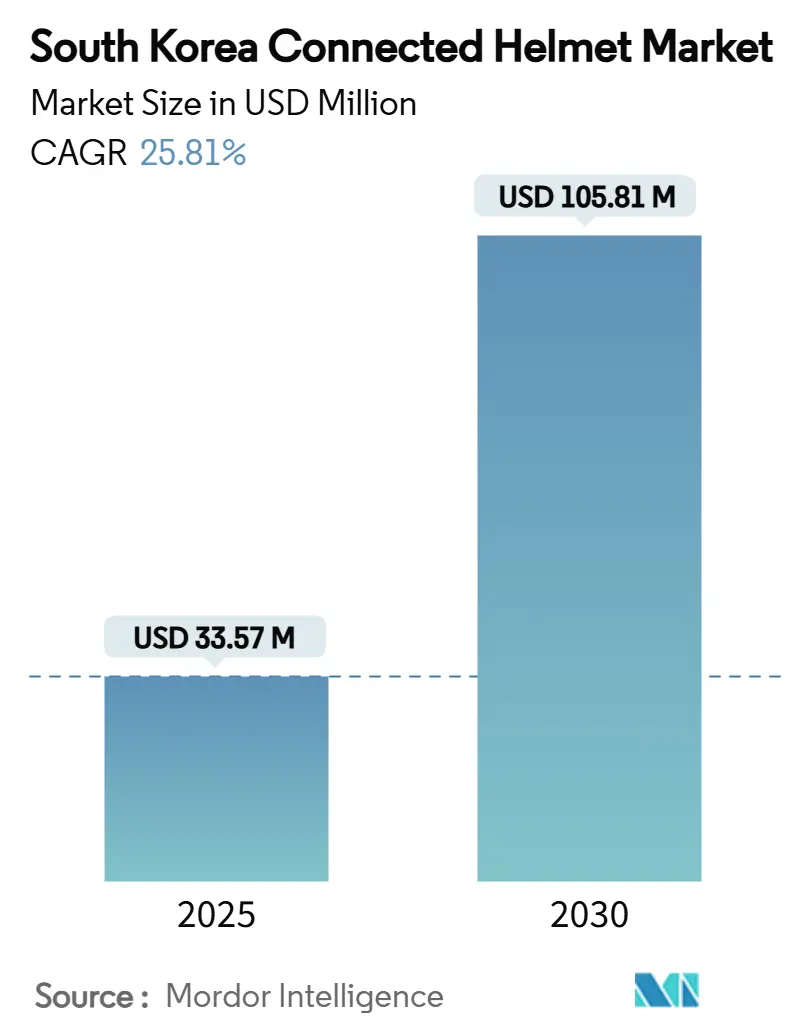

| Market Size (2025) | USD 33.57 Million |

| Market Size (2030) | USD 105.81 Million |

| Growth Rate (2025 - 2030) | 25.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Connected Helmet Market Analysis by Mordor Intelligence

The South Korea Connected Helmet Market size is estimated at USD 33.57 million in 2025, and is expected to reach USD 105.81 million by 2030, at a CAGR of 25.81% during the forecast period (2025-2030). Recent momentum comes from Vision Zero goals, over four-fifths legacy helmet‐use compliance, and a policy push to keep annual traffic deaths minimal. Rising consumer focus on predictive accident warning, telematics‐linked insurance rebates, and integration with nationwide V2X corridors supports enduring demand. Manufacturers able to merge UN Regulation No. 22 structural safety with battery-efficient electronics gain a decisive edge, while logistics fleets view crash documentation as a pathway to lower premiums. Simultaneously, spectrum-efficient chipsets, AI-enabled image recognition, and mid-range price points foster mass adoption.

Key Report Takeaways

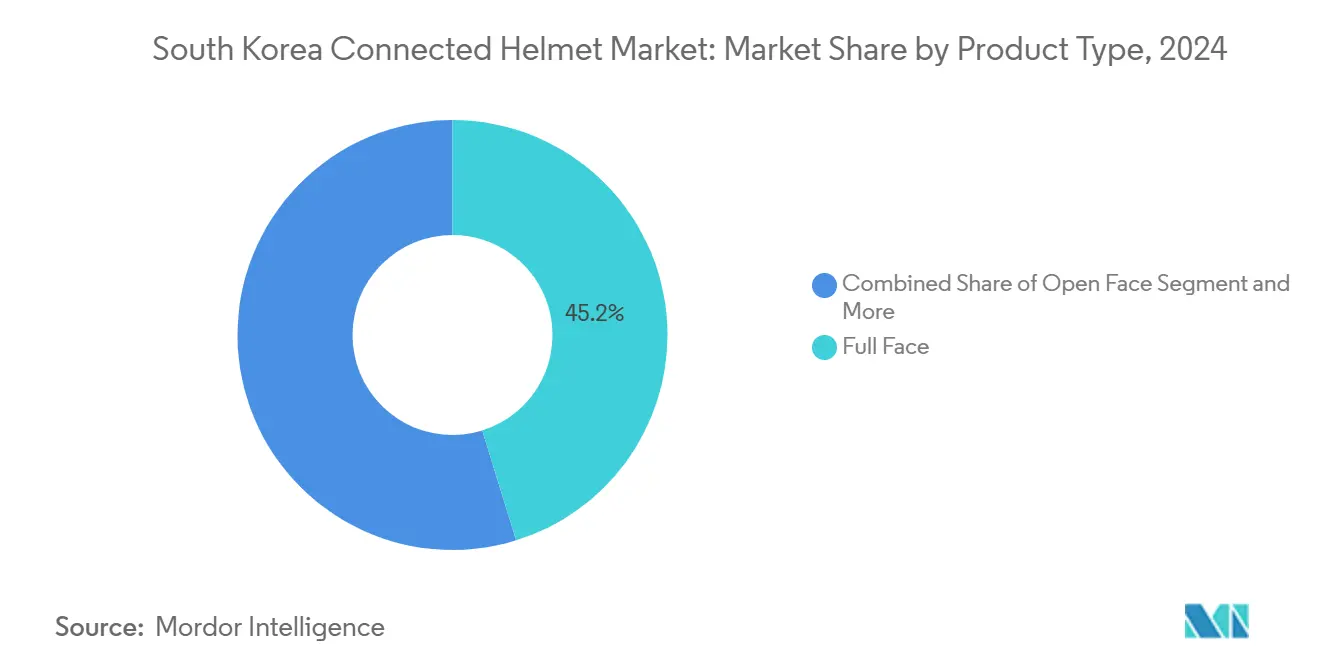

- By product type, full-face formats led the South Korean connected helmet market with 45.17% of the share in 2024; smart HUD-integrated variants are projected to advance at a 26.17% CAGR through 2030.

- By technology level, Bluetooth-only models accounted for a 35.18% share of the South Korea connected helmet market in 2024, while ADAS sensor suites are forecast to grow 25.93% annually to 2030.

- By end user, individual riders captured 67.37% revenue share of the South Korea connected helmet market size in 2024, whereas fleet/delivery demand will accelerate at a 25.97% CAGR over the same period.

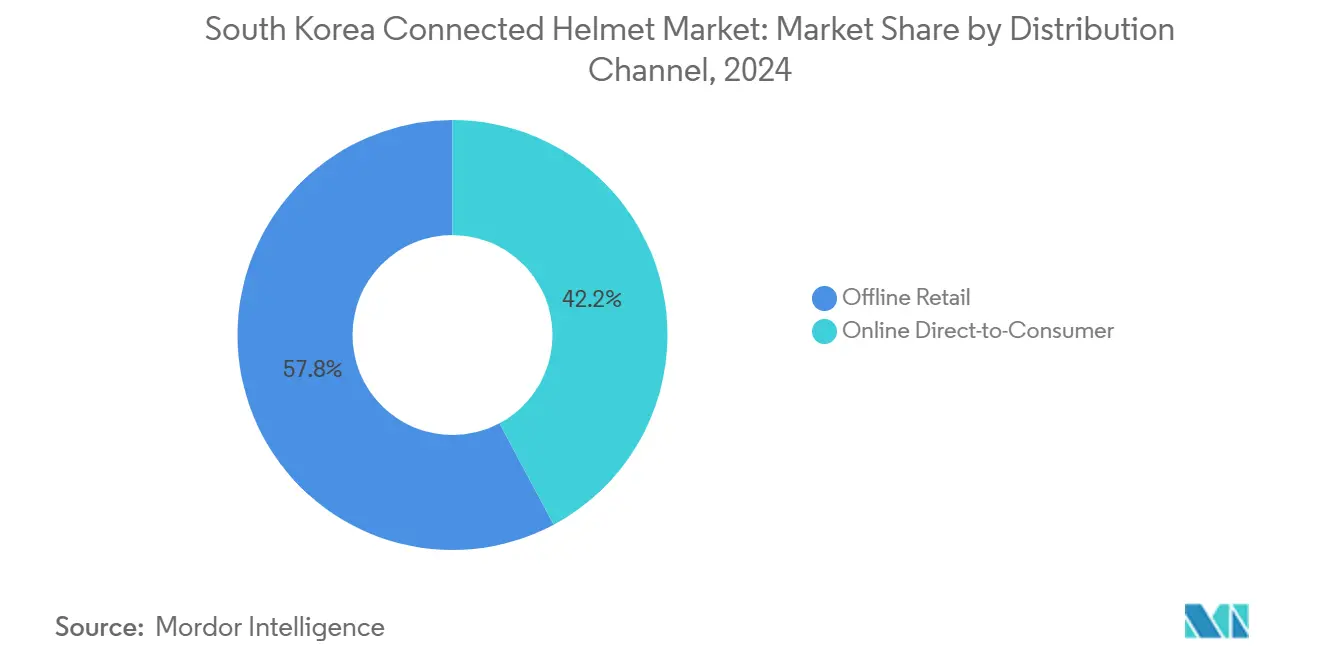

- By distribution channel, offline retail held 57.81% of South Korea's connected helmet market share in 2024, yet online direct-to-consumer is expected to clock a 26.21% CAGR until 2030.

- By price range, mid-range helmets represented 46.94% of the South Korea connected helmet market size in 2024; premium units are poised for 26.11% CAGR expansion to 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with South korea representing one among them. The global report on connected helmet market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

South Korea Connected Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Motorcycle ADAS | +4.2% | National, concentrated in Seoul-Incheon metropolitan area | Medium term (2-4 years) |

| Stringent Helmet-Safety Regulations | +3.8% | National, with enhanced enforcement in urban corridors | Short term (≤ 2 years) |

| Growth Of Premium Motorcycle | +3.1% | National, with early adoption in Busan, Daegu, Gwangju | Long term (≥ 4 years) |

| Expansion Of Direct-To-Consumer E-Commerce Channels | +2.9% | National, accelerated by digital payment infrastructure | Short term (≤ 2 years) |

| Integration Of V2X Chips Enabling | +2.7% | National, piloted in connected vehicle corridors | Medium term (2-4 years) |

| Insurance-Premium Discounts | +2.4% | National, varies by insurance provider coverage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption Of Motorcycle Adas & Hud-Enabled Helmets

Full-color HUD modules projecting navigation, speed, and hazard alerts directly into the visor elevate situational awareness in Seoul’s dense traffic. Test programs show forward-collision warnings can trim crash likelihood by one-fifth, accelerating premiumization. Domestic firms such as Sena leverage AI image-classification borrowed from auto telematics to deliver lane-merge alerts without distracting riders[1]Sena Technologies, “Sena Announces New Integrated Smart Helmet Platform,” sena.com. Touring clubs increasingly refuse non-HUD gear, pushing suppliers to integrate optics, sensors, and Bluetooth Low Energy in shells that still satisfy UN Regulation No. 22[2]United Nations Economic Commission for Europe, “Regulation No. 22 — Protective Helmets,” unece.org .

Stringent Helmet-Safety Regulations In Korea’S Road Traffic Act

Nationwide enforcement of certified helmets, paired with more than four-fifth compliance, provides a ready baseline for electronics-enhanced models. Vision Zero targets intensify scrutiny: police checkpoints now scan QR tags to verify UN Regulation No. 22 approval and electronic module integrity. Authorities began pilot trials collecting anonymized crash telemetry, signaling future compulsory data interfaces. While e-scooter compliance lagged behind, regulators indicate automated verification embedded in connected helmets could close that gap.

Growth Of Premium Motorcycle & Leisure-Touring Community

Registrations of 750 cc-plus motorcycles rose to more than one-tenth in 2024, spurring demand for helmets with intercom arrays, drone-quality cameras, and cloud-backed riding logs. Riders on Busan’s coastal loops coordinate via group-mesh V2X chips that maintain line-of-sight-free chatter. The leisure segment embraces helmets priced above KRW 800,000 (USD 607) for seamless pairing with adaptive cruise control bikes, reinforcing a cycle of high-spec hardware and software updates.

Expansion Of Direct-To-Consumer E-Commerce Channels

Mobile wallet usage beyond four-fifth of adult Koreans pushes helmet makers toward webstores that bundle firmware updates and extended warranties. Detailed 3-D sizing apps lower return rates, while live-stream demos replicate the tactile store experience. Manufacturers secure 4-6 percentage-point margin gains by bypassing distributors and leverage real-time user data to iterate modules within months rather than years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost | -2.8% | National, more pronounced in price-sensitive segments | Short term (≤ 2 years) |

| Limited Battery Life | -1.9% | National, critical for touring routes outside urban areas | Medium term (2-4 years) |

| Bluetooth / Wi-Fi Spectrum Congestion | -1.6% | Seoul-Incheon metropolitan area, major urban centers | Long term (≥ 4 years) |

| Data-Privacy Compliance Hurdles | -1.3% | National, aligned with global data protection standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Helmets

A UN-compliant polycarbonate helmet retails near KRW 90,000 (USD 68), whereas connected variants begin above KRW 420,000 (USD 318). Cash-constrained courier firms hesitate to outfit entire fleets despite safety mandates. Until scale economies and PCB standardization emerge, uptake remains skewed toward premium categories even though long-term insurance savings could offset cost.

Limited Battery Life For Long-Distance Touring Riders

Current 1,800 mAh packs supply roughly eight hours of mixed HDR camera and HUD operation. Multi-day riders on Jeju Island must carry power banks or disable high-drain features. Manufacturers are experimenting with flexible photovoltaic visors that trickle-charge during daylight, but consumer rollout awaits drop-test validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Full-Face Dominance Meets Smart Integration

Full-face units controlled 45.17% of the South Korean connected helmet market share in 2024, reflecting the public’s trust in full-jaw protection for congested streets. Smart HUD-integrated models, combining optical waveguides and micro-projectors without adding bulk, are expected to tip the segment’s South Korean connected helmet market size upward at a 26.17% CAGR.

Riders in metropolitan corridors prefer noise-isolation and air-flow design that accommodates multiple sensors. Manufacturers leverage carbon-aramid shells to offset the weight of Li-Ion modules, preserving fatigue thresholds. Modular/flip-up formats cater to commuter flexibility yet face sealing challenges when integrating broad-angle cameras. Open-face sales persist among scooter riders but record limited ADAS integration due to visor real estate.

By Technology Level: Bluetooth Foundation Enables ADAS Evolution

Bluetooth-only rigs held 35.18% share of South Korea connected helmet market size in 2024 by enabling call, music, and basic ride-stats streaming. This baseline connectivity remains vital for mass-market appeal at controlled price points.

ADAS sensor suites, grows at a robust CAGR of 25.93%—gyroscopes, millimeter-wave radar, and dual-lens cameras—push South Korea connected helmet market share of multi-feature platforms higher as OEMs preload edge-AI processors. Yet spectrum congestion in Seoul prompts companies to test UWB localization for blind-spot alerts. HUD/AR displays gain ground in touring circuits with direct-sunlight legibility breakthroughs, and firmware modularity lets riders progressively unlock functions.

By End User: Individual Riders Drive Fleet Innovation

Individual purchasers represented 67.37% of South Korea connected helmet market size in 2024, motivated by personal safety and gadget engagement. They demand hands-free control, voice assistants, and software ecosystems mirroring smartphone UX.

Fleet/delivery operators, expected to scale at 25.97% CAGR, seek tamper-evident crash logs, geo-fencing, and remote diagnostics. APIs sync helmets with route-optimization dashboards to cut idling time. Passenger and ride-hailing helmets with removable liners and QR-linked cleaning logs remain niche but benefit from shared-mobility safety campaigns.

By Distribution Channel: Physical Fitting Meets Digital Convenience

Offline retail accounted for 57.81% of South Korea connected helmet market share in 2024 owing to mandatory fit checks and UN label inspection. Helmet boutiques offer certified sizing rigs and on-site visor alignment.

In contrast, online direct-to-consumer storefronts—growing at 26.21% CAGR—enable long-tail SKU availability and flash firmware bundles. Augmented-reality head-scan apps improve sizing accuracy, with return rates falling below 5%. Partnership models see web orders collected at brick-and-mortar outlets, blending convenience with skilled fitting.

By Price Range: Mid-Range Stability Enables Premium Growth

Mid-range helmets captured 46.94% South Korea connected helmet market share in 2024, balancing safety and entry-level connectivity. Step-down economy lines face limited sensor arrays and lower-grade batteries.

Premium tiers—on track for 26.11% CAGR—bundle ADAS, HUD, 4K cameras, and eSIMs capable of OTA diagnostics. Subscription models offer cloud-storage plans and crash-response services, converting one-off gear sales into recurring revenue.

Geography Analysis

Seoul–Incheon, bolstered by 5G densification and dedicated ITS roadside units, dominates South Korea's connected helmet market, accounting for over three-fifths of its size. Early adopters are particularly keen on lane-merge alerts and traffic-signal priority data streamed directly to their helmet HUDs. The region's advanced infrastructure and high concentration of tech-savvy consumers further drive adoption rates, making it a critical hub for market growth.

Busan’s port logistics community is next in line, emphasizing fleet telematics to safeguard riders amidst the bustling cargo traffic. The integration of connected helmets into fleet management systems enhances rider safety and operational efficiency, addressing the unique challenges posed by mixed cargo traffic. Meanwhile, Daegu and Gwangju are witnessing double-digit growth, thanks to provincial government funding for Vision Zero demonstration corridors. These initiatives aim to reduce traffic fatalities and promote safer road environments, further accelerating the adoption of connected helmets. Coastal highways, a magnet for touring enthusiasts, see a surge in demand for premium helmets, especially those boasting marine-layer-resistant optics. The scenic routes and challenging weather conditions along these highways make advanced helmet features a necessity for riders.

In rural Jeollanam-do, the adoption rate lags due to inconsistent cellular coverage. However, there's potential for growth with the introduction of solar-assisted battery designs. These innovations address the region's infrastructure limitations, offering a sustainable solution for powering connected helmets. On a national scale, policies are pushing for 100% compliance with UN-approved helmet usage, and the trend leans heavily towards connected variants. The government's commitment to enhancing road safety and promoting advanced technologies is expected to further propel the market during the forecast period.

Mordor Intelligence provides coverage of the connected helmet market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Japan, India, United States, and China incorporating local coverage and market participation, as required.

Competitive Landscape

In South Korea's connected helmet market, key players like HJC, Sena, Samsung-backed Nexxbrain, and the French-Korean joint venture Cosmo-SG each command mid-single-digit market shares, indicating a medium concentration. The market is characterized by companies that integrate in-house shell production with electronics, enabling them to achieve both cost and lead-time advantages, which are critical in maintaining competitiveness.

Strategic partnerships are on the rise: HJC has licensed Sena's mesh intercom boards, and the startup Labonic, by sourcing carbon shells from OEMs, is honing in on AR optics. These collaborations highlight the growing importance of leveraging external expertise to enhance product offerings. Intellectual property battles are centered around DSRC message encryption and the innovative curved-visor HUD optics, which are pivotal in differentiating products in this competitive market.

Companies face hurdles, such as the need for UN 22 recertification with every electronics update, which adds complexity and cost to product development cycles. In a strategic pivot, firms are moving towards subscription-based crash-report SaaS, establishing data moats and customer lock-in. This shift not only creates recurring revenue streams but also strengthens customer relationships through value-added services. Meanwhile, investors are increasingly cautious, given the global shortages of high-spec chips, emphasizing the importance of secure component supply to ensure uninterrupted production and delivery.

South Korea Connected Helmet Industry Leaders

Sena Technologies Inc.

Shoei Co., Ltd.

Schuberth GmbH

LIVALL Tech Co., Ltd.

Dainese SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: South Korea tightened e-scooter helmet rules after 15.1% compliance findings, spotlighting demand for auto-verification connected helmets.

- May 2024: Allianz Partners and Cosmo Connected unveiled a subscription helmet combining automatic brake lights and fall detection with embedded personal accident insurance.

South Korea Connected Helmet Market Report Scope

| Full Face |

| Modular / Flip-up |

| Open Face |

| Half Helmet |

| Off-road / Motocross |

| Smart HUD-Integrated |

| Bluetooth-Only |

| Integrated Audio / Comms |

| HUD / AR Display |

| Crash Detection & eCall |

| ADAS Sensor Suite |

| Multi-Feature (All-in-One) |

| Individual Rider |

| Passenger |

| Fleet / Delivery |

| Offline Retail |

| Online Direct-to-Consumer |

| Economy |

| Mid-Range |

| Premium |

| By Product Type | Full Face |

| Modular / Flip-up | |

| Open Face | |

| Half Helmet | |

| Off-road / Motocross | |

| Smart HUD-Integrated | |

| By Technology Level | Bluetooth-Only |

| Integrated Audio / Comms | |

| HUD / AR Display | |

| Crash Detection & eCall | |

| ADAS Sensor Suite | |

| Multi-Feature (All-in-One) | |

| By End User | Individual Rider |

| Passenger | |

| Fleet / Delivery | |

| By Distribution Channel | Offline Retail |

| Online Direct-to-Consumer | |

| By Price Range | Economy |

| Mid-Range | |

| Premium |

Key Questions Answered in the Report

How large is the South Korea connected helmet market in 2025?

It is valued at USD 33.57 million with a 25.81% CAGR outlook to 2030.

Which product type leads sales?

Full-face helmets control 45.17% of 2024 revenue thanks to regulatory preference for full-coverage protection.

Why are ADAS sensor suites gaining traction?

Crash-warning functions demonstrated a 20.7% risk reduction, enticing riders and insurers to favor sensor-dense models.

What channels are growing fastest for helmet sales?

Online direct-to-consumer platforms are expanding at 26.21% annually as sizing apps improve fit confidence.

How do insurers support connected helmet adoption?

Carriers such as Allianz offer premium discounts and automated claims when certified helmets transmit crash logs.

What limits adoption in rural touring regions?

Limited battery life and sporadic cellular coverage hinder continuous HUD and V2X functions on extended rides.

Page last updated on: