India Connected Helmet Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

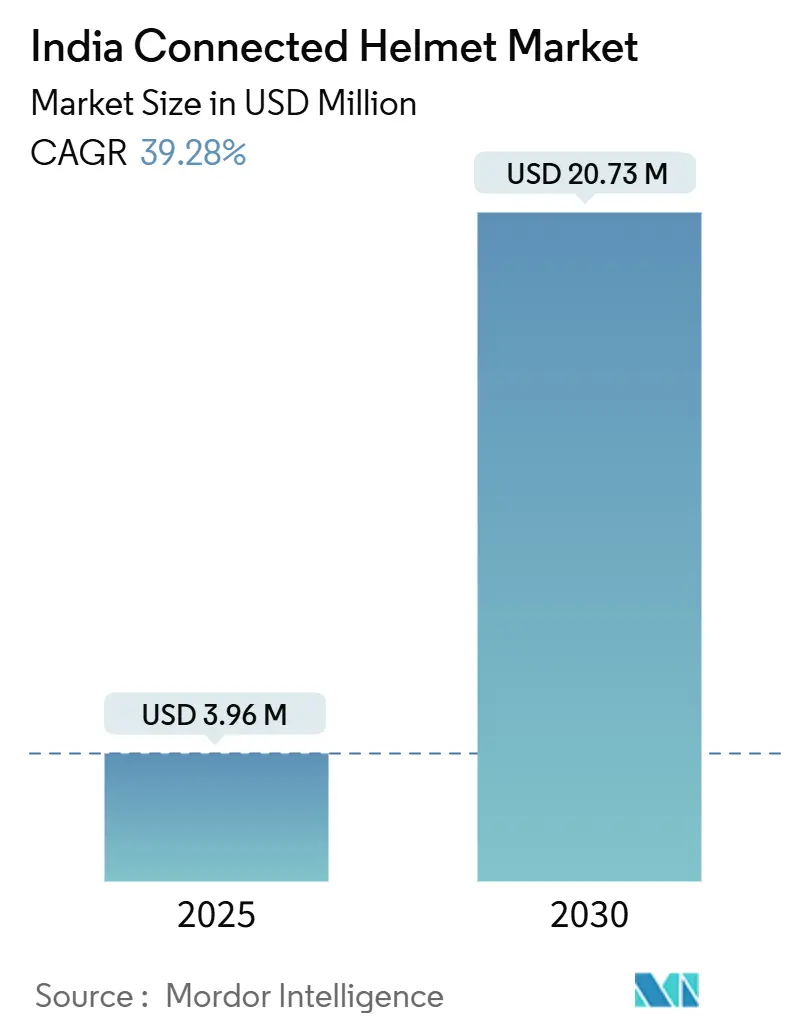

| Market Size (2025) | USD 3.96 Million |

| Market Size (2030) | USD 20.73 Million |

| Growth Rate (2025 - 2030) | 39.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Connected Helmet Market Analysis by Mordor Intelligence

The India Connected Helmet Market size is estimated at USD 3.96 million in 2025, and is expected to reach USD 20.73 million by 2030, at a CAGR of 39.28% during the forecast period (2025-2030). Multiple forces are converging to accelerate adoption: a strict federal rule that every new two-wheeler must be sold with two ISI-certified helmets, heightened road-safety enforcement, and rapid advances in connectivity, crash-detection, and heads-up display (HUD) technologies. Demand is reinforced by a vibrant domestic manufacturing base capable of mass-scale production, while electronics suppliers provide affordable sensors, batteries, and communication modules that lower bill-of-materials costs. The upshot is a connected helmet market primed for sustained double-digit expansion, with premium functionality trickling rapidly into economy price tiers. Competitive dynamics remain fluid: incumbent protective-gear makers hold manufacturing scale advantages, yet electronics specialists and mobility start-ups are injecting software-defined features that can shift brand loyalties quickly.

Key Report Takeaways

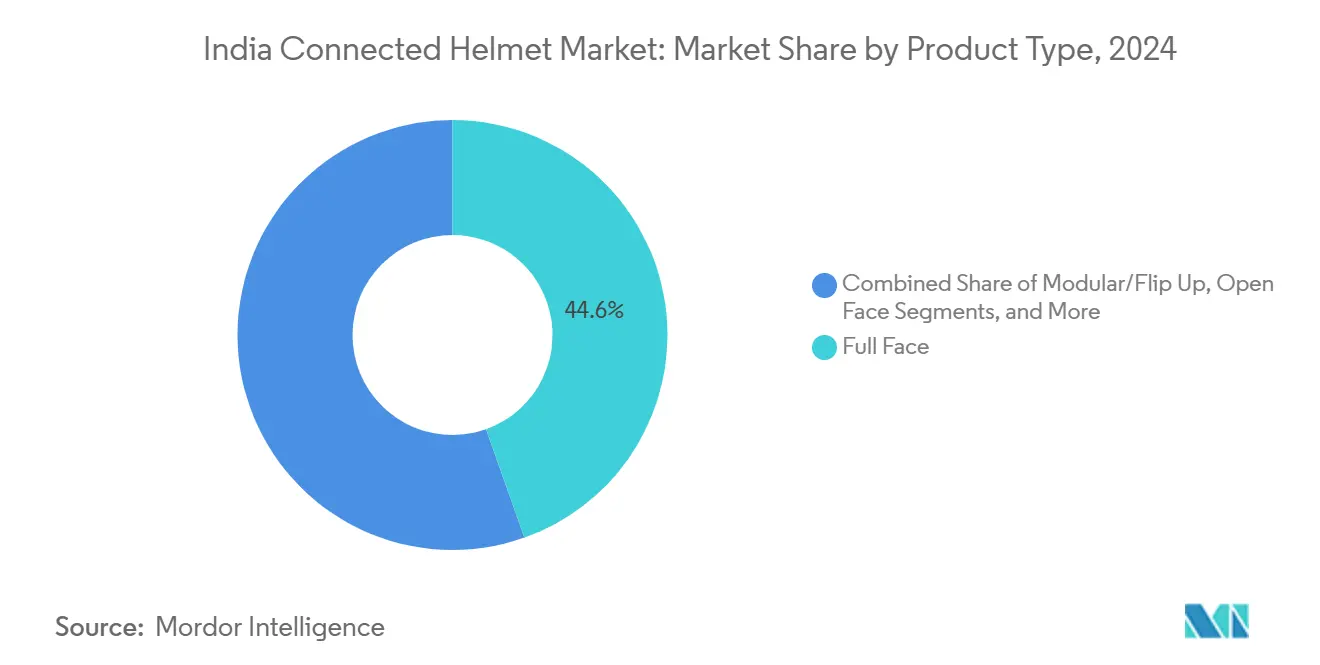

- By product type, full-face helmets claimed 44.56% of the Indian connected helmet market share in 2024; Smart-HUD-integrated models are projected to grow at a 28.40% CAGR to 2030.

- By technology, Bluetooth-only variants held 39.28% of the Indian connected helmet market size in 2024; ADAS sensor-suite models are advancing at a 32.48% CAGR through 2030.

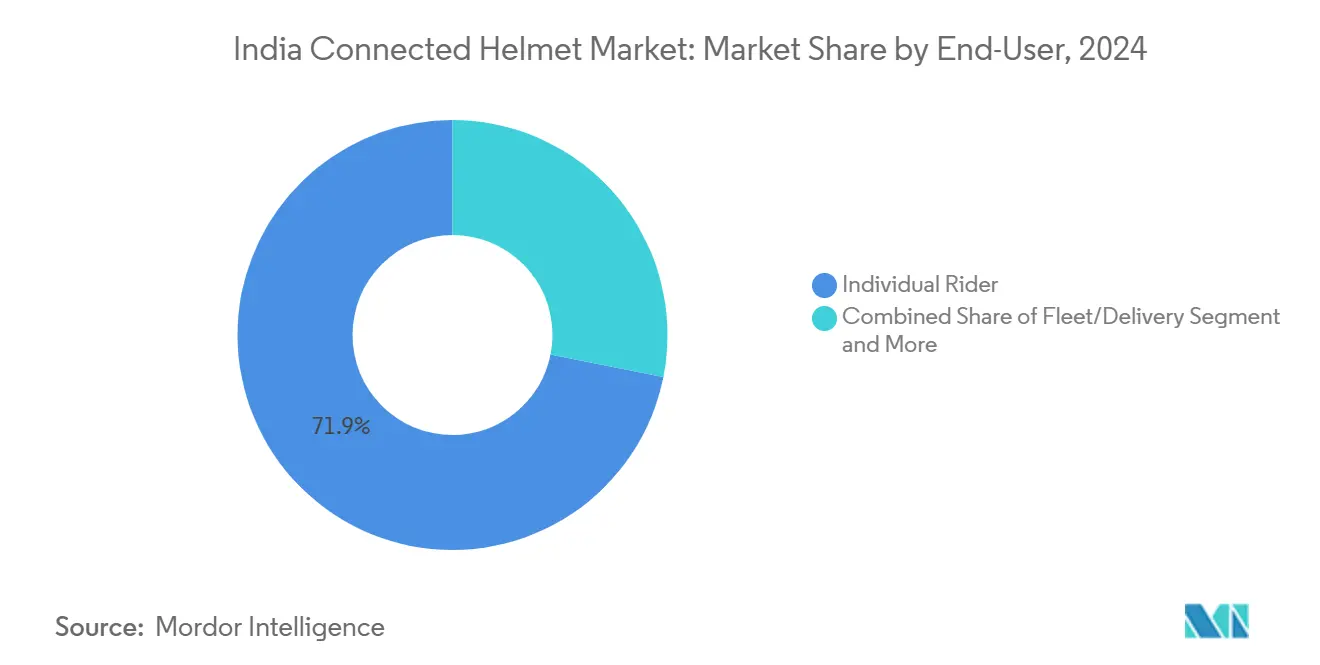

- By end user, individual riders dominated the Indian connected helmet market size, with 71.88% of the share in 2024; fleet and delivery helmets are forecast to expand at a 21.94% CAGR until 2030.

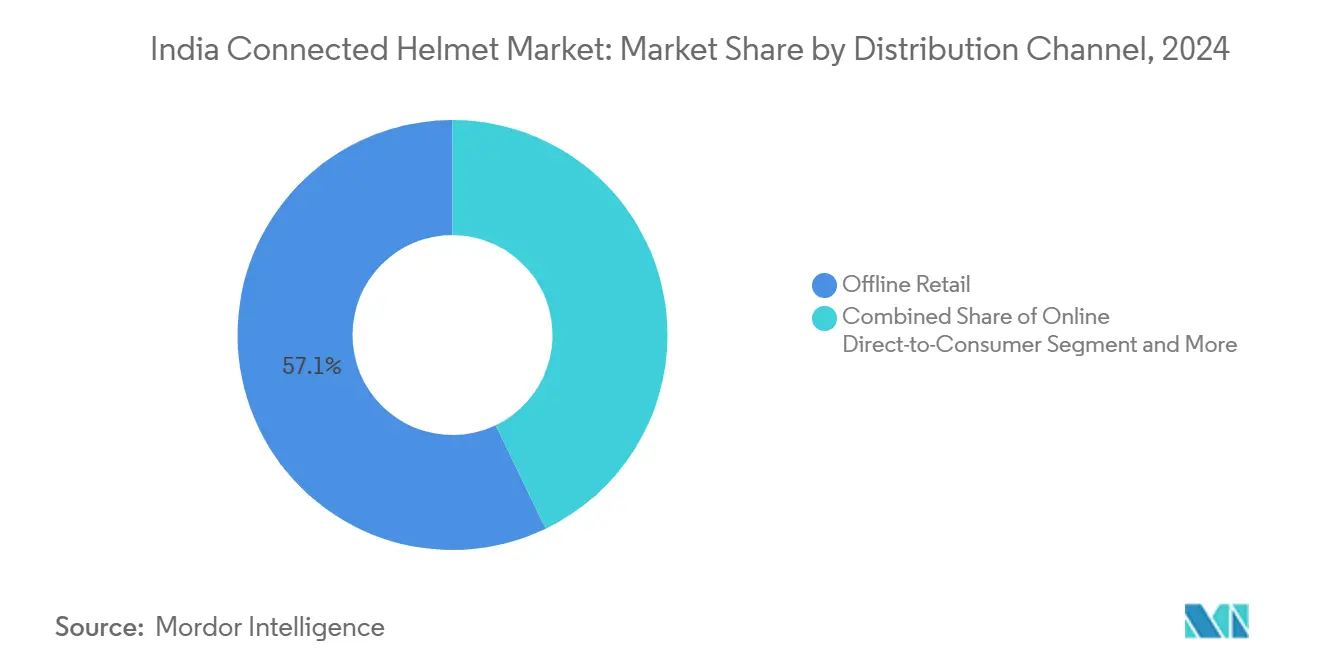

- By distribution channel, offline retail accounted for 57.13% of the Indian connected helmet market size in 2024, whereas online direct-to-consumer platforms are growing at a 27.65% CAGR over 2025-2030.

- By price range, economy models represented 47.51% of the Indian connected helmet market share in 2024; premium smart helmets are moving upward at a 22.16% CAGR through 2030.

Future direction is shaped by developments occurring across multiple countries and regions, with India contributing to the overall trajectory. The outlook on worldwide connected helmet market reflects how these are expected to evolve collectively.

India Connected Helmet Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Adoption of Motorcycle ADAS & HUD-Enabled Helmets | +12.5% | National, with early gains in South India, Maharashtra, Karnataka | Medium term (2-4 years) |

| Stringent BIS Safety-Standard Enforcement & Penalty Hikes | +8.7% | National, with stricter implementation in urban centers | Short term (≤ 2 years) |

| Growth In Mid-Premium Motorcycle Sales | +6.2% | National, concentrated in Tier-I and Tier-II cities | Medium term (2-4 years) |

| Integration of V2X Chips Enabling Group-Ride Networks | +4.8% | Urban corridors, highway networks, major metropolitan areas | Long term (≥ 4 years) |

| Expansion of Direct-to-Consumer E-Commerce Channels | +3.9% | National, with higher penetration in urban markets | Short term (≤ 2 years) |

| Insurance-Premium Discounts for Verified Connected-Helmet Use | +2.1% | National, pilot programs in select states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Motorcycle ADAS & HUD-Enabled Helmets

Manufacturers are turning the helmet into a rolling IoT node that offers a 240-degree field of view, blind-spot alerts, and crash-notification services. Field testing by Indian Institutes of Technology confirms high accuracy for edge-AI crash detection, proving the technology’s local relevance. As battery runtimes exceed 16 hours in models such as BluArmor’s C30, usability constraints that once deterred long-haul riders are receding[1]“FAQ C30,” BluArmor, thebluarmor.com. The premium use case filters into entry-level offerings, accelerating mainstream uptake of the smart motorcycle helmet market.

Stringent BIS Safety-Standard Enforcement & Penalty Hikes

Federal rules now require every new two-wheeler sale to include two ISI-certified helmets and impose fines plus potential license suspension for non-compliance. Insurers can reject claims when riders ignore helmet laws, prompting consumers to prioritize compliant and connected options that document usage[2]“Helmet Laws in India,” Bajaj Allianz, bajajallianz.com. Producers capable of meeting Bureau of Indian Standards audits quickly are best positioned to capture share, reinforcing the leadership of established Indian brands inside the connected helmet market.

Growth in Mid-Premium Motorcycle Sales

Sales of 150-400 cc motorcycles and electric scooters are climbing, creating rider segments willing to pay for comfort, style, and integrated electronics. Higher-powered bikes raise perceived risk, nudging owners toward helmets that bundle communication, navigation, and crash-mitigation features. Motorcycle firms such as TVS Motor amplify demand by prominently featuring smart helmets in showrooms and digital storefronts. The result is a feedback loop where rising bike ASPs drive accessory upgrades, propelling the smart motorcycle helmet market.

Integration of V2X Chips Enabling Group-Ride Networks

Maruti Suzuki and IIT-Hyderabad have validated India-specific V2X stacks capable of warning riders about sudden braking vehicles and intersection hazards. The Connected Motorcycle Consortium is standardizing protocols that embed two-wheelers into broader cooperative-intelligent transport systems. Smart helmets with onboard DSRC or C-V2X radios can deliver these alerts in real time without relying on the motorcycle’s electronics, giving aftermarket brands a platform edge within the connected helmet market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Upfront Cost Versus Conventional ISI Models | -4.30% | National, more pronounced in rural and Tier-III markets | Short term (≤ 2 years) |

| Limited Battery Life for Long-Distance Touring Riders | -2.80% | National highways, touring routes, rural connectivity corridors | Medium term (2-4 years) |

| Patchy 4G/5G Coverage on Tier-II/III Highways | -2.10% | Rural highways, remote touring destinations, border regions | Medium term (2-4 years) |

| Cultural Discomfort with Full-Face Smart-Helmet Form Factor | -1.60% | Rural markets, traditional user segments, hot climate regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional ISI Models

A basic ISI-approved unit sells for INR 500-2,000, whereas current smart models start near INR 5,000, a noticeable delta for riders earning under INR 25,000 monthly. Producers are responding with stripped-down SKUs, Bluetooth intercom, crash detection, and navigation prompts, but no HUD, which helps seed the entry segment of the smart motorcycle helmet market.

Patchy 4G/5G Coverage on Tier-II/Tier-III Highways

Crash-alert services dependent on cellular networks lose effectiveness on several of India’s national highways that still lack reliable 4G coverage. To cope, helmets are embedding store-and-forward data buffers that auto-dispatch SMS alerts once the signal returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robust Full-Face Adoption Underpins Feature Integration

Full-face designs held 44.56% of the Indian connected helmet market share in 2024, capitalizing on their larger shell volumes that house batteries, cameras, and HUD optics without compromising weight balance. Smart-HUD-integrated variants sprint at a 28.40% CAGR because riders value navigation arrows, speed readouts, and blind-spot visuals delivered directly in line of sight. The smart motorcycle helmet market size for modular shells is expanding as touring enthusiasts favor chin-bar flip convenience. Half-shell adoption slips as enforcement tightens and injury studies confirm poor lateral-impact performance.

Superior protection data bolsters the acceptance of full-face smart helmets. Side-impact crash analytics reveal a substantially lower fatality risk versus half-shells, amplifying consumer willingness to pay for technology that further shrinks hazard exposure. OEMs exploit this synergy: once riders upgrade for safety, they become receptive to bundled electronics, reinforcing volume scale in the smart motorcycle helmet market.

By Technology Level: Bluetooth Foundation Catalyzes Multi-Sensor Suites

Bluetooth-only units dominated 39.28% of the Indian connected helmet market size in 2024, offering music, call handling, and basic intercom at affordable price points. ADAS sensor-suite helmets are marching forward at a 32.48% CAGR as radar, ultrasonic, and camera modules attract a competitive price. The smart motorcycle helmet market size for multi-feature “all-in-one” models, ADAS, HUD, mesh comms, will likely surpass Bluetooth-only volumes in the coming years. Edge AI chips now detect collision vectors locally, easing dependence on cloud latency while keeping power draw within practical limits.

Mesh communication networks extend rider-to-rider range and self-heal when a participant drops out, a key differentiator from legacy Bluetooth daisy chains. Such capabilities bring group-ride safety to mainstream price bands, helping the smart motorcycle helmet market overstep early-adopter niches.

By End User: Individual Riders Remain Core While Fleet Demand Scales

Private owners represented 71.88% of the 2024 Indian connected helmet market size, owing to the country's commuter-centric two-wheeler culture. Delivery fleets, however, are projected to register a 21.94% CAGR to 2030 as e-commerce logistics seek telematics to curb accident downtime and negotiate lower insurance premiums. Large food-delivery platforms are already trialing bulk orders with geo-fencing features that log helmet usage per rider shift. This institutional pull complements grassroots consumer demand, broadening the smart motorcycle helmet market footprint.

Pillion-specific sub-models, lighter and with adjustable in-shell LEDs for visibility, are gaining attention after regulators clarified that passengers must wear certified helmets. Dual-pack bundles thus present an incremental revenue lever for brands.

By Distribution Channel: Digital Acceleration Challenges Showroom Dominance

Brick-and-mortar outlets (Offline Retail) still accounted for 57.13% of the Indian connected helmet market share in 2024, reflecting consumer preference for physical fit checks. Yet online direct-to-consumer portals are clocking 27.65% CAGR, fueled by easy returns, EMI payment plans, and flash-upgrade firmware over Wi-Fi. Some motorcycle OEMs now bundle helmets at the point of bike purchase or offer QR codes that route buyers to brand web stores, integrating the smart motorcycle helmet market into broader after-sales ecosystems.

Virtual-try-on utilities employing a phone camera to map head circumference to millimeter accuracy mitigate the “fit fear” that once deterred e-commerce sales. Higher basket values online offset free-shipping costs, validating omnichannel economics for helmet makers.

By Price Range: Entry Tiers Seed Demand, Premium Lines Lift Margins

Economy smart helmets absorbed 47.51% of the 2024 Indian connected helmet market size, proving that connectivity alone can sway mass-market buyers when priced under INR 4,500. Premium lines above INR 10,000 are racing at 22.16% CAGR because affluent urban riders crave HUDs, voice assistants, and carbon-fiber shells for weight reduction. Many brands adopt a laddered portfolio: start with economy SKUs to lock in users, then upsell through app notifications when higher-spec models launch. The technique stabilizes recurring revenue in the smart motorcycle helmet market without alienating price-sensitive segments.

Geography Analysis

South India Leads While North-East Surges

South India’s dominance stems from more vigorous traffic-law enforcement, higher education levels, and proximity to manufacturing clusters in Tamil Nadu and Karnataka, which lower logistics costs and speed up service support. Government road-safety campaigns televised in Malayalam, Tamil, and Kannada further normalize daily helmet use, lifting the baseline from which smart upgrades occur. Academic outreach programs at institutes such as IIT-Madras showcase prototype HUD systems, familiarizing tech-savvy youth with premium features that quickly migrate into commercial models.

Urban clusters in the West and North remain pivotal revenue pools, while East and Central zones show steady gains as smartphone penetration broadens. Brands are customizing colorways and visor tints to suit regional climate and cultural tastes, demonstrating localization’s role in this geographically diverse smart motorcycle helmet market.

Analysis of the connected helmet market by Mordor Intelligence spans multiple other regional evaluations across Europe, supported by country-level insights for China, Japan, South Korea, and United States, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The market remains moderately concentrated. Studds's, one of the leading players, scale enables aggressive entry pricing for Bluetooth models that seed the mid-range. Domestic rival Steelbird is pivoting from mass polycarbonate shells to feature-rich carbon composites. Electronics-first challengers like BluArmor leverage software DNA to introduce mesh networking, over-the-air firmware, and subscription-based navigation upgrades.

Foreign entrants, including HJC and Arai, position at the super-premium end, highlighting international safety certifications plus app-level integration with global ride-tracking platforms. Their import duties inflate retail tags, but aspirational buyers still perceive brand cachet. Meanwhile, mobility-tech start-ups are applying automotive supply-chain economics to the helmet segment, outsourcing shell molding while retaining IP on AI and cloud analytics. Patent filings for embedded radar mounts, battery-swappable cheek pads, and adaptive-tint electrochromic visors grew year-over-year in 2024, signaling an innovation arms race as the smart motorcycle helmet market matures.

Strategic alliances are rising. Allianz Partners paired Cosmo Connected to pair Personal Accident Insurance with IoT helmets, creating a bundled safety-finance product that could pressure rivals to secure similar tie-ups. Motorcycle OEMs are exploring showroom co-branding, seeing helmet connectivity as an extension of vehicle telematics. The intersection of hardware, software, and insurance is defining new battlegrounds that will shape the pace of consolidation over the next five years.

India Connected Helmet Industry Leaders

Studds Accessories Limited

Steelbird Hi-Tech India Ltd.

Vega Auto Accessories Limited

JMD Helmets Pvt. Ltd.

LIVALL Riding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: STUDDS Accessories Ltd. collaborated with Warner Bros. Discovery Global Consumer Products India to launch the Batman Edition Drifter Helmet in India. It meets both ISI and DOT safety standards, incorporating a high-impact outer shell for shock resistance and a regulated-density EPS liner for enhanced impact absorption.

- March 2025: The Ministry of Road Transport mandates two ISI-certified helmets with every new bike, immediately boosting baseline volumes for compliant manufacturers.

- December 2024: Steelbird Hi-tech India announced its plan to establish a new manufacturing facility in Hosur, Tamil Nadu. The company committed an initial investment of INR 100 crore (USD 11.5 million) and plans to increase the total investment to INR 250 crore (USD 28.5 million). The plant will employ approximately 2,000 workers and produce 20,000 helmets per day.

India Connected Helmet Market Report Scope

| Full Face |

| Modular / Flip-up |

| Open Face |

| Half Helmet |

| Off-road / Motocross |

| Smart HUD-Integrated |

| Bluetooth-Only |

| Integrated Audio / Comms |

| HUD / AR Display |

| Crash Detection & eCall |

| ADAS Sensor Suite |

| Multi-Feature (All-in-One) |

| Individual Rider |

| Passenger |

| Fleet / Delivery |

| Offline Retail |

| Online Direct-to-Consumer |

| OEM Accessory Bundles |

| Economy |

| Mid-Range |

| Premium |

| By Product Type | Full Face |

| Modular / Flip-up | |

| Open Face | |

| Half Helmet | |

| Off-road / Motocross | |

| Smart HUD-Integrated | |

| By Technology Level | Bluetooth-Only |

| Integrated Audio / Comms | |

| HUD / AR Display | |

| Crash Detection & eCall | |

| ADAS Sensor Suite | |

| Multi-Feature (All-in-One) | |

| By End User | Individual Rider |

| Passenger | |

| Fleet / Delivery | |

| By Distribution Channel | Offline Retail |

| Online Direct-to-Consumer | |

| OEM Accessory Bundles | |

| By Price Range | Economy |

| Mid-Range | |

| Premium |

Key Questions Answered in the Report

How large will the connected helmet market be in India by 2030?

The connected helmet market size is projected to reach about USD 20.73 million by 2030, reflecting a 39.28% CAGR from 2025.

Which technology segment is growing fastest within helmets?

ADAS sensor-suite models are expanding at a 32.48% CAGR as riders prioritize collision-warning and crash-alert features.

Why does South India lead national sales?

Higher enforcement of helmet laws, a strong manufacturing base, and tech-savvy consumers give South India a 33.67% revenue share.

How are delivery fleets influencing demand?

Logistics firms adopting telematics-enabled helmets to lower insurance costs are driving a 21.94% CAGR in fleet purchases through 2030.

What remains the main barrier to adoption?

Upfront cost relative to basic ISI models remains the biggest restraint, especially in price-sensitive rural areas.

Are insurance discounts available for connected helmets?

Pilot programs in select states offer premium reductions when verified usage data confirms helmet compliance during rides.

Page last updated on: