Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

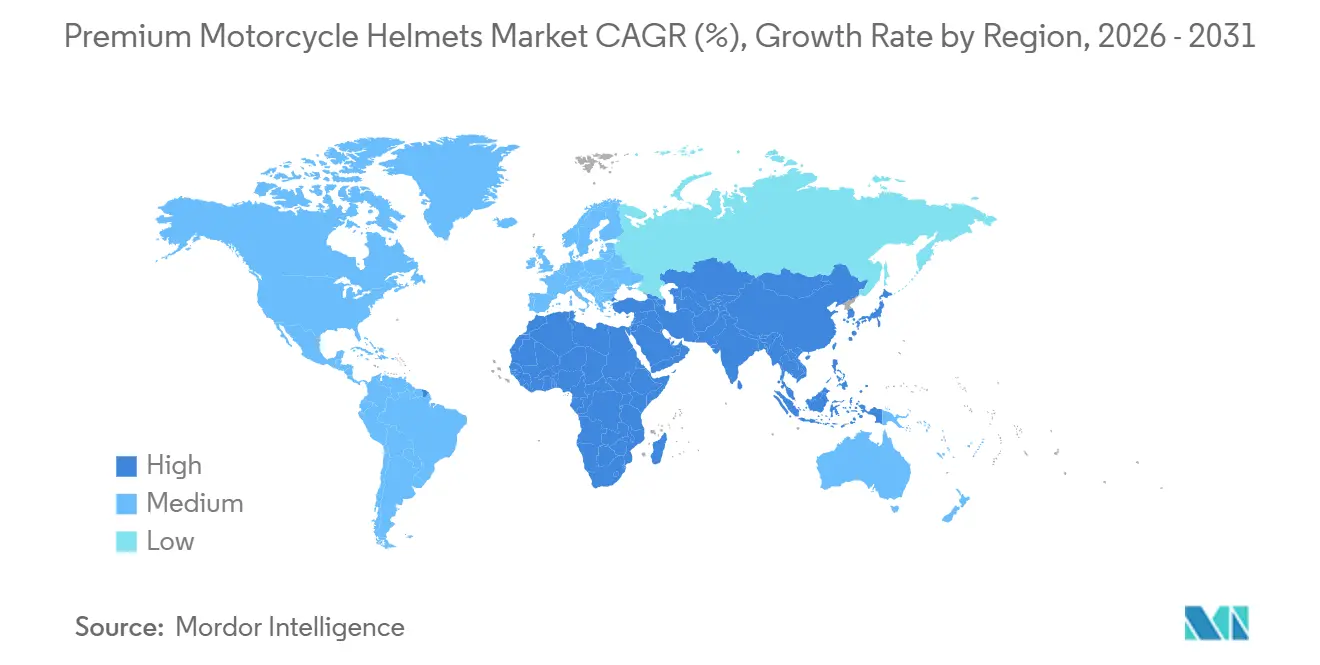

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Premium Motorcycle Helmets Market Analysis by Mordor Intelligence

The premium motorcycle helmets market size is expected to grow from USD 0.97 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 1.33 billion by 2031 at a 5.45% CAGR over 2026–2031. Regulatory upgrades, rapid material-science advances, and electronics integration are shortening product cycles while opening higher-margin niches. ECE 22.06 enforcement in Europe and homologation rules for circuit racing have eliminated legacy inventory and driven fresh tooling investment. Carbon-fiber shells trimmed weight by up to 30%, which made it possible to embed Bluetooth and heads-up displays without breaching comfort thresholds. Asia-Pacific demand is accelerating as disposable income rises and insurance discounts reward certified gear. Brands are defending share with vertically integrated production and near-shore facilities that buffer freight volatility. Institutional confidence is also visible: Liberty Media’s USD 4.5 billion acquisition of MotoGP strengthens the content-commerce loop that converts spectators into premium-gear customers[1]BUSINESS WIRE, "Liberty Media Corporation Completes Acquisition of MotoGP™", Liberty Media Corporation, libertymedia.com.

Key Report Takeaways

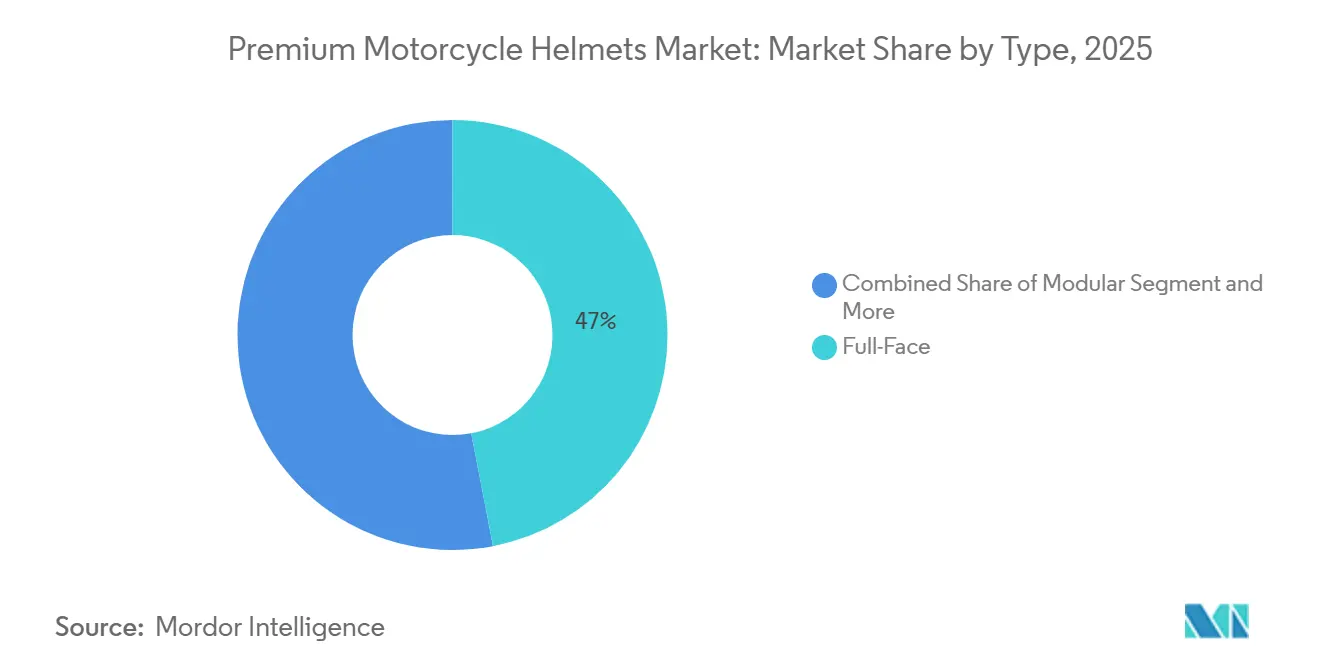

- By helmet type, full-face accounted for 46.98% revenue share in 2025; adventure/dual-sport variants are projected to grow fastest at 7.83% CAGR through 2031.

- By material type, fiberglass led with 34.72% of the Premium Motorcycle Helmets market size in 2025, while carbon fiber is forecasted to expand at a 5.98% CAGR through 2031.

- By application, street-riding helmets held a 57.83% share in 2025; track-racing models are growing fastest at a 6.78% CAGR through 2031.

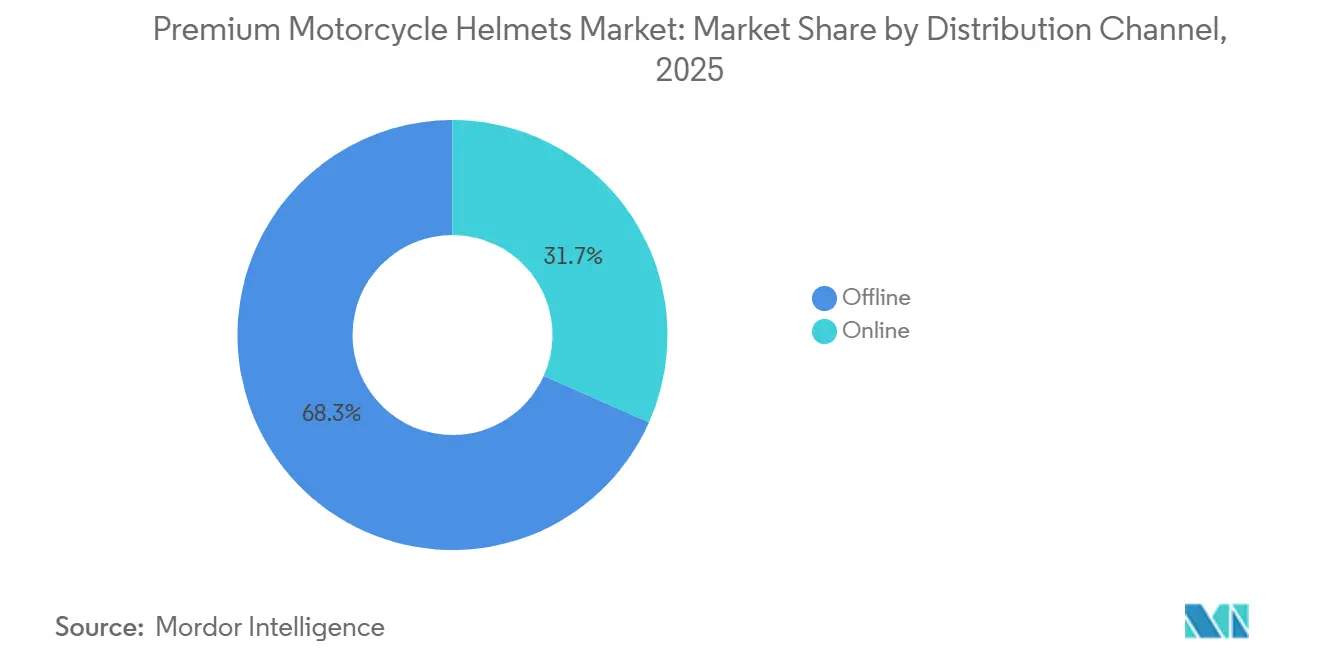

- By distribution channel, offline networks captured 68.34% of the 2025 size, whereas online sales are expected to advance at a 6.51% CAGR across the forecast period (2026-2031).

- By end-user, commuters dominated with 62.25 % of the Premium Motorcycle Helmets market size in 2025, while racers and track-day riders are projected to post the highest 6.86 % CAGR through 2031.

- By geography, Asia-Pacific commanded 38.81% share of the market in 2025 and is expected to post a 6.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Premium Motorcycle Helmets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Safety Regulations | +1.8% | Global, with early enforcement in Europe, North America, and India | Medium term (2-4 years) |

| Technological Integration | +1.3% | North America, Europe, and premium segments in Asia-Pacific | Medium term (2-4 years) |

| Rising Incomes and Superbike Adoption | +1.1% | Asia-Pacific core, with spillover to Middle East and South America | Long term (≥ 4 years) |

| Lightweight Carbon-Fiber Composites | +0.9% | Global, concentrated in Europe and North America premium segments | Long term (≥ 4 years) |

| Insurance-Linked Telematics Discounts | +0.5% | North America, Europe, and South Africa pilot programs | Long term (≥ 4 years) |

| Near-Shoring of Premium-Helmet Manufacturing | +0.4% | North America and Europe, with selective reshoring from Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Safety Regulations

New test matrices under ECE 22.06 require oblique-impact trials at higher velocities and double the number of strike points, rendering legacy molds obsolete and forcing multi-region labs to front-load R&D. Circuit racing homologation (FRHPhe-02), effective January 2026, caps rotational acceleration, compelling brands to design separate shells for track and street[2]"More helmets - FIM homologated under FRHPhe-02", FIM, fim-moto.com. India’s tropical-climate ventilation rules further regionalize geometry, while Snell M2025R aligns helmet metrics with concussion thresholds used in professional football. The cumulative requirements raise certification outlays but create durable entry barriers that favor incumbents.

Technological Integration (Bluetooth, HUD)

Bluetooth intercoms and heads-up displays have migrated from bulky aftermarket kits to fully embedded modules that add under 50 grams. A 2025 production run of Schuberth’s C5 integrates Cardo’s SC-EDGE unit within the shell, cutting wind noise by 4 dB and removing exposed brackets that previously deterred premium buyers. Component commoditization has compressed the connectivity premiums, allowing mass-market brands to standardize basic communication while ultra-premium labels maintain analog positioning. Early adopters create halo demand, but widespread uptake will hinge on warranty assurances that electronics will not compromise impact integrity.

Rising Disposable Incomes & Superbike Uptake

Middle-class expansion across Asia-Pacific redefines safety gear as a status symbol rather than a legal formality. Above-150 cc motorcycles now account for nearly one-quarter of regional two-wheeler sales, creating tailwinds for premium full-face and modular models priced above USD 300. Delivery-bike fleet growth in Western Asia and burgeoning adventure-touring culture in South America further widen the addressable pool for certified helmets.

Shift Toward Lightweight Carbon-Fiber Composites

Thermoplastic-impregnated carbon tapes achieve up to 30% weight reduction while staying within the stricter ECE 22.06 thresholds. Single-step injection matrices now bond carbon, aramid, and fiberglass in six hours versus two-day lay-up cycles, lowering scrap and broadening the material mix. Supply risk persists because one country controls 95% of battery-grade graphite, and export curbs triggered a 45% price swing in 2024, pressuring mid-tier margins.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retail Prices | -0.8% | Asia-Pacific, South America, and Africa | Short term (≤ 2 years) |

| Counterfeit Products | -0.6% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Electronics Obsolescence & E-Waste Risk | -0.4% | Global, concentrated in Europe and North America | Long term (≥ 4 years) |

| Supply-Chain Volatility | -0.3% | Global, with acute impact on Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retail Prices in Emerging Markets

In many lower-income regions, authentic ECE-compliant helmets retail at USD 80–150, while non-certified look-alikes can be had for under USD 15. Tax structures such as a 28% goods-and-services levy on high-capacity bike accessories widen the affordability gap. Domestic makers are scaling mid-price ranges to reconcile safety and cost, but currency depreciation and import tariffs continue to skew buying toward polycarbonate shells.

Counterfeit Premium-Look Helmets

Fake certification labels and pirated graphics undermine brand equity and expose riders to higher injury risk. Enforcement actions have increased: multiple agencies now conduct roadside raids, seize counterfeit inventory, and issue criminal penalties. Brands respond with NFC-enabled authenticity tags and blockchain logs, though uptake depends on consumer smartphone access. Elevated policing costs indirectly raise retail prices and dilute genuine product availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Helmet Type: Carbon Fiber Gains Despite Cost Premium

In 2025, full-face models captured 46.98% of sales, solidifying their dominance in the premium motorcycle helmet market, especially for sport-touring and track uses. Yet, as off-road tourism and overlanding gain traction, adventure and dual-sport helmet designs are set to surge at a 7.83% CAGR. New models for 2025 feature peak visors, goggle compatibility, and removable chin bars, striking a balance between enhanced ventilation and freeway aerodynamics. While touring riders gravitate towards modular flip-ups for their convenience, many are opting for lighter carbon-fiber alternatives, driven by the added weight of traditional hinges.

Regional preferences add layers of complexity to product offerings. North America leans heavily towards full-face sport shells, Europe finds a middle ground with both modular and full-face options, and a significant portion of Asia-Pacific continues to prefer open-face helmets for commuting. To navigate this complexity, brands are innovating by creating versatile shells that cater to both street and track standards. Take Shark’s Aeron, for instance: it's compliant with both ECE 22.06 and FIM 8859-2015 standards. This means dealers can stock a single SKU that seamlessly serves both racing enthusiasts and daily commuters, streamlining inventory management and enhancing perceived value.

By Material Type: Carbon Fiber Gains Despite Cost Premium

Fiberglass dominated the premium motorcycle helmet market, accounting for 34.72% of 2025 revenue. However, carbon-fiber units are projected to grow at a 5.98% CAGR through 2031. Owing to advancements like automated fiber placement and hybrid lay-ups, manufacturers are producing shells under 1,200 grams that still meet stringent dual ECE and FIM impact tests. HJC's 2024 F100 carbon, priced below EUR 700 (USD 760), is strategically positioned to undercut rival flagship models while maintaining healthy margins due to reduced labor content. While thermoplastic and ABS shells dominate entry-level price points, consumers in India and Indonesia are making a notable shift to composites, facilitated by financing plans that spread payments over twelve months.

Material selection is evolving beyond mere safety considerations, becoming a pivotal tool for brand positioning. Premium brands, for instance, emphasize hand-finished carbon weaves to justify price tags exceeding USD 800. In contrast, mid-tier brands are ingeniously blending glass and carbon, allowing them to penetrate lower price brackets without compromising on perceived performance. Liner technology is also witnessing advancements: crumple-zone polymers, which absorb approximately 30% more oblique impact energy, come at an incremental cost of USD 150. This price point, however, limits their use to adventure helmets, where buyers are willing to invest more for enhanced multi-impact resilience.

By Application: Track Racing Accelerates on New FIM Mandate

Street-riding accounted for 57.83% of demand in 2025 but will cede share to the track-racing category, projected to grow at 6.78% CAGR. The premium motorcycle helmets market size for circuit-specific lids swells as amateur motorsport enrollments rise and FRHPhe-02 certification becomes mandatory. Off-road designs preserve their niche with peak visors and enhanced ventilation important to motocross, yet they face limited crossover to on-road segments.

Club-racing growth amplifies replacement frequency—helmets must be retired after any major impact—boosting volume despite higher unit prices of USD 800–1,500. Street models, although commoditizing, remain essential in emerging economies where commuting dominates riding time. Off-road helmets maintain steady demand, protected by design features ill-suited for high-speed aerodynamics.

By Distribution Channel: Online Growth Tempered by Fit Barriers

In 2025, offline venues, such as brand showrooms, motorcycle dealers, and specialist retailers, drove 68.34% of total revenue. These traditional channels remain dominant due to their ability to provide hands-on experiences and personalized customer service. However, direct-to-consumer platforms are set to grow at a 6.51% CAGR, as brands seize the 30–40% margins that were once the domain of middlemen. The swift rise of Ruroc underscores a trend: younger riders are leaning towards visual differentiation and online peer validation, sidelining traditional narratives of craftsmanship. Social media platforms play a pivotal role in this shift, enabling brands to engage directly with their target audience and build strong online communities.

The market is witnessing the rise of hybrid purchasing pathways. Manufacturers are blending the best of both worlds, allowing customers to buy online and get fitted in-store. This approach not only enhances digital convenience but also ensures professional sizing, cutting down on return freight costs and strengthening ties with dealers. By integrating online and offline channels, brands can cater to a broader range of customer preferences while maintaining operational efficiency. During the forecast period, AI-driven shape-scanning apps hold promise, potentially offering the precision of in-person measurements. However, for widespread acceptance, challenges around trust and data privacy need addressing.

By End-User: Commuters Dominate, Racers Drive Premium Segment

In 2025, commuters accounted for 62.25% of spending, highlighting the significance of motorcycles as daily transport in densely populated Asian cities. These motorcycles have a replacement cycle of seven to ten years, as urban usage at low speeds rarely damages their EPS liners. This extended replacement cycle makes commuters a stable and consistent segment in the market. On the other hand, racers and track-day enthusiasts, projected to grow at 6.86% through 2031, replace their helmets every three to five years. They often invest over USD 800 for carbon-fiber shells, which proudly bear both FIM and ECE stamps, reflecting their preference for high-performance and safety-certified gear.

Brand collaborations are amplifying this demand among racers. A case in point: a 2024 initiative backed by Shoei provided premium helmets to newcomers at a track school. In return, these enrollees showcased the gear on their social media, highlighting the power of exposure and brand visibility in niche markets. Such collaborations not only drive sales but also strengthen brand loyalty among performance-focused consumers. Meanwhile, brands catering to commuters are responding by launching mid-range composite shells priced under USD 100. This strategy aims to attract aspirational customers desiring enhanced protection without the premium price tag of established brands, thereby expanding their reach in price-sensitive markets.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 38.81% of the market's value and is projected to grow at a CAGR of 6.49%. As salaries rise in India and Indonesia, there's a noticeable shift from scooters to motorcycles exceeding 150 cc. This shift has led to an increased demand for helmets that comply with both DOT and ECE standards. While China holds the title of the world's largest motorcycle producer, the attachment rate of premium helmets lags behind the global average. This discrepancy is largely due to inconsistent enforcement of helmet laws in rural areas. Events like Indonesia’s IMHAX draw significant crowds, yet sales predominantly fall below the USD 150 mark. This highlights a price sensitivity challenge that premium brands might address through financing options or local assembly.

North America is projected to grow at a CAGR of 3.02% until 2031. The growth is largely driven by Liberty Media’s strategic moves with MotoGP and the increasing attendance at MotoAmerica events. These factors have cultivated a track-day culture with a heightened demand for dual-certified helmets. Despite a global downturn in unit sales, Shoei’s North American revenue surged by 34.7% in fiscal 2024, underscoring the market's appreciation for perceived craftsmanship. Furthermore, Canada’s 2024 endorsement of the ECE 22.06 standard, in addition to DOT, has expanded brand options and lowered compliance costs for European manufacturers.

Europe is anticipated to witness a growth rate of 3.49% CAGR. The adoption of the ECE 22.06 standard is leveling the playing field, especially in rotational-impact testing, bridging the performance divide between premium and mid-tier brands. Leading Japanese manufacturers have adeptly navigated currency fluctuations, countering volume declines with price hikes, a testament to the strength of brand loyalty. As environmental policies gain traction, they are poised to influence purchasing decisions. This is especially true as extended-producer-responsibility regulations emphasize helmet recyclability. Currently, existing take-back initiatives manage only a small fraction of the millions of discarded units each year.

Competitive Landscape

The premium motorcycle helmet market remains moderately fragmented. The top three brands control under one-quarter of global revenue, leaving ample space for regional specialists and direct-to-consumer challengers. Incumbents defend margin through dealer networks that offer personalized fitting and post-sale services, an approach validated by Shoei’s 2024 revenue growth even as shipments fell. The company lifted list prices and benefited from yen weakness, illustrating buyers’ willingness to absorb cost inflation when craftsmanship is perceived as irreplaceable.

Emerging disruptors lean on social media and bold aesthetics. Ruroc’s Instagram-centric campaigns helped the brand reach significant unit sales by late-2024, capturing younger riders who rank design flair above heritage narratives. Technology partnerships are a second battleground: Schuberth’s deal with Cardo integrates intercom modules inside the shell, eliminating aftermarket brackets and wind-noise complaints, thereby differentiating on acoustic comfort rather than traditional safety metrics.

Regulatory convergence across ECE 22.06, DOT FMVSS 218, and Snell M2025 shrinks the technical performance delta, shifting competition toward fit, ventilation, and electronics. No manufacturer has yet committed large capex to subscription-based replacement or recyclable shell platforms, though pilot programs are underway. As such offerings mature, they may create new competitive dimensions that reward first movers with recurring revenue streams and sustainability credentials.

Premium Motorcycle Helmets Industry Leaders

-

AGV (Subsidiary of Dainese)

-

Shoei Co., Ltd

-

Schuberth GmbH

-

Arai Helmet Limited

-

Bell Helmets

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Studds, via its SMK brand, introduced Cygnus flip-back, Delta Tour, and Delta City helmets at EICMA 2025, featuring an EIRT shell and multi-density EPS liner.

- September 2025: Sena Technologies released the OUTRUSH 2 modular smart helmet with Mesh Intercom 3.0 and Wave Intercom, extending range and group connectivity.

- June 2025: BMW Motorrad unveiled the GS Rallye Carbon helmet with M-Forge™ carbon and integrated COM P1 GS communication module.

- April 2025: Reise Moto launched a BIS- and ECE 22.06-compliant helmet line in India under the Reise Moto brand.

Global Premium Motorcycle Helmets Market Report Scope

Premium motorcycle helmets refer to helmets made up of superior-quality materials, such as carbon fiber, fiberglass, plastics, and synthetic fibers, that provide high tensile strength and enhanced security to the rider of two-wheelers in case of an accident, collision, or crash. These helmets are also compatible with safety standards compared to other regular helmets.

The Premium Motorcycle Helmet Market report is segmented by material type, helmet type, application, distribution channel, end-user, and geography. By material type, the market is segmented into Fiberglass, Polycarbonate, Carbon Fiber, Kevlar, and Plastics. By helmet type, the market is segmented into Full-Face, Modular, Open-Face, and Half Helmets. By application, the market is segmented into Street Riding, Off-Road Riding, and Track Racing. By distribution channel, the market is segmented into Offline and Online. By end-user, the market is segmented into Commuters and Racers. By geography, the market is segmented into North America, Europe, South America, Asia-Pacific, and the Middle East and Africa. The market forecasts are provided in terms of value (USD) and volume (units).

By Type

| Full-Face Helmets |

| Modular Helmets |

| Open-Face Helmets |

| Half Helmets |

By Material

| Polycarbonate |

| Fiberglass |

| Carbon Fiber |

| Kevlar |

| Plastics / ABS |

By Application

| Street Riding |

| Off-Road Riding |

| Track Racing |

By Distribution Channel

| Offline (Retail Stores) |

| Online (E-commerce) |

By End-User

| Commuters |

| Racers |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Full-Face Helmets | |

| Modular Helmets | ||

| Open-Face Helmets | ||

| Half Helmets | ||

| By Material | Polycarbonate | |

| Fiberglass | ||

| Carbon Fiber | ||

| Kevlar | ||

| Plastics / ABS | ||

| By Application | Street Riding | |

| Off-Road Riding | ||

| Track Racing | ||

| By Distribution Channel | Offline (Retail Stores) | |

| Online (E-commerce) | ||

| By End-User | Commuters | |

| Racers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecasted value of the premium motorcycle helmet market in 2031?

The premium motorcycle helmet market is projected to reach USD 1.33 billion by 2031.

Which helmet type is expected to grow the fastest through 2031?

Adventure and dual-sport helmets are forecast to expand at a 7.83 % CAGR, outpacing all other types.

How quickly will online channels grow compared with offline outlets?

Online sales are anticipated to rise at a 6.51 % CAGR, while offline networks will grow more slowly due to fit-related barriers.

Why is carbon fiber becoming more popular despite higher cost?

Automated production cuts labor expense, resulting in lighter shells that justify premium pricing and deliver a 5.98 % CAGR in carbon-fiber revenue.

Which region contributes the largest share of premium helmet revenue?

Asia-Pacific accounted for 38.81 % of global revenue in 2025 and maintains the fastest regional growth trajectory.

Page last updated on: