United States Chemical Warehousing And Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

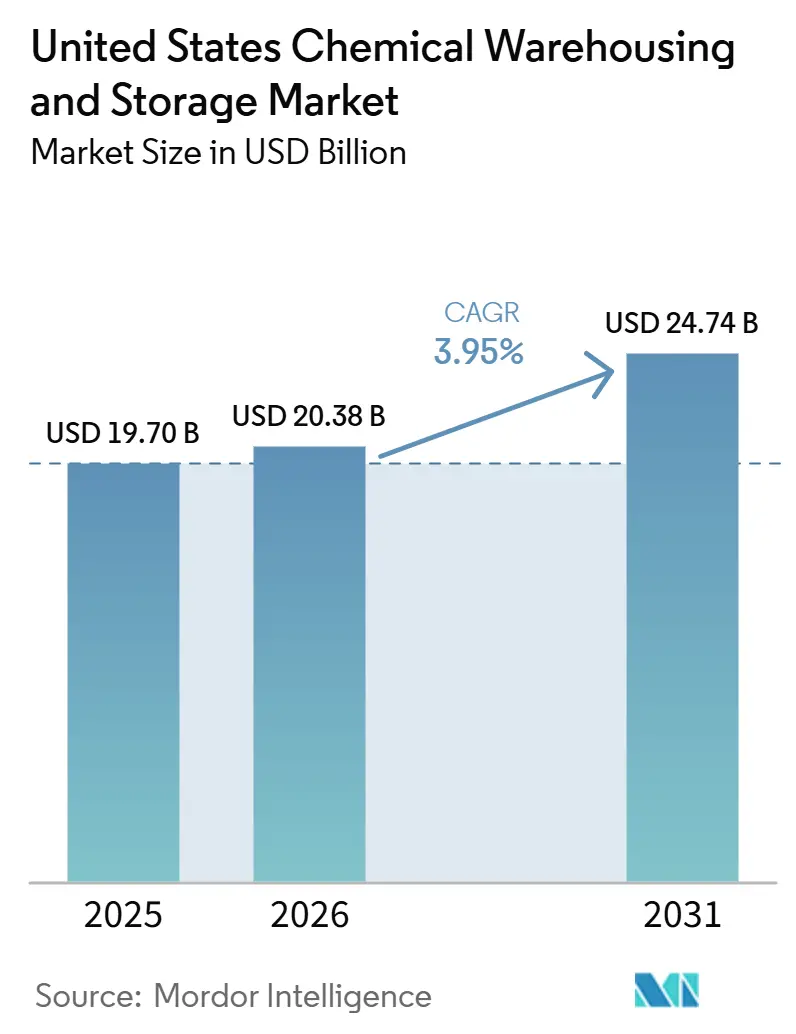

| Base Year Market Size (2025) | USD 19.70 Billion |

| Market Size (2026) | USD 20.38 Billion |

| Market Size (2031) | USD 24.74 Billion |

| Growth Rate (2026 - 2031) | 3.95% CAGR |

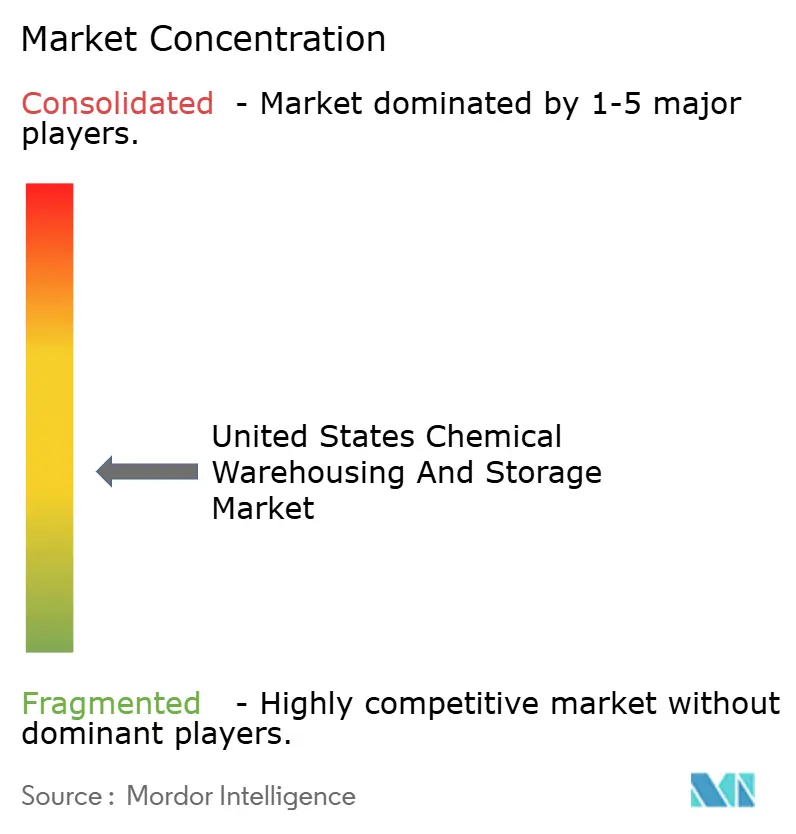

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Chemical Warehousing And Storage Market Analysis by Mordor Intelligence

The United States Chemical Warehousing And Storage Market size is expected to increase from USD 19.70 billion in 2025 to USD 20.38 billion in 2026 and reach USD 24.74 billion by 2031, growing at a CAGR of 3.95% over 2026-2031.

Storage demand continues to track Gulf Coast petrochemical buildouts and export terminal expansions, while temperature-controlled capacity rises with new biologics and specialty drug launches that require validated cold rooms and continuous monitoring. Project pipelines on the Texas and Louisiana coasts expand the addressable base for hazmat-compliant sites that can segregate flammables, corrosives, and oxidizers under one roof. Compliance updates under OSHA’s Hazard Communication Standard and EPA Tier II reporting reinforced capital upgrades and documented protocols that favor well-capitalized operators. Logistics firms invest in automation, AI-enabled visibility, and intrinsically safe systems to offset labor gaps and insurance costs while sustaining rent premiums above general-purpose industrial space.

Key Report Takeaways

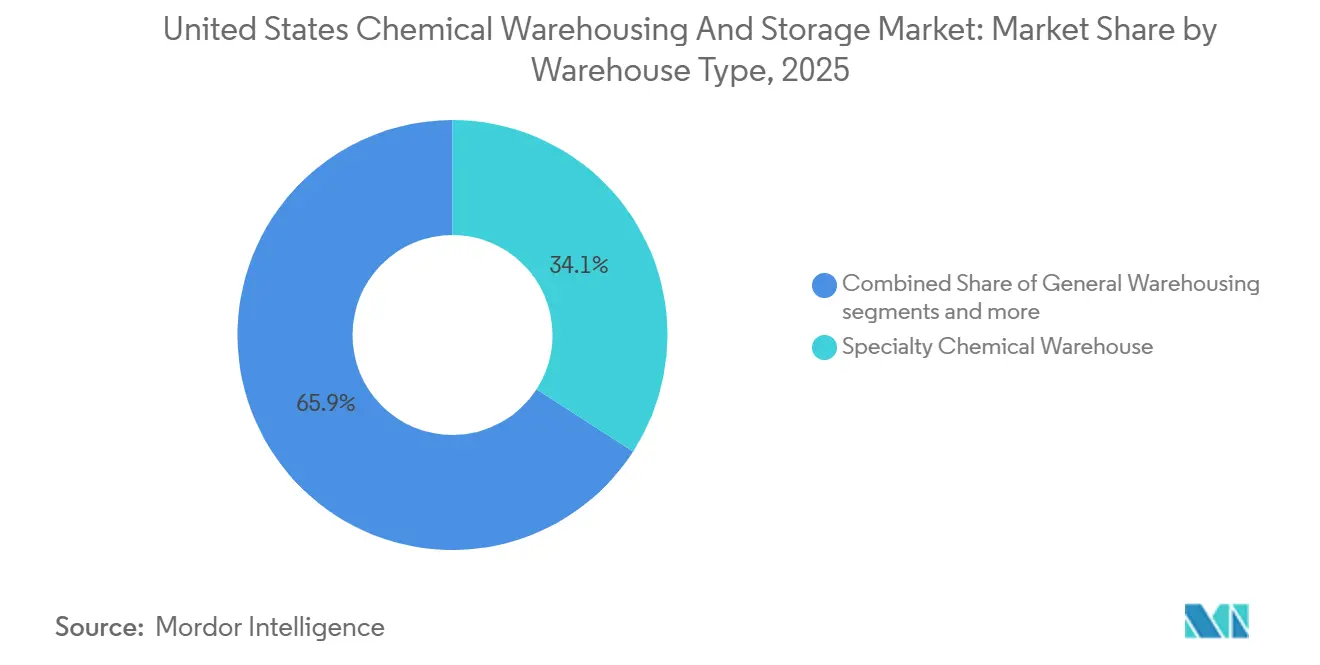

- By warehouse type, specialty chemical warehouses led with 34.12% of the United States chemical warehousing and storage market share in 2025, while temperature-controlled warehouses are projected to expand at a 4.7% CAGR through 2031.

- By chemical type, flammable liquids accounted for 40.78% of the United States chemical warehousing and storage market size in 2025, and toxic substances are forecast to grow at a 5.1% CAGR through 2031.

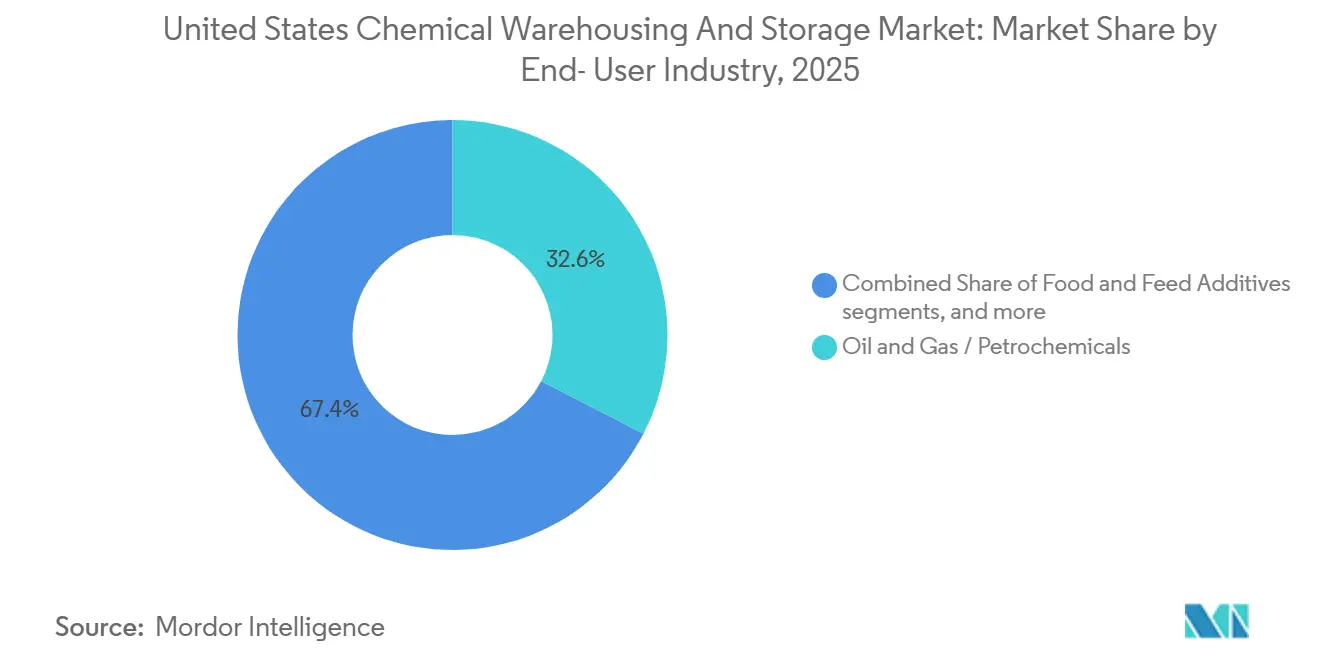

- By end-user industry, oil and gas or petrochemicals held 32.60% of the United States chemical warehousing and storage market share in 2025, while pharmaceuticals and life sciences are set to grow at a 4.3% CAGR to 2031.

- By region, the Midwest captured 26.12% market size in 2025, and the Southeast is poised for a 5.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Chemical Warehousing And Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shale Gas Boom and Petrochemical Renaissance | +1.4% | Gulf Coast core, spill-over to Midwest pipeline corridors | Medium term (2-4 years) |

| Nearshoring and Reshoring of Chemical Manufacturing | +0.8% | National, with early gains in Midwest auto clusters and Southeast pharma corridors | Long term (≥ 4 years) |

| Expansion of Gulf Coast Petrochemical Export Terminals | +0.9% | Texas and Louisiana coastal counties, Corpus Christi and Houston ship channels | Medium term (2-4 years) |

| Rising Specialty Chemicals Production Volumes | +0.7% | National, strongest in Northeast pharma hubs and Great Lakes advanced materials zones | Long term (≥ 4 years) |

| Outsourcing Trend Among Chemical Manufacturers | +0.6% | National, fastest adoption where ISO and GDP-certified 3PL infrastructure exists | Short term (≤ 2 years) |

| Growing Cross-Border Chemical Trade with Mexico and Canada | +0.7% | Texas border regions and Great Lakes USMCA corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shale Gas Boom and Petrochemical Renaissance

New and proposed Gulf Coast crackers anchor multi-year demand for hazmat-compliant storage near production centers and export corridors. Shintech’s USD 3.4 billion ethylene and chlor-alkali complex in Iberville Parish targets 2030 completion, and signals sustained feedstock-backed capacity growth in Louisiana[1]Ellie Brosnan, “Shintech Announces US$3.4 Billion at Louisiana Petrochemicals Complex,” Hydrocarbon Engineering, hydrocarbonengineering.com. ExxonMobil is evaluating an ethane cracker and polyethylene plant near Corpus Christi with a potential USD 8.6 billion capital plan, which, if approved, would expand staging needs for polymers and intermediates buildouts add further pull. Venture Global approved the USD 8.6 billion CP2 project in Cameron Parish, while Cheniere filed to add four Corpus Christi trains that would lift peak capacity by 24 mtpa. These energy megaprojects require adjacent storage of refrigerants, corrosion inhibitors, and specialty process chemicals under strict segregation with real-time inventory tracking. Export logistics reinforce the cycle, as Energy Transfer’s Flexport and Enterprise Products Partners’ expansions shape occupancy and just-in-time inventory strategies near Nederland and the Houston Ship Channel.

Nearshoring and Reshoring of Chemical Manufacturing

Pharmaceutical and specialty chemical investments increase demand for temperature-controlled storage and validated quality systems close to the United States manufacturing lines. Corporate plans disclosed by leading pharma manufacturers highlight expanded active pharmaceutical ingredients and injectable therapy capacity that will rely on GDP-compliant warehousing and 21 CFR Part 11-validated monitoring. Distributor investments mirror this shift, as Cencora committed USD 1 billion through 2030 across national hubs, including a West Coast expansion and a cold-chain scale-up at Dothan, Alabama, to meet the rise in products that need 2-to-8 degree Celsius storage. Network consolidation also supports reshoring, with DSV completing the DB Schenker acquisition in 2025, enhancing cross-regional warehousing reach and standardization. Regional operators add value-added services such as trailer wash and maintenance at ports to reduce cycle times for liquid-bulk assets, reinforcing the United States chemical warehousing and storage market as nearshoring advances.

Expansion of Gulf Coast Petrochemical Export Terminals

Corpus Christi and Houston upgrades expand LPG and LNG throughput and reshape the profile of nearby hazmat storage. Cheniere’s Corpus Christi application covers four new trains and supports pipeline and compressor infrastructure, lifting peak LNG capacity by 24 mtpa and increasing the need for specialty chemical staging compliant with maritime codes. Energy Transfer’s Nederland expansions and Enterprise Products Partners’ refrigeration additions target propane, butane, and ethane flexibility, with the combined projects influencing FOB pricing dynamics and warehouse strategies. Operators at these hubs deploy intrinsically safe equipment, bunded containment, and foam-deluge systems to meet NFPA and insurer expectations. Increased export agility demands warehouse management systems that generate customs documents in real time and support rapid destination changes with audit trails to keep dwell times low. Coverage caps for sudden-spillage risk can hinge on documented impairment testing and compliant infrastructure, reinforcing capital intensity near terminals.[2]“2026 Preview: Tariffs, New Export Capacity Weaken Gulf Coast FOB Propane Prices,” OPIS, opis.com

Rising Specialty Chemicals Production Volumes

Specialty output trends favor secure, segregated warehousing with clean handling and validated procedures. Industry data show specialty volumes improved in 2025, while the 2026 outlook remains balanced, making inventory velocity, quality systems, and flexible capacity more important than raw tonnage alone. Circular feedstocks are expanding, with initiatives such as LyondellBasell’s MoReTec process planning updates that require new segregation and chain-of-custody verifications for recycled streams. Storage providers adapt to renewable and bio-based inputs with stainless-steel tanks, vapor-control, and recovery systems designed for sensitive chemistries. As product mixes shift toward higher-value formulations, sites invest in clean staging, drum sampling controls, and continuous monitoring to reduce contamination and raise audit readiness. These dynamics support premium pricing for well-specified facilities in the United States chemical warehousing and storage market that can integrate safety, quality, and reliability at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment for Hazmat-Compliant Facilities | -0.5% | National, with acute pressure near Gulf Coast and aging Midwest sites | Medium term (2-4 years) |

| Acute Shortage of Trained Hazardous Material Handlers | -0.4% | National, most severe in high-growth Southeast corridors and remote depots | Short term (≤ 2 years) |

| Escalating Insurance and Liability Premiums | -0.3% | National, concentrated in high-risk coastal facilities | Medium term (2-4 years) |

| Land Scarcity Near Major Port and Rail Terminals | -0.2% | Texas and Louisiana ports, Northeast port zones, Great Lakes intermodal hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment for Hazmat-Compliant Facilities

Upgrading or building hazmat-ready warehouses requires significant capital for 120-minute fire-rated construction, segregated bunded zones, and foam-deluge and vapor-control systems. Operators are also updating hazard communication and safety data sheets to align with OSHA’s 2024 final rule, which sets substance compliance by January 2026 and mixture compliance by July 2027. Economic impact assessments indicate one-time costs for file and label revisions and training, even as certain labeling changes reduce recurring compliance burdens. State and federal process changes, including e-Manifest use and record retention, add system and workflow workstreams that many sites integrate with quality management and WMS applications. Storage practices must meet EPA secondary-containment expectations, with adequate capacity and compatible materials for spills and stormwater, which drives site layout and capex plans. These obligations reinforce premium pricing for compliant sites in the United States chemical warehousing and storage market, where documented safety and inspection logs are essential for insurability and customer audits.

Acute Shortage of Trained Hazardous Material Handlers

Operators face persistent skills gaps, such as hazmat handling, process knowledge, regulatory fluency, and hands-on repetition. OSHA’s HAZWOPER and function-specific training requirements add initial coursework and annual refreshers that are foundational for safe operations but lengthen onboarding cycles. Providers respond by sponsoring structured training paths, including site-specific drills and role-based certifications, to raise competency and retention among full-time associates. Companies increase reliance on standard work, error-proofing, and digital checklists to reduce variance and maintain audit readiness across shifts and sites. Automation and AI augment labor where feasible, but many tasks, such as drum sampling or incompatible product segregation, still require trained staff oversight. Labor conditions remain a structural headwind for the United States chemical warehousing and storage market, tilting investments toward intrinsically safe automation where ROI thresholds can be met.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialty Facilities Anchor Market, Yet Temperature Control Posts Steepest Growth Curve

Specialty chemical warehouses led with 34.12% in 2025, reflecting purpose-built facilities with rated fire walls, segregated bunded zones, and intrinsically safe handling that allow flammables, corrosives, and oxidizers to be managed in a single site while maintaining compliance. Temperature-controlled warehouses post the fastest growth at a projected 4.8% CAGR to 2031 as life sciences launches require validated chillers, redundant power, and 21 CFR Part 11-validated data loggers. DHL’s million-square-foot healthcare hub in Annville is designed with GDP and GMP controls and Foreign Trade Zone status to align customs and tariff processes with time-sensitive pharma flows. Facilities that can blend safety, quality, and cold-chain reliability sustain rent premiums that exceed general industrial levels in the United States chemical warehousing and storage market.

Across the base, hazardous material warehouses combine enhanced ventilation, spill containment, and secondary containment plans with compatibility-controlled storage and routine drills. General chemical storage in shared sites continues to serve non-hazmat products and finished goods, but the fastest growth sits in temperature-controlled settings that pair automation with audit-ready documentation. Recent projects include EVERSANA’s Memphis distribution center using AI-enabled robotics and a new WMS to expand cold capacity while sustaining on-time delivery metrics. These patterns consolidate demand around multi-client nodes that can standardize hazard controls and quality systems at scale for the United States chemical warehousing and storage industry.

By Chemical Type: Flammables Dominate Tonnage, While Toxics Demand High-Specification Containment and Drive Fastest Expansion

Flammable liquids accounted for 40.78% in 2025, requiring NFPA-aligned suppression, vapor-control stacks, and explosion-proof electricals to manage solvents, distillates, and low-flash-point intermediates. Toxic substances are forecast to grow at 5.1% CAGR as operators add negative-pressure rooms, HEPA filtration, and continuous atmospheric monitoring for substances like hydrogen sulfide, ammonia, and chlorine. Warehouse practices tie back to OSHA’s updated hazard classification and labeling rules that now refine flammable gas categories and address chemicals under pressure. These controls reinforce premium requirements for audit-ready documentation and incident response in the United States chemical warehousing and storage industry.

Corrosives and oxidizers add further segregation complexity and call for materials and barriers that mitigate corrosion and ignition risk. Operators deploy WMS-integrated SDS data and compatibility matrices to prevent co-storage errors while automating alerts for putaway conflicts. Export-led flammable storage near Gulf terminals must also account for pressure-rated tanks, grounding, and flame arrestors, which align with terminal operating standards. As product portfolios add circular and renewable inputs, sites invest in stainless assets and recovery systems proven in European projects, now informing the United States designs.

By End-User Industry: Petrochemicals Lead Share, Pharma Growth Outpaces on Cold-Chain Imperatives

Oil and gas or petrochemicals held 32.60% in 2025 as integrated upstream-to-export chains cluster warehousing around Gulf Coast plants and terminals. Shintech’s Louisiana investment and ExxonMobil’s Texas evaluation highlight forward capacity that will require safe staging of monomers, additives, and specialty lubricants. LNG and NGL terminal expansions deepen throughput potential and expand the need for reliable, inspected storage aligned with maritime and insurer standards.

Pharmaceuticals and life sciences are set to grow at a 4.3% CAGR through 2031 as advanced therapies demand cGMP-compliant, temperature-controlled nodes with redundancy and traceability. Distributors and 3PLs add automation, validated monitoring, and Foreign Trade Zone capabilities to reduce delays and control tariff exposure for high-value shipments. Specialty and basic chemicals continue to rely on shared sites, but elevated specification and documentation needs push growth toward facilities that centralize OSHA and EPA compliance under unified quality systems.

Geography Analysis

The Midwest captured 26.12% in 2025 as Chicago’s intermodal role connects Great Lakes manufacturing to Gulf Coast feedstock flows and East Coast imports. Network consolidation following DSV’s acquisition increases coverage across cross-dock and shared warehousing in key corridors that support two-day delivery across automotive and advanced manufacturing belts. Circular feedstocks under evaluation could route recycled streams toward Midwest converters and hubs while staging near Gulf Coast crackers for final processing.

The Southeast is projected to grow at 5.8% CAGR through 2031, lifted by Gulf-linked capacity, state incentives, and shorter dwelling times at export terminals. Regional operators add maintenance and cleaning services for tank assets to cut turnarounds and support high-utilization lanes between plants and ports. Local expansions of compliant chemical storage increase alternatives to premium-priced sites closer to the Gulf while maintaining required segregation and monitoring standards.

The Northeast links European imports to domestic distribution and hosts key healthcare hubs that need temperature-controlled capacity at scale. Rinchem’s Bensalem site and the Port of Philadelphia’s refrigerated infrastructure illustrate how import flows tie into multi-tenant hazmat storage[3]“Rinchem | Chemical & Gas Warehouse | Bensalem, Pennsylvania,” Rinchem, rinchem.com. DHL’s Annville project adds a large healthcare node with FDA and GMP features and FTZ benefits, while Cencora’s investments bridge Midwestern and coastal networks. The Southwest concentrates near Texas ports, where LNG and NGL expansions increase the need for compliant storage tied to marine schedules and customs processes. USMCA flows keep cross-border volumes high, which supports bonded storage and bilingual documentation teams in Texas. The West anchors Asian inbound flows and continues to expand multi-client capacity that can integrate hazmat within broader campus configurations when permitted.

Competitive Landscape

Competition remains moderate, with leading 3PLs and distributors differentiating through safety processes, intrinsically safe systems, and predictive maintenance that reduce audit risk and downtime. DSV’s acquisition of DB Schenker in 2025 expands scale to around 160,000 employees, improving cross-regional standardization for firms seeking unified GDP and hazmat certifications across North America and Europe. DHL is investing in healthcare hubs in the Americas, including the Annville site, to address higher cold-chain volumes with validated storage and FTZ-enabled flows.

Mid-tier players compete with data-driven managed transportation, tank wash, and capacity solutions centered on liquid bulk and chemical lanes. Healthcare-focused 3PLs deploy AI-enabled robotics and new WMS platforms to scale controlled room temperature and cold storage while holding service levels steady. These investments support rent premiums across compliant space and shape bidding strategies in the United States chemical warehousing and storage market, where quality and safety evidence are decisive.

Global operators replicate best practices across regions for isocyanates and circular streams, which informs upgrades at the United States sites handling similar products. Storage offerings evolve as circular and renewable inputs gain share, with validated chain-of-custody controls integrated into WMS and quality systems. The United States chemical warehousing and storage market rewards operators that can unify safety, quality, and compliance across multi-client campuses at scale.

United States Chemical Warehousing And Storage Industry Leaders

DHL Group

Brenntag North America

Rhenus Logistics

BDP International

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Shintech Louisiana announced a USD 3.4 billion expansion of its Iberville Parish complex, including a second ethylene unit and additional chlor-alkali and VCM capacity, with first-phase completion expected by 2030 and 163 new direct jobs.

- March 2026: Venture Global reached a final investment decision and financing for the USD 8.6 billion CP2 LNG expansion in Cameron Parish, supported by global lenders to address tight LNG markets and high Gulf Coast utilization.

- February 2026: Cheniere filed to expand Corpus Christi LNG with four new large-scale trains, new pipeline looping, and compressor capacity, targeting a 2027 sanction while the facility runs at high utilization.

- January 2026: DHL Supply Chain unveiled a one-million-square-foot life sciences and healthcare distribution center in Annville, Pennsylvania, to open later in 2026 with FDA and GMP infrastructure, temperature control, FTZ status, and energy-efficient systems.

United States Chemical Warehousing And Storage Market Report Scope

The United States Chemical Warehousing and Storage Market Report is Segmented by Warehouse Type (General Warehousing, Speciality Chemical Warehouse, Hazardous Materials Warehouses, Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, Others), by End-user Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints Coatings & Adhesives, Food & Feed Additives, Oil & Gas / Petrochemicals, Others), and by Geography (Northeast, Midwest, Southeast, Southwest, West). The Market Forecasts are Provided in Terms of Value (USD Billion).

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others | |

| By Region - United States | Northeast |

| Midwest | |

| Southeast | |

| Southwest | |

| West |

Key Questions Answered in the Report

What is the size and growth outlook for the United States chemical warehousing and storage market through 2031?

The United States chemical warehousing and storage market size is expected to rise from USD 19.70 billion in 2025 to USD 20.38 billion in 2026 and reach USD 24.74 billion by 2031 at a 3.95% CAGR over 2026-2031.

Which warehouse type leads and which is growing fastest in the United States chemical warehousing and storage market?

Specialty warehouses lead with 34.12% in 2025, while temperature-controlled sites are projected to grow at 4.8% CAGR to 2031 as biologics and specialty drugs scale.

Which chemical categories shape storage design in the United States chemical warehousing and storage market?

Flammable liquids account for 40.78% market share in 2025, demanding NFPA-aligned suppression and vapor control, while toxics are the fastest growing and require negative-pressure rooms and continuous monitoring.

What end-user segments drive demand for chemical warehousing in the United States?

Oil and gas or petrochemicals lead with 32.60% share, while pharmaceuticals and life sciences grow at 4.3% CAGR as cGMP and cold-chain requirements expand.

Which regions are most important for capacity in the United States chemical warehousing and storage market?

The Midwest holds 26.12% on strong intermodal linkages, while the Southeast is set for 5.8% CAGR, helped by proximity to Gulf Coast capacity and export terminals.

What compliance areas are most influential for warehouse investment decisions?

OSHA’s Hazard Communication amendments, EPA Tier II reporting, and PHMSA oversight shape capex for fire-rated construction, bunded containment, and validated labeling and SDS controls, which also drive audit readiness.

Page last updated on: