North America Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

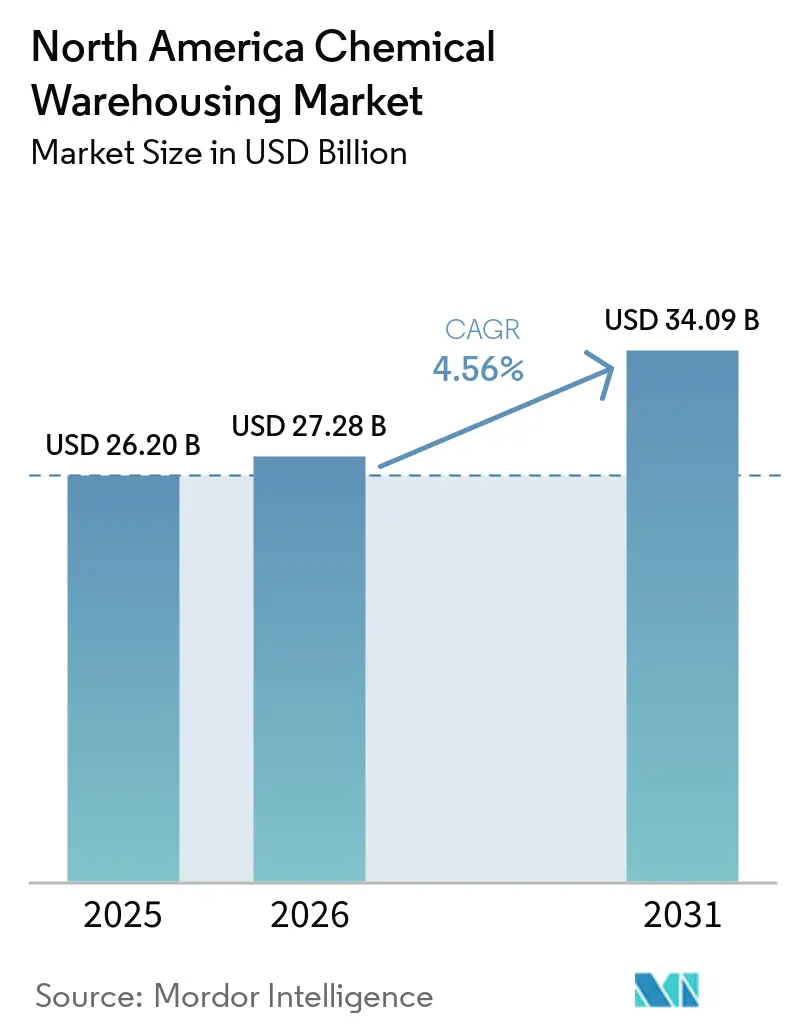

| Base Year Market Size (2025) | USD 26.20 Billion |

| Market Size (2026) | USD 27.28 Billion |

| Market Size (2031) | USD 34.09 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Chemical Warehousing Market Analysis by Mordor Intelligence

The North America chemical warehousing market size is projected to expand from USD 26.2 billion in 2025 and USD 27.28 billion in 2026 to USD 34.09 billion by 2031, registering a 4.56% CAGR between 2026 and 2031.

Rising demand for sustainability-certified storage, growth in battery-grade lithium compounds, and ongoing nearshoring into Northern Mexico are reshaping service requirements and facility locations across the North America chemical warehousing market. Operators are accelerating investments in temperature-controlled rooms, moisture-barrier zones, and AI-based safety analytics to secure high-margin contracts from pharmaceutical and electronics customers. Rail-served inland hubs near the Great Lakes and Mississippi River corridors continue to attract bulk-liquid tenants, while specialty chemical flows cluster around Gulf Coast deepwater ports. At the same time, stricter PFAS regulations and scarce hazmat-zoned land add cost pressure that favors incumbents with diversified portfolios and robust compliance records.

Key Report Takeaways

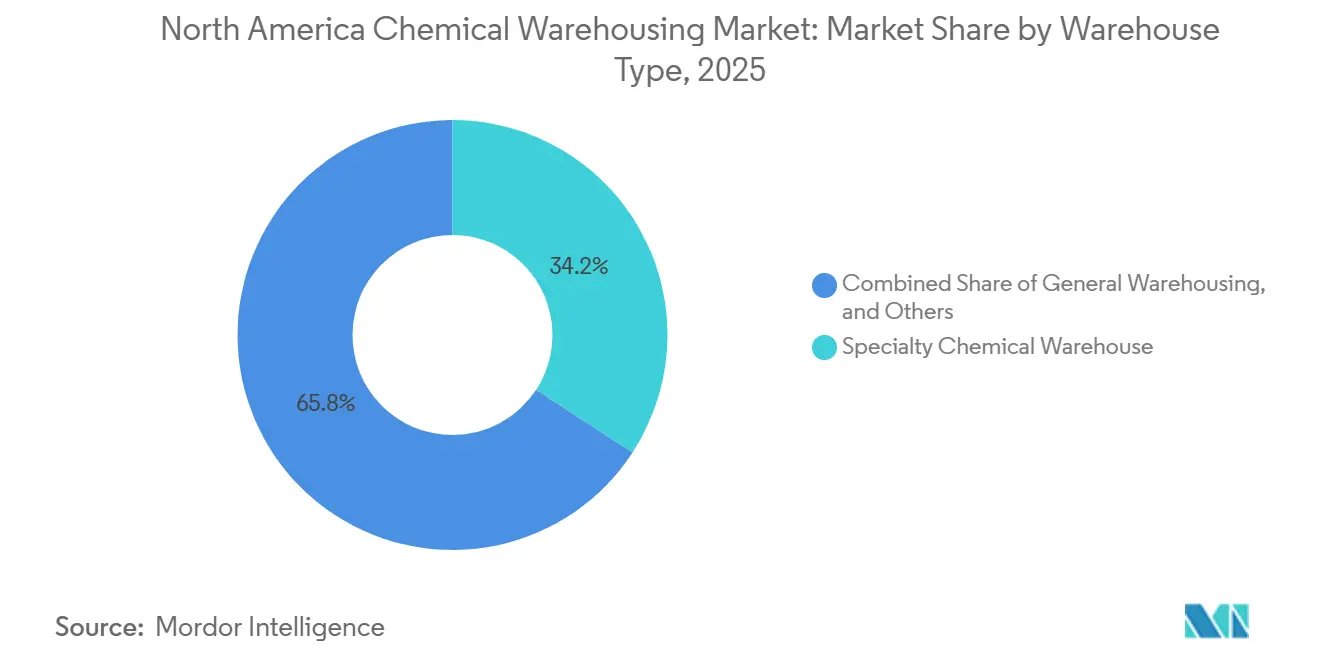

- By warehouse type, specialty chemical warehouses commanded 34.25% of the North America chemical warehousing market share in 2025, while temperature-controlled chemical warehouses recorded the fastest expansion at 5.59% CAGR through 2031.

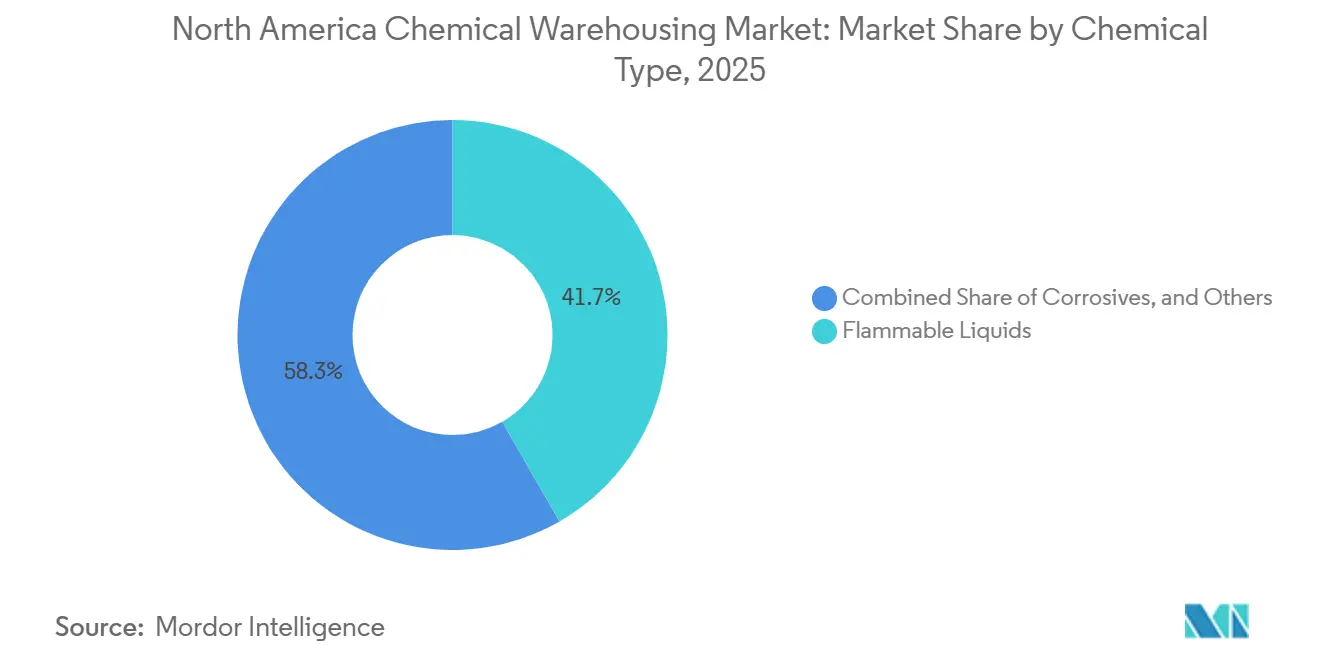

- By chemical type, flammable liquids led with 41.65% share of the 2025 North America chemical warehousing market size; whereas toxic substances advanced at a 5.31% CAGR to 2031.

- By end-user industry, oil and gas / petrochemicals held 32.46% market share in 2025, whereas pharmaceuticals and life sciences are growing at 6.89% CAGR, outpacing all other end users.

- By geography, the United States retained 91.09% of the North America chemical warehousing market share in 2025, but Mexico is projected to grow at 5.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on chemical warehousing market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in carbon-neutral pledges driving demand for LEED- and ISO 14001-certified chemical warehouses | +0.9% | North America, concentrated in California and Northeast sustainability-focused markets | Medium term (2-4 years) |

| Rapid expansion of battery-grade and energy-storage chemicals requiring segregated temperature-controlled storage | +1.1% | United States, Canada, with clusters near automotive and battery manufacturing hubs | Short term (≤ 2 years) |

| United States-Canada inland-port buildouts integrating rail, barge and pipeline links with dedicated hazmat terminals | +0.7% | Great Lakes region, Mississippi River corridor, Pacific Northwest | Long term (≥ 4 years) |

| AI-powered safety analytics lowering incident rates and insurance prerequisites, accelerating facility approvals | +0.5% | North America, led by technology-forward operators in major chemical clusters | Medium term (2-4 years) |

| Growth of bio-based and fermentation-derived chemicals creating allergen-free, contamination-controlled warehousing niches | +0.6% | United States, Canada, particularly near agricultural feedstock sources | Long term (≥ 4 years) |

| Post-CUSMA near-shoring boom shifting specialty-chemical inventory south to Northern Mexico logistics corridors | +0.8% | Northern Mexico (Monterrey, Bajio), Texas border regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Carbon-Neutral Pledges Driving Demand for LEED and ISO 14001-Certified Chemical Warehouses

Corporate sustainability targets now include Scope 3 logistics emissions, prompting shippers to insist that third-party facilities meet LEED and ISO 14001 benchmarks. Operators adopting solar roofs, high-efficiency HVAC and on-site water recycling qualify for green loans and command premium rent in the North America chemical warehousing market[1]“Chemical Safety and Climate Preparedness Resources,” Massachusetts Department of Environmental Protection, mass.gov. Energy costs averaging 6.6 cents /kWh along the Gulf Coast further improve payback periods for renewable retrofits. These certifications create tangible barriers to entry that channel volume toward well-capitalized incumbents. As state regulators align building codes with climate policy, sustainability credentials are expected to become a baseline requirement rather than a differentiator across the North America chemical warehousing market.

Rapid Expansion of Battery-Grade and Energy-Storage Chemicals Requiring Segregated Temperature-Controlled Storage

Electrolyte solvents and lithium hydroxide are hypersensitive to moisture and trace metals, forcing warehouses to add dew-point monitoring, inert gas blanketing, and isolated rooms. Rinchem’s 123,000 ft² Arizona site illustrates the upgraded ventilation and sensor arrays now standard for this trade. Precision helps reduce batch-failure risk, enabling multi-year contracts that lock in utilization. With automotive OEMs announcing 15 new battery plants by 2027, demand for such dedicated capacity is set to rise more quickly than overall activity in the North America chemical warehousing market[2]“Hazard Communication Standard,” United States Federal Register, federalregister.gov.

United States-Canada Inland-Port Build-Outs Integrating Rail, Barge and Pipeline Links with Dedicated Hazmat Terminals

Lower land costs and multimodal access allow inland hubs to compete with coastal clusters. TexAmericas Center offers 38 miles of internal rail plus barge links, granting tenants rate flexibility and redundancy. IMTT-Geismar North’s 60-acre riverfront site plans deepwater docks for 120,000 DWT vessels. Such investments enable producers to reposition inventories closer to end-users, lowering last-mile emissions while relieving congestion at Gulf Coast ports.

AI-Powered Safety Analytics Lowering Incident Rates and Insurance Prerequisites

Machine-learning models track forklift speed, aisle congestion, and temperature drift, flagging anomalies before they cascade into incidents. Rinchem cut its total-recordable-incident rate below 1, versus roughly 6 across generic 3PL peers, and negotiated lower premiums. OSHA’s warehousing emphasis program through 2026 makes such data essential for passing inspections, shortening start-up timelines for new North America chemical warehousing market entrants. Larger providers capitalize on scale to spread sensor and software costs, widening the gap with smaller rivals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical downturn risk in key end-markets (construction, plastics) causing volatile warehouse utilisation | -0.8% | North America, particularly regions dependent on construction and automotive sectors | Short term (≤ 2 years) |

| Emerging PFAS bans adding uncertainty to long-tail chemical inventories and liability management | -0.6% | United States, Canada, with California and Northeast leading regulatory action | Medium term (2-4 years) |

| Scarcity of rail-connected hazmat-zoned land parcels within Tier-1 chemical clusters | -0.7% | Gulf Coast, Great Lakes region, major chemical production hubs | Long term (≥ 4 years) |

| Rising cyber-security threats to IoT-integrated hazmat facilities increasing compliance and mitigation costs | -0.5% | North America, acute for operators with extensive digital infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyclical Downturn Risk in Key End-Markets Causing Volatile Warehouse Utilization

Paints, plastics and construction additives cycle with housing starts and auto output, shrinking inventories during recessions. New Jersey’s warehouse vacancy climbed to 9% in 2024 after 40 million ft² of speculative builds came online without committed tenants. Similar swings in the North America chemical warehousing market squeeze margin on fixed-cost assets, compelling operators to court counter-cyclical sectors such as pharmaceuticals to balance portfolio risk.

Emerging PFAS Bans Adding Uncertainty to Long-Tail Inventories and Liability Management

The expansion of EPA reporting to include over 100 PFAS chemicals, coupled with the delay of the TSCA reporting window to 2027, is intensifying compliance challenges for the chemical warehousing sector. Warehouses face increased upfront screening and declaration requirements for inbound materials, alongside the risk of stranded inventory or disposal costs if products become noncompliant or unsellable. This regulatory uncertainty is driving higher expenditures on specialty environmental insurance and enhanced compliance controls. The extended timeline further prolongs the period of ambiguity, complicating operational planning[3]“Force Majeure Declaration at Freeport,” Environmental Protection Agency, epa.gov .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Temperature Control Drives Premium Segment Growth

The North America chemical warehousing market is witnessing notable growth, with Temperature-Controlled Chemical Warehouses projected to expand at a CAGR of 5.59% through 2031, surpassing the market's overall growth rate. This highlights the increasing demand for specialized storage solutions. Specialty Chemical Warehouses, holding a 34.25% market share in 2025, reflect the industry's emphasis on quality and compliance. Customers are demonstrating a willingness to invest in certifications, documentation, and validated monitoring systems to ensure safety and regulatory adherence. These factors collectively drive the evolution of the chemical warehousing market in the region.

Demand for dew-point control, inert gas purging, and backup power makes capital intensity high, yet also locks in multi-year contracts from electronics and life-science firms. Hansen Storage doubled freezer capacity to 600,000 ft² to meet stricter climate-sensitivity standards. General Warehousing faces commoditization as shippers shift premium products into purpose-built zones across the North America chemical warehousing market, forcing non-specialists to compete on price or exit.

By Chemical Type: Toxic Substances Segment Accelerates on Pharmaceutical Growth

Flammable liquids continued to dominate with 41.65% of the North America chemical warehousing market share in 2025, yet toxic substances are forecast to grow at 5.31% CAGR as active pharmaceutical ingredients and biotechnology intermediates proliferate. Porter Logistics’ Atlanta facility handles multiple hazard classes with segregated flame rooms and foam suppression, mirroring the complexity that differentiates service providers[4]“Atlanta Hazmat Warehouse,” Porter Logistics, porter-logistics.com.

Pharmaceutical reshoring amplifies traceability and chain-of-custody requirements, amplifying demand for barcode-level visibility and dedicated storage cells. Providers that earn DEA and FDA clearances secure premium yields, reinforcing a two-tiered structure within the North America chemical warehousing market.

By End-User Industry: Pharmaceuticals Outpace Traditional Petrochemicals

Oil and Gas / Petrochemicals accounted for 32.46% of the North America chemical warehousing market size in 2025, yet Pharmaceuticals and Life Sciences are projected to expand at 6.89% CAGR, the highest among all segments. DHL Supply Chain’s lead-logistics pact with Sanyo Chemical underscores the appetite for integrated storage, kitting, and value-added services among pharmaceutical clients.

Higher qualification costs deter small operators, spurring consolidation as larger groups acquire niche players to enter regulated niches. Petrochemical flows remain steady along the Gulf Coast, but margins erode as capacity tightens in specialty verticals across the North America chemical warehousing industry.

Geography Analysis

The Gulf Coast anchors the North America chemical warehousing market through vast base-chemical output and deepwater export terminals. Announced energy projects worth USD 60 billion in 2025, 55% in Louisiana and 45% in Texas, will keep demand for bulk-tank storage elevated. The United States commands a 91.09% market share in 2025. Competitive power rates let operators run high-draw chillers while adding rooftop solar to meet Scope 3 targets. Inland Great Lakes locations use barge and unit-train links to tap Midwest manufacturers that prize just-in-time delivery.

Mexico’s northern states show accelerating warehouse construction around intermodal hubs in Monterrey and Saltillo, and grow at 5.54% CAGR annually. Post-CUSMA tariff certainty encourages specialty-chemical makers to split production between Nuevo León and Texas, creating synchronized inventory pools on both sides of the border. Canadian growth remains steady, underpinned by agrochemical and mining additives that flow through Alberta and Ontario hubs. Harmonized hazard-communication rules simplify documentation for operators managing cross-border inventories.

Climate-related shocks such as Hurricane Beryl’s 2024 landfall have prompted providers to add elevated pump houses and redundant power in coastal facilities. Diversifying capacity inland mitigates downtime risk and satisfies insurers who now require documented continuity planning for high-hazard inventories.

Mordor Intelligence provides coverage of the chemical warehousing market across other key regional markets, including Europe, Middle East, and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Canada, Germany, France, United Kingdom, Italy, and South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

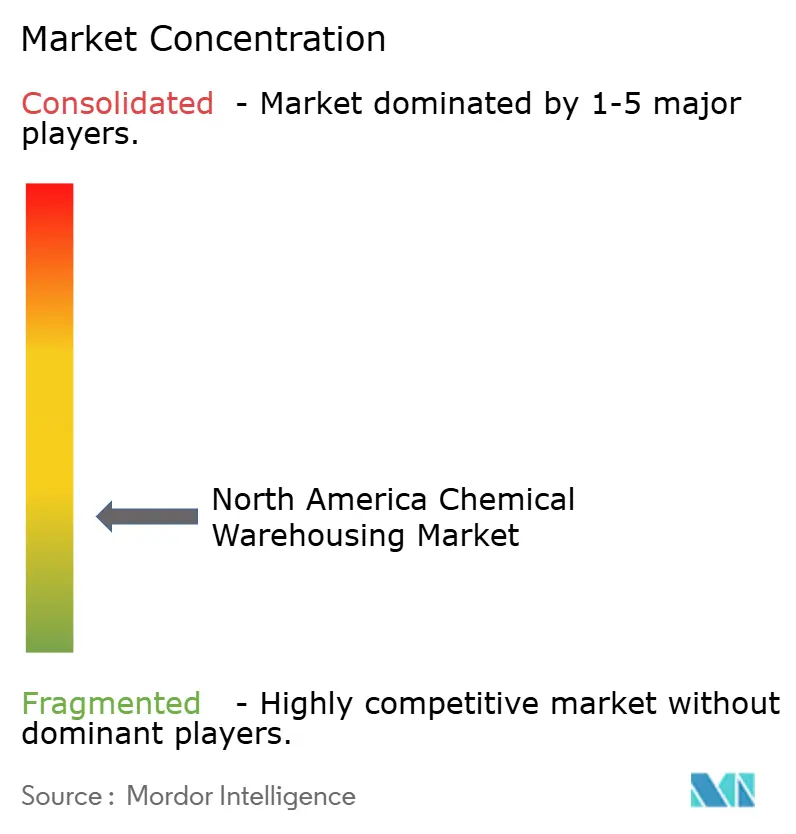

Fragmentation prevails, yet scale advantages in technology and certification are driving merger activity. Quantix’s 2024 acquisition of CLX Logistics created a platform managing USD 2 billion in spend and more than 40 distribution centers. Rinchem, Weber Logistics and Porter Logistics differentiate through AI-enabled safety, LEED buildings and deep expertise in multi-hazard segregation.

Providers racing to capture the battery-chemical boom retrofit existing bays with humidity controls and conductive-floor coatings. Those moves position incumbents to win long-duration contracts that underpin stable utilization across the North America chemical warehousing market. Sustainability credentials are now central to bids, with operators touting ISO 14001 audits and renewable-energy offsets to satisfy customer Scope 3 scorecards.

Smaller regional firms face rising cyber-security and compliance costs; many seek partnerships or become acquisition targets. The top five players are estimated to control around 32% of segment revenue, indicating moderate concentration in the North America chemical warehousing market.

North America Chemical Warehousing Industry Leaders

DHL Group

Rinchem Company, Inc.

Odyssey Logistics & Technology

ALFRED TALKE

Penske Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Supply Chain signed a five-year lead-logistics agreement with Sanyo Chemical Industries, rolling out MySupplyChain dashboards for near-real-time visibility.

- April 2025: ExxonMobil purchased nearly 100 acres in Baytown, Texas, expanding its petrochemical footprint near major hazmat rail spurs.

- March 2025: LyondellBasell approved a USD 400 million propylene expansion at Channelview Complex, targeting start-up in 2028.

- January 2025: Trecora Resources completed a USD 7.2 million sales-rack project that doubled rail-loading capacity at South Hampton.

North America Chemical Warehousing Market Report Scope

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals and Life Sciences |

| Agrochemicals |

| Paints, Coatings and Adhesives |

| Food and Feed Additives |

| Oil and Gas / Petrochemicals |

| Others |

| United States |

| Canada |

| Mexico |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals and Life Sciences | |

| Agrochemicals | |

| Paints, Coatings and Adhesives | |

| Food and Feed Additives | |

| Oil and Gas / Petrochemicals | |

| Others | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will chemical warehousing spend reach in North America by 2031?

The North America chemical warehousing market is forecast to reach USD 34.09 billion by 2031, growing at a 4.56% CAGR from 2026.

Which storage format is expanding the fastest?

Temperature-Controlled Chemical Warehouses lead growth at 5.59% CAGR as battery and life-science products demand precise climate control.

Why are operators racing for green certifications?

Shippers now include LEED and ISO 14001 compliance in bid criteria to reduce Scope 3 emissions, allowing certified sites to command premium rates.

What role does Mexico play in regional warehousing?

Nearshoring into Monterrey and Bajío makes Mexico the fastest-growing geography at 5.54% CAGR through 2031, complementing US capacity.

Which end-user vertical offers the highest margins?

Pharmaceuticals and Life Sciences deliver the fastest growth at 6.89% CAGR, requiring validated, contamination-free environments that support premium pricing.

How is technology reshaping warehouse safety?

AI-based analytics cut incident rates, lower insurance costs and speed regulatory approvals, giving tech-savvy operators a competitive edge.

Page last updated on: