United Kingdom Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

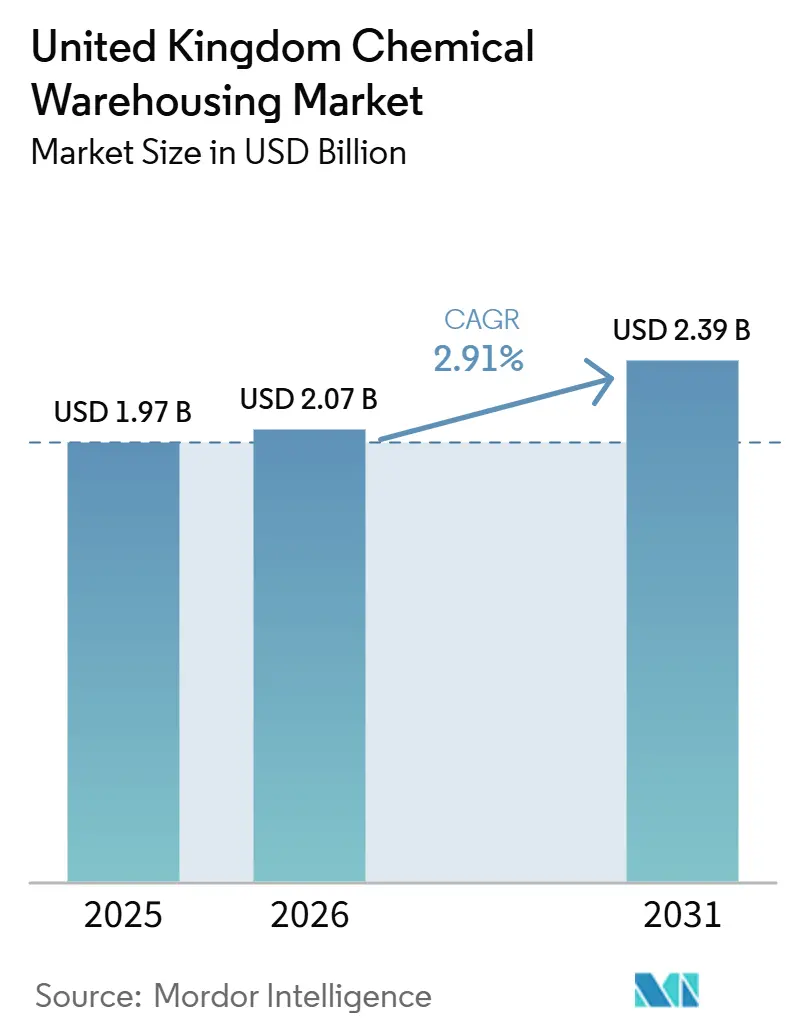

| Base Year Market Size (2025) | USD 1.97 Billion |

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 2.91% CAGR |

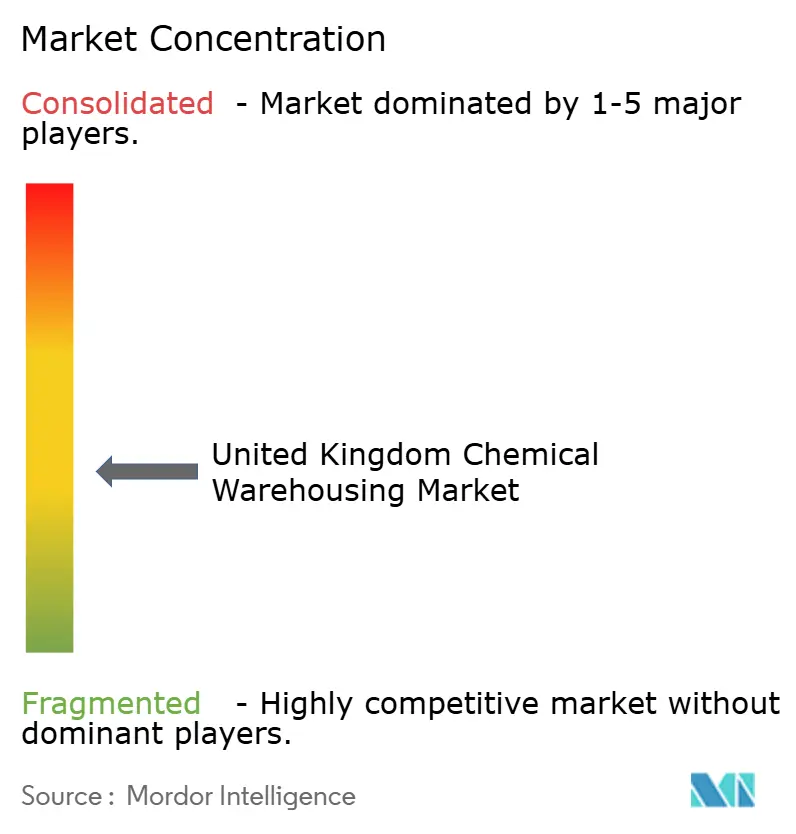

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Chemical Warehousing Market Analysis by Mordor Intelligence

The United Kingdom Chemical Warehousing Market size is expected to increase from USD 1.97 billion in 2025 to USD 2.07 billion in 2026 and reach USD 2.39 billion by 2031, growing at a CAGR of 2.91% over 2026-2031.

As a backbone to manufacturing supply chains, the sector supports a broad base of domestic production where chemicals underpin a large share of finished goods across the economy. Pharmaceutical production has strengthened through 2025, with a 4.4% increase in February and a 9.3% three month-on three month growth rate by December, reinforcing demand for temperature-controlled and GDP-compliant storage near key research and manufacturing nodes. Post-Brexit customs formalities have kept bonded capacities highly utilized. HM Revenue & Customs reports median warehouse use at 87% and peak occupancy at 90%, highlighting the importance of customs warehousing for hazardous shipments. Decarbonization pressures are shaping capex, with large-scale rooftop solar potential across the biggest warehouses and rising building performance requirements that tighten the efficiency bar for operators. Safety oversight remains rigorous under COMAH, with hundreds of establishments in England subject to enhanced inspections and climate resilience measures, which keep compliance and risk management central to operating models.

Key Report Takeaways

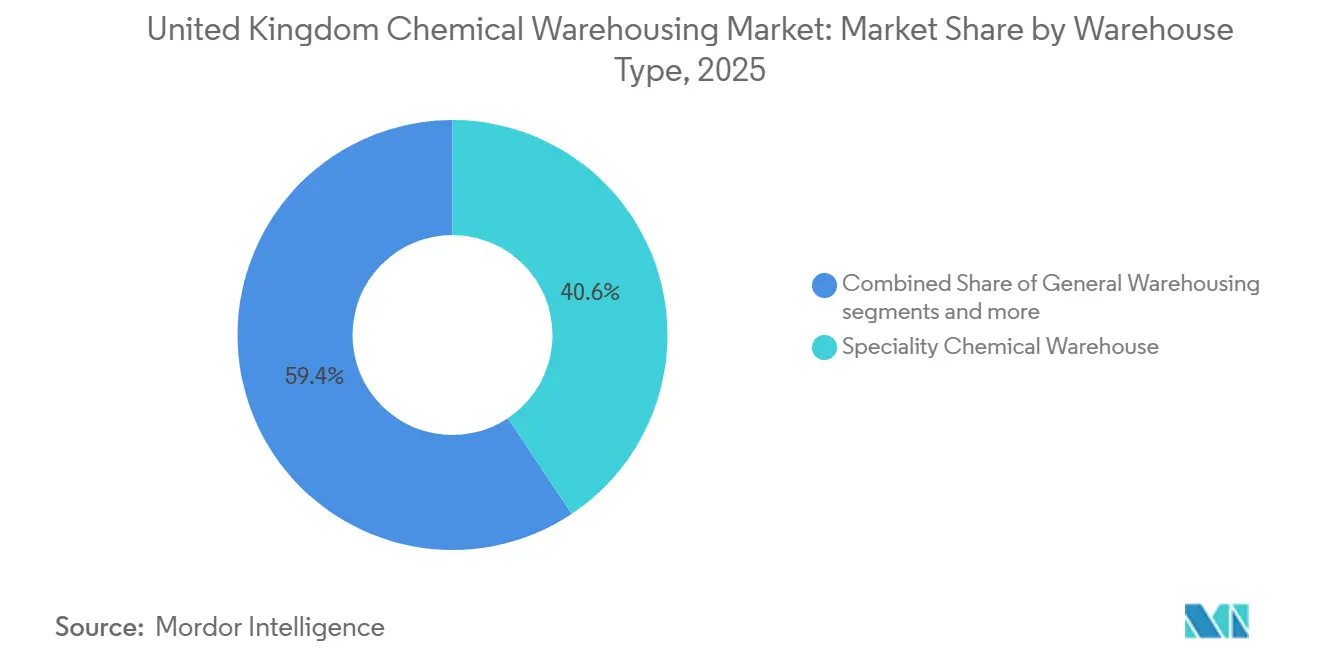

- By warehouse type, specialty chemical warehouses led with 40.64% of the United Kingdom chemical warehousing market share in 2025; temperature-controlled chemical warehouses are projected to expand at a 5.78% CAGR through 2031.

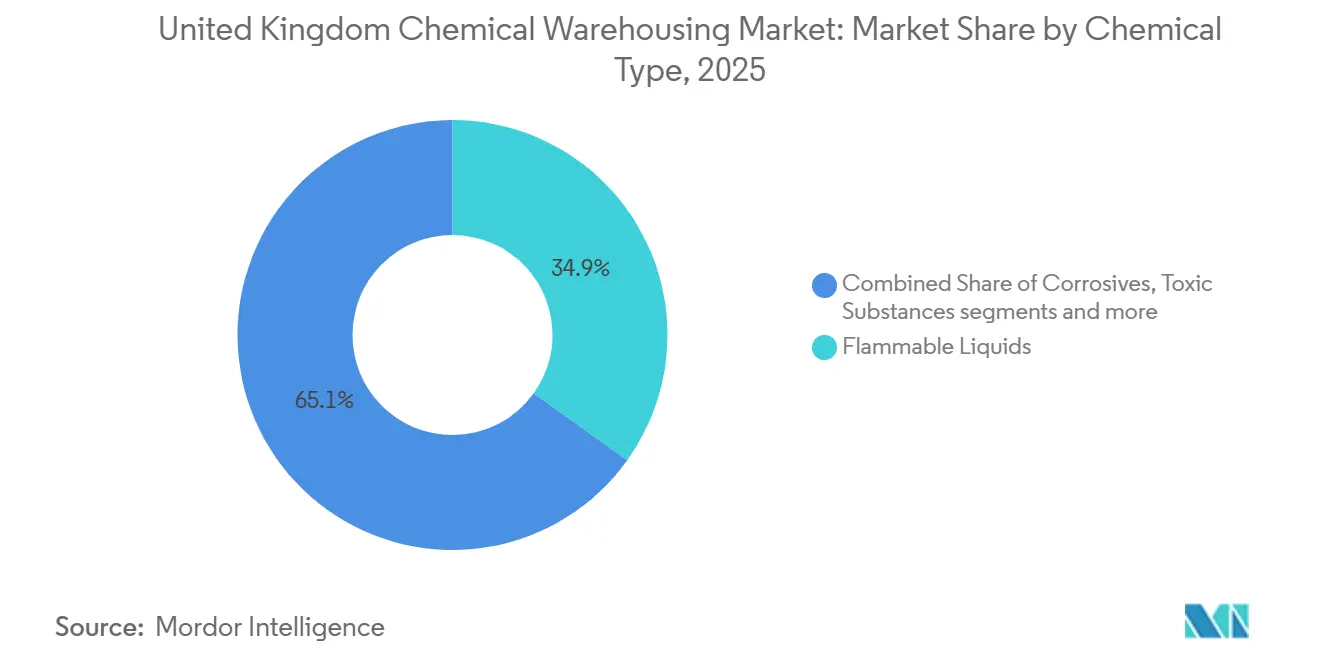

- By chemical type, flammable liquids accounted for 34.89% of the United Kingdom chemical warehousing market size in 2025, while toxic substances are forecast to rise at a 6.21% CAGR through 2031.

- By end-user industry, specialty chemicals manufacturing accounted for 31.21% of the United Kingdom chemical warehousing market share in 2025; pharmaceuticals & life sciences are set to post the fastest segment growth at a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United kingdom holds a defined position within a broader international distribution. The chemical warehousing market share data by Mordor Intelligence maps that allocation across all contributing countries and regions, globally.

United Kingdom Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical and Life Sciences Manufacturing Strength | +0.8% | England, Scotland, Wales | Medium term (2-4 years) |

| Post-Brexit Customs and Bonded Warehousing | +0.6% | England, Scotland | Short term (≤2 years) |

| Specialty Chemicals and Advanced Materials Growth | +0.5% | England, Scotland | Medium term (2-4 years) |

| Port Infrastructure Modernization | +0.4% | England, Wales, Scotland | Medium term (2-4 years) |

| Net Zero Carbon Commitments | +0.3% | United Kingdom industrial clusters | Long term (≥4 years) |

| COMAH Safety Regulation Enforcement | +0.3% | England, Scotland, Wales | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical and Life Sciences Manufacturing Strength

Pharmaceutical output in the United Kingdom expanded through 2025, with a 4.4% rise in February and a 9.3% three month on three-month pace by December, which is lifting storage needs for GDP-compliant and cold chain space close to manufacturing and research centers[1]Office for National Statistics, “Index of Production, UK: February 2025,” Office for National Statistics, ons.gov.uk. Government life sciences competitiveness indicators show the United Kingdom attracted stronger foreign direct investment and equity finance into 2024, reinforcing the pipeline of regulated products that require specialized warehousing and distribution solutions. The Life Sciences Sector Plan also outlines an AI-ready health data service with up to GBP 600 million (USD 809.46 million) of support, a move that can accelerate clinical development and expand short-cycle storage flows for investigational products. Advanced therapy medicinal products, which require cryogenic handling and strict chain of custody controls, had a notable United Kingdom trial footprint in 2024 and will continue to push specification requirements for facilities that serve biopharma supply chains. Planned expansion of biologics manufacturing capacity in the Thames Valley region signals long-term demand for adjacent sterile storage and temperature-managed logistics. All together, these forces support steady expansion in the United Kingdom chemical warehousing market as life sciences scale manufacturing, clinical operations, and cold chain networks.

Post-Brexit Customs and Bonded Warehousing

HM Revenue & Customs reported large installed customs authorized capacity with utilization rates near 87% on average and 90% at peaks, highlighting the structural reliance on bonded facilities for import buffers and duty deferment. Hazardous goods comprised a materially higher share of customs warehouse inventory relative to general stores, which reflects the importance of risk-segregated storage and spill prevention systems in bonded operations. Ongoing implementation of the EU-UK Trade and Cooperation Agreement and UK REACH places documentation and origin rules at the core of compliance, sustaining demand for bonded storage models that defer duty and VAT until goods enter free circulation. The United Kingdom Freeports program, with simplified customs processes and extended tax relief windows through the next decade, strengthens the case for locating customs warehousing within designated zones that serve chemicals trade flows. Complementary public and private port investments in cleaner fleets and added berth and rail capacity improve predictability for just-in-time hazardous shipments. As a result, customs and bonded facilities remain a strategic lever in the United Kingdom chemical warehousing market in the post-Brexit context.

Specialty Chemicals and Advanced Materials Growth

Chemicals and pharmaceuticals generated GBP 30.4 billion (USD 41.01 billion) of value added, GBP 60 billion (USD 80.94 billion) in exports, and direct employment of over 130,000 in 2023, with regional clusters anchored by pipelines and ports that shape warehousing footprints. The United Kingdom achieved a sovereign manufacturing milestone in 2026 with a pilot facility for ceramic matrix composites, which introduces new storage needs for temperature-sensitive and contamination-controlled materials. Survey data show improving order books into late 2025 but persistent margin pressure, prompting more automation and digitalization in warehouses to increase throughput and accuracy for specialty lines. Scotland’s Grangemouth cluster is executing a transition plan with investments in low-carbon hydrogen, pipeline upgrades, and new chemical manufacturing buildings, which will adjust storage mixes toward higher-value intermediates and greener feedstocks. As value-added formulations scale, multi-tenant sites with blending and repack capabilities can capture resilient margins in the United Kingdom chemical warehousing market, especially near customer clusters. These features continue to anchor investment momentum for specialty-oriented storage over the medium term.

Port Infrastructure Modernization

United Kingdom ports invested GBP 4.5 billion (USD 6.07 billion) in terminals and equipment since 2020 and a further GBP 6 billion (USD 8.09 billion) in port estate projects, including new warehousing, which signals continued capacity additions for port-centric logistics. In 2025, the government announced GBP 1.1 billion (USD 1.48 billion) of public-private maritime investment, including the UK SHORE program for clean maritime technology that will influence port handling and ancillary logistics decarbonization. The Freeports program secured GBP 6.4 billion (USD 8.63 billion) of private investment and 7,200 jobs by mid 2025, with tax relief windows extended into the next decade, creating favorable conditions for chemical storage projects near freeport sites. Department for Transport freight forecasts indicate rising container and dry bulk demand, while liquid bulk volumes remain sensitive to the energy transition, shaping throughput mix for storage operators. As berth expansions and inland rail links progress, port adjacent hazmat and cold chain facilities can rebalance networks for shorter lead times and lower risk handling in the United Kingdom chemical warehousing market. These upgrades build optionality for importers and domestic producers across key coasts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Warehouse Space Shortage | -0.4% | England ports and Scotland’s Grangemouth; limited free customs‑warehouse capacity | Short term (≤2 years) |

| High Energy and Occupancy Costs | -0.3% | Global cost pressures with heightened United Kingdom exposure | Medium term (2-4 years) |

| HGV Driver Shortage Crisis | -0.2% | United Kingdom national distribution networks | Short term (≤2 years) |

| Brexit‑Related Regulatory Uncertainty | -0.2% | United Kingdom‑wide implementation of UK REACH and rules of origin | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Warehouse Space Shortage

Structural tightness persists for compliant space, and customs-authorized capacity has shown high utilization with limited free space, which constrains flexibility for new chemical flows and seasonal peaks. Median utilization at 87% and peak occupancy near 90% indicate limited headroom, especially for dangerous goods, where inventory shares are higher in customs warehouses than in general sites. COMAH oversight adds further constraints, as priority establishments require climate risk assessments and flood preparedness protocols that can extend timelines for capacity changes. The compliance burden is appropriate for risk management, but reinforces the scarcity of upper-tier sites that can accept certain hazard classes without extensive modification[2]Health and Safety Executive, “Information and guidance on COMAH,” Health and Safety Executive, hse.gov.uk. For the United Kingdom chemical warehousing market, this means location decisions must balance proximity to ports and clusters with the limited availability of suitable lots and permits. The shorter effect is higher switching costs and longer commissioning lead times for specialized capacity.

High Energy and Occupancy Costs

Energy and occupancy expenses weigh on warehouse cost curves, and the policy drive to improve building efficiency is intensifying capex needs in the near term. Large-scale rooftop solar opportunities across the biggest United Kingdom warehouses provide an offset by reducing net electricity costs, with potential to materially add distributed generation close to logistics operations. National climate goals and the policy response to the Climate Change Committee underscore the direction of travel toward lower carbon operations, which implies continued investment in energy management, on-site renewable capacity, and certified green power. Operators in the United Kingdom chemical warehousing market are aligning designs to higher efficiency baselines and specifying low-emission handling equipment where on-site charging or shore power is available. While these efforts improve resilience and reduce lifetime costs, they can pressure near term margins during retrofit cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialization Responds to Hazard Complexity

Specialty chemical warehouses held the largest share of 40.64% in 2025 as asset owners prioritized segregation, engineered ventilation, and advanced fire suppression that align with hazardous substance handling standards. Enhanced controls for corrosive, flammable, and oxidizing substances create capital barriers that sustain service premiums and reduce supply elasticity in the United Kingdom chemical warehousing market. Priority COMAH sites in England operate under intensified oversight with climate risk assessments and flood planning, which keeps storage design and location choices tightly linked to regulation. These controls elevate the role of safety cases, emergency planning, and community liaison in day-to-day operational management. As a result, the United Kingdom chemical warehousing industry leans toward specialized footprints near ports and clusters that pair hazard control with multimodal access.[3]British Ports Association, “UK Ports invested £4.5 Billion in new infrastructure since 2020,” British Ports Association, britishports.org.uk

Temperature-controlled sites are the fastest growing of 5.78% as biopharma and advanced therapies expand clinical and commercial output with stringent GDP and GMP requirements. Facilities that support 2-8°C refrigerated storage or colder zones for biologics and cell-based therapies will command higher specification standards and closer siting to manufacturing and airports. Rising pharmaceutical production through 2025 strengthens the case for end-to-end traceability and frequent quality audits in these buildings. As the United Kingdom chemical warehousing market size advances to USD 2.39 billion by 2031 at a 2.91% CAGR, operators are calibrating footprints to concentrate higher spec units close to science parks and international gateways. This setup balances capacity for ambient and low-hazard goods while meeting rising demand for controlled environments.

By Chemical Type: Flammable Liquids Drive Volume, Toxics Command Growth

Flammable liquids retained a 34.89% of the United Kingdom chemical warehousing market size in 2025 due to their cross-industry usage in coatings, adhesives, and pharmaceutical synthesis. These products require explosion-protected systems, fire suppression technologies, and robust secondary containment, which shape design choices in the United Kingdom chemical warehousing market. Customs authorized facilities reported a higher proportion of dangerous goods relative to general warehouses, and that mix points to deeper compliance requirements within bonded storage. Corrosives and oxidizers also require careful segregation to prevent adverse reactions and to align with guidance on incompatible classes. These measures reinforce the premium on operator competence and incident prevention culture in hazardous stores.

Toxic substances emerged as fastest growing segment, registering a growth of 6.21% by 2031, driven by demand from agrochemicals, pharmaceutical intermediates, and high-purity inputs to electronics. These flows require tight worker exposure controls, serialized batch tracking, and chain of custody documentation, which favor warehouse operators with strong quality systems. Advances in zero-emission HGV pilots and new charging networks signal a long-term transition in heavy transport, which can reduce emissions intensity of toxic cargo flows without altering core safety protocols. As the United Kingdom chemical warehousing industry serves more complex products, high spec handling, data integrity, and trained staffing become decisive commercial differentiators. Together, these shifts keep hazardous materials expertise central to competitive positioning for the next cycle.

By End user Industry: Pharmaceuticals Accelerate, Specialty Chemicals Anchor

Specialty chemicals held the largest share of 31.21% in 2025 as distributors supported tailored formulations across automotive, electronics, food processing, and construction with blending and repack services. These services reward technical competence and proximity to end use, which keeps a significant portion of the United Kingdom chemical warehousing market anchored near industrial corridors and multimodal nodes. Integrated logistics with dedicated chemical handling remains attractive for customers who value compliance and short lead times. As customers seek vendor consolidation, storage sites offering formulation adjacent services can secure stickier volumes and long-term contracts.

Pharmaceuticals and life sciences represent the fastest growth avenue, projected to grow by 6.67% through 2031 as output expands and clinical pipelines widen under the national strategy. Life sciences investment commitments, including biologics expansion near Reading, add multi-year demand for GMP adjacent storage and temperature-managed distribution. Leading third-party providers have also built out dedicated healthcare and cold chain services to serve biopharma customers across EMEA, which aligns with long run growth in regulated logistics. As the United Kingdom chemical warehousing market size grows at a 2.91% CAGR to 2031, pharma-linked flows will keep shaping requirements for traceability, quality audits, and product integrity controls. This trajectory amplifies the weight of GDP and GMP standards in contract bids and network design.

Geography Analysis

England concentrates the largest share of high-spec capacity due to port proximity, pipeline connectivity, and dense customer clusters that rely on proximate storage and rapid turnaround. COMAH oversight is extensive, with hundreds of priority sites in England subject to intensified regulatory management that shapes site design and readiness. Thames side assets benefit from freeport designations and a pipeline of port and rail enhancements, which strengthen inbound reliability for chemicals and hazard-rated goods. The United Kingdom chemical warehousing market continues to concentrate around these corridors as investment in terminals and clean maritime projects improves handling efficiency and lowers emissions intensity.

Scotland’s Grangemouth cluster is executing a just transition plan with investment for hydrogen, pipeline upgrades, and new chemical manufacturing buildings, which repositions the product slate toward low-carbon pathways and high-value intermediates[4]The Scottish Government, “Grangemouth Industrial Transition Plan, Annex A – Detailed Baseline,” The Scottish Government, gov. scot. As this production base evolves, warehouse demand will reflect inputs for agrochemicals and synthetic feedstocks, along with higher safety requirements. Priority oversight at COMAH establishments further guides the configuration of hazard zones, emergency planning, and climate risk preparedness. These dynamics point to a continued concentration of specialized capacity in central Scotland with links to major ports.

In Wales and the West, maritime investment in 2025 targeted clean technologies and port estate upgrades, which set the stage for build-to-suit warehousing and improvement of port-centric logistics. Department for Transport freight forecasts suggest that container and dry bulk flows will rise, which supports additional storage capacity along strategic corridors connected to the M4 and M5. Northern industrial regions can benefit from decarbonization projects and energy transition investments that recast throughput mixes, while maintaining safety compliance for hazardous goods. These patterns collectively guide network design choices in the United Kingdom chemical warehousing market as operators calibrate locations against customer density and port access.

Mordor Intelligence delivers a comprehensive view of the chemical warehousing market across all major regions such as Europe, North America, and Middle East, alongside country-level analysis for Germany, France, Canada, South Korea, Mexico, and Italy, each offering a view of the local market realities.

Competitive Landscape

The market remains moderately concentrated overall, although compliance intensity and space constraints are gradually consolidating share among established and certified operators. Strategic moves in recent periods emphasize selective M&A and targeted capacity upgrades rather than greenfield expansion, consistent with capital discipline in a regulated environment. Brenntag’s acquisition of Airedale Group added blending, formulation, and dilution capabilities in the North of England, deepening last-mile specialty coverage and strengthening customer ties. These steps improve stickiness with downstream manufacturers that prize compliance and technical service.

Global players are also tuning portfolios toward healthcare and high-value regulated flows, as seen in DHL Group’s acquisitions in specialty healthcare logistics, which align with long-run growth in biopharma cold chain and GDP-compliant services. Kuehne+Nagel’s partnership to pilot electric HGV operations signals a practical pathway to lower fleet emissions while preserving service reliability for sensitive chemical cargoes. Port-centric warehouse strategies continue to advance as freeports and maritime decarbonization initiatives accelerate investment in berths, rail links, and clean handling equipment that can compress inland transit times. These developments expand optionality in the United Kingdom chemical warehousing market for importers and domestic manufacturers.

Technology deployment differentiates top operators, with data-driven route optimization, robotics, and serialized traceability adopted to raise accuracy and minimize emissions for regulated products. Compliance posture is a durable moat, given COMAH requirements for safety reports, emergency planning, and risk controls that deter inexperienced entrants. As customers in pharmaceuticals and specialty chemicals integrate environmental metrics into procurement, operators that blend safety, efficiency, and decarbonization will consolidate share over time in the United Kingdom chemical warehousing market. The near term cycle thus favors leaders who combine regulated know-how with sustainability-linked performance.

United Kingdom Chemical Warehousing Industry Leaders

H.W. Coates

Bowker Transport

Den Hartogh Logistics

GXO Logistics

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The United Kingdom achieved a first in advanced materials with a pilot-scale ceramic matrix composite manufacturing capability, supporting applications in hypersonics, space, and propulsion, thus driving demand for chemical warehousing.

- December 2025: Brenntag completed the acquisition of Airedale Group, a Keighley, North Yorkshire-based specialty chemical distributor, initially announced in December 2025. Integration brings blending, formulation, and dilution capabilities to Brenntag UK's network, enhancing the product portfolio and regional supply chain infrastructure for customers across the food and beverage manufacturing and metal surface treatment sectors.

United Kingdom Chemical Warehousing Market Report Scope

The United Kingdom Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, and Others), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints, Coatings & Adhesives, Food & Feed Additives, Oil & Gas / Petrochemicals, and Others). The Market Forecasts are Provided in Terms of Value (USD Billion).

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the size and growth outlook for the United Kingdom chemical warehousing market?

The United Kingdom chemical warehousing market size was USD 1.97 billion in 2025 and is projected to reach USD 2.39 billion by 2031 at a 2.91% CAGR.

Which end use sectors are driving demand for regulated storage in the United Kingdom?

Pharmaceutical and life sciences are the fastest-growing due to clinical and biologics expansion, while specialty chemicals remain the largest base of demand across automotive, electronics, food, and construction.

How is post-Brexit policy influencing warehousing strategies for chemicals?

Customs and UK REACH requirements elevate the role of bonded storage, with freeport incentives and high utilization of customs authorized capacity shaping network design.

What facility types are growing fastest within chemical warehousing?

Temperature controlled facilities are growing fast as biopharma and advanced therapies require tighter GDP and GMP standards and more cryogenic or refrigerated capacity.

Which regions in the United Kingdom are key hubs for chemical warehousing?

England’s port proximate corridors and Scotland’s Grangemouth cluster are central, supported by freeport designations, port investments, and industrial transition plans.

How is decarbonization affecting chemical warehousing capex?

Operators are aligning to stricter building performance and investing in rooftop solar and clean handling equipment, which raises near term capex but improves long term cost resilience.

Page last updated on: