Canada Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

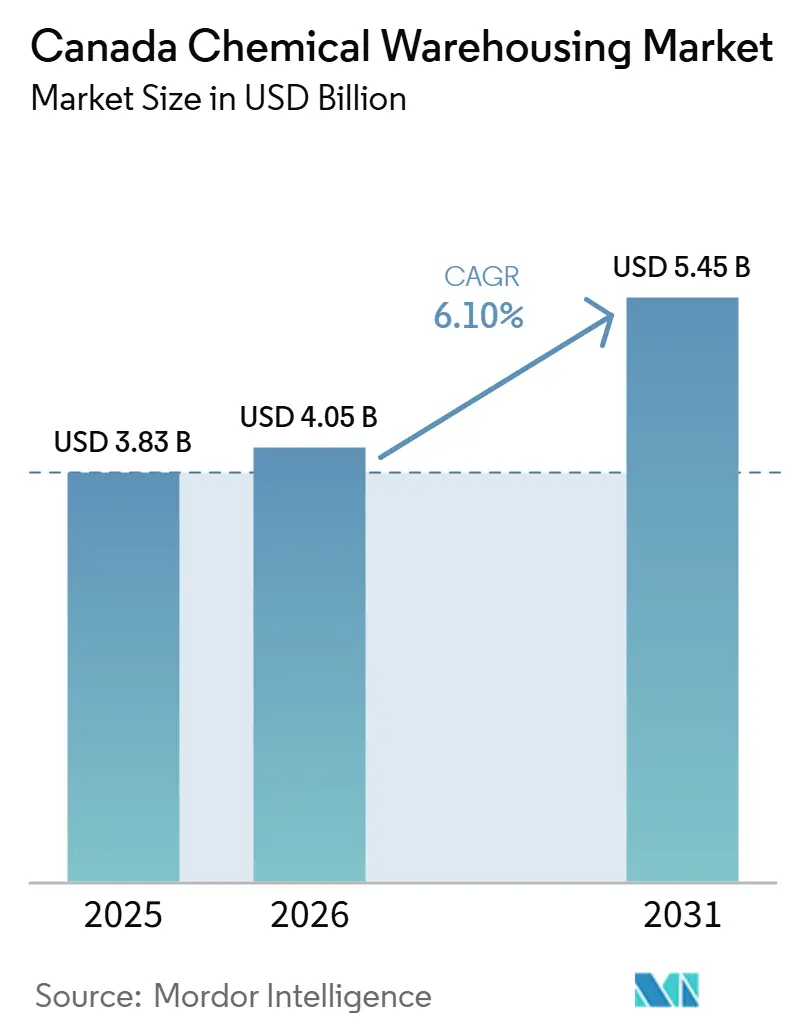

| Base Year Market Size (2025) | USD 3.83 Billion |

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 5.45 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

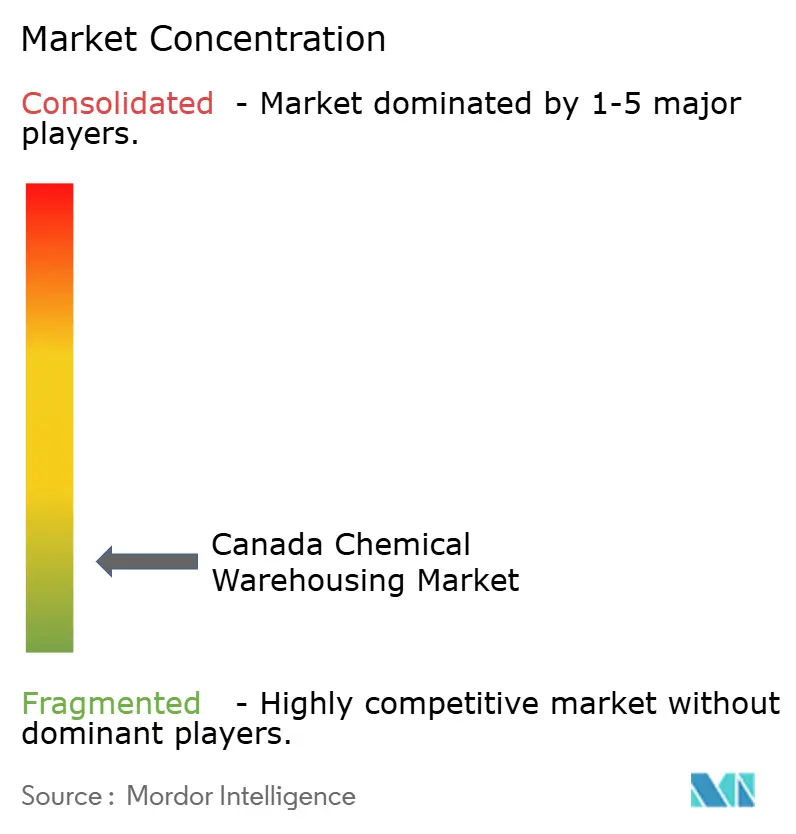

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Chemical Warehousing Market Analysis by Mordor Intelligence

The Canada Chemical Warehousing Market size is projected to be USD 3.83 billion in 2025, USD 4.05 billion in 2026, and reach USD 5.45 billion by 2031, growing at a CAGR of 6.10% from 2026 to 2031.

Growth is supported by trade-linked inventory buffering and rising demand for compliant chemical storage near major industrial and border-adjacent nodes, with Canada-U.S. chemical trade reaching USD 71.8 billion in 2024, reinforcing the need for buffer inventories and border-adjacent warehousing to reduce disruption risk and maintain service continuity, which is accelerating demand for near-border storage and buffer inventories to protect against logistics disruptions. Expanding transportation and warehousing activity, including 2023 growth and ongoing monthly gains in late 2025, suggests tightening capacity supporting pricing for specialized facilities that comply with TDG and municipal fire codes. Capital commitments in Alberta’s Industrial Heartland, notably Dow’s planned Path2Zero ethylene complex and Cando Rail’s Sturgeon Terminal expansion, are shifting infrastructure needs from ambient bulk storage to temperature-controlled and emissions-monitored spaces suited to net-zero manufacturing ecosystems. Federal support for critical minerals processing is catalyzing new requirements for reagent warehousing near planned lithium, nickel sulfate, and graphite facilities, while port capacity gaps and climatic volatility are amplifying location risk and stressing urban distribution networks in peak weather windows.

Key Report Takeaways

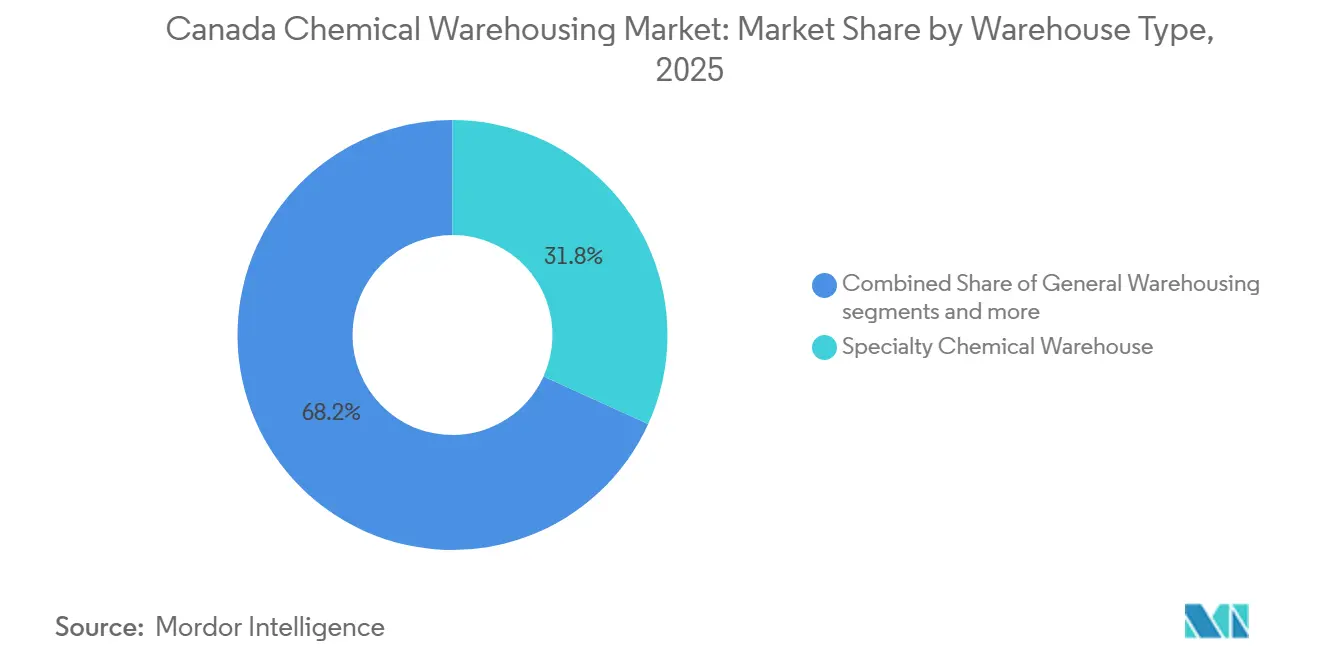

- By warehouse type, specialty chemical warehouses led with 31.79% of the Canada chemical warehousing market share in 2025, while temperature-controlled chemical warehouses are forecast to expand at a 7.41% CAGR through 2031.

- By chemical type, flammable liquids accounted for 39.74% share of the Canada chemical warehousing market size in 2025, and toxic substances are projected to grow at an 8.41% CAGR through 2031.

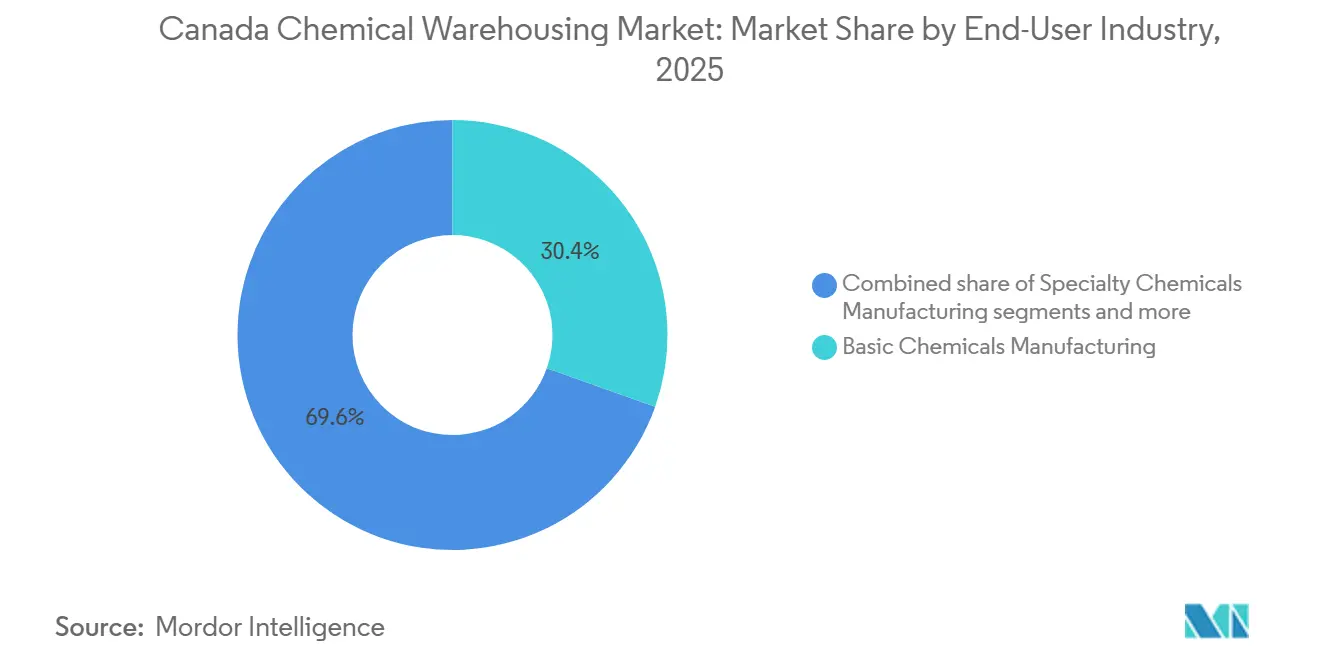

- By end-user industry, basic chemicals manufacturing held 30.41% share in 2025, and pharmaceuticals and life sciences are expected to advance at a 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Canada includes both locally based firms and those operating across multiple regions. The market landscape in the global chemical warehousing industry research shows how these players are arranged internationally.

Canada Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USMCA Integration and Cross-Border Trade | +1.3% | National, concentrated at Windsor-Detroit, Sarnia-Port Huron, and Pacific Gateway. | Medium term (2-4 years) |

| Oil Sands and Petrochemical Development | +1.1% | Alberta Industrial Heartland, with spill-over to Saskatchewan and British Columbia export terminals | Long term (≥ 4 years) |

| Mining Industry Chemical Demand | +0.9% | Northern Ontario, Northern Quebec, British Columbia interior, Saskatchewan uranium corridor | Long term (≥ 4 years) |

| Agricultural Sector Chemical Requirements | +0.8% | Prairie provinces primary, and secondary in Ontario and Quebec produce regions. | Short term (≤ 2 years) |

| Climate Change Adaptation Chemicals | +0.6% | National, with acute demand in Ontario and Quebec urban corridors, coastal British Columbia, and Arctic communities | Medium term (2-4 years) |

| Strategic Port Infrastructure | +0.7% | Pacific Gateway, Great Lakes-St. Lawrence, Atlantic Gateway | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

USMCA Integration and Cross-Border Trade

USMCA’s Chemical Sectoral Annex, reaffirmed by CIAC, the American Chemistry Council, and ANIQ in January 2026, is streamlining regulatory cooperation and reducing redundant testing, which concentrates demand for warehouse capacity near key crossings and intermodal yards serving regulated flows in the Canadian chemical warehousing market. The Windsor-Detroit corridor’s outsized share of bilateral road trade has prompted importer co-location strategies within short radii of customs plazas to mitigate dwell times and stabilize cycle times for dangerous goods.[1]Government of Canada, “State of Trade 2024,” Global Affairs Canada, international.gc.ca Increased activity in transportation and warehousing in 2023, followed by positive monthly readings into late 2025, aligns with the migration of the Canada chemical warehousing market toward border-adjacent and intermodal-integrated nodes. The potential for rail service disruptions, highlighted in 2024 with large exposure for bilateral chemical trade, has led U.S. buyers to maintain buffer inventories in Canada, lifting base demand for certified storage near crossings. Rail providers such as CN are becoming more important in supporting chemical storage networks that depend on reliable intermodal movement.[2]Canadian National Railway, “Border Logistics and Supply Chain Corridors,” CN, cn.ca

Oil Sands and Petrochemical Development

Dow’s planned USD 8.9 billion Path2Zero complex in Fort Saskatchewan aims for net-zero scope 1 and 2 emissions through integration with the Alberta Carbon Trunk Line, raising specifications for warehouse infrastructure that can support low-emissions operations in the Canada chemical warehousing market.[3]Canadian Energy Centre, “New Petrochemical Projects in Alberta Meet Economic and Environmental Objectives,” Canadian Energy Centre, canadianenergycentre.ca Linde Canada’s large-scale hydrogen project, designed with carbon capture at multi-million tonne annual levels, implies demand for temperature-sensitive inputs such as peroxides and ammonia derivatives that require controlled storage beyond ambient norms. Alberta’s Petrochemicals Incentive Program has disbursed sizable grants to anchor downstream investments, which increases the need for HAZMAT-certified, rail-served storage with humidity control, engineered spill containment, and advanced suppression systems. Cando Rail’s CAD 200 million Sturgeon Terminal expansion supports longer unit trains and higher polymer throughput, driving adjacent demand for railcar cleaning chemicals and inhibitors in certified facilities integrated within the terminal precinct. As these assets sequence into operation, the Canada chemical warehousing market is aligning capacity toward temperature-controlled bays, emissions monitoring, and integration with hydrogen and capture value chains.

Mining Industry Chemical Demand

Natural Resources Canada’s 2024 update outlines a midstream processing gap for lithium hydroxide, nickel sulfate, and graphite needed for domestic battery supply chains, which translates into sustained reagent demand and the need for specialized storage footprints in the Canada chemical warehousing market. Lithium hydroxide conversion and nickel sulfate production require significant volumes of acids and alkalis, which in turn necessitate segregated zones, corrosion management, and temperature control under TDG requirements. Mining operators are shifting toward lower-toxicity reagents to meet evolving environmental standards, yet many of these products still carry toxic classifications and refrigerated storage parameters that only a subset of facilities can meet. This shift favors warehouses with cold rooms, real-time SDS access, and integration with CANUTEC’s emergency protocols, creating a capability premium in the Canada chemical warehousing market. Positioning near Ontario, Quebec, and British Columbia battery corridors is reinforcing demand for intermodal links serving both inbound reagents and outbound processed materials.

Agricultural Sector Chemical Requirements

Statistics Canada recorded a 7.4% month-over-month decline in January 2025 chemical subsector sales due to plant maintenance and off-season demand for pesticide and fertilizer products, underscoring how seasonality drives volatility in the Canada chemical warehousing market. Fertilizer shipment data shows that a majority of annual volume concentrates in the March to June window, which requires sizable spring throughput capacity, while winter vacancy raises fixed cost burdens. Flexible, multi-client arrangements help smooth peaks by blending agrochemical volumes with mining and industrial flows to stabilize utilization over the year in the Canada chemical warehousing market. Regulatory uncertainty around Maximum Residue Limits and ongoing PMRA processes has also led to stockpiling behaviors in certain periods, spiking storage demand even when field application lags. These patterns reward operators in Prairie hubs, and Ontario-Quebec produce regions that can scale certified capacity on short notice while remaining integrated with rail and port nodes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vast Geographic Distances and Low Population Density | -0.7% | National, acute in northern territories, rural Prairies, and remote mining belts | Long term (≥ 4 years) |

| Extreme Winter Climate Challenges | -0.5% | Severe in northern regions, episodic in southern Ontario and Quebec | Short term (≤ 2 years) |

| Interprovincial Trade Barriers | -0.3% | Affects all provinces, with friction along Alberta-British Columbia and Ontario-Quebec corridors | Medium term (2-4 years) |

| Limited Chemical Manufacturing Base | -0.4% | Eastern Canada is reliant on imports, and Western Canada is weighted to upstream petrochemicals. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vast Geographic Distances and Low Population Density Constrain Network Economics

Canada’s distribution economics remain challenged by low population density across a large landmass, which increases reliance on long rail and road corridors that lengthen replenishment cycles for regulated inventories in the Canada chemical warehousing market. The Port of Vancouver’s share of national cargo tonnage and its distance from central manufacturing centers shape rail-dependent routes to Ontario and Quebec, increasing planning horizons and inventory buffers. Mining customers in northern Quebec often maintain longer safety stocks at inland warehouses due to seasonal access limits tied to winter roads and marine closures, which raises working capital requirements while protecting continuity. Rail-connected inland expansions, such as Quadra’s Malartic site enhancements, illustrate the infrastructure redundancy needed to serve smaller populations in remote zones where chemical demand is mission-critical. These constraints tilt the Canada chemical warehousing market toward operators that can integrate transload, heated storage, and on-site railcar handling at strategic inland nodes.

Extreme Winter Climate Challenges Increase Operating Costs and Restrict Chemical Specifications

Environment and Climate Change Canada’s 2025-2026 outlook underscores variable winter conditions across Canada, which complicates temperature control and handling requirements for sensitive products in the Canada chemical warehousing market. The City of Toronto’s winter operations budgeting and salt programs illustrate significant seasonal demand for deicing chemicals, concentrating throughput between November and March across urban networks. Lithium-ion battery electrolytes and comparable materials require 15°C to 25°C storage parameters that are difficult to maintain during deep cold snaps in inland industrial zones, which increases facility energy loads and monitoring needs. Maintaining 20°C±2°C for flammable and corrosive classes in cold climates raises utility costs and informs pricing models, pushing a share of demand toward near-port nodes where milder temperatures help reduce energy intensity. These dynamics accelerate specification upgrades such as engineered containment and continuous telemetry, especially in British Columbia’s Lower Mainland, where port adjacency and climate control can be combined to lower total landed cost for time-sensitive products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialty Facilities Lead Amid Petrochemical and Battery Ecosystems

Specialty chemical warehouses commanded 31.79% of the Canada chemical warehousing market share in 2025, while temperature-controlled chemical warehouses are forecast to expand at a 7.41% CAGR through 2031 within the Canada chemical warehousing market size. These trends are linked to investments in Alberta’s petrochemical corridor and battery supply chains in Ontario, Quebec, and British Columbia, which require humidity control, segregation, and emissions monitoring beyond ambient bulk storage norms. Path2Zero’s forthcoming polyethylene output and the Sturgeon Terminal scale-up are increasing demand for compliant, rail-served storage integrated with unit train operations and precise environmental controls. General warehousing continues to serve caustic soda and sodium chlorate for pulp and industrial customers, yet customers are raising expectations for lot traceability and visibility that are native to specialty configurations. The Canada chemical warehousing market is therefore bifurcating between ambient bulk sites and high-specification facilities aligned to net-zero projects and critical materials processing.

HAZMAT warehouses certified under TDG host the bulk of flammable, corrosive, and oxidizing inventories and face a lengthy certification path that includes municipal fire code approvals, spill containment capacity, and advanced suppression systems integrated with CANUTEC. Building greenfield HAZMAT capacity in British Columbia can take up to two years with multi million dollar compliance investments, which favors experienced operators and capitalized logistics providers in the Canada chemical warehousing market. Temperature-controlled chemical warehouses for lithium hydroxide, nickel sulfate, and sensitive solvents need refrigeration assets sized for industrial duty and continuous monitoring, which encourages cross-pollination of cold chain best practices from food logistics into chemical storage. These facilities are typically located near intermodal corridors and industrial hubs to reduce handling risk and improve service time for regulated inventories. The Canada chemical warehousing industry in this segment is defined by regulatory competencies, rail connectivity, and specialized building systems that enable higher pricing power and lower vacancy cyclicality.

By Chemical Type: Balancing Growth, Safety, and Environmental Compliance

Flammable liquids represented 39.74% of the Canada chemical warehousing market share in 2025, while toxic substances are forecast to grow at an 8.41% CAGR through 2031 as new mining and pharmaceutical inputs scale. Flammable inventories include solvents for paints and coatings, lubricants and fuel additives, and petrochemical feedstocks stored in controlled environments that meet emissions and fire suppression standards. West coast and Ontario-Quebec distribution hubs serve domestic demand, and U.S.-bound flows under USMCA, supported by blending rooms, rail spurs, and on-site telemetry for whole-site tank monitoring. Corrosives such as sulphuric and hydrochloric acid serve mining leaching and oilfield applications, while recycling trends and closed-loop systems shift some storage from virgin acids to interim holding for reprocessing. The Canada chemical warehousing market continues to adapt foam systems and suppression strategies in line with evolving environmental rules to limit PFAS releases while meeting NFPA-aligned performance thresholds.

Toxic substances are gaining share due to the transition toward alternative reagents such as glycine and thiosulfate in mining and the rise of pharma intermediates, which adds demand for refrigerated bays and stringent documentation controls. These products often require 2°C to 8°C storage, continuous temperature logging, and chain-of-custody records integrated with warehouse management systems, which narrows the pool of eligible facilities. Facility additions by niche providers in British Columbia and the Prairies reflect this shift, giving customers local pickup options and shorter lead times that align with seasonality and project timelines. As compliance and customer quality requirements increase, the Canada chemical warehousing market size allocation within toxic, corrosive, and oxidizer categories will reflect the capital intensity and regulatory depth of the served end markets. The Canada chemical warehousing industry remains anchored to TDG classifications, site audits, and insurer requirements that set the bar for facility design and operations.

By End-User Industry: From Basic Industrial Warehousing to Climate-Controlled Pharma Facilities

Basic chemicals manufacturing accounted for 30.41% share in 2025, while pharmaceuticals and life sciences are projected to expand at a 7.78% CAGR through 2031, reshaping storage specifications toward clean, temperature-controlled, and quality-managed footprints in the Canada chemical warehousing market. Basic chemicals support pulp, water treatment, and industrial segments using rail-served ISO tanks and transloads at customer sites, which favors warehouses with direct rail access and heated bays in cold climates. This segment faces rising expectations for traceability and real-time visibility, which pushes ambient facilities to invest in software and process upgrades or cede share to specialty operators. Agrochemicals remain seasonal, with Prairie warehouses managing heavy spring throughput and winter slack, while policy-driven stockpiling can lift mid year utilization. The Canada chemical warehousing market is also seeing durable demand from oil and gas chemicals near Alberta’s Industrial Heartland and extraction zones that require certified storage and quick-response services.

Pharmaceutical and life sciences growth depends on 2°C to 8°C rooms, humidity control, and 21 CFR Part 11 compliant systems, which eliminates the bulk of legacy ambient warehouses from contention for these contracts. Specialty chemicals manufacturing requires segregated lots, FIFO controls, and customer-specific labeling, which justifies premium storage rates and smaller inventory blocks than commodity chemicals. Paints, coatings, and adhesives concentrate around Ontario and Quebec, while food and feed additives carry certification needs that require dedicated zones within multi-client sites. The Canada chemical warehousing industry continues to add expertise in regulated documentation and sampling as customer audits intensify across pharma, food, and electronics supply chains. These specifications, together with rail and port adjacency, remain the primary differentiators in contract awards for the Canada chemical warehousing market.

Geography Analysis

The Canada chemical warehousing market tracks four logistics geographies, with the Pacific Gateway handling significant export value, Prairie hubs tied to petrochemical and fertilizer flows, Central Canada serving the bulk of imports, and Atlantic routes linking to Europe and offshore energy. British Columbia’s Lower Mainland has TDG-certified HAZMAT capacity near the Port of Vancouver, and recent facility openings in Abbotsford have expanded rail-capable, blending-ready storage to support cross-border and intermodal flows. Prince Rupert has a construction pipeline for logistics projects, including an export terminal to handle hydrocarbons and bulk liquids, which will require integrated tank farms and warehouse transloads as capacity returns after a period of lower throughput. This infrastructure is increasing demand for compliant warehouse capacity near ports and intermodal hubs, especially for time-sensitive and regulated chemical inventories..

Alberta and Saskatchewan dominate petrochemical and fertilizer warehousing with near-plant and rail-adjacent nodes, supported by grants and large private investments that anchor demand for compliant storage and transloads. Fertilizer production and shipments require seasonal surge planning, often compressing a majority of volume into spring seeding windows and leaving winter lulls, which the Canada chemical warehousing market mitigates with flexible space and cross-customer balancing. Rail-connected expansions in Quebec, such as Malartic, serve mining customers in Val d’Or and link to CN mainlines to enhance reliability and reduce greenhouse gas emissions relative to road movements. Central Canada faces urban industrial land constraints and regulatory layers that raise costs, encouraging new construction in ex urban sites with lower land prices and scalable footprints while keeping drayage reasonable to port and intermodal nodes. As these corridors evolve, the Canada chemical warehousing market size will continue to tilt toward rail-integrated, certified platforms with climate control where needed.

Atlantic Canada maintains niche chemical warehousing for marine fuels, offshore energy support, and European trade, backed by new port investments in green shipping corridors and crane infrastructure that will accelerate cargo handling and enable alternative-fuel bunkering. Northern territories require isolated depots with elongated safety stocks due to extreme winters and multi-month marine closures, which raise working capital needs despite low total volumes. Regulatory variations across provinces, including British Columbia’s WorkSafeBC rules and Quebec’s labeling requirements, reinforce the need for region-specific standard operating procedures in national networks. The Canada chemical warehousing market benefits from operators that can integrate compliance, operations, and capital planning tailored to each corridor’s climate and regulatory profile.

Mordor Intelligence tracks the chemical warehousing market across other major regions such as North America, Europe, and Middle East, with additional country-level coverage spanning Mexico, Italy, United Kingdom, Japan, China, and India, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Canada chemical warehousing market shows low concentration, with multinational logistics providers and Canadian-owned specialists sharing the landscape through integrated forwarding, rail links, and certified storage. Global players deploy advanced warehouse management and control tower visibility, while regional operators focus on regulatory agility and port-proximate capacity that aligns with TDG requirements. DHL’s lithium battery handling scale and Centers of Excellence illustrate how data-driven workflows and specialized training are becoming competitive levers in the high-spec segment. Regional leaders emphasize near-port HAZMAT footprints with segregation and climate controls that support fast transloads and lower drayage risk. Compliance and inspections under the TDG program set an entry barrier that rewards operators with documentation depth and incident readiness integrated with CANUTEC.

White-space opportunities are concentrated in temperature-controlled storage for battery-grade chemicals, circular chemical logistics for recycled acids and solvents, and lower-emission facility design that swaps HFC systems for natural refrigerants while integrating on-site renewables where feasible. Congebec’s cross-province cold chain network and planned Calgary facility near CN’s logistics park show how cold chain expertise can port to chemicals that need tighter ranges and validated monitoring. Producer-led storage integration is rising as chemical manufacturers seek tighter quality control around intermediates and finished goods, which shifts a portion of demand toward on-site or near-site warehousing. These moves align with the Canada chemical warehousing market’s pivot toward higher-spec, lower-emission, and digital-first operations.

Capital discipline and compliance cadence are becoming defining capabilities as operators allocate funds to growth and maintenance across high-spec sites. Announced network expansions, rail-yard adjacency, and LEED-oriented builds in Ontario show how ex-urban siting can unlock cubic capacity at competitive land costs while maintaining connectivity to consumer and industrial belts. Port authorities are channeling grants into green corridors, yard electrification, and crane capacity, which will reduce turn times and encourage warehouse investment near berths and rail. As operators scale climate-controlled rooms, spill containment, and specialty suppression systems, the Canada chemical warehousing market is expected to differentiate more clearly between ambient bulk platforms and high-spec HAZMAT and pharma-grade nodes. These patterns are consistent with maturing safety protocols and rising documentation requirements across end uses.

Canada Chemical Warehousing Industry Leaders

Deutsche Post DHL Group

Kuehne + Nagel

R&S Logistics

XPO Logistics

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Congebec, in partnership with CN, will develop a cold storage facility in Rocky View County, Alberta, near CN's Calgary Logistics Park. The facility will streamline container handling between the Port of Vancouver and Canadian markets, targeting temperature-sensitive goods and integrating CN's refrigerated programs.

- April 2025: Congebec and Bradner Cold Storage merged, forming a coast-to-coast cold storage network with 16 facilities across six provinces. The merger strengthens Canada's supply chain and supports food manufacturers, with plans for North American expansion driven by export opportunities and trade agreements like CPTPP.

- November 2024: Quadra Group Ltd., with Octium Solutions Inc., expanded rail infrastructure at its Malartic, Quebec site. The project added rail capacity, a heated warehouse, and on-site railcar shunting, enhancing bulk chemical transload services for mining clients and supporting emission reduction goals.

- June 2024: Univar Solutions LLC opened a distribution facility in Abbotsford, British Columbia, near the U.S. border. The site features expanded storage, rail capacity, real-time inventory systems, and blending rooms, with a focus on sustainability and efficient product delivery.

Canada Chemical Warehousing Market Report Scope

The Canada Chemical Warehousing Market Report is Segmented by Warehouse Type (General, Specialty Chemical, HAZMAT, and Temperature-Controlled), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, and Others), by End-User Industry (Basic Chemicals, Specialty Chemicals, Pharmaceuticals, Agrochemicals, Paints & Coatings, Food Additives, Oil & Gas, and Others), and Geography (Canada). Market Forecasts are in Value (USD).

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the five-year outlook for the Canada chemical warehousing market?

The Canada chemical warehousing market size is USD 4.05 billion in 2026 and is expected to reach USD 5.45 billion by 2031 at a 6.1% CAGR.

Which warehouse type is growing fastest in Canada chemical warehousing?

Temperature-controlled chemical warehouses are projected to grow fastest at a 7.41% CAGR through 2031, supported by battery and life sciences demand

How is USMCA influencing the Canada chemical warehousing market?

The Chemical Sectoral Annex is streamlining regulatory cooperation and shifting demand to border-adjacent nodes like Windsor-Detroit and the Pacific Gateway

Which chemical categories dominate storage needs in Canada?

Flammable liquids lead by share, while toxic substances are the fastest growing due to critical minerals processing and pharma inputs

What corridors are most critical for the Canada chemical warehousing market?

British Columbia’s Lower Mainland near the Port of Vancouver, Alberta’s Industrial Heartland, Prairie fertilizer hubs, and Ontario-Quebec manufacturing belts are the key nodes, with capacity emerging in Prince Rupert and targeted upgrades in Halifax

Which regulations most affect facility design and operations?

Transport Canada’s TDG regulations, municipal fire codes, WHMIS, and WorkSafeBC rules drive certification, emergency planning, and storage configurations

Page last updated on: