Asia-Pacific Chemical Warehousing And Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

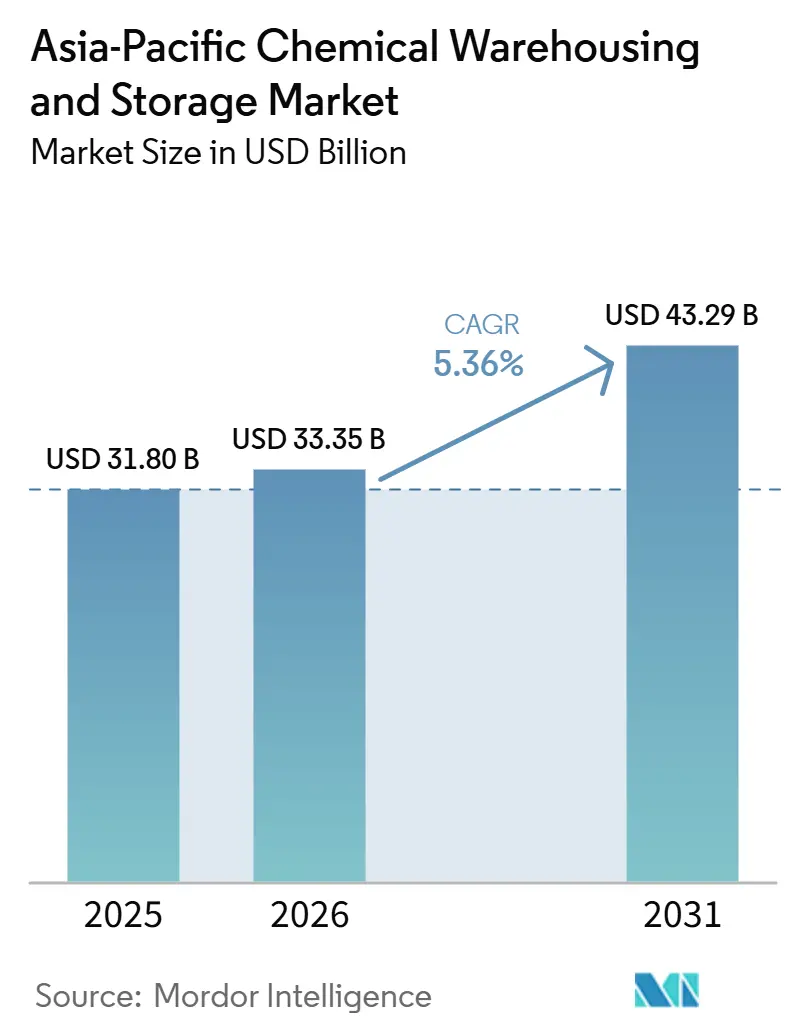

| Base Year Market Size (2025) | USD 31.80 Billion |

| Market Size (2026) | USD 33.35 Billion |

| Market Size (2031) | USD 43.29 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

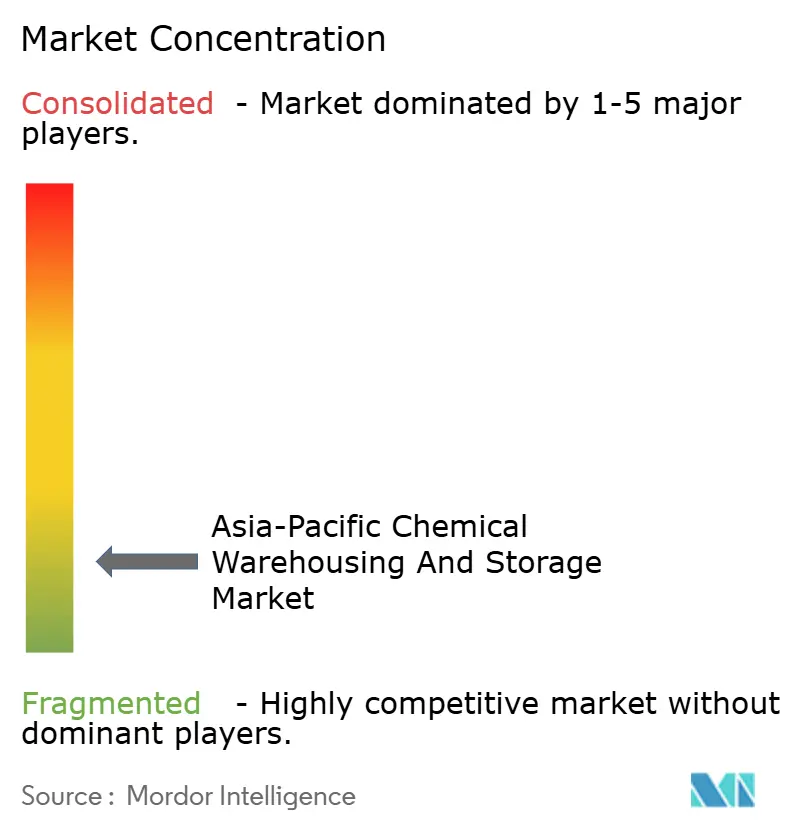

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Chemical Warehousing And Storage Market Analysis by Mordor Intelligence

The Asia-Pacific Chemical Warehousing And Storage Market size is projected to be USD 31.80 billion in 2025, USD 33.35 billion in 2026, and reach USD 43.29 billion by 2031, growing at a CAGR of 5.36% from 2026 to 2031.

Regulatory reinforcement around hazardous substances, stronger cold-chain specifications for pharmaceuticals, and digitization of inventory visibility are shaping procurement and location choices for the Asia-Pacific chemical warehousing and storage market. Capacity is tilting toward temperature-controlled and specialized storage as biologics and electronic-grade chemistries take a larger share of regional production and trade. Feedstock strategies are pivoting toward ethane and LNG-linked logistics, which are pulling new investment into terminal and cryogenic storage ecosystems that connect upstream and downstream nodes. Land scarcity on coastal corridors is compressing footprints and pushing operators inland, which accelerates the adoption of high-bay automation to maintain service levels without proportional land take. Partnerships between asset owners and third-party logistics specialists continue to scale, which raises the bar on compliance and real-time monitoring across the Asia-Pacific chemical warehousing and storage market.

Key Report Takeaways

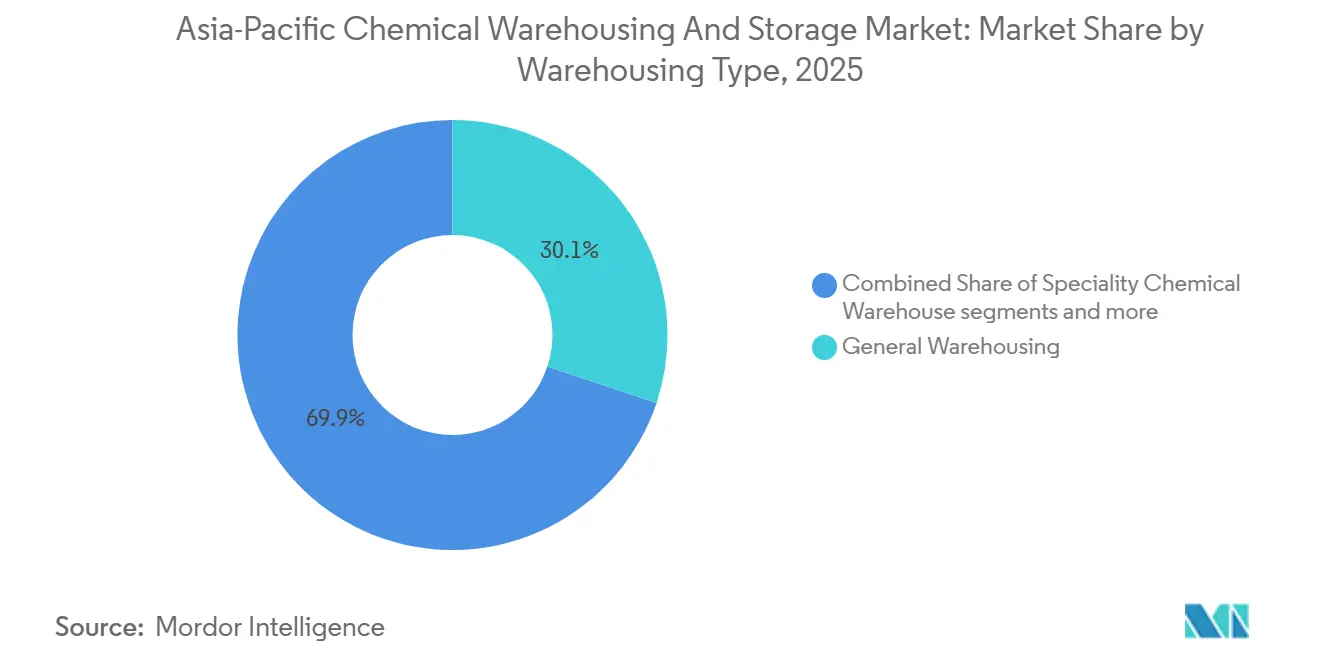

- By warehouse type, general warehousing led with 30.12% of the Asia-Pacific chemical warehousing and storage market share in 2025. Temperature-controlled facilities are projected to expand at a 6.81% CAGR through 2031, supported by cold-chain mandates and specialty handling needs.

- By chemical type, flammable liquids held a 37.68% of the Asia-Pacific chemical warehousing and storage market size in 2025. Toxic substances are forecast to grow at a 6.34% CAGR to 2031 on the back of agrochemicals and advanced materials.

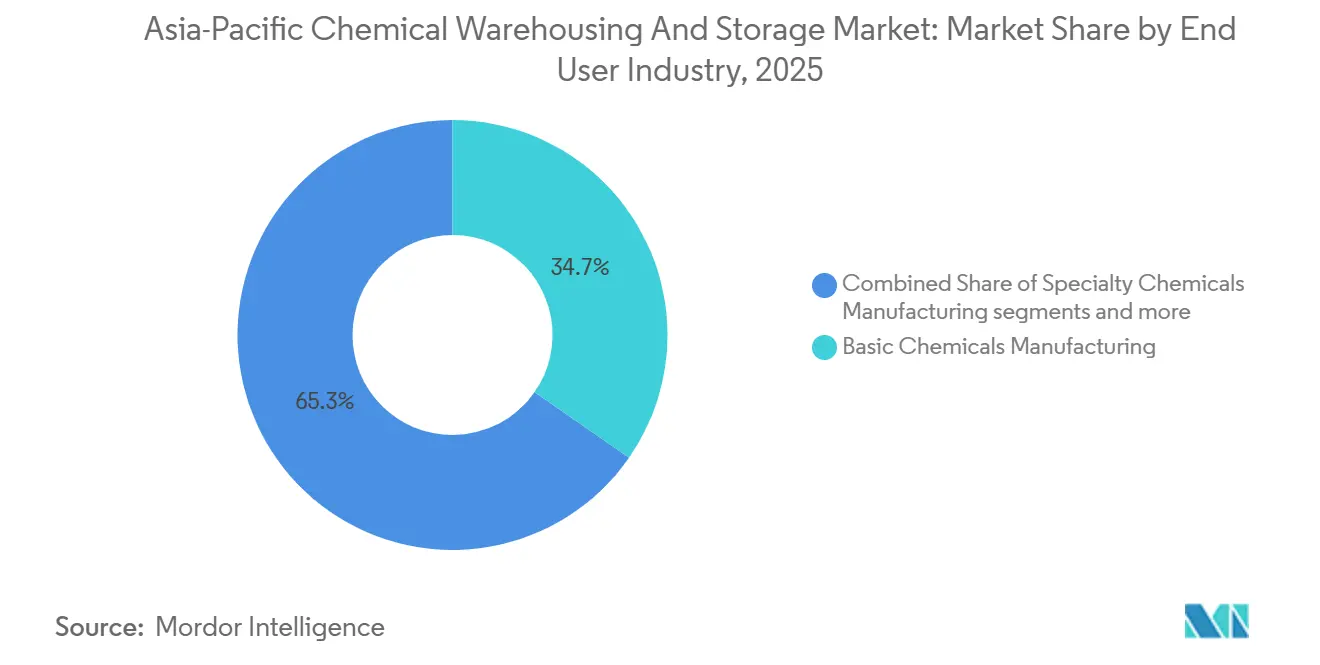

- By end-user industry, basic chemicals accounted for 34.67% of the Asia-Pacific chemical warehousing and storage market share in 2025; pharmaceuticals and life sciences are expected to post a 7.23% CAGR through 2031.

- By geography, China commanded 57.30% market share in 2025; India is set to grow the fastest at a 7.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Chemical Warehousing And Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical cold chain and life sciences manufacturing growth | +0.8% | APAC core, notably India, China, Singapore, and spill-over ASEAN | Medium term (2-4 years) |

| Accelerating outsourcing to third-party logistics (3PL) providers | +0.7% | Global model, concentrated in China, India, Southeast Asia | Short term (≤ 2 years) |

| Strategic LNG-to-chemicals hub investments | +0.9% | Thailand, Vietnam, and coastal China | Long term (≥ 4 years) |

| Build-own-operate (BOO) and build-operate-transfer (BOT) project models | +0.6% | Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Growth in specialty chemicals and advanced materials manufacturing | +1.0% | China, South Korea, Taiwan, Japan | Medium term (2-4 years) |

| E-commerce and chemical distribution to small-scale industries | +0.5% | Urban hubs in China Tier-2/3, India metros, ASEAN capitals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical Cold Chain and Life Sciences Manufacturing Growth

Cold-chain logistics is reshaping storage specifications as biologics and vaccine flows demand facilities that can maintain distinct temperature zones with tight monitoring and alerting. Regional operations are deploying rental-asset pooling to accelerate turns and limit capital lock-up, illustrated by one-way pallet shipper networks now spanning multiple Asia-Pacific hubs for clinical materials. Real-time reefer telemetry with predictive alerts has become standard in many tenders, and hour-by-hour monitoring is now embedded into procurement checklists across the Asia-Pacific chemical warehousing and storage market. Environmental Monitoring Systems with rapid alarms, as seen in Taiwan biologics storage, are increasingly specified in requests for proposals and help operators meet Good Distribution Practice expectations[1]Ministry of Emergency Management of China, “Technical Requirements for Storage Safety of Hazardous Chemical Reagent Warehouses (Draft for Comment),” MEM China, mem.gov.cn. Network buildouts in India and Southeast Asia are aligning port-proximate capacity with inland cold rooms to reduce handovers and cycle time for time- and temperature-sensitive shipments. Cold-chain square meters across APAC continue to expand under strong food and pharma pull, which supports rate resilience and utilization for temperature-controlled nodes serving the Asia-Pacific chemical warehousing and storage market.

Accelerating Outsourcing to Third-Party Logistics (3PL) Providers

Chemical producers are consolidating warehousing and transportation with lead logistics partners to gain visibility, compliance readiness, and scale-based cost control. A prominent example is the selection of a single regional leader to orchestrate tens of thousands of annual shipments across air, ocean, and road while using integrated platforms for lane risk and carrier vetting, which demonstrates how outsourcing de-risks complex networks in the Asia-Pacific chemical warehousing and storage market. Draft regulations in China are formalizing lifecycle IT tracking and electronic connectivity with authorities for dangerous goods, which is pushing smaller shippers toward 3PL partnerships that already operate compliant systems. Outsourcers are also bundling value-added services like repackaging and documentation management using specialized chemical workflows, which shortens lead times and reduces exception costs in the Asia-Pacific chemical warehousing and storage market. Network expansion by regional operators into India and Southeast Asia is strengthening the interplay between port-based nodes and inland distribution centers that support higher service reliability at scale.

Strategic LNG-to-Chemicals Hub Investments

Long-term storage and handling agreements for ethane and related feedstocks are catalyzing tank infrastructure projects that reshape downstream logistics footprints. In Thailand, a multi-year ethane storage program with a 15-year customer agreement is scheduled to deliver new capacity at a major industrial hub, reinforcing supply security and crystallizing a feedstock-flexibility strategy for petrochemical complexes that anchor the Asia-Pacific chemical warehousing and storage market. These investments reduce dependence on naphtha-only systems and enable portfolio producers to balance between ethane and other streams, which has implications for cryogenic tank maintenance routines and safety management. The safety lens is sharpening at coastal sites managing hazardous cargoes, with risk zoning research and incident analyses informing planning, emergency readiness, and land-use policy. Additional nodes in coastal China are expanding LNG and related feedstock handling with tighter integration to specialty and derivative production, which increases the importance of segregated storage for materials with nuanced temperature and contamination controls in the Asia-Pacific chemical warehousing and storage market.

Build-Own-Operate (BOO) and Build-Operate-Transfer (BOT) Project Models

Private capital and concession-based models are filling infrastructure gaps where public funding is constrained or where host governments seek to accelerate timelines for hazardous-materials storage. Long-duration storage and handling agreements tied to feedstock infrastructure illustrate how take-or-pay and fixed-capacity models can underpin return profiles in the Asia-Pacific chemical warehousing and storage market. At the distribution edge, build-to-suit investments aligned to large anchor customers are extending cold and hazmat capacity near ports and inland corridors as operators replicate concession-like predictability by locking in multi-year commitments. Private greenfield projects also standardize advanced safety systems, including automated foam-based sprinklers and warehouse management systems for chemical inventory, to meet modern tender requirements. As regulators add digital traceability conditions for hazardous chemicals, BOO and BOT operators with integrated IT and training frameworks will be better positioned to win concessions across the Asia-Pacific chemical warehousing and storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe land scarcity in coastal industrial corridors | -0.4% | Coastal China including Bohai Bay, Jiangsu, and high-density hubs like Singapore and Mumbai | Long term (≥ 4 years) |

| Chronic shortage of trained hazmat handling personnel | -0.5% | India, Southeast Asia, and select Japan sub-markets | Medium term (2-4 years) |

| Escalating insurance premiums following major incidents | -0.3% | Regional impact following incident clusters | Short term (≤ 2 years) |

| High capital intensity and long payback periods | -0.6% | Greenfield builds in India, Vietnam, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Severe Land Scarcity in Coastal Industrial Corridors

Coastal industrial belts in Asia are tightening buffer zones and risk overlays, which reduces the inventory of land parcels eligible for hazardous-materials storage. Peer-reviewed analysis of China’s coastal risk zones shows a clear contraction of permitted industrial spaces as safety-distance rules take hold, which elevates land prices and complicates expansion plans for the Asia-Pacific chemical warehousing and storage market. Operators are responding with high-bay racking, automation, and vertical density to offset constrained footprints while maintaining service levels and safety envelopes. Redevelopments are facing zoning and community constraints, and networks are rebalancing inland, which adds drayage and intermodal costs but secures buildable land. Cold-chain locations in mature metros are running tight utilization, which amplifies the premium on certified refrigerated pallet positions and creates a durable value gap with ambient storage. Over the long term, projects that blend automation, safety certification, and smart energy management will carry a cost advantage when scarce land meets higher regulatory thresholds in the Asia-Pacific chemical warehousing and storage market.

Chronic Shortage of Trained Hazmat Handling Personnel

Skill shortages in safe handling of hazardous chemicals continue to weigh on throughput, certification cycles, and insurance outcomes. Training capacity gaps are visible in emerging Southeast Asian markets, where international partners have stepped in to deliver response and decontamination curricula under chemical emergency programs. Regulatory consultations in China are specifying tighter requirements for warehousing and reagent storage, which emphasize competence, documentation, and traceability throughout the hazardous-chemical lifecycle. The resulting compliance bar raises the demand for certified supervisors and trained first responders, yet accredited training slots and simulators remain limited in many ports and industrial parks. Companies are increasingly standardizing simulated drills and 24/7 control-room monitoring to harden operations, but staffing depth and recertification remain persistent constraints for the Asia-Pacific chemical warehousing and storage market. Over time, scale operators that invest in structured training pathways will mitigate labor bottlenecks and capture premium business with higher compliance sensitivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Versatile General Warehousing Anchors the Base While Temperature-Controlled Gains Momentum

General warehousing captured 30.12% of the Asia-Pacific chemical warehousing and storage market share in 2025, reflecting broad suitability for commodity solvents, base oils, and intermediate chemicals subject to ambient conditions. Temperature-controlled facilities are pacing growth at 6.81% CAGR through 2031 as biologics, vaccines, and sensitive formulations require mapped refrigeration zones, validated sensors, and event logging. Operators continue to deploy cold rooms alongside ambient bays in the same compound to manage mixed portfolios without compromising product integrity. Purpose-built distribution hubs with sub-25°C rooms, foam-based automated sprinklers, and WMS-integrated order picking reflect a structural pivot toward premium infrastructure in high-volume nodes. Cold-chain utilization remains tight across mature metros, which sustains rent differentials relative to dry storage and supports new-build economics. Over the forecast window, the Asia-Pacific chemical warehousing and storage market will likely see greater adoption of integrated ambient-and-cold sites near ports and airports to trim handovers and reduce exception risk for sensitive loads.

The Asia-Pacific chemical warehousing and storage market size for temperature-controlled facilities is projected to expand as certification frameworks tighten around GDP, ISO 9001, and ISO 45001. Real-time telemetry, in referring to logistics and predictive alerting are becoming a default feature in new tenders, which strengthens the business case for IoT-enabled cold rooms and continuous monitoring in storage. Parallel standard-setting for toxic-substance storage is raising baseline structural requirements for fire resistance, ventilation, and seismic anchoring, which is lifting capex needs and widening performance spreads between legacy and Grade A facilities. These preferences are reshaping the Asia-Pacific chemical warehousing and storage industry profile as customers weigh multi-year commitments that bundle storage, monitoring, and compliance reporting. Facility-level investments in temperature mapping, zone segregation, and controlled airflow are also enabling operators to stretch usable capacity per square foot while upholding audit requirements. The net effect is a steady mix shift toward certified cold and specialty-ready environments within the Asia-Pacific chemical warehousing and storage market.[2]Global Cold Chain Alliance, “Deep Dive: The Asia-Pacific Cold Chain Market in 2025,” GCCA, gcca.org

By Chemical Type: Flammable Liquids Remain the Base While Toxic Substances Accelerate

Flammable liquids led the portfolio with a 37.68% share in 2025, supported by continuous refinery and petrochemical flows that align well with ambient and explosion-protected storage. Toxic substances are the fastest-growing cohort at a 6.34% CAGR through 2031 as agrochemical actives, electronic chemicals, and other reactive or health-hazardous materials scale in the region. Storage design is evolving toward dual-containment, oxygen control, and segregated rooms with enhanced ventilation to handle reactive or highly toxic inventories, raising technical requirements across the Asia-Pacific chemical warehousing and storage market. Companies are adding automated drum-filling, MDI control rooms, and round-the-clock monitoring to meet customer and insurer expectations around hazardous materials. Cryogenic tank infrastructure linked to ethane and other feedstocks will complement the broader tank farm and drum-storage mix serving diversified chemical output in Southeast Asia.

Compliance frameworks converged on stricter co-storage rules, labeling, and traceability, which is driving the segmentation of storage bays and cabinets for special classes such as self-reactivity and organic peroxides. Practical execution now depends on digital SDS libraries and WMS logic that prevent incompatible placement, a capability that is rapidly standardizing for premium operators in the Asia-Pacific chemical warehousing and storage market. Cleanroom-compatible drum and IBC storage has become a core requirement across the Asia-Pacific chemical warehousing and storage industry, where ultra-pure grades serve semiconductor or battery production. Investments in training and emergency response are also rising to match the risk profile of toxic and reactive stocks, which improves audit resilience and reduces incident downtime. As procurement teams prioritize reliability and traceability, specialized toxic-substance storage will expand faster than bulk flammables within the Asia-Pacific chemical warehousing and storage market.

By End-User Industry: Basic Chemicals Anchor Demand While Pharmaceuticals and Life Sciences Drive Premium Growth

Basic chemicals accounted for 34.67% of demand in 2025, reflecting the region’s strong base in olefins, aromatics, and other foundational products that require scale storage near refineries and petrochemical complexes. Pharmaceuticals and life sciences are the fastest-growing end-user at a 7.23% CAGR through 2031 due to rising biologics output and vaccine distribution that depend on validated cold rooms, chain-of-custody controls, and continuous telemetry. Specialized courier networks and pooled rental assets are improving turnaround and lowering capital intensity for clinical and high-value cargoes, which sustains higher storage rates for certified facilities. Cold-chain telemetry that provides hourly temperature stamps and predictive alerts is now embedded across many customer programs, which lifts expectations for storage monitoring in the Asia-Pacific chemical warehousing and storage market. Inland distribution centers with cold rooms are also scaling in India to connect domestic pharma corridors with port gateways, improving service reliability and throughput.

The Asia-Pacific chemical warehousing and storage market size linked to pharmaceuticals and life sciences is set to grow at 7.23% CAGR through 2031 as sponsors and contract manufacturers expand in key hubs. Dual-use cold capabilities also serve adjacent categories such as food-grade additives, which help amortize capital and extend cold workflows across multiple verticals. Leading logistics partners are expanding space and adding healthcare-specific programs to meet storage and handling requirements with documented compliance. The Asia-Pacific chemical warehousing and storage industry is consolidating higher-value work around operators that can integrate certifications, monitoring, and response plans. Over time, this mix shift will reinforce premium rate structures for GDP-compliant assets and broaden the gap with general ambient storage in the Asia-Pacific chemical warehousing and storage market.

Geography Analysis

China led the region with 57.30% share in 2025 as large-scale chemical production and dense coastal logistics underpin high storage utilization. The Asia-Pacific chemical warehousing and storage market size in China is anchored by coastal nodes that are tightening land-use and buffer rules, which are pushing warehouses toward vertical density and higher automation to sustain throughput within smaller footprints. Regulatory consultations are refining hazardous-chemical lifecycle tracking and storage requirements, including electronic connectivity with authorities and technical specifications for reagent warehousing. Supply-chain strategies that combine port-based tanks with inland depots reduce exposure to coastal land scarcity while preserving service levels. As producers tilt toward higher-value derivatives, specialty-ready storage and segregated bays are becoming a larger slice of the Asia-Pacific chemical warehousing and storage market in China.[3]Ministry of Emergency Management of China, “Technical Requirements for Storage Safety of Hazardous Chemical Reagent Warehouses (Draft for Comment),” MEM China, mem.gov.cn

India is the fastest-growing national market with a 7.87% CAGR through 2031, as an expanding manufacturing base and pharmaceuticals scale fuel new capacity requirements. Port-adjacent facilities with sub-25°C zones, foam-based fire suppression, and modern WMS are being added near Mumbai to serve both export flows and domestic distribution. Network expansion by global and regional logistics providers is raising service consistency and safety standards across major Indian corridors. Inland hubs are gaining traction where environmental and land constraints slow coastal builds, which redistributes the Asia-Pacific chemical warehousing and storage market toward multi-node footprints that balance drayage costs with faster approvals.

Mature markets like Japan and South Korea display tight cold-chain utilization and a steady push for automation and safety upgrades to extend the lifecycle of older facilities. High utilization for refrigerated storage in large metros supports sustained rental premiums and justifies redevelopment where land access and zoning allow. Singapore continues to act as a strategic transshipment and storage hub, while Southeast Asian nodes add cryogenic and hazardous-materials capacity tied to long-term feedstock and derivative strategies at major industrial estates. Australia and New Zealand occupy specialized roles that link temperature-controlled exports and certified hazmat storage to Asia-bound trade lanes, with updated standards for toxic-substance storage lifting baseline design and retrofitting needs. Across these sub-regions, the Asia-Pacific chemical warehousing and storage market is trending toward certified, sensor-rich, and denser footprints that deliver compliance and resilience.

Competitive Landscape

The market remains fragmented overall, although high-compliance, temperature-controlled, and specialty storage segments are increasingly consolidating among certified and capital-intensive operators. Multinationals are awarding integrated contracts to partners that can manage large, multi-country shipment portfolios with unified risk and visibility tools, which lock in repeat flows to those networks. Asset owners are upgrading cold rooms and hazardous bays with validated monitoring and response systems to meet tender requirements and insurer expectations. Companies that align facility capabilities with pharmaceutical and specialty-chemical workflows capture higher yields per pallet, strengthening the case for premium investments in the Asia-Pacific chemical warehousing and storage market.

Strategic moves cluster around long-term storage agreements, build-to-suit programs, and digital control towers. Ethane-linked storage capacity anchored by multi-year agreements in Thailand demonstrates how feedstock strategy translates into terminal buildouts that can reshape downstream logistics over a decade-plus horizon. In India, operators are adding Grade A chemical warehousing capacity with temperature-managed zones and automated safety systems close to major ports, which improves cycle times and meets modern compliance checklists. In Southeast Asia and India, regional providers are expanding their networks, leveraging customer-funded or concession-like frameworks to stabilize utilization at key strategic nodes.

Technology deployment is a central differentiator in the Asia-Pacific chemical warehousing and storage market as customers specify real-time monitoring and predictive alerting. Many pharmaceutical programs now standardize telemetry with hourly data and automated excursion alerts, elevating expectations for storage telemetry and cohesive documentation. Lead logistics partners are embedding validation, carrier compliance checks, and integrated dashboards into their chemical vertical solutions, which compresses exception handling and accelerates corrective actions. As regulators formalize lifecycle IT tracking and strengthen warehouse technical requirements, operators with integrated safety, digital, and training programs will consolidate higher-value volumes across the Asia-Pacific chemical warehousing and storage market.

Asia-Pacific Chemical Warehousing And Storage Industry Leaders

DHL Global Forwarding

Sinotrans

Toll Group

Kuehne + Nagel International AG

Yusen Logistics Co., Ltd. (Part of NYK Line)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: HOYER Group expanded the Shanghai site’s services for Covestro, commissioning automated drum-filling lines, temperature-controlled warehouses with ammonia refrigeration, and a 24/7 MDI control room under a renewed partnership.

- September 2025: Allcargo Supply Chain launched a 160,000 square foot Grade A chemical warehousing facility in Uran, Navi Mumbai, with sub-25°C cold storage, automated foam-based fire suppression, and advanced WMS, alongside plans to extend the network into additional Indian hubs.

- May 2025: Kuehne+Nagel was appointed lead logistics provider for Evonik across Asia-Pacific, managing about 70,000 annual shipments with integrated visibility and transport-management systems.

- March 2025: Royal Vopak reached final investment decision to build 160,000 cubic meters of ethane storage at Map Ta Phut, Thailand, under a 15-year agreement with PTT Global Chemical.

Asia-Pacific Chemical Warehousing And Storage Market Report Scope

The Asia-Pacific Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, Others), by End-user Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints, Coatings & Adhesives, Food & Feed Additives, Oil & Gas / Petrochemicals, Others), and by Geography (China, India, Japan, South Korea, Indonesia, Malaysia, Thailand, Vietnam, Philippines, Singapore, Australia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD Billion).

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Philippines |

| Singapore |

| Australia |

| Rest of Asia-Pacific |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific chemical warehousing and storage market?

The Asia-Pacific chemical warehousing and storage market size is USD 31.80 billion in 2025 and is forecast to reach USD 43.29 billion by 2031 at 5.36% CAGR over 2026-2031

Which segments are leading and growing the fastest within this space?

General warehousing led with 30.12% share in 2025, while temperature-controlled facilities are growing the fastest at a 6.81% CAGR through 2031.

Which chemical types dominate storage demand across APAC?

Flammable liquids held a 37.68% share in 2025, while toxic substances are the fastest-growing chemical class at a 6.34% CAGR to 2031.

Which end-user industries are shaping demand the most?

Basic chemicals accounted for 34.67% in 2025, while pharmaceuticals and life sciences led growth at a 7.23% CAGR through 2031 due to strict cold-chain and compliance needs.

Which countries are most important in capacity and growth terms?

China led with 57.30% share in 2025, and India is the fastest growing at a 7.87% CAGR through 2031.

What operational themes define competitiveness in APAC chemical storage?

Certified safety and cold-chain capabilities, real-time telemetry, high-bay automation, and long-term agreements with producers are the main differentiators supporting growth and resilience.

Page last updated on: