Europe Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

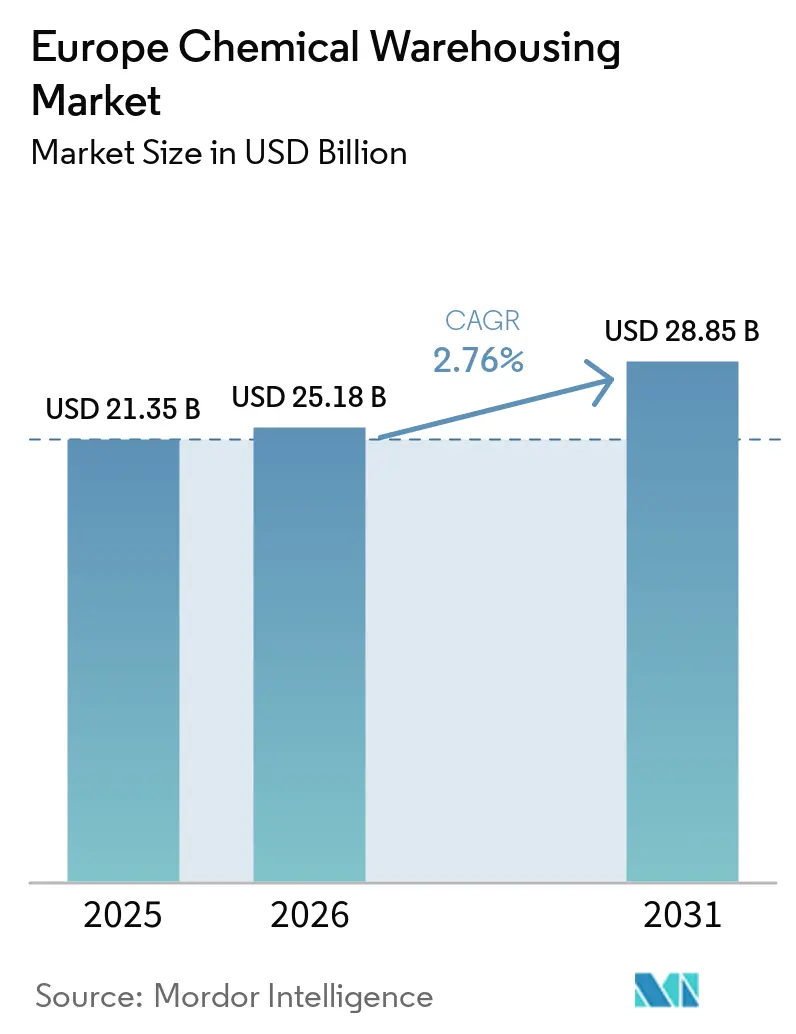

| Base Year Market Size (2025) | USD 21.35 Billion |

| Market Size (2026) | USD 25.18 Billion |

| Market Size (2031) | USD 28.85 Billion |

| Growth Rate (2026 - 2031) | 2.76% CAGR |

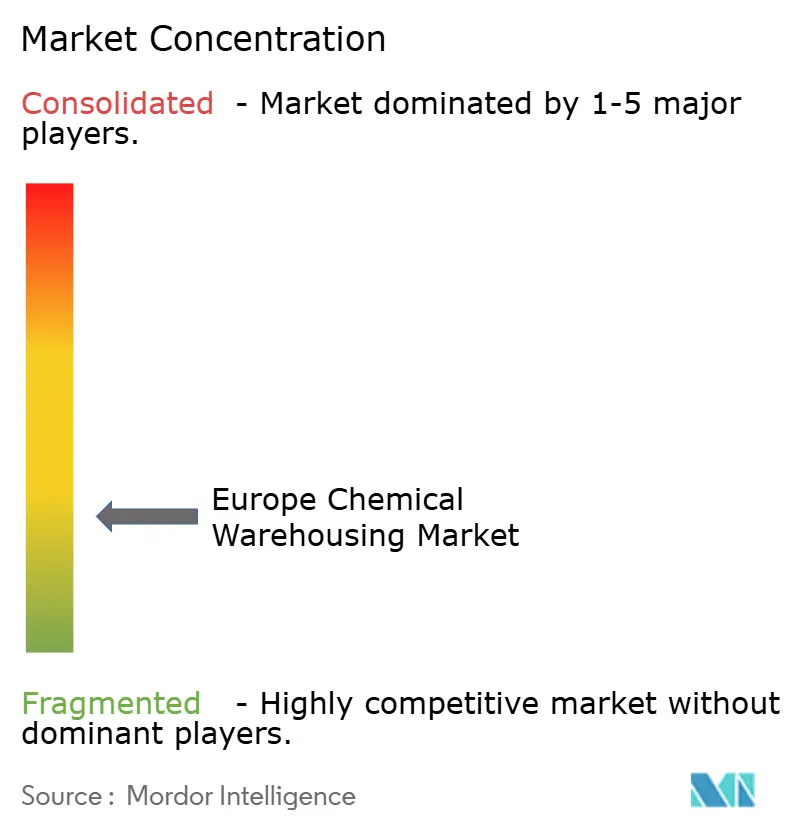

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Chemical Warehousing Market Analysis by Mordor Intelligence

The Europe chemical warehousing market size is projected to expand from USD 21.35 billion in 2025 USD 25.18 billion in 2026 to USD 28.85 billion by 2031, growing at a CAGR of 2.76% over 2026-2031.

Battery-grade input demand for gigafactories, EU decarbonization rules, and offshore-wind component growth are redistributing storage footprints and raising specification standards. Operators face a dual mandate: preserve supply-chain resilience amid Red Sea-related disruptions while funding retrofits for PFAS decontamination and QR-traceability compliance. Technology adoption quickens as Digital Europe subsidies cut automation costs by up to 60%, encouraging smaller providers to invest in robotics and cloud WMS. Consolidation is underway. DSV’s EUR 14.3 billion (USD 15.6 billion) acquisition of Schenker signals a shift toward scale-driven competitiveness, even as niche hazmat specialists defend share through deep regulatory expertise.

Key Report Takeaways

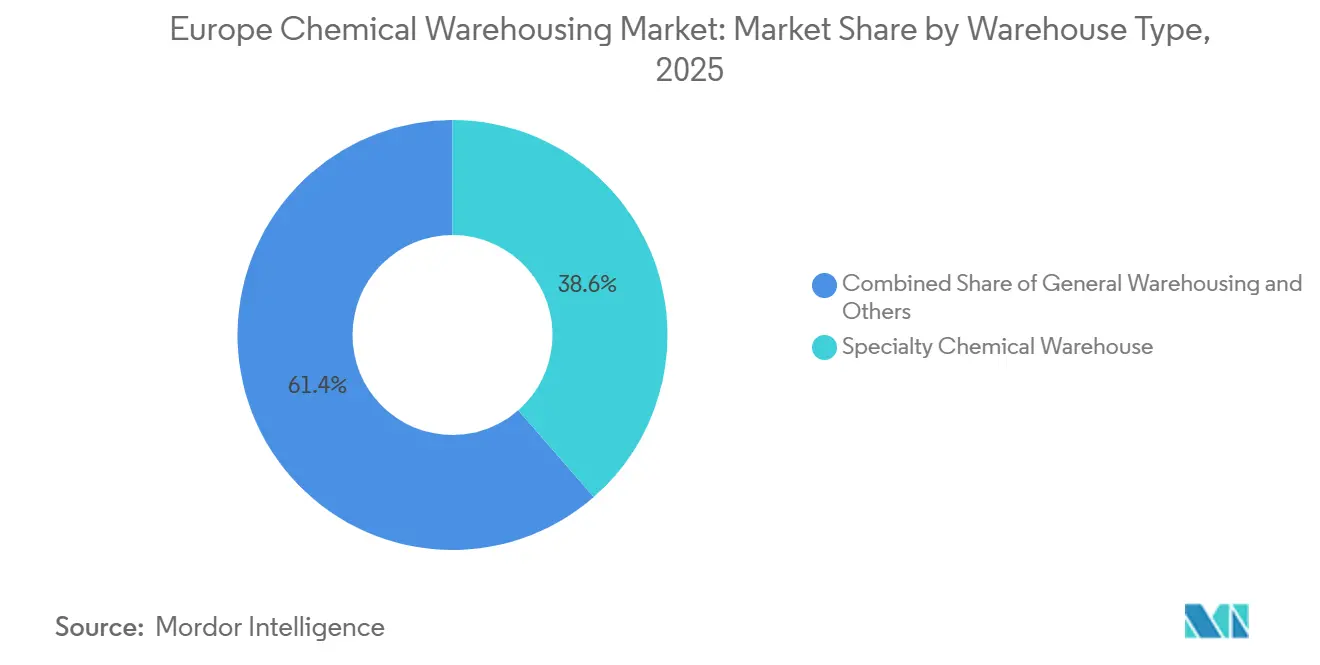

- By warehouse type, specialty chemical facilities held 38.58% of the Europe chemical warehousing market share in 2025, while temperature-controlled sites are projected to advance at a 5.62% CAGR through 2031.

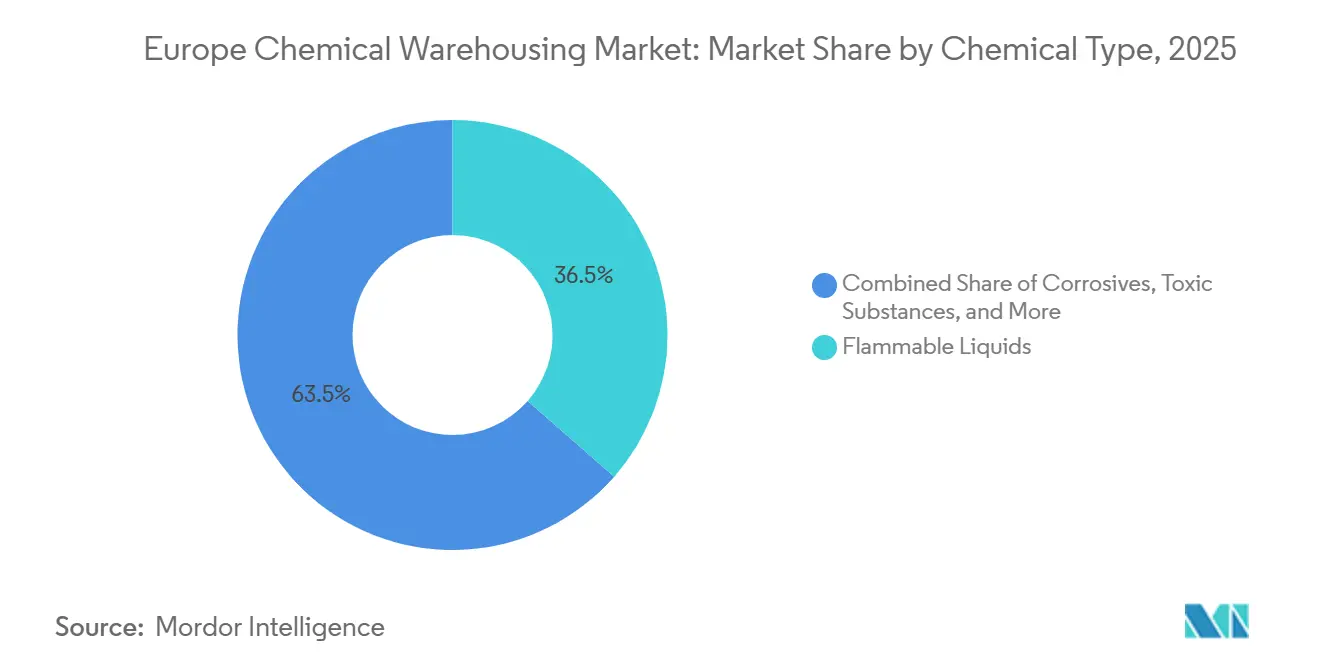

- By chemical class, flammable liquids commanded 36.46% of the Europe chemical warehousing market size in 2025; toxic substances are anticipated to post the fastest 5.20% CAGR to 2031.

- By end-user, pharmaceuticals and life sciences accounted for a 28.19% slice of the Europe chemical warehousing market size in 2025 and are expanding at a 5.51% CAGR to 2031.

- By country, Germany led with 25.43% revenue share in 2025, whereas Italy is forecast to register a 5.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global chemical warehousing market size report represents that cumulative total.

Europe Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gigafactory battery-grade chemical buildouts elevating ADR storage demand | +0.7% | Germany, Sweden, Hungary, Poland battery corridors | Medium term (2-4 years) |

| EU CBAM-linked reshoring of basic chemicals creating buffer-stock warehousing | +0.6% | Germany, Netherlands, Belgium core; Italy, Spain emerging | Long term (≥ 4 years) |

| Offshore-wind resin and hardener volume surge near North Sea ports | +0.4% | Netherlands, Germany, Denmark, UK North Sea coastal zones | Medium term (2-4 years) |

| EU Digital Europe subsidies accelerating warehouse robotics and autonomy adoption | +0.5% | Western Europe core, expanding to Central Europe | Short term (≤ 2 years) |

| Mandatory QR-traceability under EU Chemicals Strategy boosting WMS upgrades | +0.3% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Rise of contract synthesis start-ups needing flexible multi-tenant hazmat space | +0.3% | Germany, Switzerland, Netherlands biotech clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gigafactory Battery-Grade Chemical Buildouts Elevating ADR Storage Demand

Europe’s rapid battery-cell scale-up drives clustered demand for lithium hydroxide, NMP solvents, and PVDF binders that fall under ADR Class 8 regulations. Northvolt’s Ett expansion to 60 GWh by 2026 alone requires new temperature-controlled storage within a 50 km radius, pushing regional capacity past 500,000 m² by 2028. Facility investments are 30-45% costlier than standard sites because of fire-suppression upgrades, segregated hazmat bays, and ±2 °C climate control. Spatial pressure is most acute in eastern Germany, northern Sweden, and Hungary’s automotive corridor, favoring operators that can fast-track SEVESO-III permits and deploy modular warehouses[1]“Digital Europe Programme,” European Commission, digital-strategy.ec.europa.eu.

EU CBAM-Linked Reshoring of Basic Chemicals Creating Buffer-Stock Warehousing

Carbon tariffs on imported ammonia and methanol make EU production financially viable for the first time in two decades, prompting BASF and Yara to plan continental capacity restarts. Manufacturers now hold 30-45 days of feedstock double the 2023 norm to hedge supply risks, swelling warehousing footprints around Ludwigshafen, Antwerp, and Mediterranean ports. Flexibility trumps scale, so multi-product warehouses with agile WMS gain share over single-commodity tanks. Italy and Spain stand out as CBAM beneficiaries because green-hydrogen imports from North Africa offer cost advantages, sending berth-proximate storage demand surging[2]“Carbon Border Adjustment Mechanism (CBAM),” European Commission, taxation-customs.ec.europa.eu.

Offshore-Wind Resin and Hardener Volume Surge Near North Sea Ports

Blade plants in Hull, Aalborg, and Esbjerg consume more than 150,000 t a year of epoxy systems that require 15-25 °C storage and <60% RH to avoid premature curing. As the EU targets 76 GW offshore capacity by 2030, resin warehousing within 100 km of North Sea ports must scale quickly. Operators capable of FIFO inventory logic and real-time environmental monitoring win multi-year supply contracts, yielding steadier revenue streams than spot chemical storage.

EU Digital Europe Subsidies Accelerating Warehouse Robotics and Autonomy Adoption

Funding that covers up to 60% of project costs is catalyzing AGV rollouts and AI-driven WMS upgrades across the Europe chemical warehousing market. DHL and Siemens recorded inventory-accuracy jumps to 99.5%, while head-count exposure to toxic zones fell by 40% DHL. Smaller regional firms leverage grants to narrow capability gaps with global integrators, improving market fluidity yet heightening technical-skill requirements for labor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Port congestion and Red-Sea rerouting inflating dwell-time and inventory risk | -0.6% | Rotterdam, Antwerp, Hamburg major gateways | Short term (≤ 2 years) |

| PFAS phase-out liabilities requiring costly decontamination capacity | -0.5% | Germany, Netherlands, Belgium legacy sites | Medium term (2-4 years) |

| Green-finance taxonomy and higher rates raising retrofit hurdle costs | -0.3% | EU-wide, strongest in Western Europe | Long term (≥ 4 years) |

| Extreme-weather resilience mandates driving unplanned capex on sites | -0.2% | Coastal zones and flood-prone regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Port Congestion and Red-Sea Rerouting Inflating Dwell-Time and Inventory Risk

Cape-of-Good-Hope routing lengthened Asian-to-EU voyages by up to 14 days in 2025. Rotterdam’s average container dwell stretched from 4 days to 10 days, forcing importers to double safety stocks and pay higher demurrage fees. Specialty importers lacking secondary suppliers must absorb 15-20% logistics-cost inflation, shrinking margins, and nudging procurement toward reshored capacity.

PFAS Phase-Out Liabilities Requiring Costly Decontamination Capacity

Proposed EU-wide PFAS bans covering 10,000 substances push remediation costs to EUR 2-5 million (USD 2.35-5.88 million) per warehouse. Germany and the Netherlands apply stricter cleanup standards, lifting expenses another 40-60%. Older depots in legacy industrial zones face possible closure, tightening capacity in already supply-constrained Rhine-Ruhr clusters, and complicating consolidation valuations[3]“PFAS Restriction Proposal and REACH Implementation,” European Chemicals Agency, echa.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Temperature-Controlled Sites Gain Momentum

Temperature-controlled chemical warehouses captured 5.62% of the Europe chemical warehousing market share growth trajectory through 2031, reflecting surging biologics and battery-grade electrolyte demand that tolerates temperature windows of only ±2 °C. The Europe chemical warehousing market size linked to these high-specification sites is climbing as operators retrofit legacy rooms with multi-zone HVAC, humidity scrubbers, and inert-gas fire suppression to satisfy GDP and ADR rules in a single footprint. Premium build costs of EUR 1,200-1,800 (USD 1411-2117) per m² are increasingly offset by contract lengths stretching to five years for biosimilar pipelines, enabling landlords to lock in higher yields and speed debt pay-down schedules[4]“Chemical Storage Regulations,” HSE, hse.gov.uk.

Specialty chemical warehouses still controlled 38.58% of the Europe chemical warehousing market size in 2025, anchored by micro-batch electronic chemicals and performance additives that demand segregated bays, conductive-floor coatings, and ISO Clean Room annexes. General warehouses, largely bulk commodity halls, are losing pricing power as clients gravitate toward value-added blending or pre-dilution services now offered inside upgraded specialty facilities. Hazmat-only buildings remain a staple for petrochemical flows but face margin squeeze from mounting insurance premiums after PFAS contamination scares, pushing small operators toward joint-venture fire-water containment upgrades funded under Digital Europe grants.

By Chemical Type: Toxic Substances Accelerate on CDMO Upswing

Flammable liquids retained the largest 36.46% slice of the Europe chemical warehousing market share in 2025, yet toxic substances are set to expand 5.20% annually to 2031 as contract drug-substance makers scale cytotoxic lines across Ireland, Belgium, and Denmark. The Europe chemical warehousing market size tied to ADR Class 6.1 products is growing because negative-pressure ventilation, closed-loop drum-feeding, and gas-detector grids are now baseline audit points in CDMO tenders.

Corrosives and oxidizers post steadier, lower-single-digit growth as metal-finishing and aerospace niche volumes keep demand flat. A nascent “others” basket green ammonia, hydrogen carriers, bio-solvents introduces exotic pressure-temperature envelopes that conventional buildings cannot handle, prompting the first mixed-service depots with cryogenic pods and ATEX robotic arms. The shift from single-class to multi-class inventories raises WMS complexity, pushing providers toward substance-level QR passports that roll up seamlessly into REACH dossiers for regulators.

By End-User Industry: Pharma and Life Sciences Drive Premium Demand

Pharmaceuticals and life sciences accounted for 28.19% of the Europe chemical warehousing market size in 2025 and should log a 5.51% CAGR through 2031 as EU biosimilar production ramps and cell-therapy cold chains multiply. Each pallet lane now requires temperature mapping, GDP certification, and a qualified person sign-off, letting landlords charge rates 40-60% above commoditized solvent storage while simultaneously reducing vacancy risk through multi-year CDMO master agreements.

Specialty chemicals manufacturing keeps a broad 28.19% base, yet its share inches downward as CBAM policy shifts incentives toward on-site bulk storage at new low-carbon production units. Basic chemicals importers, confronted by Red Sea disruptions, are converting spot halls into safety-stock buffers but resist long contracts, muting revenue potential. Agrochemical, coatings, and food-additive customers demand stringent traceability but book space only seasonally, compelling operators to mix these verticals within dynamic slotting models powered by AI to sustain over 85% utilization.

Geography Analysis

Germany accounted for 25.43% of the Europe chemical warehousing market share in 2025, underpinned by the Rhine-Ruhr and Frankfurt-Mannheim corridors that host dense clusters of specialty and basic chemical producers. The Europe chemical warehousing market size attached to Germany is rising as Northvolt’s Heide cell plant and CATL’s Thuringia site demand temperature-controlled ADR bays within 30 km of production lines, while PFAS clean-up rules nudge smaller depots to partner with well-capitalized operators. DSV’s 2025 purchase of Schenker adds 1.6 million m² of German storage, tightening capacity control and accelerating automation rollouts to meet QR-traceability audits. Digital Europe grants further boost robotics adoption, lifting safety and inventory accuracy metrics, yet raising the technical-skills bar for labor.

Italy is projected to grow fastest at a 5.11% CAGR to 2031 as Mediterranean ports Genoa, Trieste, and Naples channel CBAM-advantaged green-ammonia and hydrogen inputs from North Africa, expanding the Europe chemical warehousing market size in Southern Europe. New multi-commodity depots near these ports blend cryogenic pods with conventional halls so importers can switch between ammonia derivatives and epoxy resins without violating SEVESO-III thresholds. Lower electricity costs versus Northern Europe draw basic-chemical reshoring, while pharmaceutical investments in Lombardy and Lazio enlarge temperature-controlled square footage. Regional authorities fast-track permits for battery-grade electrolyte warehouses serving nascent gigafactory corridors in Turin and Veneto, trimming lead-times by six months.

The Netherlands, United Kingdom, France, Spain, and Poland jointly represent just over 40% of 2025 revenue, but each faces distinct headwinds. Rotterdam’s dwell-time jump to 10 days after Red Sea rerouting pushed overflow into inland Brabant campuses equipped with AGV cross-docks. Poland’s Lower Silesia attracts ADR Class 8 traffic from LG and CATL gigafactories, yet aging roads slow first-mile transfers. France and Spain leverage offshore-wind resin demand and green-ammonia pilots to justify composite-friendly storage retrofits, while the United Kingdom offsets Brexit friction through Crown Paints and other captive contracts that anchor utilization at new temperature-controlled hubs. Rest-of-Europe markets in Czechia, Hungary, and Romania capitalize on EU cohesion funding to add modular hazmat sheds and close the infrastructure gap with Western nodes.

Coverage of the chemical warehousing market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, Middle East, and Africa, alongside detailed country-level intelligence for Germany, France, United Kingdom, Italy, Canada, and Japan, each shaped by local operating conditions.

Competitive Landscape

The Europe chemical warehousing market remains moderately fragmented: the five largest providers hold about 55-60% of stored-volume revenue, while more than 200 regional specialists handle niche ADR classes. DSV vaulted to first place via its EUR 14.3 billion (USD 15.6 billion) Schenker acquisition, integrating 430 depots and unveiling a cloud WMS that delivers substance-level QR scans across 26 countries. Kuehne + Nagel sharpened its life-sciences focus through the USD 1.4 billion Apex International purchase, adding GDP-certified space in Belgium, Denmark, and Ireland. CEVA Logistics absorbed GEFCO to deepen automotive-chemical routing, especially for isocyanate flows tied to EV battery casings.

Hazmat pure-plays such as Bertschi, Den Hartogh, and HOYER defend share through fleets of pressure-tested tank containers, on-site chemists, and 24/7 emergency teams that satisfy insurer risk matrices. GEODIS automated its Mannheim pharma hub with pick-to-light robotics and AI-driven HVAC that shaved energy use 18%, showcasing how mid-tier integrators can close the capability gap. NTG Nordic’s 2025 DTK buyout widened Northern European hazmat reach, while Sennder’s land-transport takeover positions it to bolt on storage offerings by 2026. XPO Logistics opened a 4,000 m² Nijmegen facility featuring solar power and relabelling lines, signaling sustainability as a competitive lever.

Barriers to entry stay high: SEVESO-III licensing, rising PFAS remediation liabilities, and insurer demands for dual fire-water systems inflate start-up capex. Yet Digital Europe subsidies covering up to 60% of automation costs allow smaller depots to install AGVs and blockchain-ready WMS, preserving a measure of fragmentation. Clients increasingly award contracts on predictive-compliance dashboards rather than simple rate cards, pushing laggards toward alliances or exits. These trends, coupled with active M&A pipelines, suggest the Europe chemical warehousing market will edge toward higher concentration without eliminating space for specialized hazmat boutiques.

Europe Chemical Warehousing Industry Leaders

DHL Group

Kuehne + Nagel

Rhenus Logistics

Bertschi AG

Den Hartogh Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV closed the EUR 14.3 billion (USD 15.6 billion) DB Schenker acquisition, adding 430 European depots, extensive hazmat training centers, and 3.5 million m² of warehouse space.

- March 2025: NTG Nordic bought DTK for DKK 620 million (USD 89.3 million), extending temperature-controlled reach across Denmark, Germany, and the Baltics.

- February 2025: Sennder acquired C.H. Robinson’s European land-transport arm, gaining 1,600 staff and 20 hubs, with plans to bolt on hazmat storage by 2026.

- February 2025: XPO Logistics inaugurated a 4,000 m² hub in Nijmegen with solar-powered operations and chemical relabeling services.

Europe Chemical Warehousing Market Report Scope

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals and Life Sciences |

| Agrochemicals |

| Paints, Coatings and Adhesives |

| Food and Feed Additives |

| Oil and Gas / Petrochemicals |

| Others |

| Germany |

| United Kingdom |

| Russia |

| Italy |

| Netherlands |

| Spain |

| Poland |

| France |

| Rest of Europe |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals and Life Sciences | |

| Agrochemicals | |

| Paints, Coatings and Adhesives | |

| Food and Feed Additives | |

| Oil and Gas / Petrochemicals | |

| Others | |

| By Country | Germany |

| United Kingdom | |

| Russia | |

| Italy | |

| Netherlands | |

| Spain | |

| Poland | |

| France | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe chemical warehousing market in 2026?

It is valued at USD 25.18 billion in 2026.

What CAGR is predicted for European chemical storage through 2031?

A CAGR of 2.76% is forecast for 2026-2031.

Which warehouse type is expanding the fastest?

Temperature-controlled chemical warehouses are projected to grow at 5.62% CAGR.

Which country will grow quickest to 2031?

Italy is expected to register the fastest 5.11% CAGR, driven by CBAM-linked reshoring and port advantages.

What is a major regulatory tech driver in this sector?

Mandatory QR-traceability under the EU Chemicals Strategy is spurring WMS upgrades across the region.

How is consolidation shaping competition?

DSV’s purchase of DB Schenker and other M&A moves are boosting scale advantages and nudging the market toward moderate concentration.

Page last updated on: