China Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

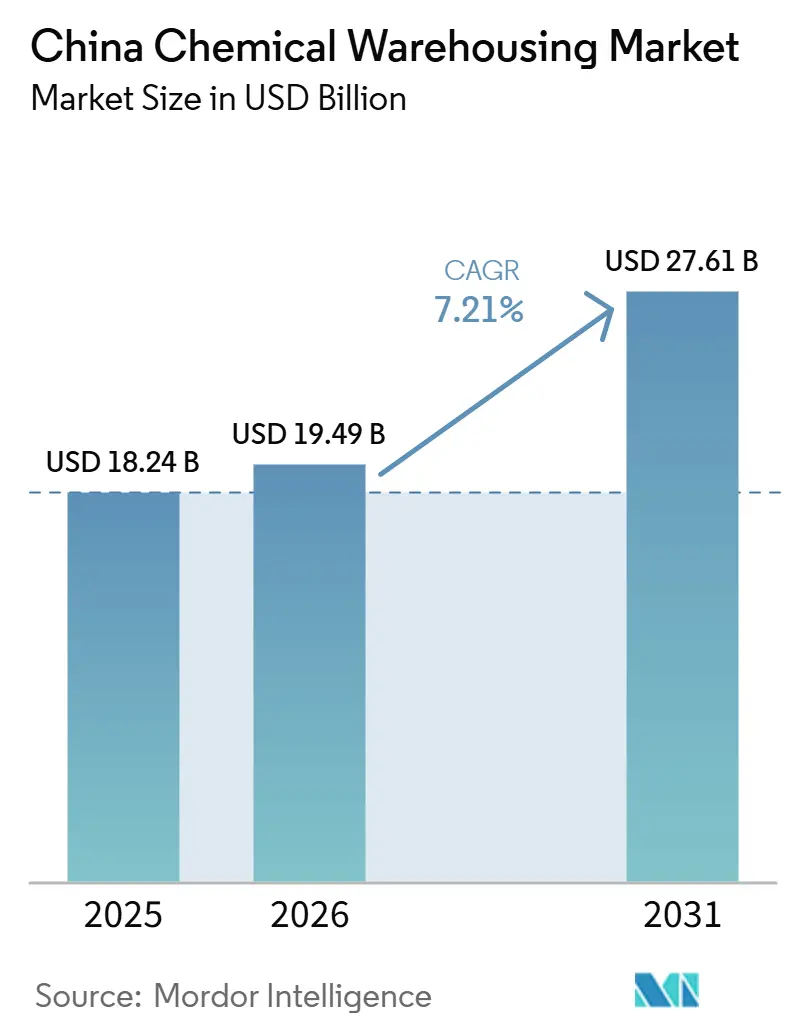

| Base Year Market Size (2025) | USD 18.24 Billion |

| Market Size (2026) | USD 19.49 Billion |

| Market Size (2031) | USD 27.61 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

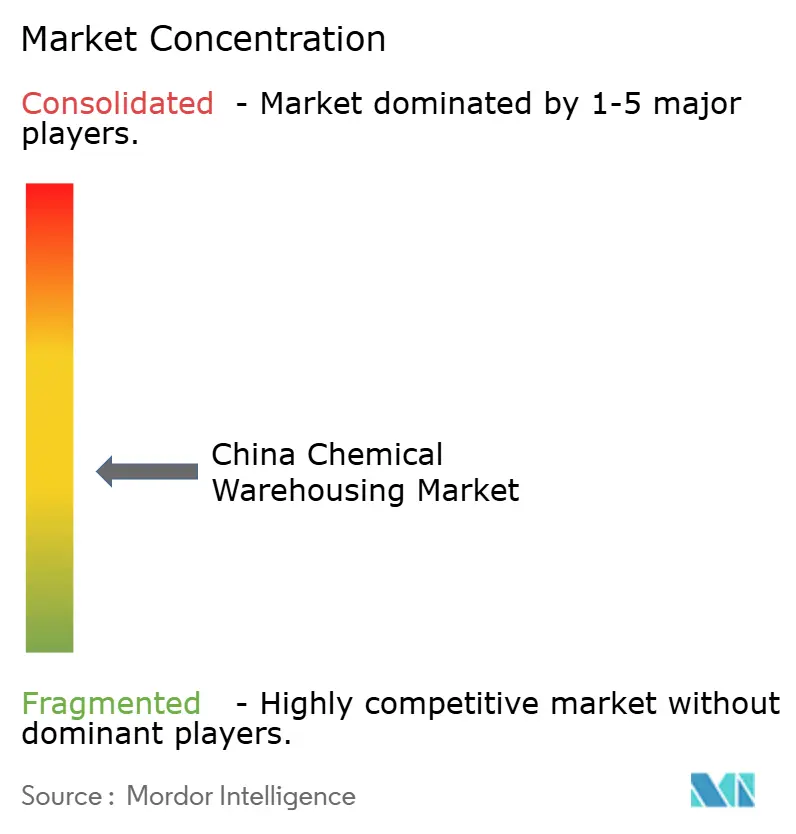

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Chemical Warehousing Market Analysis by Mordor Intelligence

The China Chemical Warehousing Market size is projected to be USD 18.24 billion in 2025, USD 19.49 billion in 2026, and reach USD 27.61 billion by 2031, growing at a CAGR of 7.21% from 2026 to 2031.

The Chinese chemical warehousing market is supported by a sustained expansion of petrochemical and specialty chemical capacity in 2026 and a firm regulatory shift toward automation and real-time safety monitoring that improves compliance quality. Investment in temperature-controlled capacity is accelerating due to pharmaceutical GDP standards and rising cold-chain flows tied to higher-value APIs and intermediates. Multimodal corridors under the Belt and Road framework are shortening dwell times and improving asset turns, which favors operators located at bonded and customs-supervised nodes. The Chinese chemical warehousing market is moderately concentrated in coastal provinces with rapid growth in inland renewable-energy zones, and competitive intensity is rising as state-owned giants integrate marine, rail, and inland logistics while global 3PLs scale digital orchestration and ESG-linked services.

Key Report Takeaways

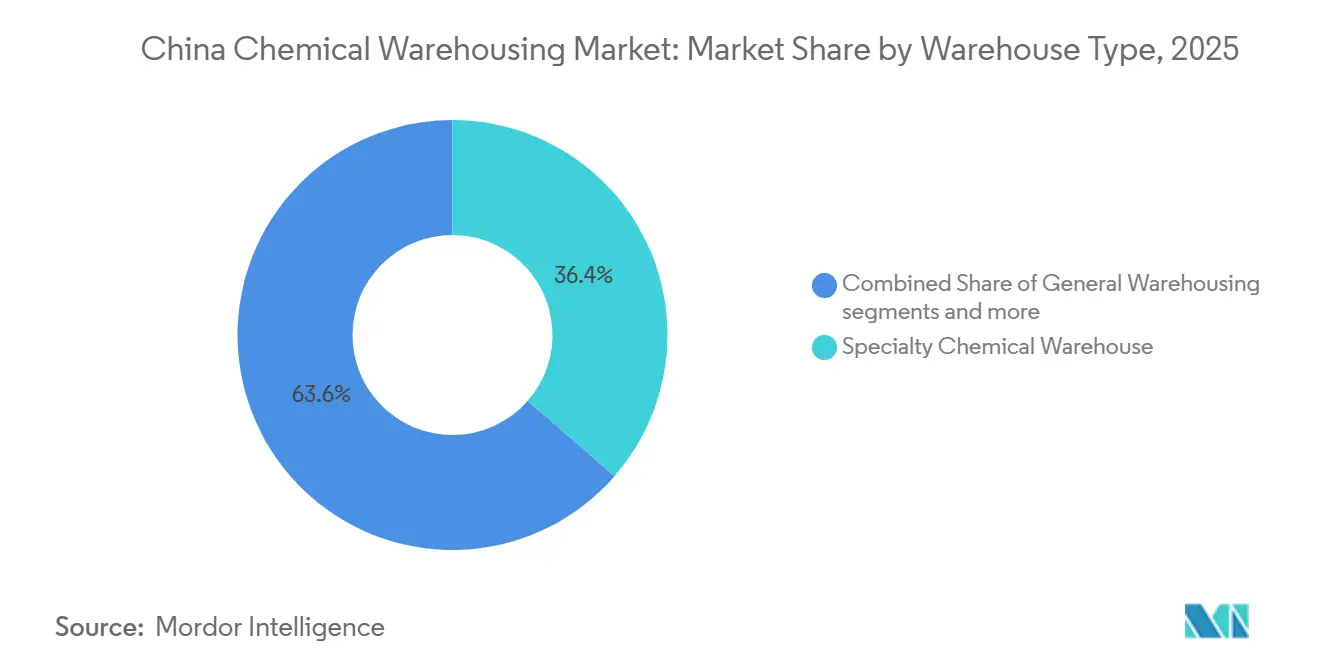

- By warehouse type, specialty chemical warehouses led with 36.42% of the China chemical warehousing market size in 2025, and temperature-controlled chemical warehouses are projected to grow the fastest with a CAGR of 8.62% through 2031.

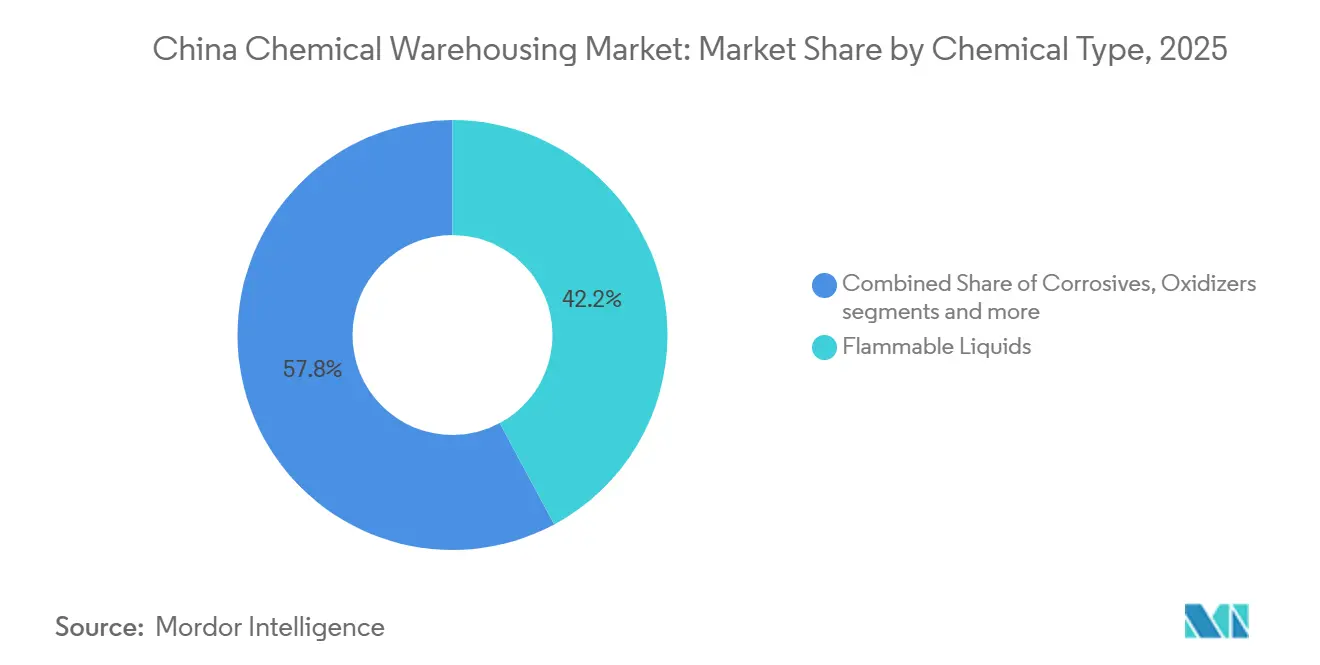

- By chemical type, flammable liquids accounted for 42.16% of the China chemical warehousing market share in 2025, while toxic substances are projected to grow at the fastest pace at a CAGR of 9.41% through 2031, due to electronic, chemical, and semiconductor-linked demand.

- By end-user industry, basic chemicals manufacturing remained the largest, accounting for a market size of 47.23% of the China chemical warehousing market size in 2025, and pharmaceuticals and life sciences are projected to record the fastest growth of 7.89% CAGR through 2031, owing to stronger GDP compliance.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Dynamics observed within China present a country level view when set against the broader international context. The chemical warehousing market analysis by Mordor Intelligence provides that expanded global perspective.

China Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Chemical Manufacturing Base | +2.1% | Global, with concentration in coastal provinces (Jiangsu, Shandong, Guangdong) and expansion into inland renewable-energy zones | Medium term (2-4 years) |

| Stringent Chemical Safety Regulations | +1.8% | National, with higher enforcement in urban chemical enterprise relocation zones and designated chemical parks | Short term (≤ 2 years) |

| Belt and Road Initiative (BRI) Logistics Growth | +1.3% | National corridors linking coastal ports (Beibu Gulf, Zhanjiang) to inland hubs (Chongqing, Chengdu, Lanzhou), ASEAN spill-over | Long term (≥ 4 years) |

| Growth in Specialty and Fine Chemicals Sector | +1.0% | National, with advanced concentration in Yangtze River Delta and Greater Bay Area industrial clusters | Medium term (2-4 years) |

| Yangtze River Economic Belt Development | +0.6% | Yangtze River Economic Belt provinces (Hubei, Anhui, Jiangsu, Zhejiang), ecological-priority zones | Medium term (2-4 years) |

| Smart Warehousing Technology Integration | +0.4% | National adoption, with early gains in Tier-1 logistics hubs (Shanghai, Shenzhen, Guangzhou) and Hubei corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Chemical Manufacturing Base

China’s petrochemical and chemical sector is set to deliver value-added growth above 5% annually through 2026, with emphasis on high-end polyolefins, electronic chemicals, and new-energy feedstocks under the 2025 to 2026 stable growth plan. Large-scale programs continue to add capacity and draw in specialized warehousing for flammable and toxic materials with tighter custody needs. Foreign direct investment in life sciences and specialty platforms, including the USD 475 million Wuxi site, adds momentum to GDP-compliant storage and distribution. The China chemical warehousing market benefits as throughput rises for electronic-grade solvents and engineered materials that require inert-atmosphere, contamination-free storage. This upstream shift compresses dwell times and raises the value of automation, raising utilization and stabilizing margins for certified operators.

Stringent Chemical Safety Regulations

The Dangerous Chemicals Safety Law, effective May 1, 2026, sets a 127-article framework that enforces dual-person receipt and dual-person custody for highly toxic and major-hazard materials, with records kept for at least three years. The GB 45673-2025, which took effect on November 1, 2025, mandates full-process automation for high-risk processes and upgrades continuous monitoring and safety instrumentation. Warehouses are adding IoT sensors, compliant sprinklers, and government-interconnected control systems to meet approvals and pass audits. Smaller facilities without the capital to retrofit are either consolidating or exiting, which tilts demand to certified parks and integrated platforms with high compliance readiness. The Chinese chemical warehousing market shifts toward fewer but more automated and traceable sites as enforcement intensifies in 2026.[1]Guifanku Editorial Board, “GB 45673-2025 General Specification for Safety Production Standardization,” Guifanku, guifanku.com

Belt and Road Initiative (BRI) Logistics Growth

The New International Land-Sea Trade Corridor surpassed 1 million TEUs in 2025 with a 72.5% year-on-year increase and now runs 14 fixed rail-sea routes linking Beibu Gulf and Zhanjiang ports with inland nodes such as Chongqing and Chengdu. A March 2025 model combining JSQ trains with roll-on and roll-off vessels enabled direct transfer to ocean carriers at Qinzhou bound for Dubai, cutting handoffs and reducing congestion exposure. In the first-half of 2025, cargo volume reached 746,000 TEUs, which supports bonded and customs-supervised storage demand near corridor junctions. Integrated logistics packages that bundle customs e-filing and tracking are reducing coordination time for shippers. The Chinese chemical warehousing market captures higher throughput and faster rotations at these hubs as the corridor diversifies product categories to include chemicals and intermediates.

Growth in the Specialty and Fine Chemicals Sector

National policy under Made in China 2025 emphasizes electronic chemicals, bio-based materials, and high-performance fibers, which require controlled environments and strict segregation in storage. The standards push for carbon-footprint accounting and quality-traceability, which promotes auditable supply chains that favor specialized warehouses with RFID and batch tracking. New fine-chemical capacity, including isophorone diisocyanate, commissioned in 2025, increases demand for sealed-containment and ventilation-compliant warehouses. These storage formats carry premium pricing, which offsets higher per-square-meter operating costs. The Chinese chemical warehousing market gains from this mix shift as operators that align with specialty customers’ protocols win longer contracts and lower loss ratios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictive Land Use Policies for Hazardous Materials | -1.2% | National, with acute constraints in urban relocation zones and safety-distance buffer areas around schools, hospitals, residential centers | Short term (≤ 2 years) |

| High Compliance and Infrastructure Costs | -0.9% | National, with higher burden on small/micro enterprises and facilities undergoing GB 45673-2025 retrofits | Medium term (2-4 years) |

| Frequent Regulatory Changes and Enforcement | -0.7% | National enforcement, with provincial variance in hidden-risk investigation cycles and safety-supervision intensity | Short term (≤ 2 years) |

| Chemical Industry Relocation Pressures | -0.5% | Urban chemical enterprises in coastal Tier-1/Tier-2 cities (Shanghai, Guangzhou, Ningbo), with relocation to designated inland parks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Restrictive Land Use Policies for Hazardous Materials

The Dangerous Chemicals Safety Law requires prescribed safety distances between hazardous storage and sensitive receptors and pushes new projects into approved chemical parks that undergo periodic reviews[2]CCTV Newsroom, “Dangerous Chemicals Safety Law Comes into Effect on May 1, 2026,” CCTV, news.cctv.cn . Environmental impact rules linked to new pollutants strengthen screening and alignment with ecological zoning and park-level EIAs. These layers reduce eligible land and prolong approvals, sending projects to zones where transport and emergency services lag coastal hubs. The Chinese chemical warehousing market sees higher capital intensity per tonne as siting constraints and buffer areas expand in 2026. Developers navigate this by prioritizing designated parks with built-in safety and response infrastructure where approvals are more predictable.

High Compliance and Infrastructure Costs

TGB 45673-2025 upgrades and three-simultaneities requirements are lifting capex on automation, detection, ventilation, and diking while mandating facility commissioning with the main project. Hazmat insurance premiums rose 40% from 2024 to 2025, and the law now calls for environmental liability insurance for storage sites. Recurring third-party safety evaluations add to operating costs as operators connect monitoring systems to government platforms. Small micro enterprises with fewer than 20 employees or with annual revenue below RMB 3 million (USD 0.4 million) face the heaviest strain and are consolidating into larger platforms. The Chinese chemical warehousing market is consolidating toward operators that can amortize digital and compliance overhead while maintaining service reliability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialized Facilities Capture Premium, Controlled Environments Surge

Specialty chemical warehouses held the largest market share of 36.42% of the China chemical warehousing market in 2025, as customers shifted to fine and electronic chemicals that require segregation and contamination control. These sites use inert-gas blanketing for oxygen-sensitive compounds, controlled humidity for hygroscopic materials, and batch genealogy tracked with RFID to meet chain-of-custody needs in semiconductors and biologics. Temperature-controlled chemical warehouses are growing the fastest, with a CAGR of 8.62% through 2031 under stricter GDP rules and rising cold-chain flows of APIs and specialty intermediates, which strengthens compliance-led differentiation. General chemical warehouses continue to serve stable bulk products with fewer integrity risks, although margin pressure is rising as shippers prioritize liability protection in sensitive categories. The Chinese chemical warehousing market favors operators that blend specialty infrastructure and digital orchestration to raise asset turns and service quality under tighter enforcement.

Growth within this segmentation tracks technology deployment and regulatory readiness in 2026. HAZMAT warehouses that manage flammables, corrosives, and toxics are upgrading to explosion-proof systems and automated suppression aligned to GB and legal requirements on dual-person custody and real-time tracking. Operators are piloting digital twins and AI-driven scheduling to improve slotting and labor efficiency, reporting productivity gains that defend margins despite higher compliance costs. The Chinese chemical warehousing industry is moving to standardized automation and integrated monitoring to ensure approvals and to interoperate with government platforms in 2026. The Chinese chemical warehousing market continues to differentiate on specialty readiness, GDP performance, and audit velocity that reduces customer risk.

By Chemical Type: Liquids Dominate Volumes, Toxics Accelerate on Semiconductor Demand

Flammable liquids held the largest share of 42.16% of the China chemical warehousing market in 2025, as solvents, alcohols, and hydrocarbon distillates drive consistent throughput in coatings, adhesives, and petrochemical feedstocks. Storage requires explosion-proof electricals, grounding, and rated separation distances that elevate capex but support stable utilization and multi-year customer contracts. Toxic substances are growing the fastest at a CAGR of 9.41% through 2031, lifted by electronic chemicals and semiconductor supply chain ambitions that demand sealed containment and continuous ventilation. Corrosives remain significant and must be segregated with chemically resistant flooring and neutralization systems to avoid exothermic risk, which encourages siting in integrated parks with shared emergency response[3]Ministry of Commerce of the People’s Republic of China, “Work Plan for Stable Growth in the Petrochemical and Chemical Industry (2025–2026),” Ministry of Commerce, picpolicy.mofcom.gov.cn. The Chinese chemical warehousing market is reinforced by oxidizer-handling protocols and higher insurance costs that raise pricing but support premium storage for risk-intensive SKUs.

Operators are adapting to the complexity profile of liquids and toxics with stricter documentation, including dual-custody logs and retention of custody records for at least three years. This triggers investment in digital traceability and permissioned access to acquire with customers in pharmaceuticals and electronics. The Chinese chemical warehousing industry is pivoting to high-integrity storage that reduces loss events and improves audit readiness in 2026. These shifts help the Chinese chemical warehousing market meet procurement criteria that increasingly weigh compliance proof and performance history alongside pricing.

By End-User Industry: Basic Chemicals Anchor Base Load, Pharma Scales Fastest

Basic chemicals manufacturing held the largest end-user share of 47.23% in 2025, with strong volumes in polyethylene, polypropylene, methanol, and caustic soda that anchor base-load storage. The segment relies on tank farms and drum storage close to production clusters where economies of scale and proximity support predictable turns. Pharmaceuticals and life sciences are growing the fastest with a CAGR of 7.89% through 2031 as GDP compliance raises demand for temperature mapping and real-time deviation handling, with AstraZeneca’s USD 475 million Wuxi site reinforcing long-term volume. Specialty chemicals for semiconductors and performance plastics require contamination-free spaces and detailed batch genealogy that favor automated AS/RS investments. The China chemical warehousing market accommodates seasonal agrochemical flows with flexible capacity while enforcing traceability and emissions-accounting rules in fertilizers and synthetic rubber.

Oil and gas and petrochemical flows remain material and benefit from marine fleet renewal and integration initiatives that secure berth access and tankage. Food and feed additives overlap with pharma-grade handling in some cases, which opens cross-selling opportunities for operators certified for both segments. The China chemical warehousing market continues to reward end-to-end providers that connect inbound raw materials with outbound finished goods across bonded and non-bonded footprints. End-user diversification stabilizes utilization and mitigates single-segment cyclicality in 2026.

Geography Analysis

Coastal provinces, notably Jiangsu, Shandong, and Guangdong, held the largest capacity base in 2025 in the China chemical warehousing market due to deep-water terminals, legacy chemical parks, and port-proximate bonded zones. The Guangdong–Hong Kong–Macao Greater Bay Area is forming a premium corridor for high-value flows, aided by Sinotrans’s joint venture for a chemical logistics hub in Zhanjiang with registered capital of RMB 207.2 million (USD 29.1 million). BASF’s Verbund complex in Zhanjiang, with an announced EUR 10 billion plan (USD 10.8 billion), is adding captive demand for inert-atmosphere and temperature-controlled storage. Pharma logistics networks in the region, including digital 4PL initiatives, are pulling forward GDP-compliant capacity.

Inland provinces, including Inner Mongolia, Gansu, and Ningxia, are scaling faster in 2026 under coal-to-chemicals programs and renewable-power integration that lower carbon intensity and diversify siting. Junzheng Group’s wind, solar, and hydrogen complex in Inner Mongolia, with an investment of CNY 19.36 billion (USD 2.7 billion), illustrates the pull for bonded and customs-supervised warehousing at rail-to-road hubs that connect to export corridors. Northern and central multimodal hubs in Beijing, Tianjin, Chongqing, and Chengdu are compressing dwell times through enhanced rail-sea arrangements, including the JSQ train to roll-on and roll-off model launched in March 2025 for direct vehicle transfers to ocean carriers.

Logistics arteries under the New International Land-Sea Trade Corridor surpassed 1 million TEUs in 2025 and are expanding product mix to include more chemical feedstocks and intermediates, which tightens operations at corridor nodes. As coastal cities tighten land-use rules and complete relocation of urban chemical facilities, capacity is migrating into designated parks that undergo triennial risk assessments and install government-linked safety systems. The China chemical warehousing market, therefore, balances a coastal anchor with rising inland throughput, with automation and compliance connectivity shaping where new projects gain approvals in 2026.

Coverage of the chemical warehousing market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, Europe, and Middle East, alongside detailed country-level intelligence for South Korea, Japan, Canada, France, India, and Germany, each shaped by local operating conditions.

Competitive Landscape

The market remains moderately concentrated overall, although high-compliance and automated chemical warehousing segments are increasingly consolidating among large state-owned and certified operators. State-owned platforms leverage terminal access and integrated rail-sea-warehouse solutions to offer single-window services from marine to inland nodes. International 3PLs compete on digital orchestration and ESG-linked offerings to win high-compliance customers. Specialized domestic chemical logisticians focus on hazmat certification depth and real-time traceability to differentiate in segments with elevated risk and documentation needs.

COSCO Shipping Energy integrated chemical-carrier assets in 2024 and disclosed in March 2026 shipbuilding contracts for one ethylene carrier and 18 oil tankers totaling RMB 7.882 billion (USD 1.1 billion), along with chemical tanker shipping revenue of RMB 333 million (USD 46.3 million) in 2025, which strengthens its control of marine-to-terminal flows. The company also completed an acquisition of target entities for RMB 1.05 billion (USD 147.5 million) in 2024, which tightened vertical integration. Kerry Logistics Network expanded its chemical-handling subsidiaries and received recognition from multinational chemical producers for safety and partnership quality in 2025, signaling an emphasis on verified compliance.

Technology and ESG are central to competitive positioning in 2026. China Logistics Group’s “Liuyun” model, filed at the national registry in 2025, supports intelligent warehousing, visual recognition, and predictive maintenance to reduce idle times and speed audits. Rokin advanced its ESG credentials with SBTi-validated targets in March 2026 and won a award for AI-powered cold chain automation that aligns with the needs of pharma and specialty chemicals in 2025. Autonomous logistics pilots, including L4 vehicles that have accumulated over 42 million kilometers, offer a pathway to mitigate driver shortages in dangerous goods. These capabilities help the China chemical warehousing market narrow the gap between higher compliance overhead and the need for cost control through better utilization and fewer manual errors.

China Chemical Warehousing Industry Leaders

Sinotrans Ltd.

Yongtaiyun Chemical Logistics

Rokin Logistics

Den Hartogh Logistics

Hoyer Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The Dangerous Chemicals Safety Law was passed on December 27, 2025, and will take effect on May 1, 2026, adding dual-person custody and real-time monitoring obligations for hazardous storage.

- March 2025: Rokin Logistics was designated a National Emergency Transport Support Fleet partner, which expands access to emergency-response channels for hazardous shipments.

China Chemical Warehousing Market Report Scope

The China Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and more), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, and more), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and more). The Market Forecasts are Provided in Terms of Value (USD Billion).

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals and Life Sciences |

| Agrochemicals |

| Paints, Coatings and Adhesives |

| Food and Feed Additives |

| Oil and Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals and Life Sciences | |

| Agrochemicals | |

| Paints, Coatings and Adhesives | |

| Food and Feed Additives | |

| Oil and Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the current size and expected growth of the Chinese chemical warehousing market?

The China Chemical Warehousing Market size was USD 18.24 billion in 2025 and is projected to reach USD 27.61 billion by 2031 at a 7.21% CAGR.

Which warehouse types are leading and growing fastest in China’s chemical storage landscape?

Specialty chemical warehouses led with 36.25% in 2025 due to contamination-sensitive products, while temperature-controlled chemical warehouses are growing the fastest, at a CAGR of 8.62% through 2031 under GDP standards.

What regulatory changes most affect chemical warehousing operators in China?

The Dangerous Chemicals Safety Law, effective May 1, 2026, and GB 45673-2025 require dual-person custody, automation for high-risk processes, and real-time monitoring linked to government platforms.

Which regions in China are key for chemical warehousing capacity and growth?

Jiangsu, Shandong, and Guangdong anchor capacity while Inner Mongolia, Gansu, and Ningxia are expanding fastest on coal-to-chemicals and renewable-linked investment tied to multimodal corridors.

How are technology and automation changing chemical warehousing operations in China?

Operators are deploying AI for warehouse scheduling, digital twins for slotting, and IoT for safety monitoring, which improve productivity and audit speed under stricter enforcement.

Which end-user industries drive demand for chemical warehousing in China?

Basic chemicals remain the base load, while pharmaceuticals and life sciences are scaling fastest due to GDP compliance and ongoing investments by multinationals.

Page last updated on: