France Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

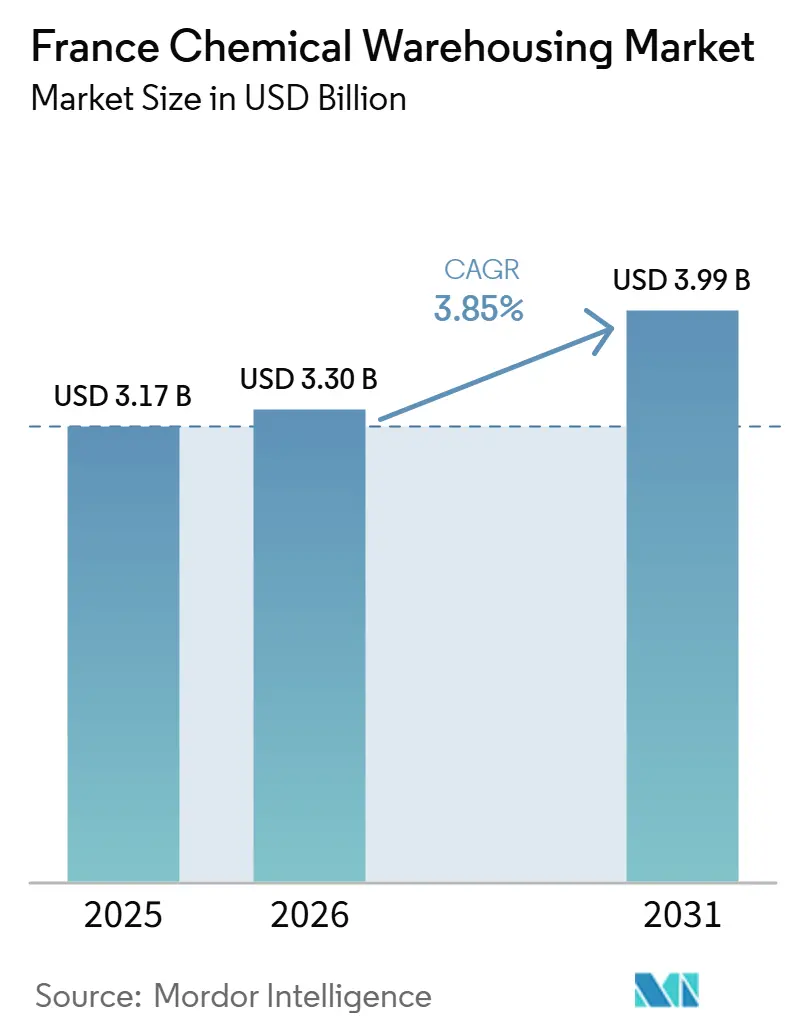

| Base Year Market Size (2025) | USD 3.17 Billion |

| Market Size (2026) | USD 3.30 Billion |

| Market Size (2030) | USD 3.99 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

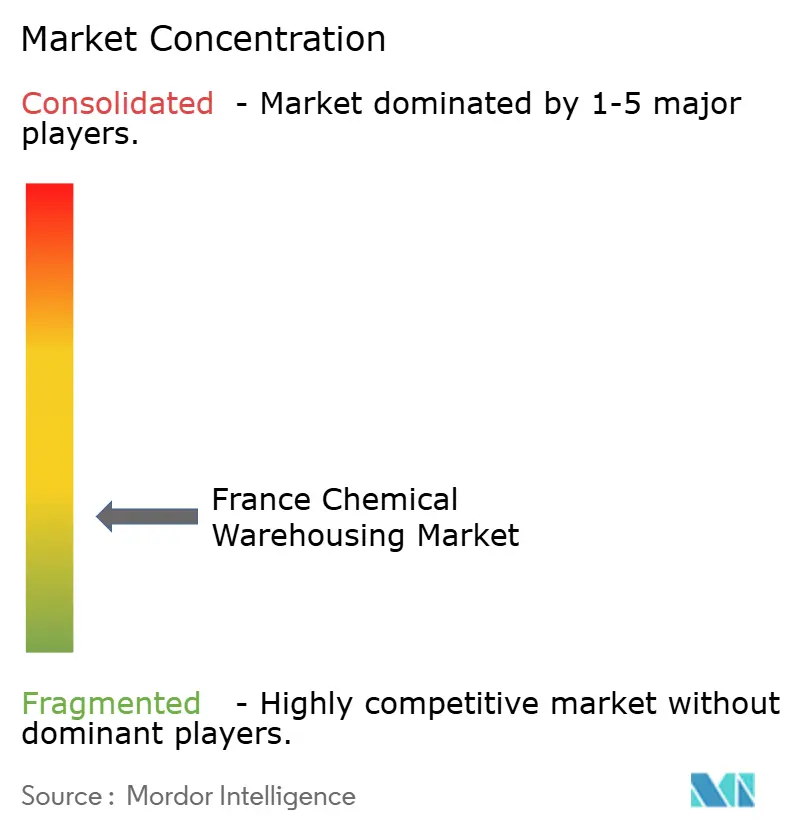

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Chemical Warehousing Market Analysis by Mordor Intelligence

The France Chemical Warehousing Market size is expected to increase from USD 3.17 billion in 2025 to USD 3.30 billion in 2026 and reach USD 3.99 billion by 2030, growing at a CAGR of 3.85% over 2026-2030.

France remains Europe’s second-largest chemical producer with 13% of EU chemical sales, which sustains baseline storage demand even as operators adjust capacity to evolving product mixes and compliance requirements. Production in several basic chemical categories stayed below mid-2021 levels through 2024, which tempered utilization in bulk-commodity depots and shifted focus toward higher-specification warehouses serving pharmaceuticals and specialty chemicals. Investment softness in 2024 and tighter post-2019 safety expectations encourage consolidation among facilities that lack scale or upper-tier SEVESO certifications, while incumbents deploy capital toward energy efficiency, digital monitoring, and temperature control to differentiate services. Port and inland-corridor programs are improving multimodal options and site availability. This supports clustering of chemical warehousing near maritime and river gateways linked to Lyon and the Seine axis. Pharmaceutical API reshoring and life sciences investments expand demand for GDP-certified temperature-controlled storage, which lifts the premium segment of the France chemical warehousing market.

Key Report Takeaways

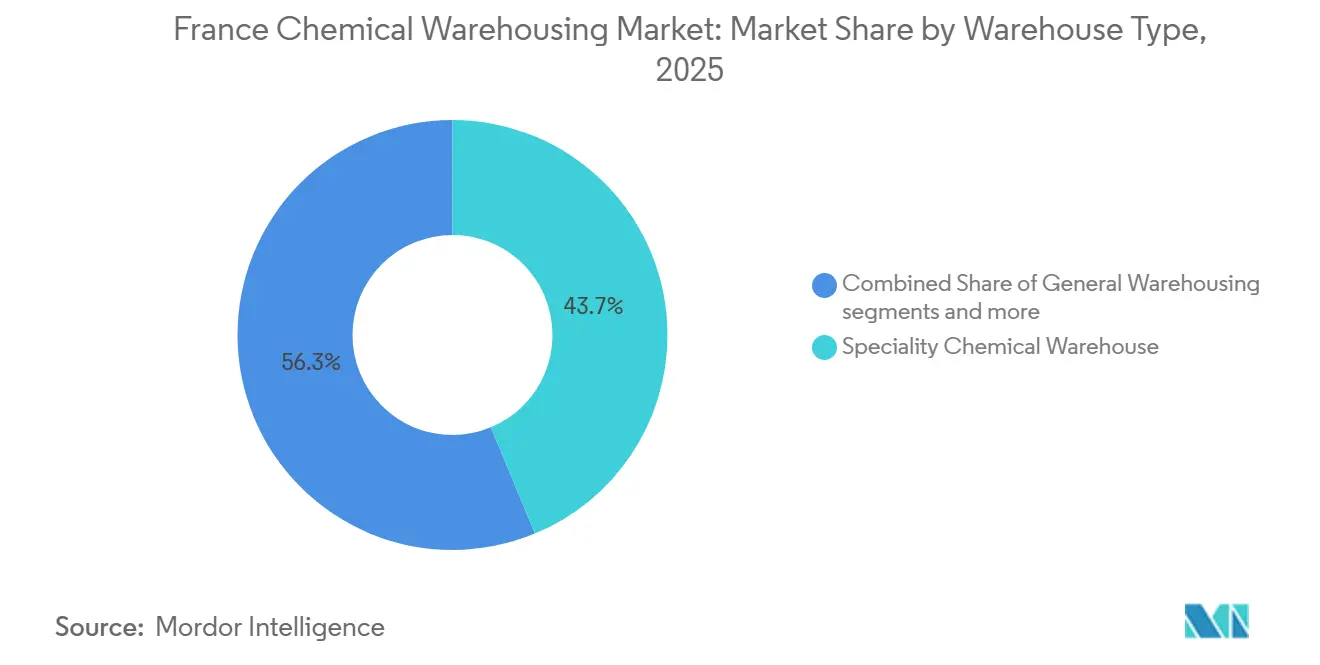

- By warehouse type, Specialty Chemical Warehouses led with 43.74% of France chemical warehousing market share in 2025, while Temperature-Controlled Chemical Warehouses are projected to record the fastest 4.65% CAGR through 2031.

- By chemical type, Flammable Liquids accounted for 34.62% share of the France chemical warehousing market size in 2025, and Toxic Substances are expected to advance at a 4.86% CAGR through 2031.

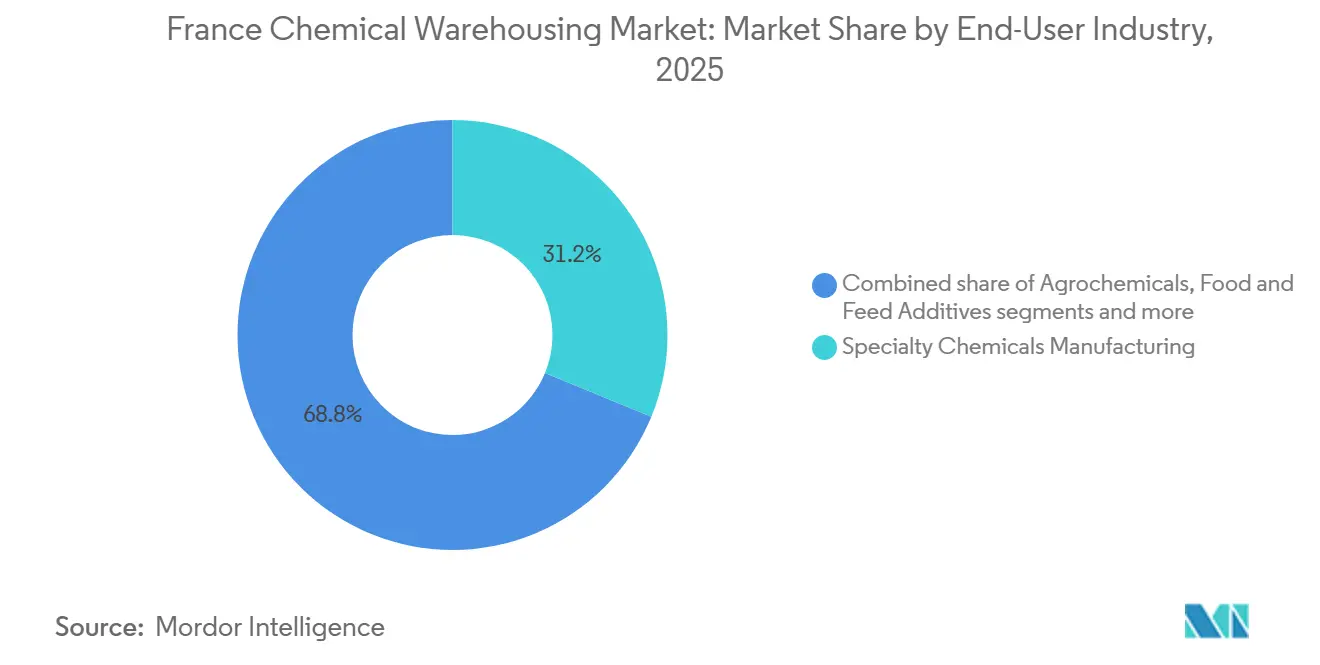

- By end-user industry, Specialty Chemicals Manufacturing held 31.21% share in 2025, while Pharmaceuticals & Life Sciences is forecast to expand at a 5.24% CAGR to 2031.

- By geography, Île-de-France was the largest regional base in 2025, and Auvergne-Rhône-Alpes is projected to post the fastest 4.2% CAGR during 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

National developments in France connect differently with activity unfolding across other parts of the world. In the global chemical warehousing market coverage, Mordor Intelligence integrates these into a single analytical framework.

France Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strategic European Logistics Hub Position | +0.6% | National, with concentrated gains in Grand Ports Maritimes (Le Havre, Marseille, Dunkirk) and the Lyon-Rhône corridor | Medium term (2-4 years) |

| Pharmaceutical and Cosmetics Industry Strength | +1.2% | National, with primary clusters in Île-de-France, Lyon Gerland, Normandy, and Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| Lyon Chemical Valley Expansion | +0.5% | Regional, concentrated in Lyon metropolitan area, Chemical Valley platforms, spill-over to Grenoble-Isère | Long term (≥ 4 years) |

| Port Infrastructure Development | +0.7% | National coastal and inland ports: Le Havre-Seine Axis, Marseille-Fos, Dunkirk, Lyon-Rhône-Saône axis, future Seine-Nord corridor in Hauts-de-France | Long term (≥ 4 years) |

| Industrial Chemicals for Manufacturing | +0.4% | National, with key concentrations in Normandy petrochemicals, Rhône-Alpes specialty chemicals, and Hauts-de-France industrial chemistry | Short term (≤ 2 years) |

| Energy Transition Chemical Storage | +0.6% | Regional clusters in Normandy, Lyon-Feyzin, and Grand Port Maritime zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strategic European Logistics Hub Position

France’s location on both Atlantic and Mediterranean seaboards and its borders with six EU member states concentrate flows through maritime gateways and inland nodes that now benefit from new industrial land commitments and multimodal connectivity programs. The state’s March 2024 plan to bring early EUR 1 billion to 1,500 hectares across the three largest port zones by 2030 expands co-location options for chemical warehousing, blending, and distribution alongside green-fuel, battery, and petrochemical projects. Policy initiatives within the national logistics strategy also stress sustainable supply chains and better spatial planning, which align with land-use and ZFE constraints and steer new capacity toward multimodal sites with rail and river access. Strengthening of the Rhône-Saône axis and inland terminals supports barge-to-warehouse transshipment of bulk liquids and tank containers, which reduces trucking dependencies and improves compliance for ADR cargo. The France chemical warehousing market benefits from this synchronized expansion. Operators can integrate port utilities, rail spurs, and shared safety infrastructure, lowering unit operating costs in concentrated clusters. The result is a gradual shift of new build decisions toward these corridors, which reinforces a hub-and-spoke model for national distribution centered on coastal ports and Lyon.

Pharmaceutical and Cosmetics Industry Strength

France’s medicine and cosmetics complexes underpin a large and persistent need for high-specification storage, including cold chain, clean zones, and validated processes that meet GDP and ISO quality requirements. Pharmaceutical production spans 271 sites and supports national health sovereignty initiatives, while new API and biologics programs by Sanofi and EUROAPI drive adjacent demand for proximity warehousing with HEPA filtration, HVAC zoning, and validated batch traceability. Sanofi’s investments in biologics manufacturing, including capacity expansions at Vitry-sur-Seine and Le Trait, add specialized flows that rely on tight storage controls and clearly documented handling. EUROAPI’s Med4Cure programs further extend onshore production for corticosteroids, macrolides, and advanced particle engineering, which call for safe segregation and controlled environments in upper-tier SEVESO facilities. Purpose-built logistics assets, such as CEVA’s new Strasbourg site and Cryoport’s Paris-region center, illustrate the quality and temperature layers that have become standard in life sciences handling in France. The France chemical warehousing market sees the premium end of the spectrum expand as these health-sector projects mature and pull through ancillary chemical and packaging inventories that need compliant storage.

Lyon Chemical Valley Expansion

Decarbonization programs anchored in the Lyon Chemical Valley are shaping new requirements for warehousing near platform operators and R&D centers. The DECLYC initiative, led by AXELERA and the Métropole de Lyon, mobilizes industrial partners to reduce emissions through energy, hydrogen, and process efficiency work packages, which will influence siting and specifications for storage used by nearby producers and laboratories. Regional plans to improve energy systems, steam provision, and water footprints can tilt warehouse economics toward platform adjacency where shared services are accessible and where safety perimeters support SEVESO-compliant operations. A planned underground hydrogen link as part of broader European corridors supports growth in high-pressure cylinder handling and specialized bay configurations, which may expand niche storage categories within the France chemical warehousing market. Circular-economy initiatives like the Circulyz eco-park create a need for contamination-controlled reverse logistics for recovered solvents and secondary raw materials, which require clear segregation from virgin inputs. Inland waterway enhancements at Port Edouard Herriot also support tank-container flows for chemical goods that benefit from river-to-warehouse orchestration.

Port Infrastructure Development

The Grand Ports Maritimes framework centralizes capacity growth at Le Havre, Marseille-Fos, and Dunkirk, while public commitments to open large tracts of industrial land by 2030 expand options for operators to build vertically integrated chemical logistics clusters. This land pipeline is important for the France chemical warehousing market because it pairs with ongoing investments in rail and barge connectivity, which allow better modal balance for hazardous cargo and reduce last-mile constraints. [1]Ministère de la Transition Écologique, “Strategie Logistique,” Ministère de la Transition Écologique, consultations-publiques.developpement-durable.gouv.fr Marseille-Fos has invested in rail and inland movements and maintains barge capacity along the Rhône-Saône corridor, where reliability improvements support time-sensitive chemical shipments destined for Lyon and other inland terminals. On the Seine axis, the LNG FSRU in Le Havre underpins feedstock availability for energy-intensive chemical processes, which sustains upstream and downstream warehousing for associated intermediates. New inland links, such as the future Seine-Nord Europe canal, also enable larger-barge flows and can lift waterfront depot development in Hauts-de-France once commissioned. This network of ports and waterways forms a backbone that supports warehousing density in locations with shared utilities and established safety infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor Costs and Social Charges | -0.8% | National, with acute pressure in Île-de-France and high-wage metropolitan areas | Medium term (2-4 years) |

| Complex ICPE Authorization Process | -0.5% | National, with concentrated effects in regions with high Seveso-site density | Long term (≥ 4 years) |

| Frequent Industrial Action and Strikes | -0.3% | National, with elevated disruption in unionized logistics hubs | Short term (≤ 2 years) |

| Stringent Environmental Liability Regime | -0.6% | National, with heightened compliance burdens on Seveso upper-tier sites and ICPE installations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Energy Costs for Cold Warehouses

Employer contributions in France remain significant, and recent threshold changes for social charges have tightened eligibility for lower-rate brackets, which raises effective employment costs for many warehouse roles. Adjustments that took effect in 2025 increase the wage bases to which some contributions apply, which adds pressure to operators that rely on ADR-certified staff whose compensation bands fall into the newly constrained thresholds. The annual ceiling for social security rose in 2025 and is set to rise again in 2026, which lifts contributions calculated on those bases and increases payroll outlays in absolute terms for operators. Energy costs remain volatile as well, and the 2024 industrial energy bill stayed above its 2019 level, which narrows margins and reduces operators’ ability to absorb parallel wage growth. Negotiated wage increases and limited productivity gains across the market sector add to the challenge of maintaining unit costs in line with contract pricing. The France chemical warehousing market, particularly the cold-chain segment, must therefore continue to invest in automation and energy-saving technologies to offset payroll drift and protect service levels.

Complex ICPE Authorization Process

Chemical warehousing is typically registered under ICPE categories that require robust submissions and prefectoral authorizations, which extend lead times for new capacity and increase the cost of greenfield market entry. Environmental authorization dossiers include detailed impact and hazard studies, and projects that cross SEVESO thresholds must align with European and national safety directives, which together lengthen the project cycle. Since 2023, PFAS disclosure and monitoring obligations for many ICPE facilities have added new analytical requirements, and periodic reporting schedules challenge laboratories and assets that must comply on tight timelines. Installations that blend or repack can straddle multiple rubrics and, in some cases, IED frameworks, which raises documentation expectations and can add steps during reviews.[2]data.gouv.fr, “ICPE Concerned by IED – Nouvelle-Aquitaine,” data.gouv.fr, data.gouv.fr Regional inspection services maintain close oversight in high-density zones such as Hauts-de-France, which helps maintain safety standards while also increasing the need for specialist compliance teams inside warehouse operators. The France chemical warehousing market therefore tends to reward incumbents with established ICPE sites and documentation muscle that can navigate authorization cycles and adjust to evolving environmental rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Temperature-Controlled Facilities Lead Growth as Biologics Reshoring Accelerates

Specialty Chemical Warehouses captured 43.74% in 2025, supported by higher-value intermediates and batch-segregated inventories that require inerting, controlled climates, and rigorous traceability, which anchor premium pricing within the France chemical warehousing market. Temperature-Controlled Chemical Warehouses are projected to post the fastest 4.65% CAGR through 2031 as new biologics and API programs expand the scope and stringency of GDP-compliant storage near production hubs, adding to the France chemical warehousing market size at the top end of specifications. New facilities such as CEVA’s Strasbourg site and Cryoport’s Paris-region center illustrate how temperature layering and clean handling have become operational baselines in health-related flows. This capability set tailors warehousing footprints around pharma manufacturing arcs in Île-de-France, Normandy, and Auvergne-Rhône-Alpes, where time-sensitive product requires short transfer distances. At the same time, commodity-oriented General Warehousing faces softer utilization where basic chemical output fell below mid-2021 levels, which trims bulk storage needs until downstream demand normalizes.

Hazardous Materials Warehouses continue to consolidate toward operators that invest in safety systems, digital monitoring, and compliance expertise, which aligns with national oversight intensity and SEVESO criteria at upper thresholds. Inland waterway and rail-served depots strengthen the proposition for hazardous flows by reducing road exposure and enabling gate-to-gate movements within safety perimeters. The France chemical warehousing industry therefore bifurcates, with ambient commodity sites adjusting to flatter volumes and premium temperature-controlled assets expanding in line with pharmaceutical and specialty chemical growth. Warehouse operators that co-locate within port and platform zones can leverage shared utilities and emergency systems that reduce unit costs and capex per pallet for compliant storage. This positions multimodal clusters as preferred destinations for new builds and expansion projects through the forecast period.

By Chemical Type: Toxic Substances Fastest Growth Amid Pharmaceutical API Complexity

Flammable Liquids held 34.62% in 2025 within the France chemical warehousing market, reflecting the footprint of petrochemical supply chains and the need for bunded storage, foam suppression, and compliant transfer systems under the relevant ICPE rubrics. Toxic Substances are projected to grow at 4.86% CAGR through 2031 as onshore API and biologics projects involve intermediates and HPAPIs that require sealed handling, negative-pressure zones, and fine particulate filtration to meet occupational and product-safety limits. This evolution expands the France chemical warehousing market size at the higher-specification end of the chemical-type mix and raises the importance of integrated digital traceability. Corrosives and oxidizers show steadier demand patterns tied to industrial applications and water treatment, with growth rates constrained by substitution trends and slower cycles in certain heavy industry segments.

Future capacity planning increasingly distinguishes between passive containment for flammable products and active mitigation systems for toxics, which implies higher capital intensity where vapor capture and scrubber systems are warranted. Operators that can concentrate such assets across multiple sites gain economies of scale in maintenance and compliance documentation, which can lower long-run costs per pallet for high-risk categories. Inland terminals linked to river corridors support drayage alternatives for dangerous goods that benefit from fewer urban interfaces and closer integration with platform utilities. As a result, chemical-type portfolios are shifting toward more controlled environments in regions with strong life sciences and specialty chemical pipelines.

By End-User Industry: Pharmaceuticals Lead Growth Trajectory

Specialty Chemicals Manufacturing held 31.21% of France chemical warehousing market share in 2025, underpinned by sectors like coatings, electronics, and flavors that require clean, documented storage and frequent batch segregation. Pharmaceuticals & Life Sciences is expected to grow at 5.24% CAGR to 2031 due to large-scale biomanufacturing commitments, onshoring of APIs, and stronger distribution requirements for temperature-sensitive therapies, which lift the premium segment of the France chemical warehousing market. Strategic investments by global logistics providers continue to densify cold-chain footprints in regions such as Alsace and Île-de-France, where facilities are purpose-built to GDP and ISO standards and integrate advanced traceability systems.

Basic chemical chains contend with softer utilization that mirrors production gaps against 2021 baselines, which affects tank farms and large-lot storage pending stronger export cycles in nearby European markets. In contrast, distribution networks for life sciences and high-spec specialties have tighter service-level requirements that favor certified operators with robust quality systems and audit readiness, which supports margin stability even as input costs fluctuate. Select retail-adjacent categories, such as cosmetics, overlap with this infrastructure through ambient and cool storage of formulations and packaging that value contamination-free handling. Investments by third-party logistics providers in the Lyon metropolitan area reinforce the role of platform-proximate hubs that can feed both regional manufacturing and national replenishment.

Geography Analysis

The France chemical warehousing market has its largest concentration in Île-de-France, Le Havre–Seine axis, Marseille-Fos, and the Lyon-Rhône corridor, supported by mature industrial bases and multimodal links that reinforce clustering economies. Île-de-France hosts significant pharmaceutical and cosmetics hubs, which sustain demand for temperature-controlled storage and validated handling close to manufacturing and distribution nodes. National logistics strategies emphasize sustainable capacity planning and land-use coherence, which is material in dense regions where greenfield options tighten, and logistics observatories guide development choices. The France chemical warehousing market size at the premium end continues to grow in the capital region due to ongoing life sciences logistics investments and the presence of API programs that require strict environmental controls.

Auvergne-Rhône-Alpes is projected to be the fastest-growing region at a 4.2% CAGR to 2031, linked to the Lyon Chemical Valley’s decarbonization and innovation agenda, which aligns warehousing with platform utilities and shared infrastructure. River terminal enhancements at Port Edouard Herriot support barge-served chemical flows that can be routed to nearby sites, which reduces road mileage and handling complexity for hazardous cargo. The France chemical warehousing market benefits regionally from platform adjacency and coordination among industrial partners, which improve the business case for high-specification warehouses near production and R&D clusters. Significant life sciences and specialty chemical flows add to the need for certified operations that can meet consistent service levels under audit conditions.

Normandy and Hauts-de-France also see structural opportunities from energy and inland-waterway programs. The LNG FSRU in Le Havre enlarges energy import options and supports upstream chemical value chains connected to the Seine corridor, which add to warehousing activity around raw and intermediate materials. The future Seine-Nord Europe canal will reinforce barge modalities for heavy and hazardous cargo and expand the case for waterfront depots with direct barge-to-warehouse interfaces once operational. Oversight structures in northern regions have strong ICPE controls, which raise operating standards and favor experienced operators who can maintain compliant operations at scale. In the south, Marseille-Fos’s industrial-port ecosystem supports large-scale warehousing with multimodal options and shared services that reduce per-unit costs in chemicals logistics.

Mordor Intelligence's coverage of the chemical warehousing market extends across other regions including Europe, Middle East, and Africa, while country-specific intelligence is also available for Italy, Germany, China, India, South Korea, and Canada, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The France chemical warehousing market is fragmented and shaped by scale players that combine multimodal density, strong certifications, and digital capabilities. The integration of DB Schenker into DSV’s network in 2026 expanded DSV’s French footprint, bringing sizable warehouse capacity and deep capabilities in health and regulated goods logistics.[3]DSV, “DSV intègre Schenker en France,” DSV, dsv.com Companies with platform-proximate sites leverage port and inland terminal utilities, shared safety perimeters, and better rail and river access, which lower operating costs for hazardous and temperature-sensitive flows. Life sciences-oriented providers continue to expand GDP-compliant footprints in regions such as Alsace and Île-de-France, reflected in CEVA’s specialized pharma facility in Strasbourg and Cryoport’s Paris-region center.

Strategic moves include targeted site acquisitions and long-term concessions that secure space near industrial corridors and strengthen time-to-market for sensitive cargo. DHL Supply Chain’s acquisition of a site in the Lyon metropolitan area illustrates pre-emptive positioning in a high-potential region aligned with life sciences and advanced materials demand. Distribution and specialty chemical groups invest in product stewardship and sustainability portfolios that influence warehousing needs, including transitions toward PFAS management, safer formulations, and packaging shifts that alter storage and handling requirements. In parallel, expansions in Northern Europe logistics networks by liquid chemicals carriers create routing and equipment synergies for flows touching France, which supports cross-border service continuity for hazardous cargo.

Competitive differentiation increasingly depends on integrated quality systems, audit readiness, and digitization. Operators deploy WMS and WCS platforms, real-time monitoring, and analytics to improve slotting, temperature mapping, and maintenance cycles in line with the France chemical warehousing market’s shift toward high-specification services. Energy-efficiency investments such as LEDs, rooftop solar, and smart controls lower operating expenses and improve resilience during tariff or excise volatility, which preserves margins as wage costs and compliance outlays rise. These capabilities, combined with inland and maritime connectivity, enable leaders to meet strict service levels and scale across regions without diluting safety and quality performance.

France Chemical Warehousing Industry Leaders

DHL Group

Geodis

Hoyer Group

Brenntag

Den Hartogh Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DSV completed the integration of DB Schenker in France, consolidating a network that includes specialized contract logistics for health and regulated sectors and a broad domestic distribution footprint.

- February 2026: France Chimie highlighted a critical investment decline and underutilized production capacity, reinforcing the need for European-level measures to secure competitiveness, which may influence domestic logistics planning.

- November 2025: Brenntag Specialties and Calyxia formed a distribution partnership focused on advanced materials solutions, which supports a shift toward sustainable chemistry and handling requirements in ambient warehouse environments.

- November 2025: Dantra Group joined HOYER Group, expanding the combined network in Northern Europe for liquid chemicals logistics and creating synergies for cross-border flows that connect to France.

France Chemical Warehousing Market Report Scope

The France chemical warehousing market is segmented by warehouse type (General, Specialty, HAZMAT, and Temperature-Controlled), by chemical type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, and Others), end-user industry (Basic Chemicals, Specialty Chemicals, Pharmaceuticals, Agrochemicals, Paints/Coatings, Food Additives, Oil & Gas, and Others), and geography. Market forecasts are in value terms, USD.

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the France chemical warehousing market size and growth outlook to 2031?

The France chemical warehousing market size is expected to increase from USD 3.30 billion in 2026 to USD 3.99 billion by 2031 at a 3.85% CAGR, following USD 3.17 billion in 2025.

Which warehouse types are leading and growing fastest in France?

Specialty Chemical Warehouses led with 43.74% share in 2025, while Temperature-Controlled Chemical Warehouses are projected to post the fastest 4.65% CAGR through 2031.

Which chemical categories will expand storage needs most in France by 2031?

Toxic Substances are expected to grow the fastest at 4.86% CAGR due to API and biologics complexity, while Flammable Liquids held 34.62% in 2025.

Which end-user segments are most attractive for operators in France?

Specialty Chemicals Manufacturing held 31.21% share in 2025, and Pharmaceuticals & Life Sciences are set to expand at a 5.24% CAGR to 2031 on the back of onshore biomanufacturing.

Which regions offer the strongest opportunities for new facilities?

Île-de-France remains the largest base, and Auvergne-Rhône-Alpes is projected to grow the fastest at 4.2% CAGR due to Lyon Chemical Valley’s decarbonization and innovation agenda.

What strategic factors differentiate leading operators in France?

Certification depth, multimodal connectivity, and digitization, including GDP and ISO frameworks, rail and river access, and real-time monitoring, are the primary differentiators.

Page last updated on: