United States Benzathine Penicillin G Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

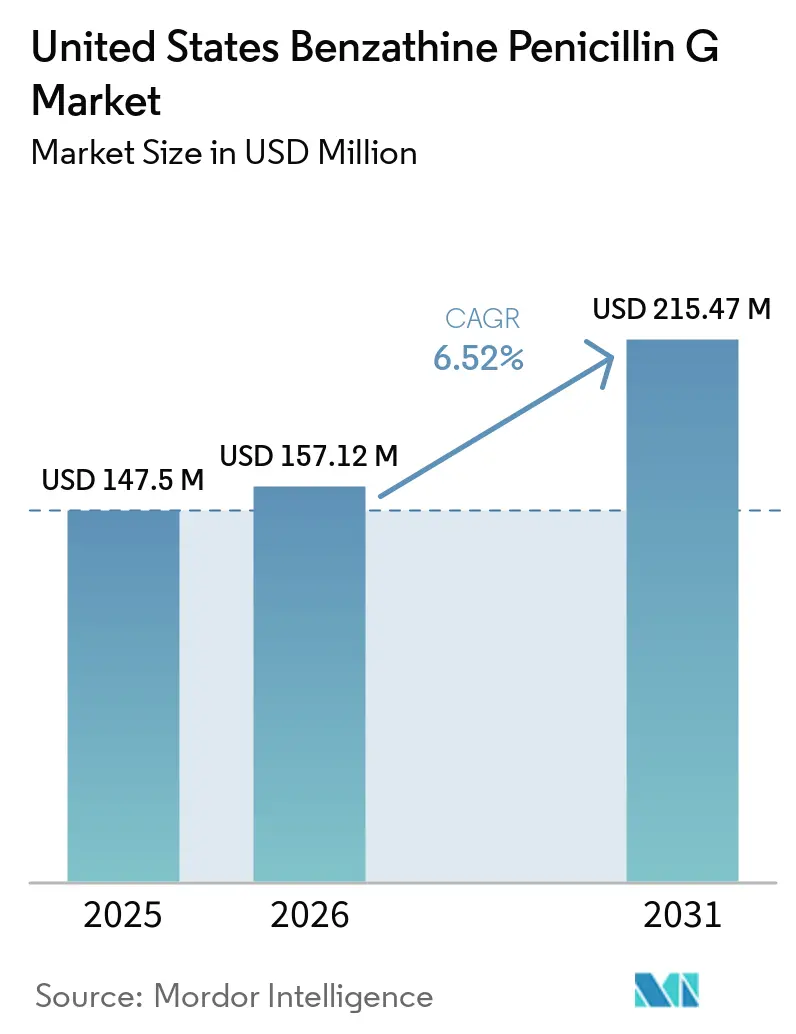

| Base Year Market Size (2025) | USD 147.5 Million |

| Market Size (2026) | USD 157.12 Million |

| Market Size (2031) | USD 215.47 Million |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

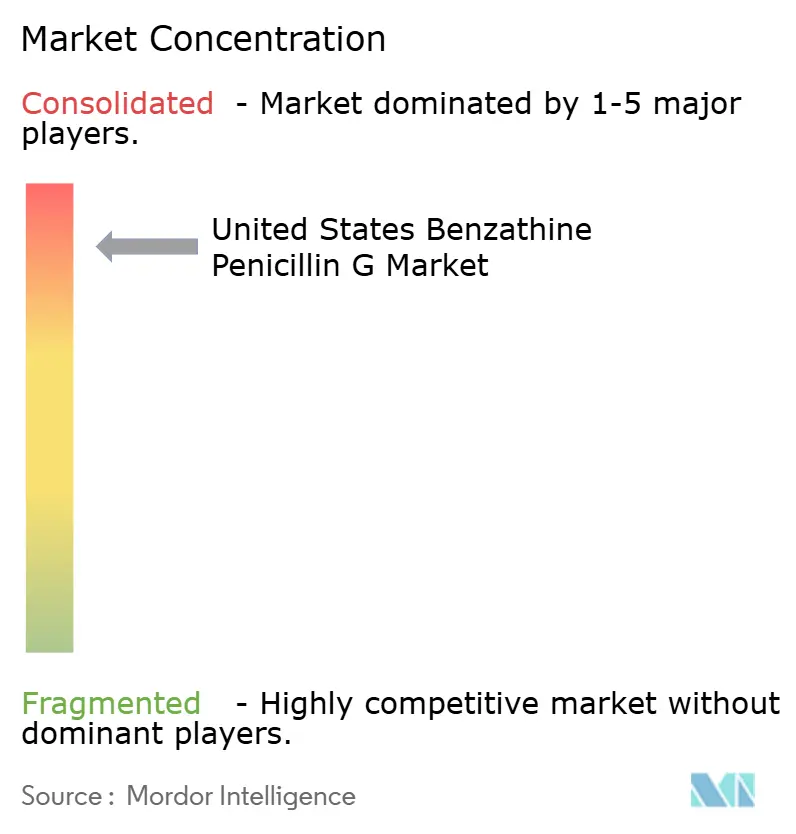

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Benzathine Penicillin G Market Analysis by Mordor Intelligence

The United States Benzathine Penicillin G Market size is projected to be USD 147.5 million in 2025, USD 157.12 million in 2026, and reach USD 215.47 million by 2031, growing at a CAGR of 6.52% from 2026 to 2031.

The market is being shaped by the combined pull of congenital syphilis treatment, persistent adult latent syphilis therapy, and long-duration rheumatic fever prophylaxis rather than by new product launches or broader label expansion. Demand in the United States benzathine penicillin G market is unusually rigid because these use cases depend on a single established injectable therapy and there is no clinically acceptable oral substitute in key patient groups, especially during pregnancy and in long-term prophylaxis settings. The United States benzathine penicillin G market is also being defined by supply reliability, since repeated shortages have shifted procurement behavior toward temporary imports, direct clinical allocation, and tighter public health stewardship. This has made the United States benzathine penicillin G market less responsive to normal pricing or channel changes and more responsive to case burden, treatment urgency, and stock availability in high-incidence states. The result is a market where future opportunity rests less on expanding use and more on restoring dependable supply, widening qualified sourcing, and supporting clinic-level access in regions with the highest public health need.

Key Report Takeaways

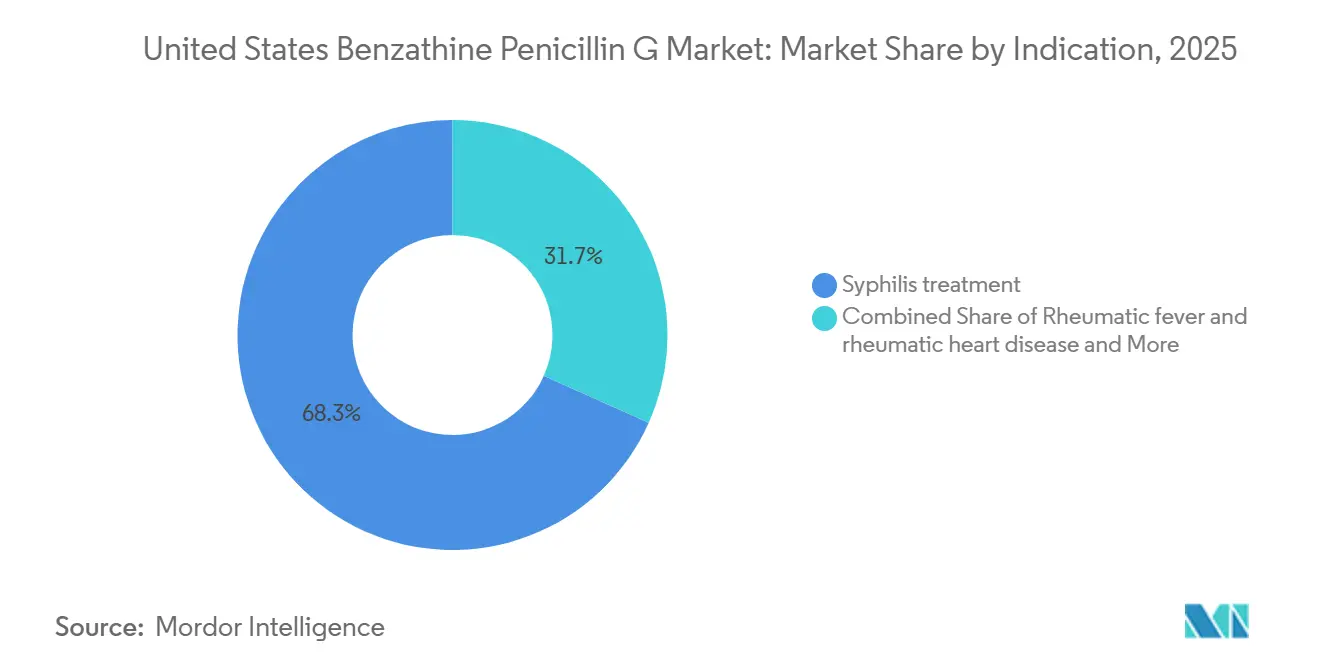

- By indication, syphilis treatment held 68.31% of the United States benzathine penicillin G market share in 2025, while rheumatic fever and rheumatic heart disease prophylaxis is projected to expand at 7.38% CAGR through 2031.

- By procurement channel, wholesalers accounted for 45.24% share in 2025, while emergency import channels are forecast to grow at 8.83% CAGR through 2031.

- By product presentation, prefilled syringes accounted for 73.24% share of the United States benzathine penicillin G market size in 2025, while powder and diluent for suspension is forecast to advance at 8.52% CAGR through 2031.

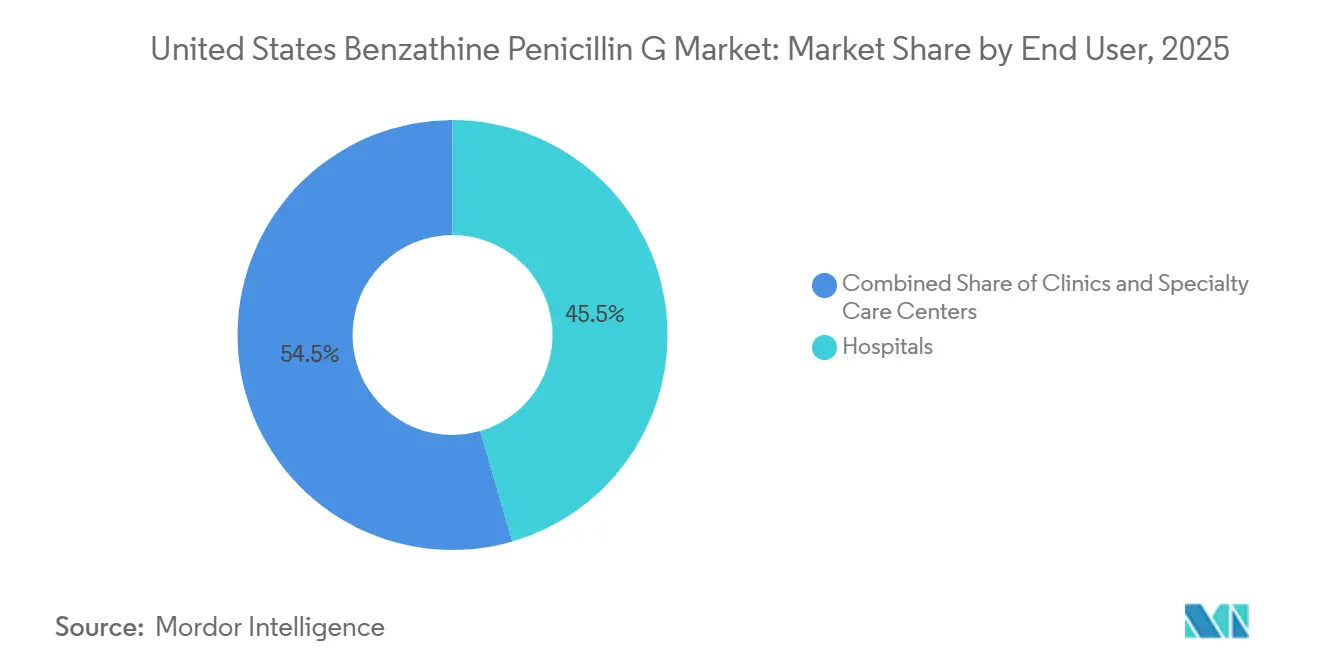

- By end user, hospitals held 45.52% share in 2025, while clinics are expected to record the fastest growth at 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Benzathine Penicillin G Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Congenital Syphilis Treatment Urgency | +2.0% | South, Southwest, Southeast US, highest impact in TX, AZ, MS, LA, CA | Short term (≤ 2 years) |

| Persistent Adult Syphilis Caseload And Repeat-Dose Latent Therapy | +1.5% | National, concentrated in urban cores and rural high-prevalence counties | Medium term (2-4 years) |

| Need For Long-Acting Rheumatic Fever Prophylaxis | +0.8% | National, with elevated impact in lower-income and underinsured populations | Long term (≥ 4 years) |

| Temporary Import Pathways Expand Powder-Format Demand | +1.0% | National, spillover to public health networks in shortage-impacted states | Short term (≤ 2 years) |

| Public-Health Buffer Stocking And Direct Clinic Procurement | +0.5% | National, with early gains in states with active public health tender programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Congenital Syphilis Treatment Urgency

Congenital syphilis remains the clearest immediate demand trigger in the United States benzathine penicillin G market because the CDC reported nearly 4,000 newborn cases in 2024 and described that total as the twelfth straight annual increase and 700% above 2015 levels[1]Centers for Disease Control and Prevention, “Sexually Transmitted Infections Surveillance, 2024 (Provisional),” CDC STI Statistics, cdc.gov.. The case total understates drug demand because every confirmed infant case can also lead to maternal treatment, partner treatment, and broader prenatal follow-up that consumes additional doses. This means that one reported event can translate into several treatment courses across connected care settings rather than a single isolated prescription. The heaviest pressure falls on Southern and Southwestern states, where case intensity is already high and public health programs often direct supply toward pregnant patients first. As a result, any disruption in manufacturing or allocation reaches the most urgent patients early and keeps the United States benzathine penicillin G market tightly linked to maternal and neonatal care capacity.

Persistent Adult Syphilis Caseload And Repeat-Dose Latent Therapy

The adult syphilis burden still supports broad baseline demand in the United States benzathine penicillin G market even though primary and secondary syphilis declined in 2024 from the prior year. Treatment intensity matters more than headline case counts because latent and late-latent disease require three weekly doses of 2.4 million units, which creates much higher volume per patient than early-stage infection. This dosing pattern turns latent cases into a strong volume driver that can remain hidden when planners focus only on reported incident infections. Demand also moves through the system more slowly than it does for acute symptomatic care, which can leave inventory planning out of step with actual refill needs. That lag helps sustain shortage conditions and keeps the United States benzathine penicillin G market exposed to repeat stress even when the most visible STI indicators appear to improve.

Need For Long-Acting Rheumatic Fever Prophylaxis

Rheumatic fever and rheumatic heart disease prophylaxis is a smaller part of current demand, but it is one of the most durable supports for the United States benzathine penicillin G market. WHO updated its guidance in 2024 and continued to support intramuscular benzathine penicillin G as the preferred secondary prophylaxis approach for eligible patients who require long-term protection from recurrence[2]World Heart Federation, “A Global Milestone, WHO Launches New Guidelines to Combat Rheumatic Heart Disease,” World Heart Federation, world-heart-federation.org.. The supporting evidence base remained strong, with a 14-fold reduction in recurrence for intramuscular therapy compared with oral regimens. This matters in the United States because a small but real patient pool exists in underserved communities, including Indigenous groups and recent immigrant populations, where long-duration prophylaxis cannot be deferred easily. Each newly retained patient adds recurring injections over multiple years, which gives this indication a steadier demand profile than outbreak-driven STI treatment.

Temporary Import Pathways Expand Powder-Format Demand

Temporary import authorizations have changed how the United States benzathine penicillin G market functions during shortage periods because the FDA opened access to Extencilline from France in January 2024 and Lentocilin from Portugal in July 2024. Both products arrived as powder and diluent for suspension rather than the prefilled syringes that many U.S. providers had used for years. That difference forced clinical teams to adopt reconstitution workflows, but it also widened the practical supply base when domestic stock could not meet need. Public health clinics and specialty centers adapted faster because they already handled higher-acuity patients and had staff who could absorb new preparation steps. This has given powder formats a more durable place in the United States benzathine penicillin G market and supported continued adoption beyond the first emergency response phase.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-Source Domestic Supply And Prolonged Shortage Risk | -1.2% | National, most acute in high-demand Southern and Southwestern states | Short term (≤ 2 years) |

| Sterile Injectable Manufacturing And Cold-Chain Complexity | -0.8% | National, barriers to new entrant manufacturing disproportionate in rural supply chains | Long term (≥ 4 years) |

| Powder Reconstitution Workflow Slows Imported-Product Uptake | -0.4% | National, concentrated in outpatient clinics and rural health settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-Source Domestic Supply And Prolonged Shortage Risk

The largest restraint on the United States benzathine penicillin G market is the continued reliance on one FDA-approved domestic manufacturer. Pfizer's King Pharmaceuticals subsidiary remained the sole approved domestic source, which left the entire market exposed when shortage cycles persisted after April 2023 and when the July 2025 recall removed critical prefilled syringe lots from circulation. Pfizer's January 2026 update still showed allocation at the wholesaler level and delayed recovery for key presentations, and later updates extended recovery expectations further into 2027. The wider sterile injectable shortage pattern also matters because quality failures and limited margins have repeatedly disrupted low-cost injectable drugs across the healthcare system. That leaves the United States benzathine penicillin G market in a position where medical need exists, but treatable volume still depends on whether one supply chain can perform without interruption.

Sterile Injectable Manufacturing And Cold-Chain Complexity

Benzathine penicillin G remains difficult to manufacture at scale because it combines specialized sterile processing with demanding quality control expectations. The product must meet strict particle and suspension characteristics, move through aseptic fill-finish steps, and retain integrity across refrigerated handling and distribution. These requirements narrow the list of manufacturers that can move from chemical capability to dependable finished-dose supply for the United States benzathine penicillin G market. The compliance burden is also rising because updated contamination control expectations apply to international suppliers that may want to serve U.S. shortages. Even when temporary imports are allowed, the combination of sterility, validation, packaging, and cold-chain execution slows scale-up and keeps replacement capacity limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Syphilis Drives Volume, Prophylaxis Reshapes The Long-Term Mix

Syphilis treatment accounted for 68.31% share in 2025, which kept it firmly at the center of the United States benzathine penicillin G market. That position reflects the continued scale of congenital and adult syphilis treatment need, with the CDC reporting nearly 4,000 congenital syphilis cases in 2024 and continued national STI pressure. Syphilis also has high clinical urgency because treatment cannot be delayed easily in pregnancy and latent infection often requires multi-dose therapy. Other indication categories remain smaller, but they are still medically necessary and do not behave like discretionary demand.

Rheumatic fever and rheumatic heart disease prophylaxis is projected to grow at 7.38% CAGR through 2026-2031, making it the fastest-expanding indication in the United States benzathine penicillin G market. WHO's 2024 guidance reinforced intramuscular prophylaxis as the preferred long-term approach and a strong recurrence advantage over oral therapy. This segment grows differently from syphilis because patients can remain on therapy for years and require repeated injections at regular intervals. That long-duration pattern means new patient starts continue to build demand even if syphilis case growth becomes less severe over time.

By Product Presentation: Prefilled Syringes Lead, But Powder Formats Gain Ground

Prefilled syringes captured 73.24% share in 2025 and remained the dominant presentation within the United States benzathine penicillin G market. Their lead came from provider familiarity, faster administration, and lower preparation burden in busy clinical settings. That advantage was weakened by the 2025 recall, which removed important prefilled lots and exposed the risk of relying too heavily on one format and one domestic source. The recall period also pushed more providers to reassess their willingness to use formats that require reconstitution if that meant securing reliable supply.

Powder and diluent for suspension is projected to grow at 8.52% CAGR through 2026-2031, which makes it the fastest-growing product segment. FDA enforcement discretion brought Extencilline and Lentocilin into the country in this format, creating a practical supply path that had not existed before 2024. As high-volume public health sites gain more comfort with reconstitution, the workflow penalty becomes easier to manage. That supports lasting format diversification in the United States benzathine penicillin G market even after some domestic syringe supply returns.

By End User: Hospitals Anchor Current Demand, Clinics Expand Faster

Hospitals held 45.52% share in 2025, which kept them as the largest end-user group in the United States benzathine penicillin G market. They remain central because congenital syphilis treatment in neonates, high-risk maternal care, and severe streptococcal infections often move through hospital-linked teams. CDC and Pfizer guidance during shortage periods also directed the most limited product toward the most urgent patients, which reinforced hospital importance in allocation decisions. Specialty centers still represent a meaningful channel, especially for STI care and long-term prophylaxis, even if some of their volumes sit outside standard commercial visibility.

Clinics are projected to grow at 7.25% CAGR through 2026-2031, the fastest pace among end users. State public health programs have increasingly routed supply toward outpatient settings to improve access in high-burden communities and preserve hospital inventory for the most acute cases. Medicaid coverage for imported products also made clinics more capable of treating patients during domestic shortages, especially where formal billing guidance was introduced. This supports a gradual channel shift in the United States benzathine penicillin G market toward outpatient treatment in public health heavy regions.

By Procurement Channel: Wholesalers Remain Largest, Emergency Imports Become Structural

Wholesaler procurement accounted for 45.24% share in 2025, which made it the largest formal channel in the United States benzathine penicillin G market. That lead reflects the long-established route through which Bicillin L-A moved to hospitals and pharmacies before the shortage deepened. During the recall period, however, wholesaler flow became more constrained because product remained on allocation and customers were often instructed to exhaust local availability before seeking direct requests[3]Pfizer Hospital US, “Availability Update for Bicillin L-A, August 21, 2025,” Pfizer, pfizerhospitalus.com.. This means the channel stayed large in structure, but it operated more as a controlled distribution tool than as a normal open market pathway.

Emergency import channels are forecast to expand at 8.83% CAGR through 2026-2031, the fastest rate among procurement routes. That growth suggests the United States benzathine penicillin G market has moved beyond a short-lived shortage response and into a more permanent multi-source access model. Once states, clinics, and health systems set up billing codes, supply agreements, and clinical workflows around imported products, those systems are likely to remain active even after domestic availability improves. Direct institutional contracting is also gaining relevance because large providers have learned that standard wholesale allocation may not fully cover non-discretionary treatment demand.

Geography Analysis

The heaviest demand concentration in the United States benzathine penicillin G market sits in the South and Southwest because congenital syphilis rates and case counts remain highest in those states. CDC state tables showed Texas with 930 congenital syphilis cases, Arizona with 233, California with 512, and Louisiana with 109, while Mississippi, Arizona, and Texas all posted rates far above the national level. Those figures explain why Southern and Southwestern public health systems became early users of emergency imports and clinic-directed allocation. These states carry both high treatment urgency and high operational pressure because pregnant patients and newborns cannot be shifted easily to alternative therapies. In practice, this makes the United States benzathine penicillin G market most sensitive to policy and supply decisions in a handful of high-burden jurisdictions.

The Western United States has a different but equally important demand profile within the United States benzathine penicillin G market. California combines high absolute volume with active state response, while Nevada and New Mexico show elevated rates that point to persistent prenatal care access gaps rather than simple population size effects. California's Department of Public Health issued detailed shortage and recall guidance in 2025 and directed conservation measures toward pregnant patients while supporting imported-product distribution networks. That kind of structured response matters because it gives providers a clearer pathway for triage, billing, and product substitution during supply shocks. Western states therefore play an outsized role in setting practical access patterns when shortages intensify.

Northeastern and Midwestern states carry lower absolute caseloads, but they still face meaningful risk because supply disruption in a single-source market affects every region. Their demand mix often leans more toward hospital-centered care and specialty follow-up, including patients on long-term rheumatic fever prophylaxis who need continuity rather than one-time treatment. Maryland, Illinois, and Ohio still reported notable congenital syphilis burdens in CDC tables, which means lower-volume regions cannot be treated as insulated from the crisis. As domestic recovery stretches into late 2026 and 2027, imported procurement infrastructure is likely to remain nationally relevant rather than fading once the highest-burden states stabilize.

Competitive Landscape

The United States benzathine penicillin G market is highly concentrated because Pfizer, through King Pharmaceuticals, remains the only FDA-approved domestic manufacturer of benzathine penicillin G injectable suspension. That position has made supply continuity more important than brand competition, since any quality issue or production gap at one company quickly becomes a nationwide access problem. The July 2025 voluntary recall of multiple Bicillin L-A lots showed how quickly that risk can convert into clinical rationing and extended recovery timelines. Pfizer's January 2026 availability update then confirmed that allocation remained in place for key presentations, which kept the supply picture tight into 2026. In this setting, competitive position is measured less by marketing reach and more by whether a supplier can deliver usable sterile product at scale.

Temporary imported competition has entered the United States benzathine penicillin G market through regulatory discretion rather than through standard domestic generic approval. Laboratoires Delbert gained access for Extencilline in January 2024, which created the first meaningful external supply support during the domestic shortage. Laboratórios Atral followed with Lentocilin in July 2024, and that authorization extended the pool of available imported doses into 2026. These companies compete less on formal share and more on availability, format, and speed of deployment under shortage conditions. Their presence has still changed the structure of the market because public health systems now have operating experience with non-domestic supply.

The remaining white space in the United States benzathine penicillin G market lies in domestic generic finished-dose entry, but the barriers are high. A prospective entrant would need more than penicillin chemistry expertise because sterile fill-finish capability, contamination control, regulatory compliance, and dependable cold-chain execution all matter at the finished-product level. That is why global antibiotic API capability has not yet translated into a visible wave of U.S. finished-dose entrants. Until that changes, the competitive structure will remain narrow, and imported stopgap suppliers will continue to matter whenever domestic output falls short of public health need.

United States Benzathine Penicillin G Industry Leaders

Pfizer Inc.

Laboratoires Delbert

Laboratórios Atral

Provepharm

Biopharma S.r.l.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: King Pharmaceuticals (Pfizer subsidiary) extended the next delivery of 1.2 million and 2.4 million unit prefilled syringe presentations to October 2026, with anticipated full recovery pushed to Q4 2027, further prolonging one of the longest-running critical drug shortages in recent US history and sustaining demand for imported alternatives through the forecast period.

- January 2026: Pfizer confirms wholesale allocation continuation. Pfizer's January 21, 2026 availability update confirmed that Bicillin L-A prefilled syringes remain on allocation at the wholesaler level, with next estimated delivery for pediatric 600,000 unit presentations in December 2026 and recovery Q4 2026, a timeline that effectively leaves pediatric presentations in chronic constraint through most of 2026.

United States Benzathine Penicillin G Market Report Scope

As per the scope of the report, benzathine penicillin G is a long-acting form of penicillin antibiotic used to treat bacterial infections. It is a penicillin antibiotic that is administered via intramuscular injection and provides sustained, low-level release of penicillin into the bloodstream, making it effective for treating conditions like syphilis, rheumatic fever, and streptococcal infections.

The segmentation for the United States benzathine penicillin G market by indication includes treating syphilis, prophylaxis for rheumatic fever and rheumatic heart disease, addressing Group A streptococcal infections, and other medical indications. By product presentation, the market is segmented into prefilled syringes and powder with diluent for suspension. By end user, the segmentation includes hospitals, clinics, and specialty care centers. By procurement channel, the market is segmented into wholesaler procurement, tenders from state and local public health, emergency import channels, and direct contracts with institutions. For each segment, the market size and forecast are provided in terms of value (USD).

| Syphilis treatment |

| Rheumatic fever and rheumatic heart disease prophylaxis |

| Group A streptococcal infections |

| Other Indications |

| Prefilled syringe |

| Powder and diluent for suspension |

| Hospitals |

| Clinics |

| Specialty Care Centers |

| Wholesaler procurement |

| State and local public-health tenders |

| Emergency import channels |

| Direct institutional contracting |

| By Indication | Syphilis treatment |

| Rheumatic fever and rheumatic heart disease prophylaxis | |

| Group A streptococcal infections | |

| Other Indications | |

| By Product Presentation | Prefilled syringe |

| Powder and diluent for suspension | |

| By End User | Hospitals |

| Clinics | |

| Specialty Care Centers | |

| By Procurement Channel | Wholesaler procurement |

| State and local public-health tenders | |

| Emergency import channels | |

| Direct institutional contracting |

Key Questions Answered in the Report

What is driving demand for benzathine penicillin G in the United States?

Demand is being driven by congenital syphilis treatment, persistent adult latent syphilis therapy, and long-term rheumatic fever prophylaxis. The market was valued at USD 147.50 million in 2025 and is projected to reach USD 215.47 million by 2031 at a CAGR of 6.52%.

Which indication accounts for the largest share of use in the United States?

Syphilis treatment led with a 68.31% share in 2025. Its scale reflects both maternal and adult treatment needs and the multi-dose burden of latent disease.

Why are emergency imports becoming more important for supply?

Emergency imports are becoming more important because the domestic market depends on a single FDA-approved manufacturer and repeated shortages have kept supply tight. This channel is projected to grow at 8.83% CAGR through 2031.

Which product format is growing the fastest?

Powder and diluent for suspension is the fastest-growing format at 8.52% CAGR through 2031. Growth is linked to imported products from France and Portugal that entered during the shortage period.

Which care settings use the most benzathine penicillin G?

Hospitals held the largest end-user share at 45.52% in 2025 because neonatal treatment, high-risk pregnancy care, and severe infections often route through hospital-linked teams.

Why is rheumatic fever prophylaxis important even though it is a smaller segment today?

It is the fastest-growing indication at 7.38% CAGR through 2031 because patients often remain on therapy for years and need repeated injections. That creates steady recurring demand even when STI case trends fluctuate.

Page last updated on: