Peptide Antibiotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

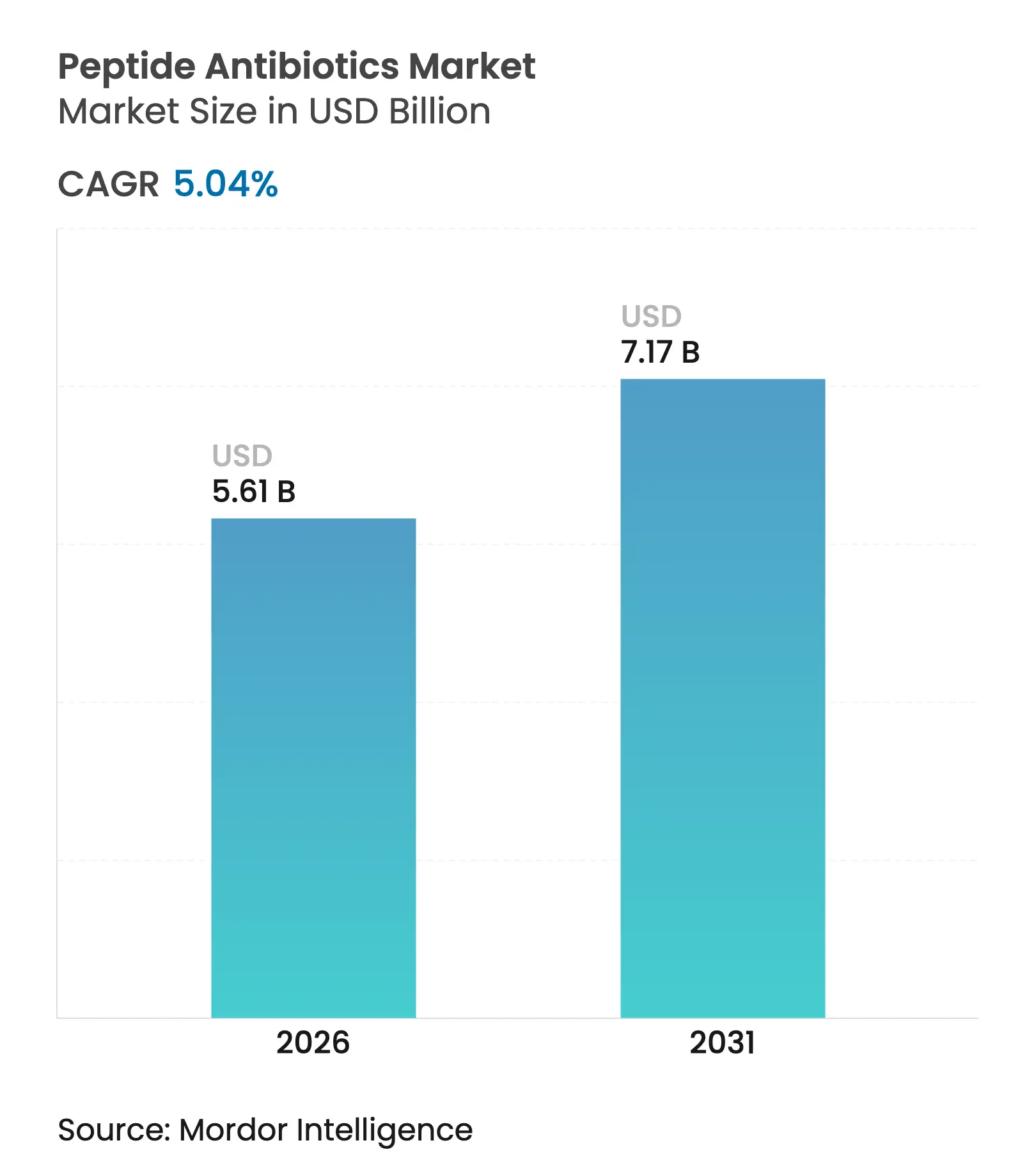

| Market Size (2026) | USD 5.61 Billion |

| Market Size (2031) | USD 7.17 Billion |

| Growth Rate (2026 - 2031) | 5.04 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Peptide Antibiotics Market Analysis by Mordor Intelligence

Peptide antibiotics market size in 2026 is estimated at USD 5.61 billion, growing from 2025 value of USD 5.34 billion with 2031 projections showing USD 7.17 billion, growing at 5.04% CAGR over 2026-2031. Rising multidrug resistance, an expanding discovery pipeline that now contains almost 900,000 AI-identified antimicrobial peptide sequences, is accelerating product innovation.[1]Sarah Dixon, “Artificial intelligence reveals 900,000 antimicrobial peptides,” nature.com Regulatory incentives such as the FDA’s Qualified Infectious Disease Product designation extend exclusivity windows and speed approvals, improving commercial viability. Meanwhile, heavy capital deployment exemplified by CordenPharma’s EUR 900 million (USD 1,043 million) manufacturing outlay and Merck’s USD 493 million oral-delivery licensing signals sustained confidence in the peptide antibiotics market. Topical hydrogel innovations and AI-guided RiPP discovery further enlarge the addressable opportunity base, even as premium pricing and production complexity temper near-term adoption.

Key Report Takeaways

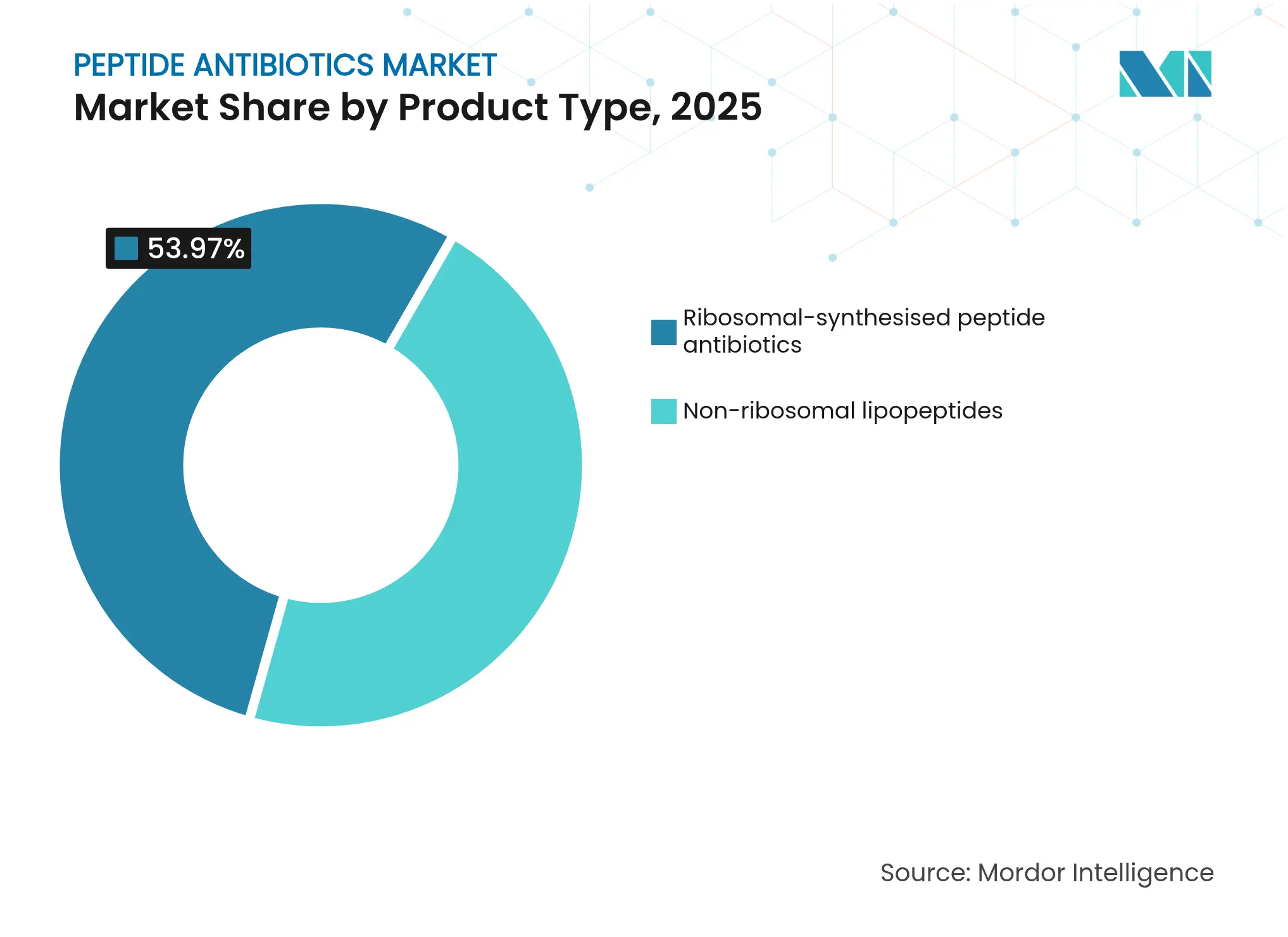

- By product type, non-ribosomal lipopeptides led with 46.03% revenue share in 2025, while ribosomal RiPPs are projected to expand at a 13.08% CAGR through 2031.

- By disease, skin infections accounted for 41.12% of the peptide antibiotics market size in 2025; hospital-acquired and ventilator-associated bacterial pneumonia are forecast to grow at a 10.05% CAGR to 2031.

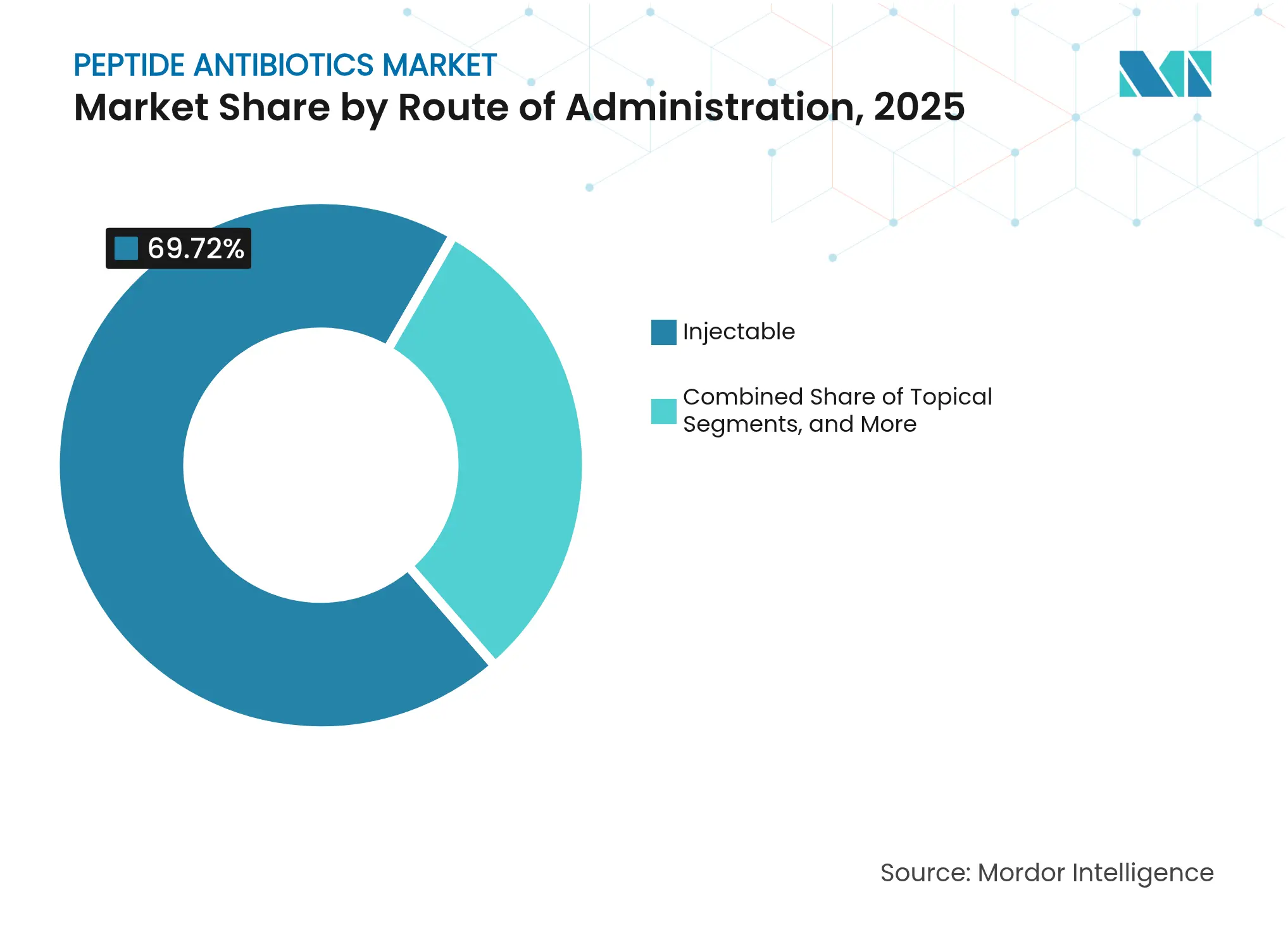

- By route of administration, injectable formulations held a 69.72% share in 2025, whereas topical hydrogels are advancing at a 12.29% CAGR through 2031.

- By distribution channel, hospital pharmacies controlled 56.94% of 2025 revenues, and online pharmacies are expected to post a 14.02% CAGR between 2026 and 2031.

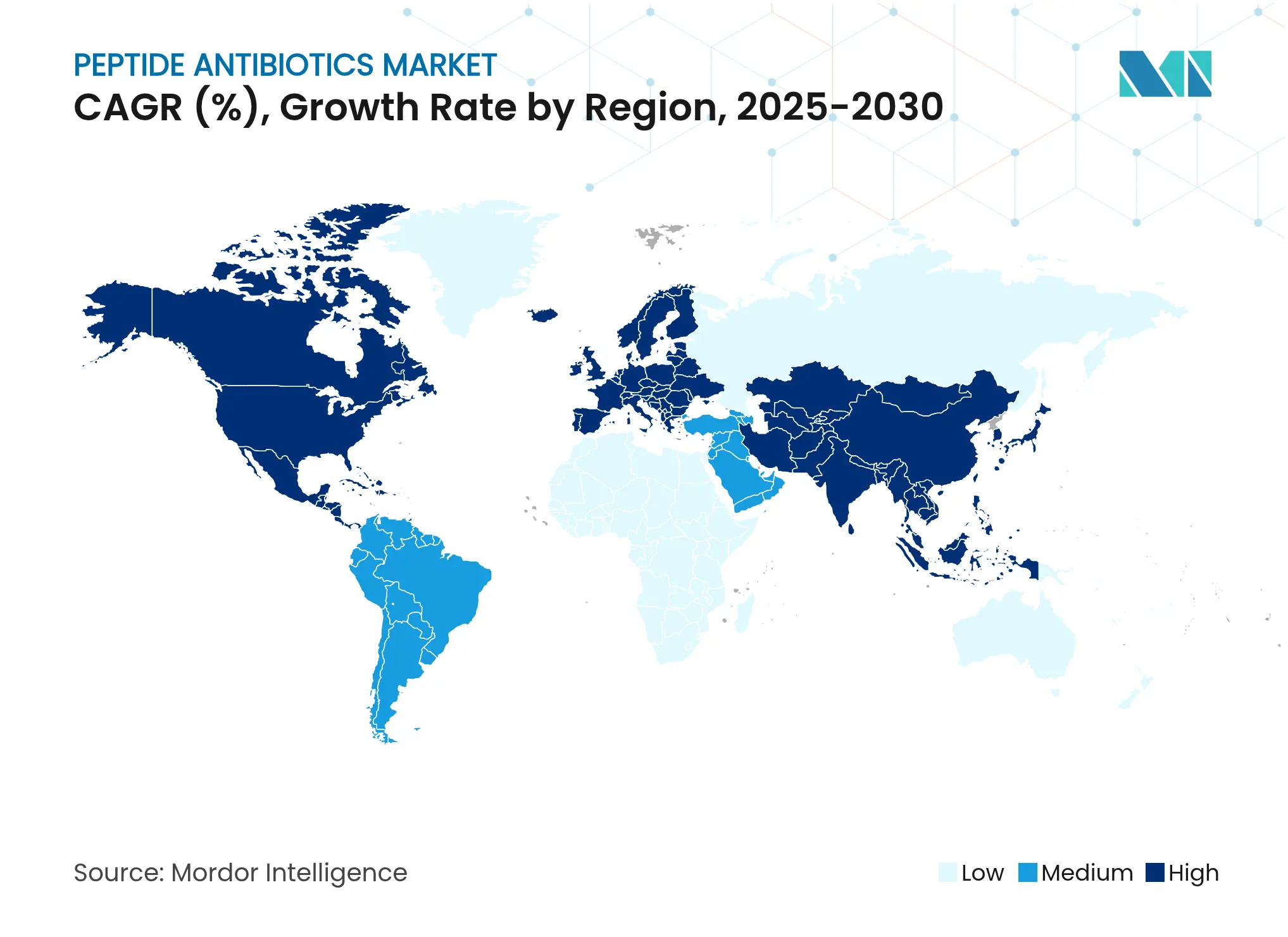

- By geography, North America captured 38.12% of global revenue in 2025; Asia Pacific is projected to register a 9.7% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peptide Antibiotics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Prevalence Of Multidrug-Resistant Bacterial Infections Rising Prevalence Of Multidrug-Resistant Bacterial Infections | +1.80% | Global, with highest impact in Asia Pacific and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.80% | Geographic Relevance:Global, with highest impact in Asia Pacific and North America | Impact Timeline:Medium term (2-4 years) |

Intensifying R&D Pipeline For Ribosomal & Non-Ribosomal Peptide Antibiotics Intensifying R&D Pipeline For Ribosomal & Non-Ribosomal Peptide Antibiotics | +1.20% | North America & EU, spill-over to APAC | Long term (≥ 4 years) | |||

Surging Demand For Last-Resort Antibiotics In Critical Care Settings Surging Demand For Last-Resort Antibiotics In Critical Care Settings | +1.00% | Global, with acute need in ICU environments worldwide | Short term (≤ 2 years) | |||

Favourable Regulatory Incentives (GAIN/QIDP, Orphan Status) Favourable Regulatory Incentives (GAIN/QIDP, Orphan Status) | +0.90% | Global, primarily US and EU markets | Short term (≤ 2 years) | |||

AI-Driven Genome-Mining Unlocking Novel RiPP Classes AI-Driven Genome-Mining Unlocking Novel RiPP Classes | +0.70% | Global, with early gains in US, UK, Singapore | Long term (≥ 4 years) | |||

Peptide-Hydrogel Delivery Platforms Expanding Topical & Implant Use-Cases Peptide-Hydrogel Delivery Platforms Expanding Topical & Implant Use-Cases | +0.60% | Global, with advanced adoption in North America and Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Multidrug-Resistant Bacterial Infections

Carbapenem-resistant Acinetobacter baumannii now shows resistance rates above 70% in several regions, making last-line options essential. Massatide A, a fifth-class lanthipeptide, inhibits linezolid- and methicillin-resistant Staphylococcus aureus at 0.25 µg/mL, surpassing many legacy drugs. The WHO 2024 priority pathogen update highlights peptide agents as uniquely capable of bypassing conventional resistance mechanisms.[2]World Health Organization, “Antimicrobial resistance fact sheet,” who.int In intensive-care units, Stenotrophomonas maltophilia isolation rose from 7% to 15% over two decades, with ceftazidime resistance reaching 72.5%. These epidemiological shifts keep the peptide antibiotics market under constant demand pressure.

Intensifying R&D Pipeline for Ribosomal & Non-Ribosomal Peptide Antibiotics

More than 1,172 biosynthetic gene clusters for aminovinyl-cysteine peptides have been catalogued, expanding the discovery funnel. Eli Lilly’s USD 100 million (USD 115 million) AMR Action Fund commitment, coupled with its OpenAI collaboration, shows large-cap pharma pivoting toward peptide solutions. Researchers recently mined 9,601 antimicrobial peptides in Lactobacillaceae genomes, demonstrating unprecedented breadth in ribosomal candidates.[3] Rubing Du, “Uncovering Encrypted Antimicrobial Peptides in Health-Associated Lactobacillaceae by Large-Scale Genomics and Machine Learning,” Microbiome, microbiomejournal.biomedcentral.com CARB-X backing for Peptilogics underlines public-private alignment on non-ribosomal innovation. The FDA’s 2024 approval of four peptide drugs validates regulator confidence.

Favourable Regulatory Incentives (GAIN/QIDP, Orphan Status)

The FDA’s QIDP pathway grants five-year exclusivity extensions and priority reviews, accelerating launches such as AbbVie’s Emblaveo, which achieved a 76.4% cure rate in trials. EMA equivalence has smoothed European entry, with Pfizer’s aztreonam-avibactam gaining a positive CHMP opinion. The recent approval of Blujepa, the first triazaacenaphthylene inhibitor, underscores regulators' openness to novel mechanisms. BARDA funding of USD 318 million further de-risks R&D spend for qualified assets. Collectively, these incentives sustain momentum in the peptide antibiotics market.

Peptide-Hydrogel Delivery Platforms Expanding Topical & Implant Use-Cases

Self-assembling hydrogels boost bactericidal activity 64-fold when combined with oxacillin against MRSA, widening topical therapy appeal. Nanogel conjugates with cell-penetrating peptides clear over 90% of uropathogens in vivo, a 36% improvement versus conventional regimens. Boronate-ester release hydrogels sustain activity for weeks, improving anti-tuberculosis outcomes. Dissolving microneedles now deliver antimicrobial peptides with greater patient compliance for skin infections.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Production Costs & Premium Pricing High Production Costs & Premium Pricing | -1.40% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.40% | Geographic Relevance:Global, with highest impact in price-sensitive markets | Impact Timeline:Short term (≤ 2 years) |

Limited Reimbursement And Pricing Incentives For Novel Antibiotics Limited Reimbursement And Pricing Incentives For Novel Antibiotics | -0.90% | Global, with acute impact in cost-constrained healthcare systems | Short term (≤ 2 years) | |||

Cytotoxicity & Stability Challenges In Systemic Applications Cytotoxicity & Stability Challenges In Systemic Applications | -0.80% | Global, particularly affecting IV formulations | Medium term (2-4 years) | |||

Stringent Regulatory Requirements For Demonstrating Superiority Over Existing Therapies Stringent Regulatory Requirements For Demonstrating Superiority Over Existing Therapies | -0.60% | Global, with highest burden in highly regulated markets (US, EU) | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Production Costs & Premium Pricing

Peptide synthesis requires specialized equipment, pushing production costs higher than small-molecule benchmarks. Sustainability audits show elevated process-mass intensity for complex lipopeptides, with limited CGMP capacity and purification bottlenecks. Cost-minimization studies comparing daptomycin to vancomycin highlight affordability constraints in resource-limited settings. Manufacturing setbacks, such as the FDA’s rejection of a Venatorx–Melinta BARDA-funded combination over production issues, show cost pressures can derail approvals.

Cytotoxicity & Stability Challenges in Systemic Applications

Proteolytic degradation and salt sensitivity reduce systemic peptide half-life, demanding frequent dosing or chemical modifications. Bacteria counter peptides through degradation enzymes and efflux pumps, though resistance evolution remains slower than with small molecules. Achieving therapeutic plasma levels while avoiding cytotoxicity is difficult, with protease degradation and formulation costs acting as twin hurdles. Structural tweaks such as cyclization improve stability but increase manufacturing complexity. As a result, only a fraction of discovered peptides progress to clinical stages.

Segment Analysis

By Product Type: Non-Ribosomal Dominance Meets Ribosomal Innovation

Non-ribosomal lipopeptides secured 46.03% of the peptide antibiotics market share in 2025, anchored by daptomycin and polymyxins that remain indispensable against resistant Gram-positive and Gram-negative infections. Daptomycin’s ability to evade BceAB-mediated resistance in Streptococcus pneumoniae sustains its frontline status. Polymyxin B and colistin regained importance as last-resort therapies for carbapenem-resistant organisms despite emerging MCR-gene resistance. Manufacturing advances, such as CordenPharma’s plant expansions, support supply stability for this mature segment.

Ribosomal RiPPs are projected to grow at a 13.08% CAGR, the highest among product classes. Synthetic-biology tooling has uncovered 987 new RiPP gene clusters in lichen fungi, opening fresh discovery space. Machine-learning guided evolution produced LBDA-D, which shows enhanced activity against Escherichia coli and S. aureus. Heterologous expression systems now enable scalable RiPP production, reducing historical supply constraints. As a result, the peptide antibiotics market size for ribosomal candidates is set for rapid expansion over the forecast period.

Note: Segment shares of all individual segments available upon report purchase

By Disease: Skin Infections Lead While HABP/VABP Accelerates

Skin infections accounted for 41.12% of the peptide antibiotics market size in 2025, supported by topical delivery formats that suit diabetic foot ulcers and post-surgical wounds. Locilex (pexiganan) illustrates focused development while dissolving microneedles to improve compliance in outpatient care. Long-acting lipoglycopeptides such as dalbavancin have broadened their reach beyond skin indications, reporting clinical success rates up to 100% in bloodstream infections. Growing diabetes prevalence and high rates of MRSA in community settings sustain demand for skin-directed therapeutics within the peptide antibiotics market.

Hospital-acquired and ventilator-associated bacterial pneumonia hold smaller baseline revenue but are slated for a 10.05% CAGR, the fastest among disease areas. AbbVie’s newly approved Emblaveo achieved a 76.4% cure rate in late-stage trials. Intensive-care infection rates remain high, with S. maltophilia doubling in incidence over two decades. The critical nature of respiratory infections ensures premium reimbursement and steady hospital uptake, and advanced inhalable or long-acting injectable peptides under development promise to deepen future penetration.

By Route of Administration: Injectable Dominance Challenged by Topical Innovation

Injectables maintained a 69.72% revenue share in 2025, underscoring the necessity for rapid systemic exposure in severe infections. Vancomycin achieved appropriate use in 89.1% of cardiac-surgery cases following IDSA protocols. Cold-chain infrastructure and trained infusion staff favour hospital settings, keeping the peptide antibiotics market anchored in inpatient care. However, high production costs and lengthy infusion times present cost-containment challenges for payers.

Topical hydrogels, rising at a 12.29% CAGR, employ self-assembling peptide networks that achieve minimum inhibitory concentrations as low as 2 µM against MRSA. Hydrogel microspheres now pack high drug loads with controlled release, solving earlier capacity issues. Patient preference for non-invasive therapy and the reduced risk of systemic toxicity fuel adoption. The peptide antibiotics market, therefore, shows growing modality diversification beyond traditional intravenous regimens.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Hospital Pharmacy Control Meets Online Growth

Hospital pharmacies controlled 56.94% of global sales in 2025 due to the acute nature of infections addressed and the sterility requirements of many formulations. Centralized compounding units and temperature-controlled storage preserve drug integrity, reinforcing hospital leadership. The prevalence of healthcare-associated infections, estimated to affect millions annually, keeps peptide antibiotic demand concentrated in inpatient care.

Online pharmacies, forecast at a 14.02% CAGR, benefit from telehealth expansion and the advancing feasibility of oral peptide delivery. Merck’s USD 493 million Cyprumed deal aims to transform peptides into tablets, a development that would expand outpatient channels. Retail pharmacies occupy a middle ground, dispensing oral agents and select topical products, but growth remains limited until more peptide antibiotics transition to community prescribing.

Geography Analysis

North America generated 38.12% of 2025 global revenue, the highest regional contribution. The FDA’s QIDP framework expedited approvals for cutting-edge agents such as Blujepa and Emblaveo, while BARDA committed USD 318 million in contracts to antimicrobial R&D. Private investments, including Eli Lilly’s USD 100 million AMR fund and CordenPharma’s plant expansion, reinforce supply and discovery capacity. Research hubs like McMaster University continue to pioneer AI-based discovery models, expanding the peptide antibiotics market footprint across North America.

Asia Pacific is the fastest-growing region with a projected 9.7% CAGR through 2031. AstraZeneca’s USD 2.5 billion Beijing R&D center enhances local peptide capabilities, while Chinese regulators approved Vibativ for serious infections, giving Cumberland Pharmaceuticals access to a vast market. Singapore’s institutes are advancing bacteriophage-peptide synergy programs, underscoring region-wide commitment to antimicrobial resistance. Government stewardship initiatives, coupled with capacity additions across India and South Korea, drive sustained uptake within the peptide antibiotics market.

Europe remains a pivotal contributor, supported by EMA streamlined pathways and manufacturing depth. Positive CHMP opinion for Pfizer’s aztreonam-avibactam highlights regulatory efficiency. Academic centres such as Chalmers University developed peptide hydrogels that boost oxacillin potency 64-fold, demonstrating innovation strength. Meanwhile, Middle East and Africa and South America show nascent adoption, aided by improving healthcare infrastructure and awareness campaigns focused on antimicrobial stewardship.. At the same time,the region's,,,the . At the same time,

Competitive Landscape

Market Concentration

The peptide antibiotics market features moderate concentration, with leading firms leveraging scale, AI partnerships, and manufacturing depth to secure advantage. Merck’s USD 493 million Cyprumed deal aims to overcome oral-delivery barriers that have long constrained peptide uptake.

Strategic alliances increasingly center on AI-driven discovery; Eli Lilly’s partnership with OpenAI exemplifies how generative models can compress hit-to-lead timelines. At the device interface, Amferia’s EUR 1.2 million (USD 1.3 million) investment positions its hydrogel dressings for rapid U.S. entry, achieving 64-fold potency improvements over standard care. White-space opportunities in long-acting injectables encourage players such as Melinta to invest in weekly-dosed lipoglycopeptides, extending hospital discharge options.

Emerging disruptors include Peptilogics, which secured CARB-X funding for fracture-infection therapeutics, and startups leveraging synthetic biology to create bespoke RiPPs. Competitive tactics also involve aggressively pursuing QIDP status to gain five additional years of exclusivity and access to priority FDA review queues. Overall, investment scale and regulatory expertise remain decisive factors shaping positioning within the peptide antibiotics market.

Peptide Antibiotics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GSK received FDA approval for Blujepa (gepotidacin), the first triazaacenaphthylene bacterial topoisomerase inhibitor for uncomplicated urinary tract infections.

- March 2025: AstraZeneca announced a USD 2.5 billion R&D center in Beijing with macro-cyclic peptide collaborations.

- February 2025: AbbVie obtained FDA clearance for Emblaveo (aztreonam-avibactam) to treat multidrug-resistant Gram-negative infections.

- February 2025: Cumberland Pharmaceuticals gained Chinese approval for Vibativ (telavancin) in pneumonia and severe skin infections.

Table of Contents for Peptide Antibiotics Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Multidrug-Resistant Bacterial Infections

- 4.2.2Intensifying R&D Pipeline For Ribosomal & Non-Ribosomal Peptide Antibiotics

- 4.2.3Favourable Regulatory Incentives (GAIN/QIDP, Orphan Status)

- 4.2.4AI-Driven Genome-Mining Unlocking Novel RiPP Classes

- 4.2.5Peptide-Hydrogel Delivery Platforms Expanding Topical & Implant Use-Cases

- 4.2.6Surging Demand For Last-Resort Antibiotics In Critical Care Settings

- 4.3Market Restraints

- 4.3.1High Production Costs & Premium Pricing

- 4.3.2Cytotoxicity & Stability Challenges In Systemic Applications

- 4.3.3Limited Reimbursement And Pricing Incentives For Novel Antibiotics

- 4.3.4Stringent Regulatory Requirements For Demonstrating Superiority Over Existing Therapies

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Ribosomal-synthesised peptide antibiotics

- 5.1.2Non-ribosomal-synthesised peptide antibiotics

- 5.2By Disease

- 5.2.1Skin infection

- 5.2.2HABP / VABP

- 5.2.3Blood-stream infection

- 5.2.4Other infections

- 5.3By Route of Administration

- 5.3.1Injectable

- 5.3.2Topical

- 5.3.3Others

- 5.4By Distribution Channel

- 5.4.1Hospital pharmacies

- 5.4.2Retail pharmacies

- 5.4.3Online pharmacies

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes global overview, market-level overview, core segments, financials as available, strategic information, market rank/share, products & services, recent developments)

- 6.3.1Merck & Co.

- 6.3.2GSK plc

- 6.3.3Melinta Therapeutics

- 6.3.4AbbVie

- 6.3.5Xellia Pharmaceuticals

- 6.3.6Sandoz AG

- 6.3.7Cumberland Pharmaceuticals

- 6.3.8Pfizer Inc.

- 6.3.9Eli Lilly & Co.

- 6.3.10Amferia AB

- 6.3.11AstraZeneca plc

- 6.3.12CordenPharma International

- 6.3.13Thermo Fisher Scientific

- 6.3.14Teva Pharmaceuticals

- 6.3.15Zhejiang Hisun Pharma

- 6.3.16Lupin Ltd

- 6.3.17Glenmark Pharmaceuticals

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product Type

- Ribosomal-synthesised peptide antibiotics

- Non-ribosomal-synthesised peptide antibiotics

- Ribosomal-synthesised peptide antibiotics

- By Disease

- Skin infection

- HABP / VABP

- Blood-stream infection

- Other infections

- Skin infection

- By Route of Administration

- Injectable

- Topical

- Others

- Injectable

- By Distribution Channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

- Hospital pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Peptide Antibiotics Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 5.34 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 4.97 B (2024) | Global Consultancy A | Excludes topical formulations and relies on hospital purchase price only | ||

USD 5.20 B (2024) | Regional Consultancy B | Adds veterinary and food-grade volumes and freezes ASP for ten years |