United States Antibiotic Resistance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

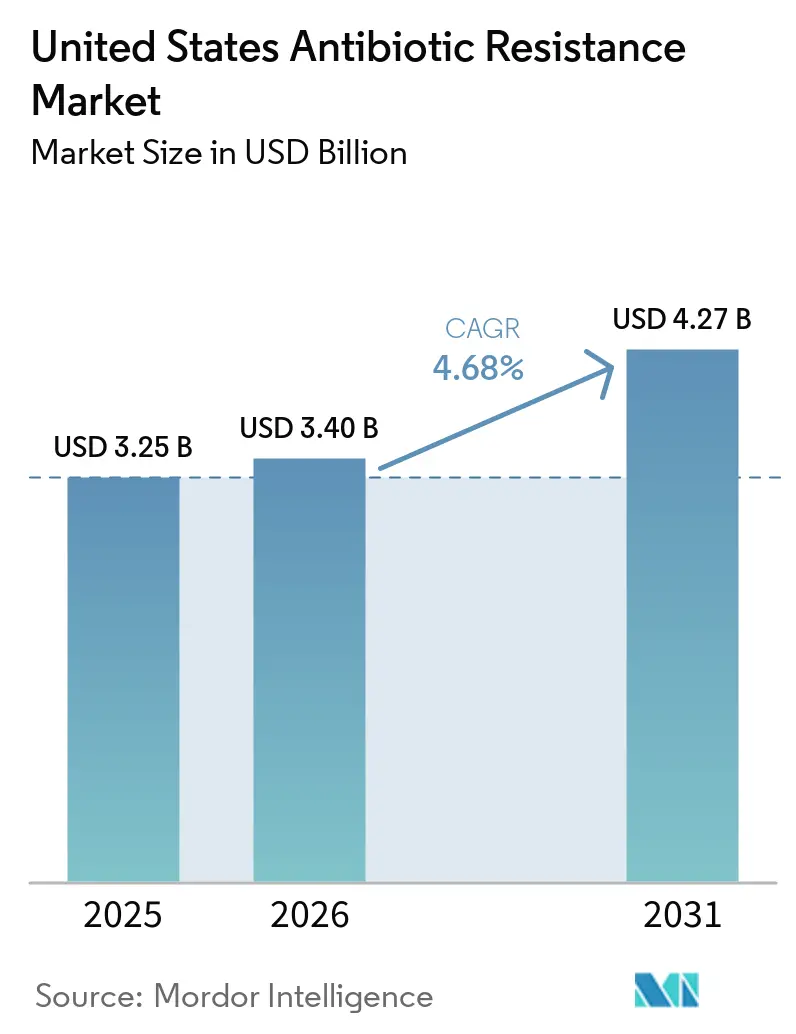

| Base Year Market Size (2025) | USD 3.25 Billion |

| Market Size (2026) | USD 3.40 Billion |

| Market Size (2031) | USD 4.27 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

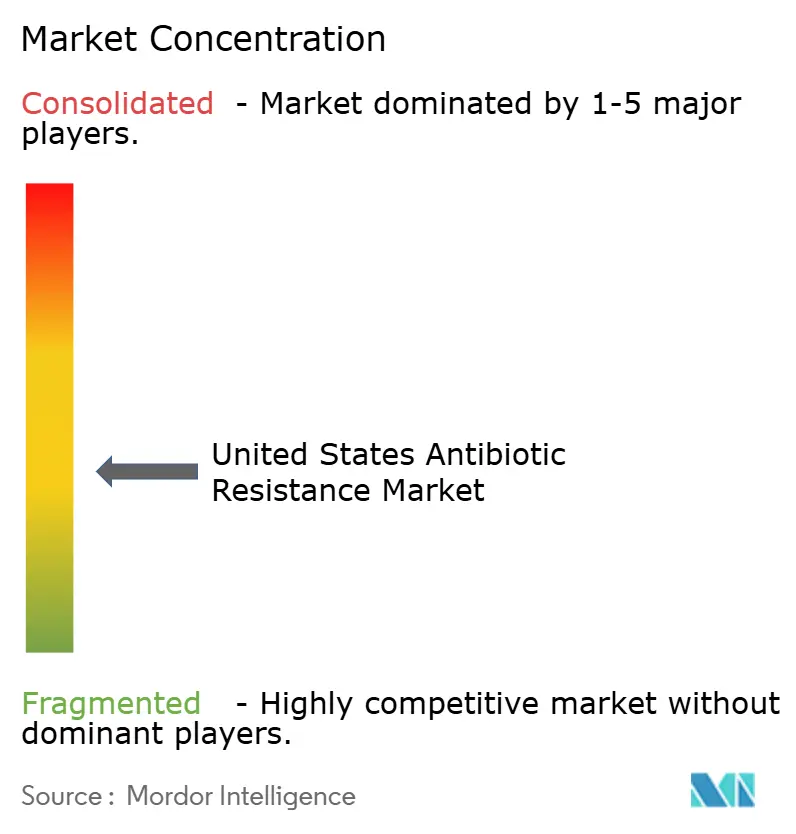

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Antibiotic Resistance Market Analysis by Mordor Intelligence

The United States Antibiotic Resistance Market size is expected to grow from USD 3.25 billion in 2025 to USD 3.40 billion in 2026 and is forecast to reach USD 4.27 billion by 2031 at 4.68% CAGR over 2026-2031.

Growth in the market is being supported by the persistent burden of antimicrobial-resistant infections across hospitals and other care settings, with the CDC estimating at least 2.8 million resistant infections and more than 35,000 associated deaths each year in the country. A CDC fact sheet released in July 2024 showed a 20% collective increase in 6 antimicrobial-resistant hospital-onset infections during the pandemic versus pre-pandemic levels, and rates for all but MRSA remained above earlier baselines as of 2022, which points to durable demand rather than a temporary spike. Federal action is also changing the revenue profile of the United States antibiotic resistance market, as BARDA awarded Shionogi an initial USD 119 million commitment in April 2026, with total options up to USD 482 million, to establish domestic cefiderocol manufacturing under Project BioShield. At the same time, mandatory CMS-linked AUR reporting has improved prescribing visibility since January 2024, and the 2025 split into separate AU and AR measures is sharpening stewardship decisions around when newer agents are used. The United States antibiotic resistance market still faces a narrow innovation base, with HHS ASPE noting only 4 systemic antibacterial NMEs approved from 2020 through October 2024, while the PASTEUR Act remains unpassed and leaves the reimbursement gap unresolved for many higher-cost novel antibiotics.

Key Report Takeaways

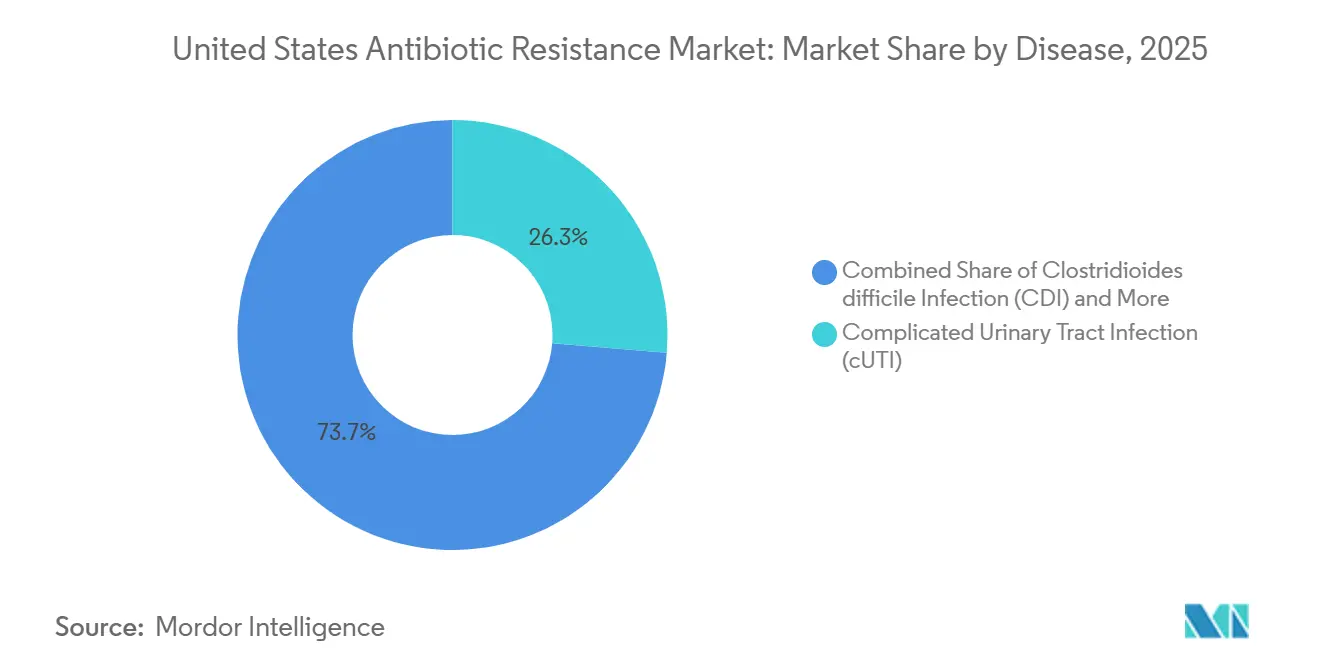

- By disease, complicated urinary tract infection held 26.31% of the United States antibiotic resistance market share in 2025, while Clostridioides difficile infection is projected to expand at 5.38% CAGR through 2031.

- By pathogen, Staphylococcus aureus accounted for 23.24% of the United States antibiotic resistance market size in 2025, while Pseudomonas aeruginosa is forecast to grow at 6.52% CAGR through 2031.

- By drug class, beta-lactam and beta-lactamase inhibitor combinations represented 31.52% of the United States antibiotic resistance market size in 2025, while combination therapies are expected to advance at 8.25% CAGR through 2031.

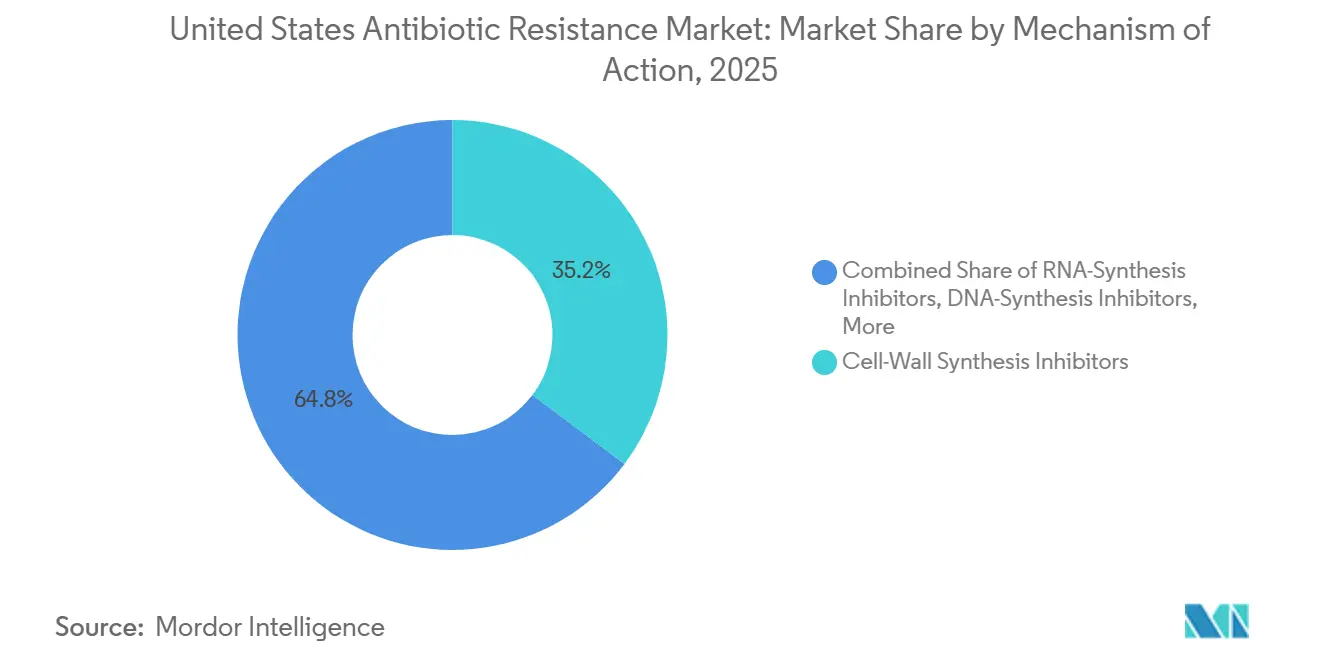

- By mechanism of action, cell-wall synthesis inhibitors captured 35.24% of market value in 2025, while NA-synthesis inhibitors are expected to record the highest CAGR at 8.83% through 2031.

- By distribution channel, hospital pharmacies held 58.44% share in 2025, while online pharmacies are projected to grow at 8.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Antibiotic Resistance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Burden Of Drug-Resistant Infections | +1.6% | National, with acute intensity in Northeast, Southeast, and urban West Coast ICU networks | Short term (≤ 2 years) |

| Federal AMR Funding And Stockpiling Support | +0.9% | National, with manufacturing benefits anchored near BARDA-partnered facility sites | Medium term (2-4 years) |

| QIDP, Fast Track, And LPAD-Enabled Approvals | +0.8% | National | Medium term (2-4 years) |

| Stewardship And AUR Reporting Sharpening Targeted Use | +0.5% | National, with early gains in Colorado, South Carolina, and Nebraska | Short term (≤ 2 years) |

| New Oral Step-Down Options For Hard-To-Treat UTIs | +0.6% | National, with stronger effect in community and outpatient settings | Medium term (2-4 years) |

| Microbiome-Sparing CDI Innovation | +0.6% | National, concentrated in gastroenterology and infectious disease referral centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Burden of Drug-Resistant Infections Drives Persistent Clinical Demand

Resistance severity in United States hospitals has not returned to pre-pandemic baselines, and that keeps clinical demand firm in the United States antibiotic resistance market. CDC surveillance published in June 2026 found that the share of carbapenemase-producing CRE harboring blaNDM genes rose from 5.4% in 2016 to 39.8% in 2023. This shift matters because NDM-positive strains weaken the effectiveness of many beta-lactam and beta-lactamase inhibitor combinations that were central to earlier treatment strategies. It expands the need for agents with metallo-beta-lactamase activity, including cefiderocol and aztreonam-avibactam, and supports premium use in high-acuity cases[1]AbbVie Inc., “U.S. FDA Approves EMBLAVEO for the Treatment of Adults With Complicated Intra-Abdominal Infections With Limited or No Treatment Options,” AbbVie Press Release, abbvie.com. The United States antibiotic resistance market is therefore being driven by a harder-to-treat resistance profile rather than by a temporary wave of infections.

Federal AMR Funding and Stockpiling Support Stabilizes Commercial Returns

BARDA is moving from a pure R&D supporter toward an active procurement partner, and that is changing the return profile in the United States antibiotic resistance market. In September 2024, Basilea entered an OTA agreement with BARDA that provided potential total non-dilutive funding of up to USD 268 million over up to 12 years, with USD 29 million committed at signing. Qpex Biopharma also received cumulative BARDA awards totaling USD 92 million for xeruborbactam-based combination products, with options that could take the total to USD 132 million. These commitments matter because public procurement is flowing toward gram-negative programs in HABP, VABP, bloodstream infection, and related hospital indications where routine reimbursement remains weak. Federal demand is therefore acting as a stabilizer for pipeline investment that normal hospital purchasing would not reliably support in the United States antibiotic resistance market.

QIDP, Fast Track, and LPAD-Enabled Approvals Compressing Time-to-Market

Regulatory pathways under the GAIN Act are improving launch visibility in the United States antibiotic resistance market by shortening development timelines and extending exclusivity for eligible products. AbbVie’s EMBLAVEO received FDA approval on February 7, 2025, after earlier QIDP and Fast Track designations, and became the first fixed-dose intravenous monobactam and beta-lactamase inhibitor combination for adults with complicated intra-abdominal infections who have limited or no treatment options. EXBLIFEP was approved in February 2024 for complicated urinary tract infection and benefited from the QIDP exclusivity framework. HHS ASPE reported that 3 products had already been approved under the LPAD pathway as of February 2024, which shows that narrow-population approvals are becoming more practical for developers targeting resistant infections. The approval pattern from 2023 through 2025 was therefore stronger than the zero-NME stretch seen during 2020 through 2022, and that supports a steadier near-term output of launch candidates.

Microbiome-Sparing CDI Innovation Resets Recurrence Economics

Clostridioides difficile therapy is opening a different growth path for the United States antibiotic resistance market because treatment value is moving from short-term control toward recurrence prevention. Ibezapolstat showed a 96% clinical cure rate with 0% recurrence in Phase 2b, and Acurx linked that profile to selective sparing of beneficial gut microbiome families. Acurx reached End-of-Phase 2 agreement with the FDA in May 2024 and moved the program toward Phase 3 readiness, which reduced execution uncertainty around this mechanism. Nature Communications also published 2025 data showing that the experimental glycopeptide EVG7 protected against recurrent CDI by sparing Lachnospiraceae family members, which supports the broader microbiome-preserving approach. That makes CDI the clearest area where the United States antibiotic resistance market is shifting toward mechanistic differentiation instead of incremental improvement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak Hospital Economics Under DRG-Style Reimbursement | -0.5% | National, most acute in community and safety-net hospitals with thin operating margins | Short term (≤ 2 years) |

| High Evidentiary Burden For Safety And Superiority | -0.2% | National | Medium term (2-4 years) |

| Offshore API And Fermentation Concentration Risk | -0.1% | National, amplified in states with large hospital systems dependent on generic IV antibiotics | Medium term (2-4 years) |

| Post-Approval Resistance Surveillance And Narrow Labels | -0.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Hospital Economics Under DRG-Style Reimbursement Compress Adoption

Hospital adoption remains a core brake on the United States antibiotic resistance market because Medicare inpatient payment is still tied to fixed DRG reimbursement rather than to the specific antibiotic selected. That structure can leave hospitals choosing between a novel course priced at USD 10,000 to USD 50,000 and a generic option that costs far less, even when resistance profiles support the newer product. The fiscal year 2026 IPPS rule kept the underlying framework in place, and NTAP windows still expire after a limited period for recently approved antibiotics[2]Centers for Medicare & Medicaid Services, “Medicare Program, Hospital Inpatient Prospective Payment Systems for Acute Care Hospitals, FY 2026 Rates,” Federal Register, regulations.justia.com. Developers have therefore faced a heavier burden in formulary negotiations because hospitals often ask for budget-impact evidence before listing a new agent. Until a subscription-style model is enacted, reimbursement will remain the main unresolved commercial risk in the United States antibiotic resistance market.

High Evidentiary Burden for Safety and Superiority Prolongs Development Timelines

The United States antibiotic resistance market also faces a slower development cycle because regulators still require demanding evidence packages for safety, manufacturing, and clinical validity. The February 2024 complete response letter for cefepime-taniborbactam showed that chemistry, manufacturing, and controls issues can delay promising agents even when clinical efficacy is not the main concern. This burden is especially hard for LPAD-style programs because difficult-to-treat infections occur in smaller and more concentrated patient pools, which makes enrollment and trial execution harder. Combination regimens and phage-based therapies face an added challenge because regulatory precedent remains less mature for both trial design and evidence interpretation. The available exclusivity incentives improve economics after approval, but they do not materially reduce the pre-approval work needed to bring a new product into the United States antibiotic resistance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: cUTI Anchors Revenue While CDI Resets Recurrence Therapy Economics

Complicated urinary tract infection accounted for 26.31% of market value in 2025, making it the largest disease segment in the United States antibiotic resistance market. This position reflects the large burden of ESBL-producing Enterobacterales and carbapenem-resistant uropathogens in both inpatient and outpatient care. The 2025 IDSA guideline update on complicated urinary tract infections endorsed resistance-profile-based antibiotic selection, which supports the clinical role of newer agents over older empiric options[3]Infectious Diseases Society of America, “2025 Guideline Update on Complicated Urinary Tract Infections,” IDSA, idsociety.org. A Phase 3 trial published in 2026 also showed non-inferiority for cefepime-nacubactam and aztreonam-nacubactam versus imipenem-cilastatin in cUTI, including infections caused by resistant gram-negative strains.

Clostridioides difficile infection is projected to grow at 5.38% CAGR through 2031, which makes it the fastest-growing disease segment in the United States antibiotic resistance market. Growth is being supported by recurrent disease burden and by the commercial emergence of live biotherapeutics and microbiome-sparing antibiotics that aim to break the recurrence cycle. Complicated intra-abdominal infection gained a new option when EMBLAVEO was approved in February 2025 for adults with limited or no treatment options, which improved coverage for metallo-beta-lactamase-linked resistance patterns. ABSSSI and CABP also benefited from ZEVTERA’s U.S. commercial availability in May 2025, while HABP, VABP, and bloodstream infection remain the most commercially difficult areas because reimbursement support still lags clinical need.

By Pathogen: MRSA Volume Leadership Masks an Accelerating Gram-Negative Threat

Staphylococcus aureus, led mainly by MRSA, represented 23.24% of the United States antibiotic resistance market size in 2025, which kept it as the largest pathogen segment. Its lead came from large absolute patient volumes and from the depth of approved therapies already available for gram-positive care pathways. JAMA Network Open reported that MRSA accounted for the majority of total antimicrobial-resistant infections estimated in U.S. hospitals, which helps explain why it still anchors current demand. Even so, historical volume leadership is no longer the full story because resistance growth is shifting toward more difficult gram-negative threats.

Pseudomonas aeruginosa is projected to expand at 6.52% CAGR through 2031, making it the fastest-growing pathogen category in the United States antibiotic resistance market. The 2024 IDSA guidance added specific attention to differential susceptibility across newer beta-lactam agents for difficult-to-treat resistant P. aeruginosa, which shows how quickly prescribing complexity is increasing. Klebsiella pneumoniae and Escherichia coli remain major sources of demand inside cUTI and bloodstream infection, and their commercial importance rises further as metallo-beta-lactamase patterns spread.

By Drug Class: BL/BLI Combinations Anchor Revenue While Combination Therapies Gain Share

Beta-lactam and beta-lactamase inhibitor combinations captured 31.52% of market value in 2025, which made them the leading drug class in the United States antibiotic resistance industry. Their position reflects the continued reliance on ceftazidime-avibactam, meropenem-vaborbactam, imipenem-cilastatin-relebactam, and newer combinations such as aztreonam-avibactam for resistant gram-negative care. This class remains central because it covers several high-value hospital indications where beta-lactam backbones still guide first-line treatment decisions. The commercial base is also strengthened by the fact that these agents are already embedded in resistance-focused stewardship protocols and hospital pathways.

Combination therapies are forecast to grow at 8.25% CAGR through 2031, which reflects rising clinician preference for dual approaches when single-agent susceptibility is uncertain or absent. This trend is strongest in difficult-to-treat gram-negative infections, where evidence-based combination use is increasingly supported by updated guidance. At the same time, the February 2024 complete response letter for cefepime-taniborbactam showed that fixed-dose combinations also carry manufacturing execution risk alongside clinical risk. Outside this leading class, tetracyclines such as omadacycline retain relevance in CABP and ABSSSI, while cephalosporins gained fresh momentum with ZEVTERA and domestic supply strategy improved when Paratek completed full U.S. onshoring of NUZYRA API manufacturing in November 2024.

By Mechanism of Action: Cell-Wall Agents Lead While RNA-Synthesis Inhibitors Accelerate Fastest

Cell-wall synthesis inhibitors held 35.24% of market value in 2025, which gave them the largest mechanism share in the United States antibiotic resistance market. This group includes beta-lactams, carbapenems, lipoglycopeptides, and the BL and BLI combinations that remain standard across cUTI, HABP, VABP, bloodstream infection, and several other resistant indications. Their share is likely to remain stable because these agents address the widest range of high-acuity infections seen in hospital settings. The category also benefits from long-standing clinician familiarity, which supports prescribing continuity even as resistance patterns evolve.

RNA-synthesis inhibitors are projected to grow at 8.83% CAGR through 2031, which makes them the fastest-growing mechanism group. That growth comes mainly from fidaxomicin-class use in CDI, where selective gut activity and microbiome preservation are becoming stronger treatment differentiators. DNA-synthesis inhibitors also gained visibility in 2025 when GSK’s Blujepa, which contains gepotidacin, was approved by the FDA for uncomplicated urinary tract infections in female adults and adolescents. Protein-synthesis inhibitors still retain important roles in CABP, ABSSSI, and gram-positive bloodstream infections, but resistance-profile-matched prescribing is steadily tightening the link between susceptibility testing and selection of differentiated mechanisms.

By Distribution Channel: Hospital Pharmacies Dominate as Oral Therapies Drive Online Channel Growth

Hospital pharmacies accounted for 58.44% of distribution value in 2025, which kept them as the dominant channel in the United States antibiotic resistance industry. This lead reflects the fact that many resistant infections still require inpatient diagnosis, intravenous therapy, microbiology support, and close clinical monitoring. The channel also benefits from stewardship oversight, because novel antibiotic use is often tied to documented resistance or specialist review. As a result, hospital settings continue to capture the highest-value treatment courses even as outpatient options begin to expand.

Online pharmacies are projected to grow at 8.53% CAGR through 2031 as oral step-down therapy becomes more practical for selected resistant infections. That trend is linked to broader clinical acceptance of oral follow-on treatment, especially in cUTI and CDI pathways where inpatient initiation can be followed by outpatient completion. GSK reported positive Phase 3 PIVOT-PO data for tebipenem HBr in October 2025, and that result supported the long-term shift toward oral treatment options for infections that were once managed almost entirely with intravenous therapy. Retail pharmacies remain relevant for CABP, ABSSSI, and oral completion regimens, but the faster growth rate is moving toward digital and mail-enabled dispensing models as the oral pipeline broadens.

Geography Analysis

The United States antibiotic resistance market functions as one national market, but its demand profile changes meaningfully across regions because resistance intensity, hospital complexity, and reimbursement exposure are not evenly distributed. Northeastern metropolitan systems and urban West Coast ICU networks show some of the highest concentrations of carbapenem-resistant gram-negative pathogens, which makes them early demand centers for premium therapies. New York City illustrates this pattern clearly, as annual NDM-CRE cases rose from 58 in 2019 to 388 in 2024 and pushed more attention toward agents active against metallo-beta-lactamase producers. These tertiary centers also tend to adopt BARDA-supported and LPAD-linked products earlier because they have the infectious disease staffing, microbiology support, and patient acuity needed to justify newer antibiotics.

The Southern United States represents a different operating environment for the United States antibiotic resistance market because long-term acute care hospitals and community hospitals carry high resistant infection burdens but face tighter reimbursement pressure. HABP and VABP are especially important in these settings because ventilated and medically complex patients account for a large share of severe resistant infections. However, DRG-based Medicare payment and managed Medicaid pressure make formulary adoption harder in facilities with thinner margins, even when clinical demand is present. NTAP offers some relief, but its limited duration and cost coverage do not fully close the gap for premium antibiotics after the first years of launch. This leaves the South with a larger gap between clinical need and realized commercial uptake than many higher-income coastal systems.

The Midwest and Mountain West show a more gradual but important shift in the United States antibiotic resistance market because stewardship infrastructure is improving and AUR reporting participation is rising. Nebraska hospitals increased AU module reporting participation from 14% in 2022 to 61% in 2024, which signals stronger surveillance discipline and more structured antibiotic use oversight. As reporting depth improves, these regions are better positioned to move away from broad empiric prescribing and toward narrower resistance-tested use of newer agents. That transition should support targeted uptake over time, even if near-term revenue remains lower than in the highest-acuity urban referral centers.

Competitive Landscape

The United States antibiotic resistance market is fragmented at the developer level and moderately concentrated at the commercial level. Large diversified companies such as Pfizer and Merck still hold meaningful positions through established products and distribution reach, but many recent launch candidates and newer approvals have come from small and mid-sized specialty developers. HHS ASPE noted that only 4 systemic antibacterial NMEs were approved between 2020 and October 2024, which confirms how thin the current innovation base remains even as demand stays firm. That scarcity creates both risk and opportunity because fewer active developers means supply vulnerability, while the remaining companies face less direct launch competition in several resistant indications.

Strategic moves now center on scale, procurement alignment, and domestic supply security. CorMedix completed the acquisition of Melinta Therapeutics in September 2025, adding a portfolio of 7 marketed products that had generated USD 120 million in 2024 revenue and showing that cash-flow-positive antibiotic assets are becoming targets for consolidation. Shionogi’s April 2026 BARDA Project BioShield award for cefiderocol, with options up to USD 482 million, went further by showing that stockpiling contracts can serve as an investable commercial model for companies willing to build U.S.-based production. Paratek’s completion of full U.S. onshoring for NUZYRA API manufacturing in November 2024 added another competitive signal because supply resilience is becoming part of the value proposition in hospital procurement. These moves suggest that competitive strength is now shaped as much by funding structure and manufacturing footprint as by clinical differentiation alone.

White-space opportunities remain strongest in severe gram-negative infections and in recurrence-focused CDI care. Agents with confirmed activity against NDM- and OXA-48-producing Enterobacterales in bloodstream infection and HABP or VABP still face limited direct competition, which leaves room for specialists with validated MBL coverage. In CDI, Acurx is moving ibezapolstat toward later-stage development while Nestlé Health Science took over global rights to VOWST, which shows how recurrence prevention is becoming a defined competitive lane rather than a side niche. Non-conventional modalities still look fragile by comparison, as BiomX discontinued its Phase 2b BX004 phage trial in December 2025 after internal review, which underlined the execution risk still attached to alternative platforms. Competitive positioning in the United States antibiotic resistance market will therefore continue to favor companies that can pair clear resistance relevance with funding support, manageable trial design, and credible manufacturing plans.

United States Antibiotic Resistance Industry Leaders

Pfizer Inc.

Merck & Co., Inc.

AbbVie Inc.

Melinta Therapeutics LLC

Shionogi & Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Shionogi Inc. was awarded a contract through BARDA's Project BioShield for Fetroja (cefiderocol) as a critical countermeasure against drug-resistant gram-negative infections and biothreat pathogens, with initial funding of USD 119 million and total options up to USD 482 million. The contract commits Shionogi to establishing a US-based cefiderocol manufacturing facility, representing the largest single BARDA commitment to a gram-negative antibiotic to date.

- March 2026: Acurx Pharmaceuticals announced the initiation of a clinical trial program for ibezapolstat in patients with multiply-recurrent CDI, positioning it as the first potential single agent to treat acute CDI and simultaneously prevent recurrence, after achieving a 96% clinical cure rate with 0% recurrence in Phase 2b.

United States Antibiotic Resistance Market Report Scope

As per the scope of the report, the antibiotic resistance market refers to the industry segment focused on the development, production, and commercialization of products aimed at combating antibiotic resistance.

The segmentation for the United States antibiotic resistance market is categorized by disease, pathogen, drug class, mechanism of action, and distribution channel. By disease, the market includes clostridioides difficile infection (CDI), complicated intra-abdominal infection (cIAI), acute bacterial skin and skin-structure infections (ABSSSI), hospital- and ventilator-acquired bacterial pneumonia (HABP/VABP), complicated urinary tract infection (cUTI), community-acquired bacterial pneumonia (CABP), and bloodstream infection (BSI). By pathogen, it covers acinetobacter baumannii, staphylococcus aureus, pseudomonas aeruginosa, escherichia coli, klebsiella pneumoniae, enterococcus faecium/VRE, and other priority pathogens. By drug class, the segmentation includes beta-lactam/beta-lactamase inhibitor combinations, oxazolidinones, tetracyclines, cephalosporins, lipoglycopeptides, combination therapies, and other classes. By mechanism of action, the market is divided into cell-wall synthesis inhibitors, protein-synthesis inhibitors, DNA-synthesis inhibitors, RNA-synthesis inhibitors, and other mechanisms. By distribution channel, it includes hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. For each segment, the market size and forecast are provided in terms of value (USD).

| Clostridioides difficile Infection (CDI) |

| Complicated Intra-Abdominal Infection (cIAI) |

| Acute Bacterial Skin and Skin-Structure Infections (ABSSSI) |

| Hospital- and Ventilator-Acquired Bacterial Pneumonia (HABP/VABP) |

| Complicated Urinary Tract Infection (cUTI) |

| Community-Acquired Bacterial Pneumonia (CABP) |

| Bloodstream Infection (BSI) |

| Acinetobacter baumannii |

| Staphylococcus aureus |

| Pseudomonas aeruginosa |

| Escherichia coli |

| Klebsiella pneumoniae |

| Enterococcus faecium / VRE |

| Other Priority Pathogens |

| Beta-lactam / Beta-lactamase Inhibitor Combinations |

| Oxazolidinones |

| Tetracyclines |

| Cephalosporins |

| Lipoglycopeptides |

| Combination Therapies |

| Other Classes |

| Cell-Wall Synthesis Inhibitors |

| Protein-Synthesis Inhibitors |

| DNA-Synthesis Inhibitors |

| RNA-Synthesis Inhibitors |

| Other Mechanisms |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| By Disease | Clostridioides difficile Infection (CDI) |

| Complicated Intra-Abdominal Infection (cIAI) | |

| Acute Bacterial Skin and Skin-Structure Infections (ABSSSI) | |

| Hospital- and Ventilator-Acquired Bacterial Pneumonia (HABP/VABP) | |

| Complicated Urinary Tract Infection (cUTI) | |

| Community-Acquired Bacterial Pneumonia (CABP) | |

| Bloodstream Infection (BSI) | |

| By Pathogen | Acinetobacter baumannii |

| Staphylococcus aureus | |

| Pseudomonas aeruginosa | |

| Escherichia coli | |

| Klebsiella pneumoniae | |

| Enterococcus faecium / VRE | |

| Other Priority Pathogens | |

| By Drug Class | Beta-lactam / Beta-lactamase Inhibitor Combinations |

| Oxazolidinones | |

| Tetracyclines | |

| Cephalosporins | |

| Lipoglycopeptides | |

| Combination Therapies | |

| Other Classes | |

| By Mechanism of Action | Cell-Wall Synthesis Inhibitors |

| Protein-Synthesis Inhibitors | |

| DNA-Synthesis Inhibitors | |

| RNA-Synthesis Inhibitors | |

| Other Mechanisms | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is driving growth in the United States antibiotic resistance market?

Growth is supported by a rise from USD 3.40 billion in 2026 to USD 4.27 billion by 2031 at 4.68% CAGR, along with persistent resistant infections, federal stockpiling activity, and tighter AUR-linked stewardship.

Which disease area contributes the most revenue?

Complicated urinary tract infection leads with 26.31% of 2025 value, supported by ESBL and carbapenem-resistant uropathogen burden and a growing set of approved therapies.

Which pathogen is growing the fastest in the United States?

Pseudomonas aeruginosa is the fastest-growing pathogen segment at 6.52% CAGR through 2031 as difficult-to-treat resistant strains and MBL-linked profiles become more important.

Why do newer antibiotics still face slow hospital uptake?

DRG-based inpatient reimbursement still fixes hospital payment regardless of antibiotic choice, so many providers remain cautious when novel agents carry much higher acquisition costs.

Which distribution channel dominates current sales?

Hospital pharmacies lead with 58.44% of 2025 distribution value because many resistant infections still require inpatient diagnosis, intravenous treatment, and stewardship review.

Where are the strongest competitive opportunities emerging?

The clearest openings are in severe gram-negative infections linked to NDM and OXA-48 resistance, and in CDI recurrence prevention where microbiome-sparing approaches are gaining traction.

Page last updated on: