Antibacterial Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

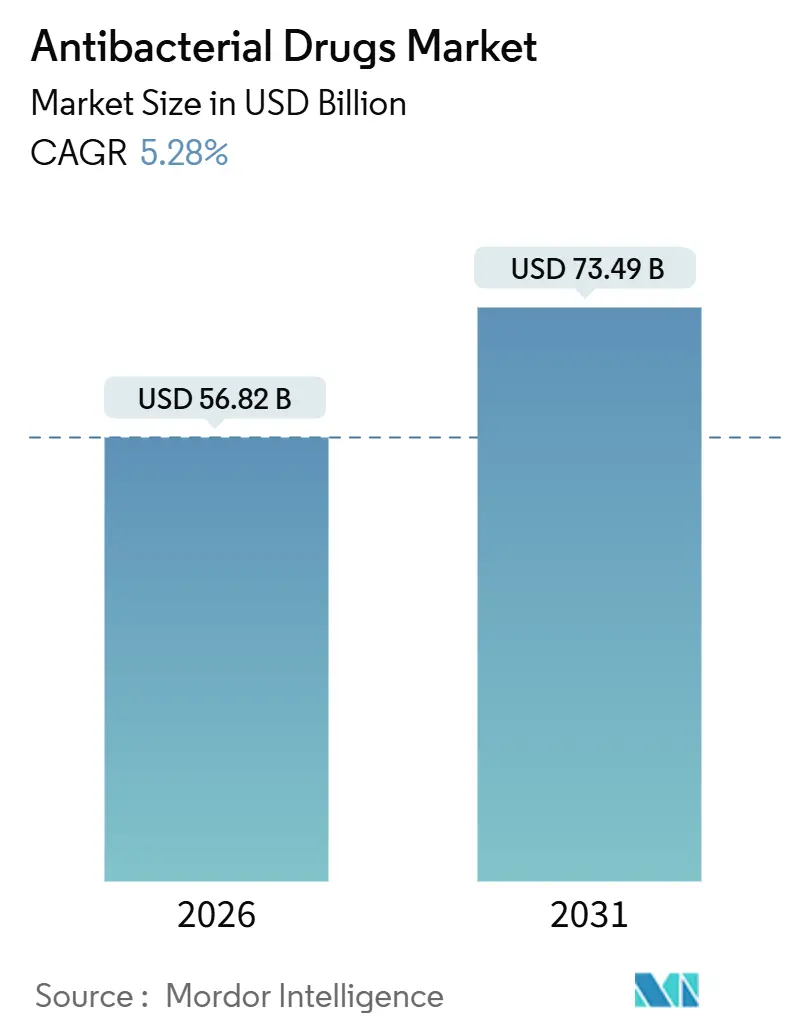

| Market Size (2026) | USD 56.82 Billion |

| Market Size (2031) | USD 73.49 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibacterial Drugs Market Analysis by Mordor Intelligence

The Antibacterial Drugs Market size is estimated at USD 56.82 billion in 2026, and is expected to reach USD 73.49 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031).

Mounting antimicrobial-resistance, shifting reimbursement rules, and population aging are increasing both the therapeutic urgency and the commercial complexity of the antibacterial drugs market. Intensive hospital protocols continue to anchor growth in parenteral formulations while stewardship programs prompt a gradual pivot toward narrow-spectrum agents. Digital pharmacy expansion, policy-backed pull incentives, and climate-driven disease spikes are further reshaping competitive priorities. At the same time, AI-enabled discovery is cutting preclinical timelines, opening a window for smaller innovators to introduce first-in-class mechanisms at a pace the industry has not seen in decades.[1]Hannah Devlin, “AI-Driven Antibiotic Discovery Accelerates Lead Optimization,” Nature, nature.com

Key Report Takeaways

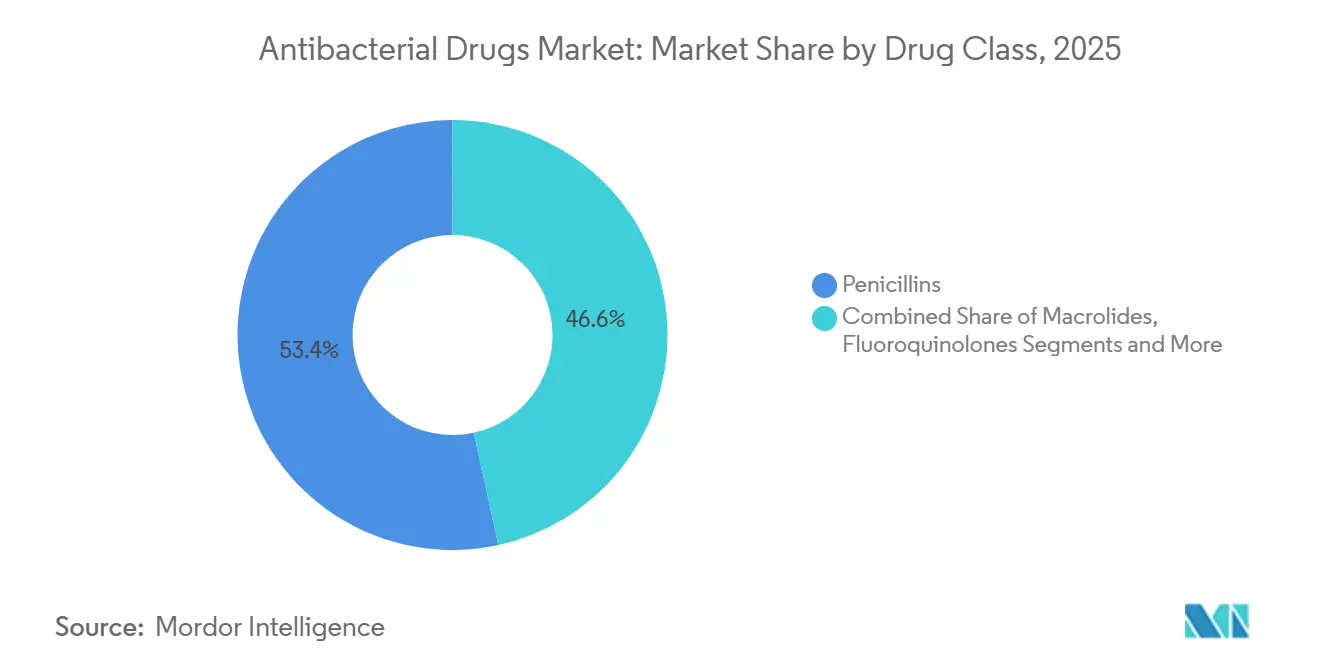

- By drug class, penicillins led with 53.41% antibacterial drugs market share in 2025, while the same class is projected to advance at a 6.67% CAGR through 2031, outpacing other classes.

- By drug mechanism, cell-wall synthesis inhibitors accounted for 51.68% of 2025 revenue, whereas protein-synthesis inhibitors are forecast to post the fastest 7.27% CAGR to 2031.

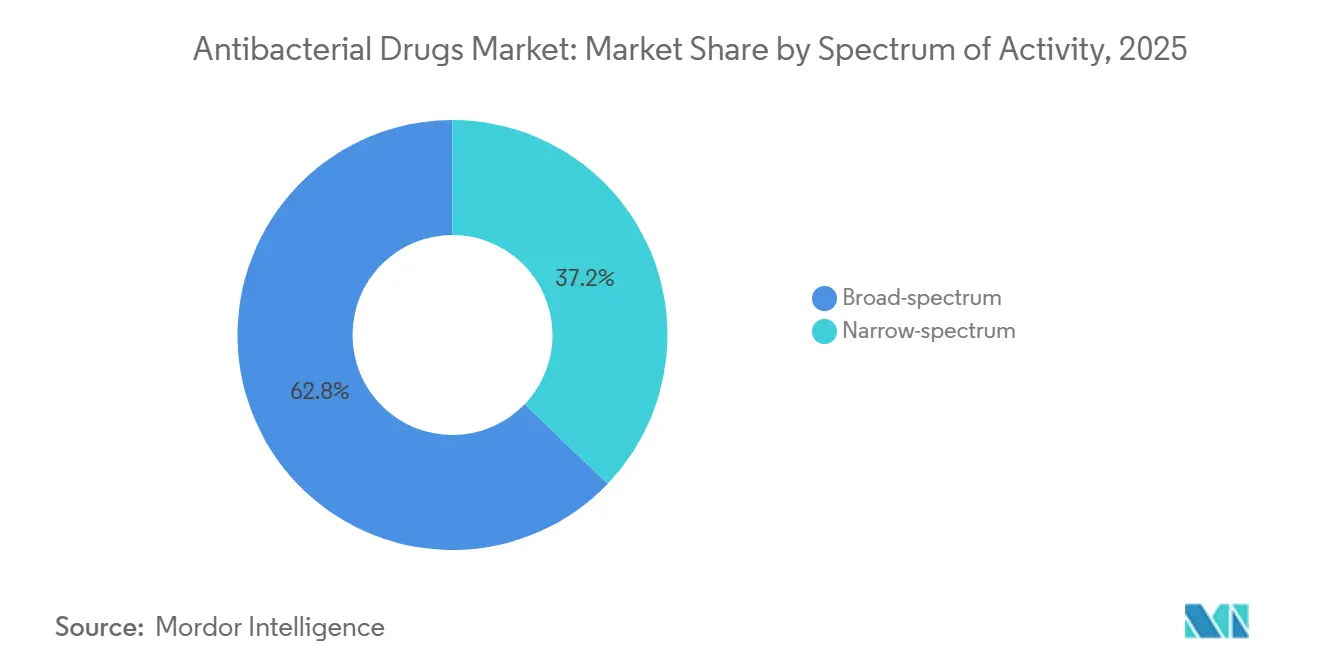

- By spectrum of activity, broad-spectrum agents captured 62.84% share in 2025; narrow-spectrum alternatives are set to expand at an 8.22% CAGR through 2031, the quickest among spectrum categories.

- By route of administration, oral formulations represented 51.32% of 2025 sales, while parenteral products are expected to record the highest 7.14% CAGR to 2031.

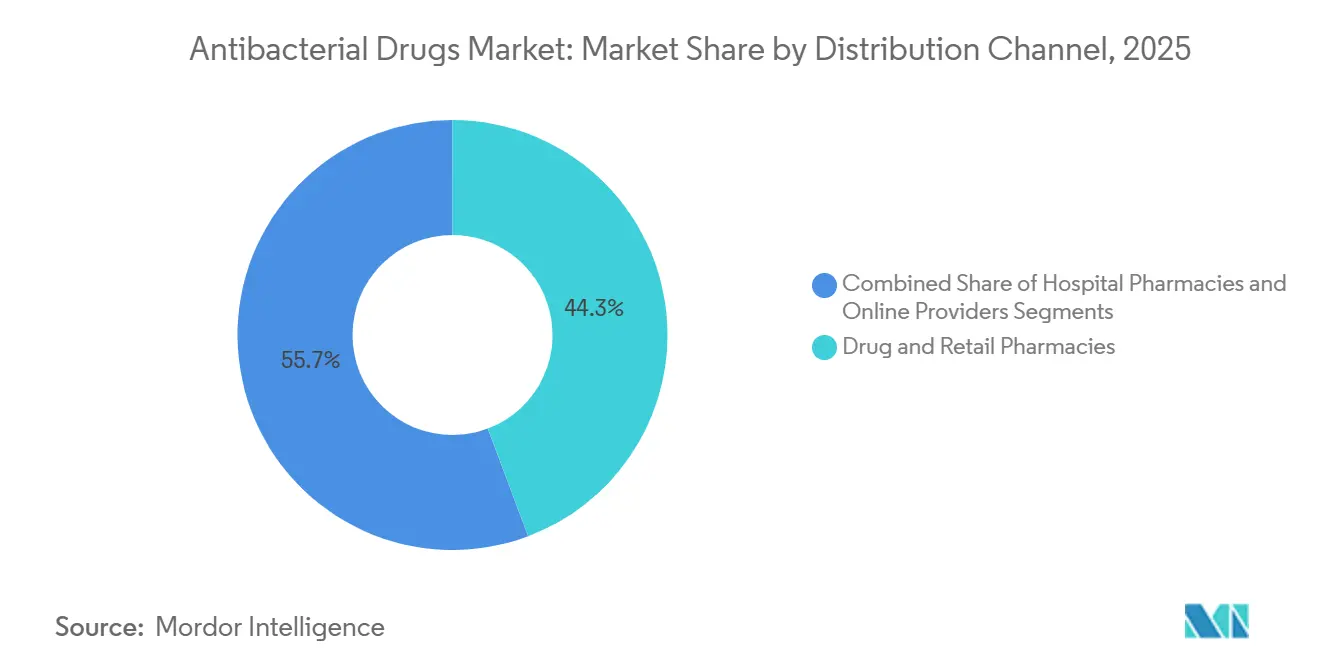

- By distribution channel, drug stores and retail pharmacies held 44.26% of revenue in 2025, as online providers are projected to grow the fastest at a 9.74% CAGR through 2031.

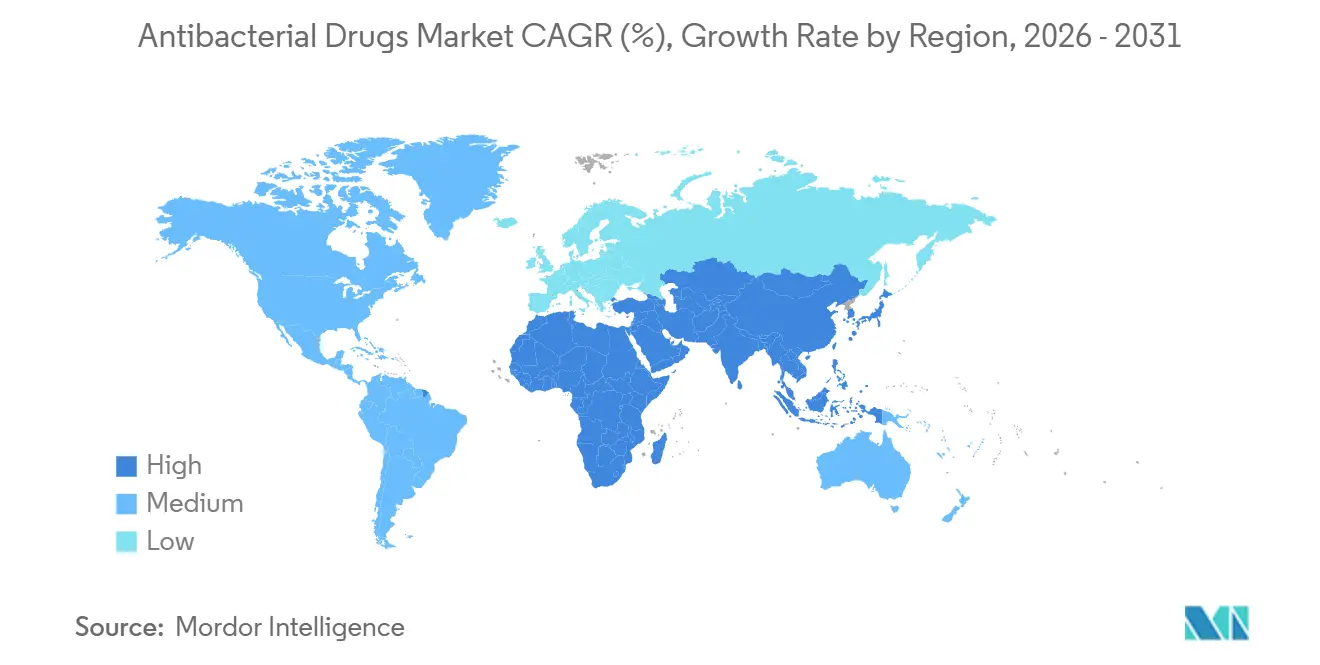

- By geography, Asia-Pacific commanded 39.53% of global revenue in 2025 and is also anticipated to log the leading 7.06% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antibacterial Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Prevalence of Drug-Resistant Bacterial Infections | +1.2% | Global, with acute pressure in South Asia, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Growing Geriatric & Immunocompromised Population | +0.9% | North America, Europe, Japan; emerging in China as demographics shift | Medium term (2-4 years) |

| Increased Government Pull-Incentives & Funding Models | +0.7% | North America, Europe; pilot programs in Australia and South Korea | Medium term (2-4 years) |

| AI-Driven Antibiotic Discovery Shortening R&D Cycles | +0.6% | Global, led by innovation hubs in United States, United Kingdom, and Switzerland | Long term (≥ 4 years) |

| Probiotic-Enabled PK Boosting that Accelerates IV-To-Oral Switch | +0.4% | North America, Europe; clinical adoption nascent in Asia-Pacific | Short term (≤ 2 years) |

| Climate-Driven Surge in Water-Borne & Zoonotic Bacterial Outbreaks | +0.5% | South Asia, Sub-Saharan Africa, Southeast Asia; spill-over to Middle East & North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Drug-Resistant Bacterial Infections

Antimicrobial resistance now appears among the top ten global health threats. In 2025, the WHO reported that more than half of the Escherichia coli isolates it tracked showed resistance to at least one critical antibiotic class.[2]WHO Newsroom Staff, “WHO Releases 2025 Antibacterial Products in Clinical and Preclinical Development,” World Health Organization, who.int Regional surveillance in Europe confirmed carbapenem-resistant Klebsiella pneumoniae rates above 60% in Greece and Romania, driving hospitals to last-resort polymyxins despite nephrotoxicity risks. Excess U.S. healthcare costs from drug-resistant infections stand at USD 4.6 billion each year.[3]Lisa M. O’Hara, “Antibiotic Resistance Threats in the United States,” Centers for Disease Control and Prevention, cdc.gov Consequently, 43 of 90 clinical-stage antibacterial candidates now target Gram-negative superbugs. Rising resistance is therefore a direct volume and value driver that is shaping formulary negotiations across every major payer market.

Growing Geriatric and Immunocompromised Population

UN data show the global 65-plus demographic headed for 1.6 billion citizens by 2050. Older adults consume 2.3 times more antibiotics per capita than the overall average across OECD nations. Expansion of biologic oncology and autoimmune therapies is enlarging the immunocompromised cohort, with febrile neutropenia still affecting over 15% of chemotherapy patients. Japan epitomizes this shift; antibiotic prescriptions for those older than 75 rose 18% between 2023 and 2025. These twin demographic and therapeutic vectors create sustained demand that favors high-acuity settings and fuels growth in the antibacterial drugs market.

Increased Government Pull Incentives and Funding Models

Subscription contracts now reward innovation independent of volume. The NHS launched a GBP 10 million per-year subscription in 2024, guaranteeing income for two priority antibiotics. The proposed U.S. PASTEUR Act earmarks USD 6 billion over 10 years for similar agreements. CARB-X alone disbursed USD 87 million in 2024 to early-stage developers. Venture capital inflows rebounded by 34% that same year. Collectively, these pull incentives mitigate commercial risk and entice new entrants into the antibacterial drugs industry.

AI-Driven Antibiotic Discovery Shortening R&D Cycles

An AI platform used by a GSK–Oxford collaboration screened 1.2 billion chemical structures and produced 12 lead compounds in just 18 months, a timeline once measured in years. Machine-learning models can now predict minimum inhibitory concentrations with 89% accuracy. Pfizer reports AI trimmed preclinical attrition by 22% and shaved USD 50 million from candidate costs. Faster discovery directly lowers burn rates, encouraging mid-cap firms to re-enter the antibacterial drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unfavourable Reimbursement Limiting ROI on Novel Agents | -0.8% | Global, acute in United States and Germany where cost-effectiveness thresholds tighten | Medium term (2-4 years) |

| Generic Erosion & Global Price-Cap Expansion | -0.6% | Global, led by India, China, and European Union reference pricing | Long term (≥ 4 years) |

| Adoption of Non-Drug Infection-Control Tech Cannibalising Demand | -0.3% | North America, Europe, Japan; nascent in urban Asia-Pacific | Short term (≤ 2 years) |

| Tightened Effluent-Limit Rules for API Plants in India & China | -0.4% | Asia-Pacific, with supply-chain ripple effects in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unfavorable Reimbursement Limiting ROI on Novel Agents

ICER judged cefiderocol cost-ineffective at its USD 3,500 launch cost, recommending a 40% price cut. Germany’s Federal Joint Committee similarly granted modest premiums to three debut antibiotics in 2025. Medicare Part D antibiotic outlays are projected to fall 12% by 2030 under current policy. Two biotech bankruptcies in 2024 underscore the financial peril for single-asset firms. Unless subscription models scale rapidly, the antibacterial drugs market may witness an innovation pullback.

Generic Erosion and Global Price-Cap Expansion

The FDA cleared 47 generic antibiotic applications in 2024, slashing U.S. prices by 65% within six months. India capped retail margins at 16% on 12 additional antibiotics in 2025. China’s bulk-procurement tenders drive 50-70% list-price cuts within weeks of award. EU reference-pricing proposals could soon equalize prices across 27 states. Persistent deflation pressures revenue growth across most legacy molecules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Penicillins Retain Primacy as Combination Formulas Extend Utility

Penicillins contributed 53.41% to antibacterial drugs market share in 2025, and the class is on track for a 6.67% CAGR through 2031. Amoxicillin-clavulanate and piperacillin-tazobactam reinforce the section’s grip, because beta-lactamase inhibitors shield the core molecule from resistance mechanisms, allowing hospitals to keep penicillins at the center of empiric regimens. Cephalosporins, driven by fourth- and fifth-generation molecules, are closing utilization gaps in surgical prophylaxis thanks to reliable activity against methicillin-resistant Staphylococcus aureus. Carbapenems and monobactams, the premium corner of the portfolio, capture less volume but high average selling prices due to their status as last-line defenses. Fluoroquinolones face volume attrition after FDA black-box upgrades, yet remain indispensable for complicated urinary tract infections where oral step-down is critical.

Combination science sets the competitive agenda. Dual beta-lactam/beta-lactamase inhibitor cocktails keep penicillins central even as resistant strains spread. Meanwhile, fusions such as aztreonam-avibactam grant monobactams a new lease on life against metallo-beta-lactamase producers. The interplay of premium launch prices and rapid generic erosion will decide how much additional value drug-class leaders can capture. For strategic planners, re-investment in established classes via formulation or PK-boosting technologies offers a defensible path to volume while entirely new mechanisms mature.

By Drug Mechanism: Protein-Synthesis Inhibitors Accelerate Amid Cell-Wall Resistance

Cell-wall synthesis inhibitors generated over half of 2025 revenue, yet protein-synthesis inhibitors are moving with a 7.27% CAGR to 2031, eclipsing broader industry velocity. The shift correlates with the proliferation of carbapenemases and extended-spectrum beta-lactamases that blunt traditional beta-lactams. Macrolides, aminoglycosides, and novel-generation tetracyclines are receiving disproportionate R&D funding as developers seek mechanisms less prone to cross-class resistance. The antibacterial drugs market size for membrane disruptors, riboswitch inhibitors, and quorum-sensing blockers is still nascent but attracting early-stage capital injections.

As next-generation ribosomal binders move down the pipeline, formulary managers will weigh pay-for-performance models that factor in the stewardship value of non-cross-resistant classes. Broad adoption depends on clinical differentiation, safety, and price. Over the forecast window, companies that deliver clear superiority in Gram-negative efficacy without nephro- or oto-toxicity stand to unlock premium slots on hospital protocols, even if initial volumes appear modest.

By Spectrum of Activity: Stewardship Push Elevates Narrow-Spectrum Alternatives

Broad-spectrum products accounted for 62.84% of sales in 2025 but stewardship-driven demand is propelling narrow-spectrum agents at an 8.22% CAGR to 2031. U.S. Core Elements guidelines now require justifications for broad empiric prescribing, incentivizing narrow regimens whenever diagnostic clarity emerges. Fidaxomicin’s commercial momentum in Clostridioides difficile indicates payer willingness to support targeted therapy at premium prices. Japanese and European reimbursement bonuses reinforce the trend.

Nonetheless, broad-spectrum drugs remain essential for sepsis and other time-critical infections where immediate coverage trumps specificity. Diagnostic turnaround improvements will gradually realign the clinical threshold that divides empiric broad therapy from targeted narrow follow-up. Suppliers should thus cultivate balanced portfolios that meet both stewardship metrics and critical-care needs, integrating rapid diagnostics to demonstrate responsible use.

By Route of Administration: IV Therapies Climb on Hospital Intensity and OPAT Expansion

Oral dosage forms contributed slightly more than half of total 2025 revenue, yet the parenteral segment is tracking a 7.14% CAGR to 2031, outpacing the broader antibacterial drugs market. Rising hospitalization for severe infections, coupled with the growth of outpatient parenteral antibiotic therapy (OPAT), puts IV formulations in a sweet spot. New once-daily oral options and PK-boost strategies are improving adherence, but high-acuity settings still demand the rapid peak plasma levels only IV delivery supplies.

OPAT expansion promises a blended revenue model: hospital start-ups followed by home-based IV continuation. Manufacturers able to bundle drug, delivery device, and remote monitoring services will gain edge. Meanwhile, inhaled and topical innovations—such as liposomal amikacin—are positioned to solve organ-specific delivery challenges, a niche but growing slice of the antibacterial drugs industry.

By Distribution Channel: Online Platforms Rewrite Access Economics

Drug stores and retail chains retained 44.26% of 2025 value share, yet online providers are surging at a 9.74% CAGR through 2031. Permanent tele-prescribing rules and same-day logistics from entrants such as Amazon Pharmacy reset consumer expectations for convenience. Hospital group-purchasing organizations counterbalance by negotiating steep discounts for inpatient inventory, squeezing manufacturer margins in mature channels.

Serialization rules under the EU Falsified Medicines Directive raise the compliance bar for e-pharmacies but also enhance trust, contributing to sustained e-commerce growth. Manufacturers cultivating direct-to-consumer strategies and digitally integrated adherence support will stand to capture the incremental upside from this distribution transition within the antibacterial drugs market.

Geography Analysis

Asia-Pacific delivered 39.53% of global antibacterial drugs market revenue in 2025 and is forecast to post a 7.06% CAGR to 2031. China’s 2024 reimbursement expansion added 200 million rural residents, boosting demand for oral cephalosporins and macrolides. India continues to produce 60% of the world’s generic antibacterial supply, yet environmental upgrades mandated for API clusters are lifting cost curves, which could dampen price-based competitive advantage. Japan’s stewardship roadmap seeks a 20% prescription reduction by 2030, a volume constraint partially offset by its fast-growing elderly cohort.

North America and Europe remain policy laboratories. Fourteen QIDP designations granted by the FDA during 2024-25 extend exclusivity but do not guarantee market uptake when Medicare formularies restrict coverage. The European Medicines Agency cleared seven antibiotics in 2024, though German and U.K. reimbursement boards capped premiums, demonstrating the rehearsal of cost-effectiveness over novelty. Subscription pilots in England, Australia, and South Korea expand the template but still involve small absolute revenue pools.

Middle East, Africa, and South America face climate-linked outbreak volatility. Cholera cases spiked 340% in Sub-Saharan Africa during 2024 floods. Brazil’s inclusion of linezolid and tigecycline for drug-resistant tuberculosis adds USD 120 million to annual procurement budgets. Gulf states channel sovereign-fund capital toward domestic cephalosporin plants, aiming to bolster regional autonomy. Across these varied settings, growth drivers are decoupling from GDP, underscoring the need for supply-chain resilience and local-policy fluency.

Competitive Landscape

Global competition is moderately concentrated. Pfizer, Merck, and GlaxoSmithKline defend maturating franchises through dose-optimization, pediatric labels, and fixed-dose combinations. Indian generics—Cipla, Dr. Reddy’s, Sun Pharma—exploit vertical integration to undercut prices in volume-based tenders, illuminating the cost-centric segment of the antibacterial drugs industry.

Innovation flows through biotech pipelines enabled by pull incentives. Breakthrough designation for a phage cocktail targeting multidrug-resistant Pseudomonas signals regulatory readiness to entertain biologics. Pfizer’s 2025 patent for a metallo-beta-lactamase inhibitor illustrates how incumbents intend to sustain exclusivity on core beta-lactam platforms. Competitive advantage is therefore tilting toward firms that combine agility—fast R&D cycles, flexible manufacturing, nimble regulatory strategy—with stewardship-aligned commercialization.

Looking ahead, market winners will be those that pair differentiated mechanisms with credible access solutions. This includes subscription-model advocacy, real-time resistance-data services, and patient-support programs that integrate digital adherence tracking. Failure to align with these evolving commercial norms risks margin erosion, even for clinically outstanding assets.

Antibacterial Drugs Industry Leaders

GlaxoSmithKline plc

Merck & Co., Inc.

Novartis AG

Johnson & Johnson Services LLC

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The Global Antibiotic Research & Development Partnership gained FDA approval for NUZOLVENCE (zoliflodacin), the first single-dose oral therapy for uncomplicated gonorrhea.

- September 2025: Tabuk Pharmaceuticals and Cumberland launched Vibativ (telavancin) injection in Saudi Arabia.

- August 2025: Iterum Therapeutics commenced U.S. commercialization of ORLYNVAH (sulopenem etzadroxil + probenecid) oral tablets for uncomplicated urinary-tract infections.

- February 2025: AbbVie secured FDA clearance for EMBLAVEO (aztreonam + avibactam) in combination with metronidazole for complicated intra-abdominal infections.

Global Antibacterial Drugs Market Report Scope

Antibacterial drugs are medicines that treat bacterial infections by targeting processes like cell wall formation, protein synthesis, or DNA replication. These drugs can either destroy bacteria (bactericidal) or inhibit their reproduction (bacteriostatic).

The Antibacterial Drugs Market Report is Segmented by Drug Class, drug mechanism, spectrum of activity, route of administration, distribution channel, and geography. By Drug Class, the market is segmented into Penicillins, Cephalosporins, Carbapenems & Monobactams, Macrolides, Fluoroquinolones, Aminoglycosides, Sulfonamides & Others. By Drug Mechanism, the market is segmented into Cell-wall synthesis inhibitors, Protein-synthesis inhibitors, DNA/RNA-synthesis inhibitors, Folic-acid pathway inhibitors, Membrane disruptors & novel MoA. By Spectrum of Activity, the market is segmented into Broad-spectrum and Narrow-spectrum. By Route of Administration, the market is segmented into Oral, Parenteral/IV, and Topical/Others. By Distribution Channel, the market is segmented into Hospital Pharmacies, Drug Stores & Retail Pharmacies, Online Providers. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The Market Forecasts are Provided in Terms of Value (USD).

| Penicillins |

| Cephalosporins |

| Carbapenems & Monobactams |

| Macrolides |

| Fluoroquinolones |

| Aminoglycosides |

| Sulfonamides & Others |

| Cell-wall synthesis inhibitors |

| Protein-synthesis inhibitors |

| DNA/RNA-synthesis inhibitors |

| Folic-acid pathway inhibitors |

| Membrane disruptors & novel MoA |

| Broad-spectrum |

| Narrow-spectrum |

| Oral |

| Parenteral / IV |

| Topical / Others |

| Hospital Pharmacies |

| Drug Stores & Retail Pharmacies |

| Online Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Penicillins | |

| Cephalosporins | ||

| Carbapenems & Monobactams | ||

| Macrolides | ||

| Fluoroquinolones | ||

| Aminoglycosides | ||

| Sulfonamides & Others | ||

| By Drug Mechanism | Cell-wall synthesis inhibitors | |

| Protein-synthesis inhibitors | ||

| DNA/RNA-synthesis inhibitors | ||

| Folic-acid pathway inhibitors | ||

| Membrane disruptors & novel MoA | ||

| By Spectrum of Activity | Broad-spectrum | |

| Narrow-spectrum | ||

| By Route of Administration | Oral | |

| Parenteral / IV | ||

| Topical / Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Drug Stores & Retail Pharmacies | ||

| Online Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the antibacterial drugs market in 2026?

The antibacterial drugs market size is USD 56.82 billion in 2026.

What is the projected growth rate to 2031?

The market is forecast to grow at a 5.28% CAGR, reaching USD 73.49 billion by 2031.

Which drug class holds the largest share?

Penicillins lead with 53.41% antibacterial drugs market share as of 2025.

Why are narrow-spectrum antibiotics growing faster than broad-spectrum options?

Stewardship policies now reward targeted therapy, pushing narrow-spectrum agents to an 8.22% CAGR.

What role does AI play in antibacterial discovery?

AI screening and optimization have reduced lead-identification timelines to 18 months and cut preclinical attrition by 22%.

How are online pharmacies influencing distribution?

Regulatory changes and same-day delivery are driving a 9.74% CAGR for online providers, gradually reallocating volume away from traditional retail pharmacies.

Page last updated on: