Anti-Neprilysin Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

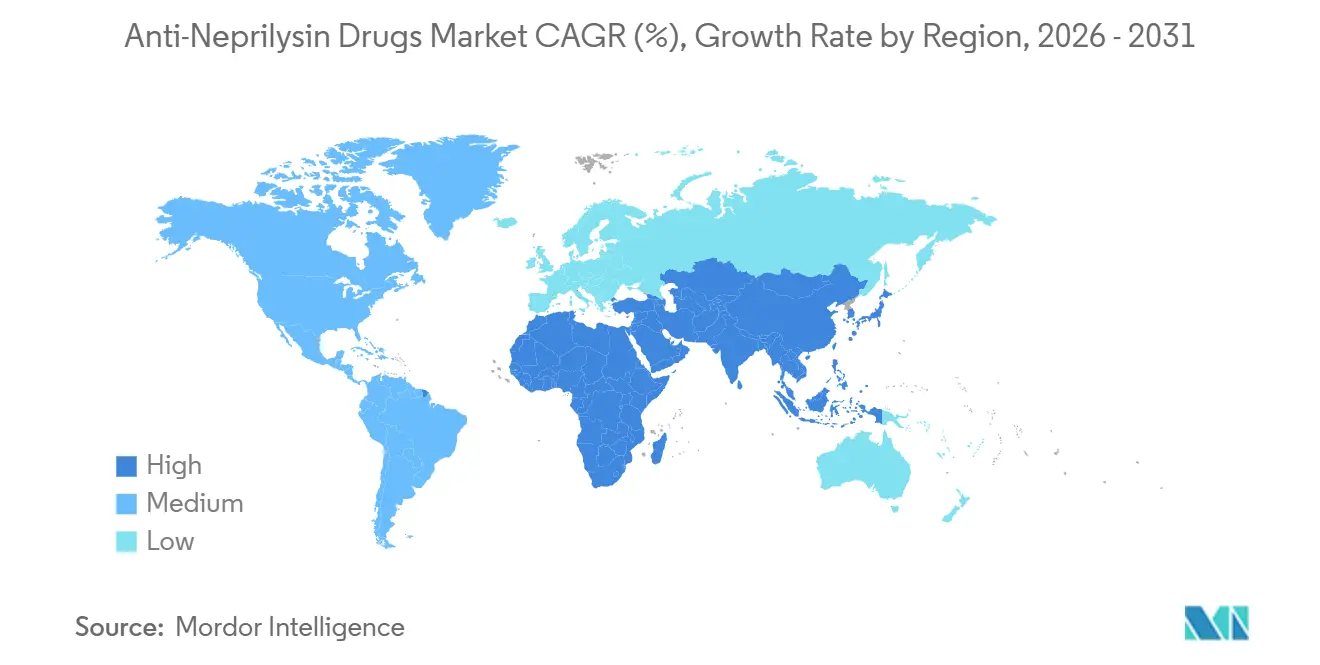

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

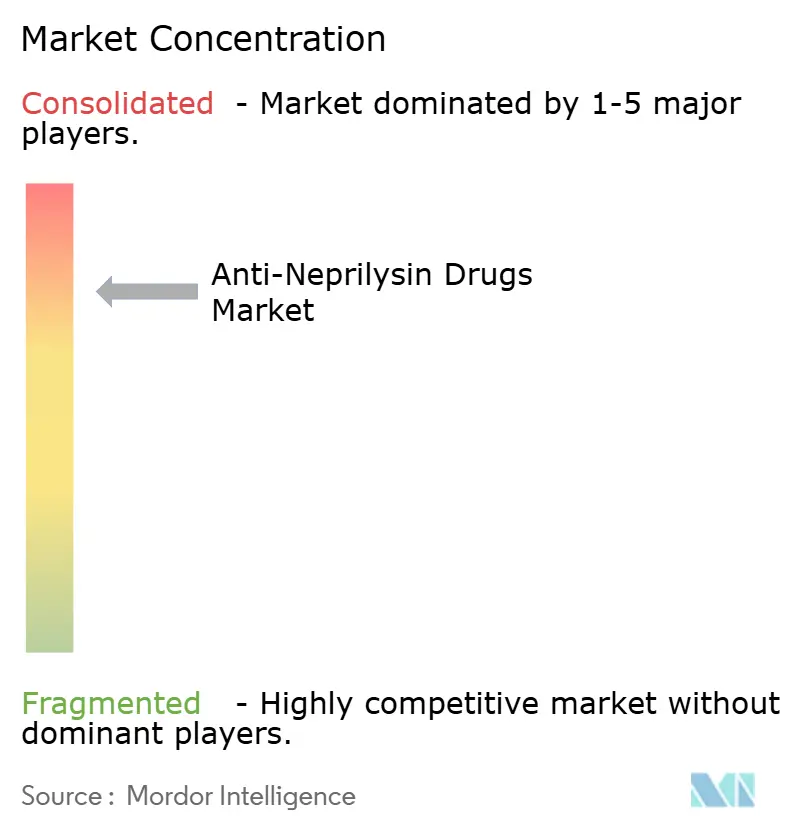

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Neprilysin Drugs Market Analysis by Mordor Intelligence

The Anti-Neprilysin Drugs Market size is expected to increase from USD 1.38 billion in 2025 to USD 1.45 billion in 2026 and reach USD 1.82 billion by 2031, growing at a CAGR of 4.63% over 2026-2031.

Demand stays underpinned by a worldwide heart-failure burden that remains stubbornly high and by guideline upgrades that now position angiotensin receptor–neprilysin inhibitors (ARNIs) as first-line therapy for heart failure with reduced ejection fraction (HFrEF). Competitive dynamics are also shifting: biologic antibodies and peptides are entering early-stage trials, while pricing pressure is intensifying in the United States and Europe as courts reject patent-extension bids. Regulatory broadening into preserved-ejection-fraction and pediatric segments, coupled with expansion in Asia-Pacific markets such as Japan, China, and the Philippines, gives the anti-neprilysin drugs market a multi-regional growth runway. At the same time, health-system cost containment, the arrival of inexpensive generics, and emerging cognitive-safety debates are tempering sales expectations.

Key Report Takeaways

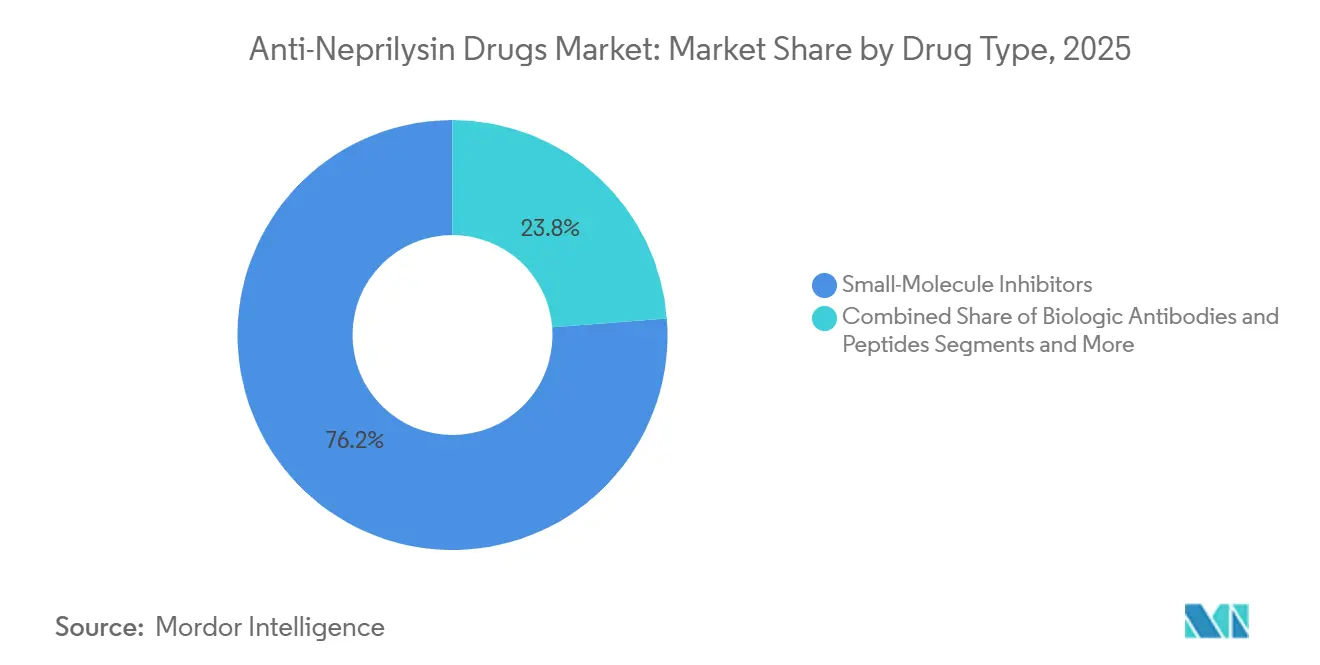

- By drug type, small-molecule inhibitors led with 76.23% revenue share in 2025; biologic antibodies and peptides are poised for the quickest climb, advancing at an 8.46% CAGR to 2031.

- By indication, HFrEF contributed 61.53% of anti-neprilysin drugs market share in 2025, while HFpEF/HFmrEF is projected to register a 7.34% CAGR through 2031.

- By dosage form, tablets accounted for 86.35% of the anti-neprilysin drugs market size in 2025 and injectables are predicted to rise at a 6.77% CAGR over the outlook period.

- By distribution channel, hospital pharmacies held 52.42% revenue in 2025, yet online and specialty outlets are expanding at an 8.97% CAGR to 2031.

- By geography, North America generated 38.64% sales in 2025; Asia-Pacific is tracking the fastest regional CAGR at 6.25% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anti-Neprilysin Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic Heart Failure & Hypertension | +1.2% | Global, strongest absolute growth in Asia-Pacific and North America | Long term (≥ 4 years) |

| Guideline Inclusion of Sacubitril/Valsartan | +1.0% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Regulatory Expansion into HFpEF & Pediatrics | +0.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Once-Daily Next-Gen Small-Molecule NEP Inhibitors | +0.5% | Global, early clinical impact | Long term (≥ 4 years) |

| Low-Cost Biomanufacturing of Anti-Neprilysin Antibodies | +0.4% | North America, Europe, India | Long term (≥ 4 years) |

| Expansion of Digital Titration & Remote-Monitoring Platforms | +0.3% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Heart Failure & Hypertension

Worldwide heart-failure prevalence touched 64 million people in 2024 and continues to climb, largely because populations are aging and hypertension control remains inconsistent.[1]World Health Organization, “Heart Failure Statistics 2024,” WHO, who.inThe American Heart Association counted 6.9 million U.S. adults living with the condition in 2024, estimating that one in five Americans will develop heart failure during their lifetime. Direct medical spending in the United States reached USD 30.7 billion in 2024, a burden that elevates payers’ interest in drug classes shown to curb hospitalization.[2]Centers for Disease Control and Prevention, “Heart Failure Facts,” CDC, cdc.gov Asia-Pacific is experiencing the fastest case-count expansion as urban diets high in sodium collide with limited blood-pressure screening, yet reimbursement gaps slow uptake. The persistence of high mortality, projected to reach 8 million global deaths by 2030, keeps attention fixed on therapies with proven survival benefit.

Guideline Inclusion of Sacubitril/Valsartan (ARNI)

In 2024 the American College of Cardiology designated ARNI as preferred first-line treatment for HFrEF, replacing long-standing ACE inhibitor and ARB standards.[3]American College of Cardiology, “2024 Expert Consensus Decision Pathway,” ACC, acc.org European guidelines mirrored that upgrade, although payer rules differ across member states, slowing uniform rollout. U.S. hospital formularies responded by making ARNI the default heart-failure therapy, yet insurers still enforce prior-authorization hurdles that delay initiation. In single-payer systems such as Ireland and the United Kingdom, budget caps create local restrictions, demonstrating how clinical endorsement alone does not guarantee access. Even so, guideline elevation supports steady prescription growth and strengthens the class in negotiations with health plans.

Regulatory Expansion into HFpEF & Pediatrics

The U.S. FDA’s 2021 label broadening to include chronic heart-failure patients with ejection fractions below normal unlocked a clinically significant HFpEF population previously underserved by pharmacotherapy. Pediatric approvals in the United States (2019) and Japan (2024), plus a granule formulation launched in April 2024, further extended reach to younger cohorts. Although the PARAGON-HF trial narrowly missed its primary endpoint, post-hoc analyses guided regulators toward nuanced HFpEF indications. These progressive approvals enlarge the eligible pool and offer headroom for sales momentum despite looming generic erosion.

Once-Daily Next-Gen Small-Molecule NEP Inhibitors

Pipeline agents seek to simplify dosing and address theoretical amyloid-beta accumulation concerns. Regeneron’s REGN5381 activates natriuretic peptide receptor 1 directly, avoiding neprilysin blockade and aiming for once-daily or even less frequent regimens. Phase-3-stage candidates are absent, so commercial impact sits beyond the current forecast window, yet R&D disclosures signal where competitive play is heading. The prospect of differentiated mechanisms may restrain the long-run price-cutting ability of generics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent Expiry & Generic Erosion of Entresto | -0.9% | North America, Europe | Short term (≤ 2 years) |

| High Therapy Cost & Reimbursement Barriers | -0.6% | Global, acute in Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Rising Adoption of Alternative HF Drug Classes | -0.5% | Global | Medium term (2-4 years) |

| Long-Term Cognitive-Safety Concerns | -0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Expiry & Generic Erosion of Entresto

A Delaware court decision in July 2025 cleared Alembic, MSN, Laurus, and Lupin to launch generic sacubitril/valsartan, ending Novartis’s bid for exclusivity through 2026. Branded cardiovascular drugs typically lose 30-50% price inside the first year of multi-source competition, and European approvals such as Teva’s Irish listing in September 2025 set the stage for wider erosion. Novartis still holds method-of-use patents into the 2030s, but they cannot block generic marketing for on-label indications, so volume share is likely to slide toward 20-30% by 2028 unless a next-generation product emerges.

High Therapy Cost & Reimbursement Barriers

Entresto’s U.S. list price topped USD 6,000 per patient annually in 2024, triggering prior-authorization hurdles that delay starts and create administrative drag. In single-payer systems, cost-effectiveness ceilings push payers to limit use. The U.K. National Institute for Health and Care Excellence placed the incremental cost-effectiveness ratio near its upper payment threshold, leading some National Health Service trusts to stagger adoption. Out-of-pocket costs in lower-middle-income economies still exceed household income for many patients, restricting uptake until generics penetrate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Small Molecules Hold Sway While Biologics Catch Up

Small-molecule inhibitors retained 76.23% of 2025 revenue because sacubitril/valsartan lacks a differentiated competitor. Biologic antibodies and peptides, however, are tracking the fastest 8.46% CAGR and could erode this dominance from 2029 onward. The anti-neprilysin drugs market size for biologics is expected to grow meaningfully once the first late-phase candidates read out pivotal data. Manufacturing cost remains a hurdle, yet expanded peptide and antibody capacity in the United States and Europe is lowering barriers.

The anti-neprilysin drugs market has room for next-generation classes that avoid angioedema and cognitive-safety debates. Regeneron’s natriuretic peptide receptor agonist shows early promise, but material commercial impact lies beyond the forecast window. Without near-term replacements, generics will seize share from branded small molecules first, followed by eventual disruption as biologics prove value.

By Indication: HFrEF Dominates, HFpEF Surges

HFrEF delivered 61.53% of 2025 sales thanks to unequivocal survival data and class-I guideline placement. HFpEF/HFmrEF, however, is the fastest-growing indication, rising at 7.34% and expected to narrow the gap by 2031. The anti-neprilysin drugs market share for HFpEF could jump once ongoing real-world studies validate outcomes in higher-ejection-fraction patients. Pediatric approvals widen the total treated pool further, albeit from a smaller base.

Systemic hypertension remains a niche, and pain or CNS disorders are still exploratory. Nevertheless, label expansions broaden payers’ willingness to reimburse, creating incremental volume even if per-patient profit compresses under generic pricing.

By Dosage Form: Tablets Prevail While Injectables Surface

Tablets made up 86.35% of revenue in 2025, buoyed by three strength options that support titration. The anti-neprilysin drugs market size for injectables is rising at a 6.77% CAGR, though from a low base, mainly because biologic candidates require parenteral routes. Pediatric granule formulations help niche sub-groups but do not shift overall dollar mix. As generic tablets proliferate, innovators may push subcutaneous biologics to reclaim premium pricing.

By Distribution Channel: Hospital Pharmacies Still Lead But Online Channels Accelerate

Hospital pharmacies controlled 52.42% of 2025 revenue, reflecting initiation during inpatient stays. Online and specialty outlets, however, will grow quickest at 8.97% on the back of mail-order convenience and integrated remote-monitoring packages. As generics hit shelves, prior-authorization barriers shrink, steering volume away from hospitals toward retail and digital channels that handle high-throughput dispensing.

Geography Analysis

North America’s leadership rests on robust diagnosis rates, guideline adherence, and higher disposable income, yet the Inflation Reduction Act will negotiate Medicare prices from 2026, trimming topline by 10-15% for branded therapies. Canada’s provincial formularies offer generally favorable coverage, although Québec caps annual growth in public-drug spending, nudging Novartis toward risk-sharing deals.

Europe transitions into a value-driven phase. While Germany maintains unrestricted access, Southern and Eastern member states apply tighter budget controls. Ireland’s early generic listing showcases the speed with which competitive entry can reshape drug spending. Expect further price compression once pan-European tenders gain momentum.

Asia-Pacific is the undisputed growth engine. Japan’s pediatric clearance and China’s expanded National Reimbursement Drug List reinforce volume, but average selling price is lower because of local procurement rules. The Philippines’ 2024 approval signals Southeast Asia’s widening access, though affordability remains a sticking point in Vietnam and Indonesia.

Middle East and Africa are nascent. The United Arab Emirates’ National Succinct Statement in 2024 points to gradual uptake, but the region’s heart-failure infrastructure is still developing. South America offers selective pockets of strength—Brazil’s public procurement and private insurance ¬ uptake—yet macroeconomic volatility in Argentina and other markets curbs visibility.

Competitive Landscape

The anti-neprilysin drugs market is highly concentrated. That share is now slipping as Alembic, MSN, Lupin, and Laurus debut authorized generics. Novartis counters with an evidence-generation campaign of over 40 studies and heavy U.S. manufacturing investment. Should it successfully launch a biologic successor by 2030, the company could defend premium territory even as tablet revenue erodes.

Generic challengers rely on steep discounts to win volume, especially in price-sensitive geographies such as India and parts of Africa. Regeneron’s REGN5381 introduces a mechanistically distinct threat, though commercialization is unlikely before 2031. Meanwhile, digital-health alliances that wrap titration and monitoring into a service help differentiate products in payer negotiations.

Combination possibilities, such as an ARNI-SGLT2 inhibitor single pill, remain untapped. Whoever marries pharmacology with adherence technology first could gain a defensible niche even in a commoditizing landscape.

Anti-Neprilysin Drugs Industry Leaders

Novartis International AG

Cipla Ltd

Regeneron Pharmaceuticals

Teva Pharmaceutical

Laurus Labs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ireland’s Health Products Regulatory Authority cleared Teva’s generic sacubitril/valsartan tablets, marking Europe’s first generic entry.

- January 2025: Lupin secured U.S. FDA approval for generic sacubitril/valsartan, expanding multi-source competition.

- December 2024: Eli Lilly announced a USD 3 billion expansion of its Wisconsin injectable-medicine plant, boosting capacity for pipeline products.

Global Anti-Neprilysin Drugs Market Report Scope

Neprilysin inhibitors (NEPi), also called anti-neprilysin drugs, are therapeutic agents that block the zinc-dependent neprilysin enzyme, which breaks down vasoactive peptides like natriuretic peptides (ANP, BNP), bradykinin, and substance P.

The Anti-Neprilysin Drugs Market Report is segmented by Drug Type, Indication, Dosage Form, Distribution Channel, and Geography. By Drug Type, the market is segmented into Small-Molecule Inhibitors, Biologic Antibodies & Peptides, and Dual-Target Candidates. By Indication, the market is segmented into HFrEF, HFpEF/HFmrEF, Hypertension, Pain & CNS, and Alzheimer’s Disease. By Dosage Form, the market is segmented into Tablets, Suspension, and Injectables. By Distribution Channel, the market is segmented into Hospital, Retail, and Online & Specialty. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Small-Molecule Inhibitors |

| Biologic Antibodies & Peptides |

| Dual-Target (ACE/NEP, ECE/NEP) Candidates |

| Heart Failure – Reduced EF (HFrEF) |

| Heart Failure – Preserved/Borderline EF (HFpEF/HFmrEF) |

| Systemic Hypertension |

| Pain & CNS Disorders |

| Alzheimer’s & Cognitive Disorders |

| Tablets |

| Suspension |

| Injectables |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online & Specialty Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Small-Molecule Inhibitors | |

| Biologic Antibodies & Peptides | ||

| Dual-Target (ACE/NEP, ECE/NEP) Candidates | ||

| By Indication | Heart Failure – Reduced EF (HFrEF) | |

| Heart Failure – Preserved/Borderline EF (HFpEF/HFmrEF) | ||

| Systemic Hypertension | ||

| Pain & CNS Disorders | ||

| Alzheimer’s & Cognitive Disorders | ||

| Dosage form | Tablets | |

| Suspension | ||

| Injectables | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online & Specialty Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the anti-neprilysin drugs market in 2026?

The anti-neprilysin drugs market size is valued at USD 1.45 billion in 2026 and is forecast to expand to USD 1.82 billion by 2031.

Which indication drives most anti-neprilysin drug sales today?

Heart failure with reduced ejection fraction (HFrEF) accounted for 61.53% of global revenue in 2025.

What impact will generics have on Entresto pricing?

Multi-source competition is expected to cut branded prices by 30-50% within the first year after generic entry.

Which region is set to grow fastest through 2031?

Asia-Pacific is expected to post the highest CAGR at 6.25% through 2031 owing to regulatory approvals and expanding reimbursement.

Are biologic alternatives close to launch?

Biologic antibodies and peptides are in early clinical stages; none are projected to reach market before 2030.

How do digital titration platforms influence ARNI adoption?

Remote-monitoring programs accelerate dose optimization and can raise adherence, improving real-world effectiveness while supporting payer coverage.

Page last updated on: