Penicillin Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.72 Billion |

| Market Size (2031) | USD 12.68 Billion |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

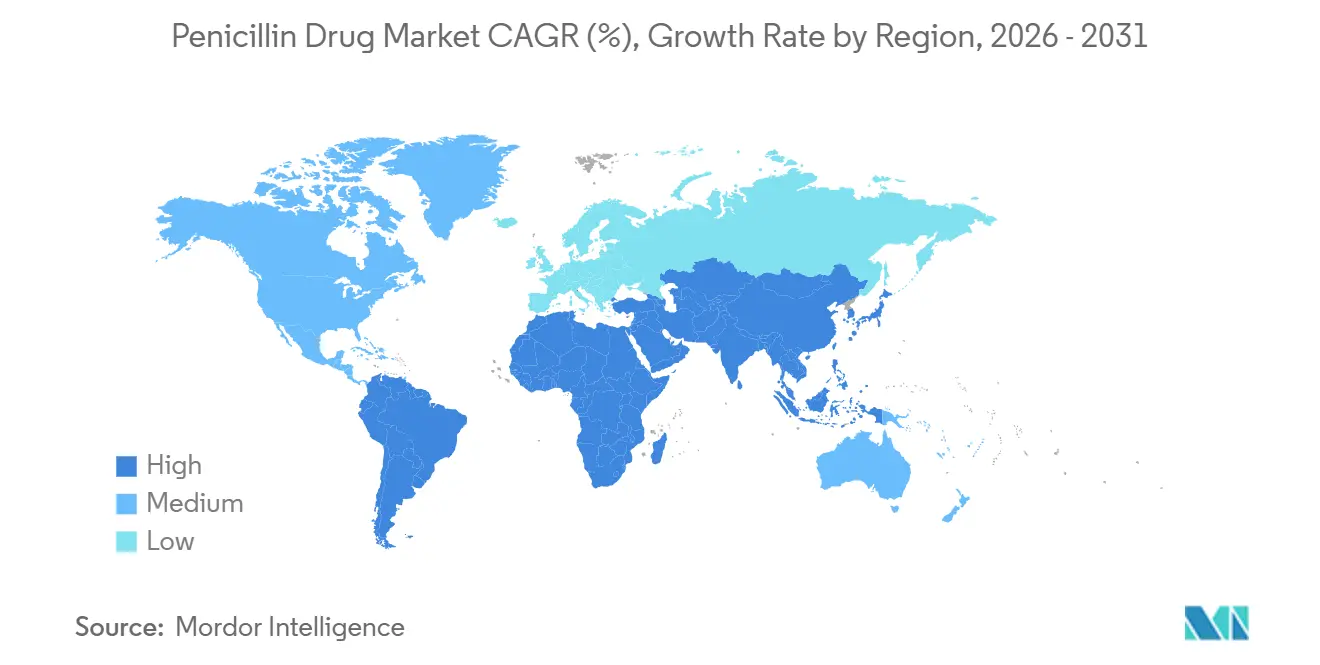

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Penicillin Drug Market Analysis by Mordor Intelligence

The Penicillin Drug Market size is projected to expand from USD 10.49 billion in 2025 and USD 10.72 billion in 2026 to USD 12.68 billion by 2031, registering a CAGR of 3.41% between 2026 to 2031.

A confluence of persistent community-acquired infections, cost-focused procurement in emerging economies, and incremental innovation in β-lactamase inhibition continues to underpin steady demand. Hospitals are upgrading formularies to extended-spectrum combinations that blunt the rise of extended-spectrum β-lactamase pathogens, while community pharmacies in the United Kingdom and Australia now initiate oral amoxicillin therapy, accelerating self-care. India’s January 2026 Minimum Import Price (MIP) of USD 35 per kilogram on bulk penicillin has begun to reset Asian cost structures, favoring domestic producers over Chinese imports.[1]Press Information Bureau Staff, “Minimum Import Price on Bulk Penicillin,” Press Information Bureau, pib.gov.in At the same time, artificial-intelligence-enabled fermentation is squeezing variable costs by up to 11% at advanced facilities.[2]Zhang Li, “AI-Driven Optimization of Penicillin Fermentation,” Biotechnology and Bioengineering, wiley.com Counterbalancing these positives, antimicrobial resistance continues to erode first-line efficacy, and novel β-lactam/β-lactamase inhibitor agents, priced an order of magnitude higher than legacy molecules, are cannibalizing high-acuity volumes in North America and Europe.

Key Report Takeaways

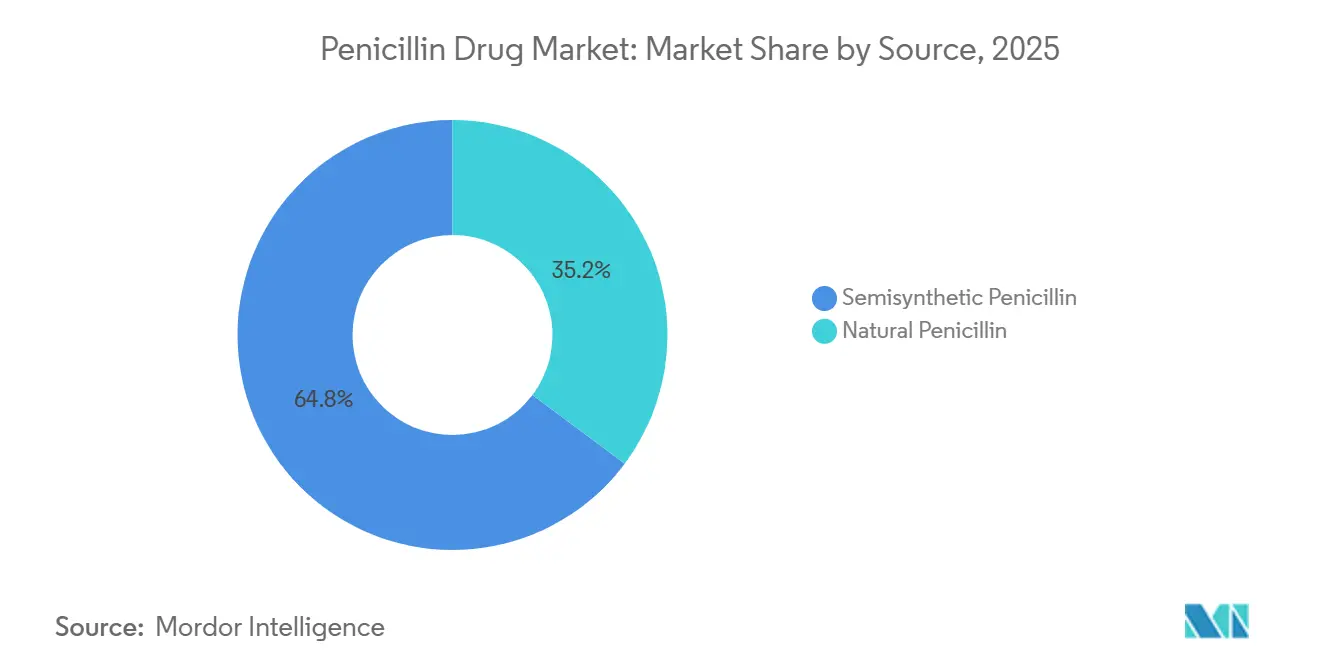

- By source, semisynthetic penicillin captured 64.78% of 2025 sales and is also the fastest-growing source category at a 5.26% CAGR through 2031, reflecting sustained aminopenicillin demand in community care.

- By product type, aminopenicillin led with 41.63% of 2025 revenue, while β-lactamase-inhibitor combinations are projected to record the highest CAGR at 5.88% through 2031.

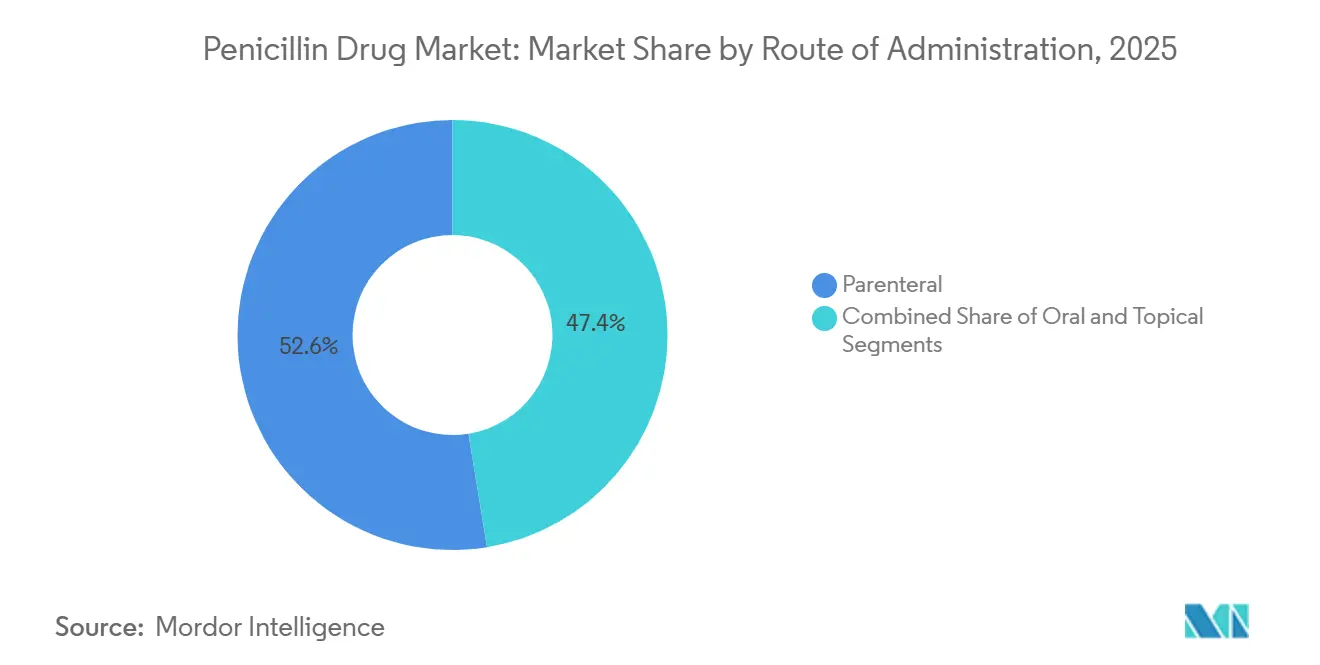

- By route of administration, parenteral formulations retained 52.56% share in 2025, whereas oral formulations are forecast to expand at a 7.32% CAGR to 2031.

- By spectrum of activity, broad-spectrum agents held 46.82% of 2025 revenue, but extended-spectrum penicillins are expected to grow fastest at 6.44% through 2031.

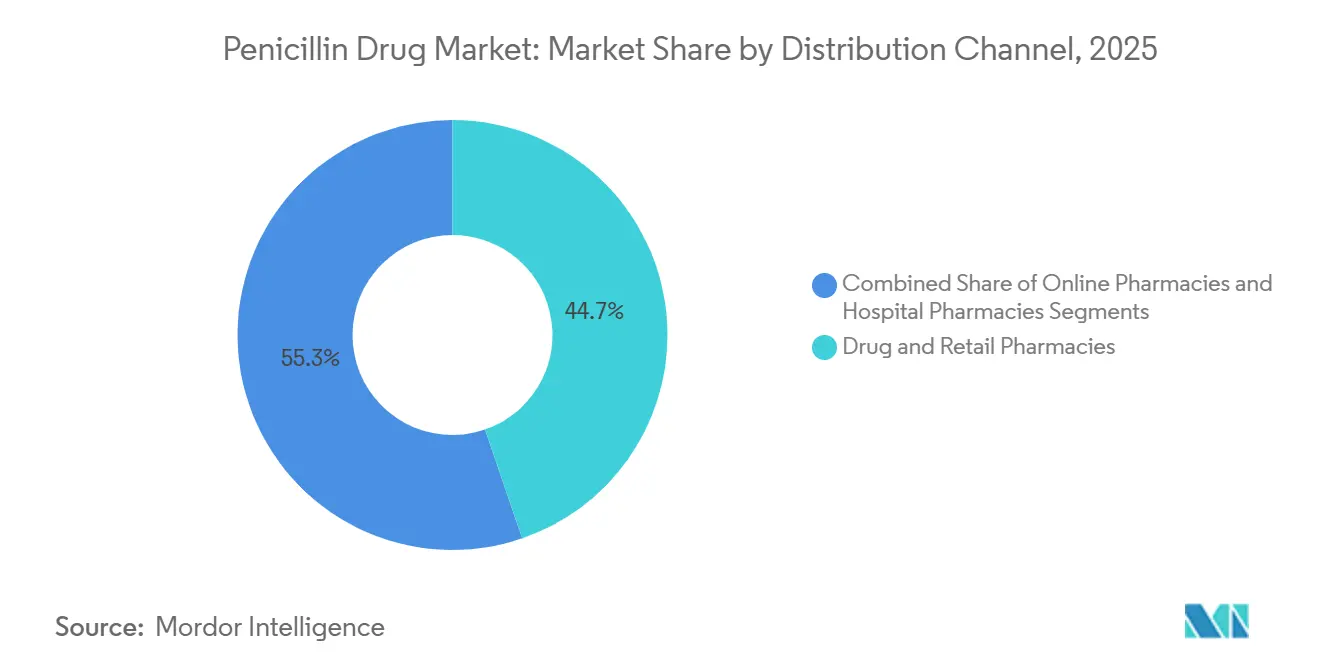

- By distribution channel, drug and retail pharmacies accounted for 44.74% of 2025 volumes, while online pharmacies are poised to advance at a 7.82% CAGR through 2031.

- By geography, Asia-Pacific led with 34.57% of 2025 sales, whereas the Middle East and Africa region is projected to register the quickest growth, at a 6.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Penicillin Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Bacterial Infections | +0.8% | Global | Medium term (2–4 years) |

| Rising Demand for Affordable Generics in Emerging Markets | +0.7% | APAC, South America, MEA | Medium to Long term (2–4+ years) |

| Government Incentives for Domestic API Production | +0.5% | India, China, ASEAN | Medium term (2–4 years) |

| Pharmacy-First Retail Initiatives Boosting Community Dispensing | +0.4% | UK, Australia, Canada | Short to Medium term (≤4 years) |

| AI-Enabled Fermentation Cost Efficiencies | +0.3% | Global | Long term (≥4 years) |

| Penicillin Prophylaxis Programs for Rheumatic Heart Disease | +0.4% | Sub-Saharan Africa, South Asia, Pacific Islands | Medium to Long term (2–4+ years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Bacterial Infections

Respiratory, urinary tract, and skin infections now drive more than 70% of penicillin prescriptions, and their incidence is climbing with urban air-pollution levels in megacities such as Delhi and Jakarta.[3]World Health Organization Staff, “Global Antimicrobial Resistance and Use Surveillance System 2025,” World Health Organization, who.int Amoxicillin remains the empiric mainstay for uncomplicated pneumonia, while aging demographics in OECD countries triple UTI incidence among those older than 65. Influenza seasons continue to spawn secondary bacterial pneumonia; U.S. amoxicillin-clavulanate scripts spiked 18% during the 2024-2025 flu season. These trends cement penicillin relevance in outpatient care, especially where diagnostic microbiology is scarce.

Rising Demand for Affordable Generics in Emerging Markets

Dose-prices between USD 0.10 and 0.50 keep generic penicillins at the top of essential-medicine lists in regions where out-of-pocket payments exceed 40% of total health expenditure. India exported 42,000 metric tons of penicillin APIs in 2024, with 60% destined for sub-Saharan Africa and Southeast Asia. Brazil cleared 37 new generic registrations in 2025, the highest in seven years. Chinese amoxicillin capsules traded at USD 8 per 1,000 units in early 2026, down one-third from 2023, underpinning volumes across rural pharmacy outlets.

Government Incentives for Domestic API Production

India’s Production Linked Incentive scheme earmarked USD 830 million for domestic penicillin intermediates, shrinking Chinese import reliance to 55% by end-2025. Aurobindo’s Andhra Pradesh plant adds 15,000 metric tons of capacity, the world’s largest single-site investment in a decade. China’s 2025 mandate that 30% of public-hospital antibiotics be sourced from domestic APIs has galvanized CSPC and NCPC expansions. Similar incentives appear in the European Union’s draft Critical Medicines Act.

Pharmacy-First Retail Initiatives Boosting Community Dispensing

The United Kingdom’s Pharmacy First program enabled pharmacists to dispense oral antibiotics for seven minor infections without physician scripts, issuing 1.2 million penicillin courses in its first year. Australia’s 2025 rule change lets pharmacists initiate amoxicillin for UTIs, shifting 300,000 GP visits annually. Early Canadian pilots show a 14-hour reduction in time-to-treatment for acute sinusitis.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Antimicrobial Resistance (AMR) | -0.9% | Global, acute in South Asia & Southern Europe | Long term (≥4 years) |

| Stringent GMP & Regulatory Compliance Costs | -0.5% | Global, hardest on SMEs | Short to Medium term (≤4 years) |

| Fermentation-Feedstock Supply Volatility | -0.3% | North America, Europe | Short term (≤2 years) |

| Uptake of Novel β-Lactam/BLI Combinations Cannibalizing Demand | -0.4% | North America, Western Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Antimicrobial Resistance (AMR)

Penicillin non-susceptibility in Streptococcus pneumoniae hit 18.3% across the European Union in 2024, up 3.6 percentage points from 2020. Indian data show 42% of community Escherichia coli UTIs now harbor ESBL genes, sidelining amoxicillin. U.S. deaths linked to penicillin-resistant pneumococci total 3,600 annually. Stewardship programs have responded by curbing empiric penicillin use in intensive care units, trimming high-margin volumes.

Stringent GMP & Regulatory Compliance Costs

FDA warning letters to penicillin API plants jumped to 14 in 2024-2025, often for aseptic lapses that triggered costly shutdowns. Europe’s Annex 1 revision now requires isolator technology for sterile processes, a USD 5.4 million upgrade per line. Indian exporters spent USD 120 million on compliance upgrades in 2024 alone, shaving 3 percentage points off operating margins. Smaller firms unable to fund such capex are exiting, concentrating production among the top players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Semisynthetic Maintains Lead

Semisynthetic variants generated 64.78% of 2025 sales, and their 5.26% CAGR keeps the penicillin drug market ahead of natural derivatives. Amoxicillin and ampicillin together cover over 60% of prescriptions, while benzathine penicillin-G sustains rheumatic heart disease programs. Sandoz’s 20% capacity expansion for 6-aminopenicillanic acid in 2024 underscores ongoing investment.

Natural penicillin remains critical for syphilis and rheumatic fever, but fermentation limitations and slower innovation limit upside. Nonetheless, donor-funded prophylaxis ensures a stable niche, particularly in Africa and Southeast Asia

By Product Type: β-Lactamase Inhibitors Accelerate

Aminopenicillins held 41.63% of 2025 revenue, yet β-lactamase-inhibitor combinations grow fastest at 5.88%. EMA’s 2025 approval of a high-dose amoxicillin-clavulanate option should lift adherence. Piperacillin-tazobactam continues to dominate antipseudomonal use in ICUs, while extended-spectrum agents such as ticarcillin-clavulanate leverage stewardship demand for carbapenem-sparing regimens.

By Route of Administration: Oral Rises Quickly

Oral formulations are growing at 7.32% as community pharmacists in the UK and Australia dispense antibiotics without GP scripts. Pediatric suspensions account for 40% of oral volumes; Cipla’s dispersible amoxicillin tablet rapidly reached 8% domestic share in India. High-dose oral regimens show pharmacokinetic profiles sufficient for select meningitis cases. Parenteral agents, however, remain indispensable for severe hospital infections.

By Spectrum of Activity: Extended-Spectrum Gains Ground

Extended-spectrum combinations expand at 6.44% as hospitals chase carbapenem stewardship targets. Piperacillin-tazobactam achieved non-inferiority to meropenem for ESBL bloodstream infections, bolstering positioning. Narrow-spectrum agents endure for pharyngitis and syphilis but face prescribing inertia toward broader coverage.

By Distribution Channel: Online Disruption

Drug and retail pharmacies still deliver 44.74% of 2025 penicillin volumes, but online platforms climb at 7.82% after India’s e-pharmacy rule change and Brazil’s similar approval. Hospital channels remain insulated for parenteral therapies procured via tenders.

Geography Analysis

Asia-Pacific captured 34.57% of 2025 sales, with India’s MIP and API incentives tipping production toward local champions, while China’s stricter prescribing guidelines reduced empiric penicillin volume but improved appropriateness metrics. Japan’s super-aging demographics keep UTI and pneumonia incidence high. Australian pharmacist prescribing powers bolster community uptake.

Rapid strep diagnostics in the United States drive a pivot back to narrow-spectrum penicillin-V, even as Germany negotiated 15% generic price cuts. The UK’s Pharmacy First maintains oral growth despite overall antibiotic decline, while France and Spain trimmed penicillin volumes double digits via awareness campaigns.

The Middle East and Africa show the fastest pace at 6.36%. Saudi Vision 2030 funds 120 new primary-care centers and 20 tertiary hospitals, expanding antibiotic reach. UAE telemedicine-linked e-pharmacies accelerate oral dispensing without in-person visits. Rwanda’s prophylaxis blueprint offers a replicable model for neighboring countries.

South America is recovering as Brazil streamlines generic approvals and Argentina normalizes import flows. Brazil’s 37 generic registrations in 2025 expand Farmácia Popular coverage to high-dose combinations.

Competitive Landscape

The penicillin drug market indicates moderate concentration. Indian and Chinese API players enjoy 30-40% cost advantages from large-scale fermentation. Aurobindo’s 2024 greenfield plant underscores capital barriers to entry. Downstream formulation remains fragmented, though digital platforms like PharmEasy are trialing private-label antibiotics that compress the wholesaler layer.

Differentiation pivots on next-generation inhibitors, sustainability, and digital supply chains. Sandoz cut glucose use 6% through AI process control, defending European share against cheaper imports. Cipla’s pediatric dispersible tablets illustrate unaddressed formulation niches. Market participants that combine cost leadership with regulatory excellence and omnichannel distribution are best placed to outpace the penicillin drug market.

Penicillin Drug Industry Leaders

Pfizer Inc.

Aurobindo Pharma Ltd.

Centrient Pharmaceuticals

GlaxoSmithKline plc

Sandoz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Alembic launched Pivya (pivmecillinam) 185 mg tablets in the United States for uncomplicated UTIs, introducing a novel β-lactam mechanism.

- January 2026: Supply of Bicillin L-A 1.2 million-unit syringes resumed in Australia; 600,000-unit format remains in shortage until Aug 2026.

- January 2026: India imposed an MIP of USD 35 per kg on bulk penicillin to promote domestic API production under its PLI scheme.

Global Penicillin Drug Market Report Scope

As per the scope of the report, penicillin is a group of beta-lactam antibiotics derived from Penicillium fungi, used to treat bacterial infections by breaking down their cell walls.y.

The Penicillin Drug Market Report is segmented by Source, Product Type, Route of Administration, Spectrum of Activity, Distribution Channel, and Geography. By Source, the market is segmented into Natural and Semisynthetic penicillins. By Product Type, the market is segmented into Aminopenicillin, Penicillinase‑Resistant, Antipseudomonal, β‑lactamase‑Inhibitor Combinations, and Extended‑Spectrum penicillins. By Route of Administration, the market is segmented into Oral, Parenteral, and Topical formulations. By Spectrum of Activity, the market is segmented into Narrow, Broad, and Extended spectrum penicillins. By Distribution Channel, the market is segmented into Hospital Pharmacies, Drug & Retail Pharmacies, and Online Pharmacies. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Natural Penicillin |

| Semisynthetic Penicillin |

| Aminopenicillin |

| Penicillinase-Resistant |

| Antipseudomonal |

| β-lactamase-Inhibitor Combinations |

| Extended-Spectrum |

| Oral |

| Parenteral |

| Topical |

| Narrow-Spectrum |

| Broad-Spectrum |

| Extended-Spectrum |

| Hospital Pharmacies |

| Drug & Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Natural Penicillin | |

| Semisynthetic Penicillin | ||

| By Product Type | Aminopenicillin | |

| Penicillinase-Resistant | ||

| Antipseudomonal | ||

| β-lactamase-Inhibitor Combinations | ||

| Extended-Spectrum | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| By Spectrum of Activity | Narrow-Spectrum | |

| Broad-Spectrum | ||

| Extended-Spectrum | ||

| By Distribution Channel | Hospital Pharmacies | |

| Drug & Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global sales of penicillin drugs be by 2031?

The penicillin drug market is forecast to reach USD 12.68 billion by 2031, reflecting a 3.41% CAGR from 2026.

Which product type is growing fastest?

Β-lactamase-inhibitor combinations such as amoxicillin-clavulanate are projected to grow at 5.88% through 2031.

Why are oral formulations gaining share?

Pharmacy-first schemes in the United Kingdom and Australia allow pharmacists to initiate therapy, pushing oral growth to a 7.32% CAGR.

What impact does India’s Minimum Import Price have?

The USD 35 per kg MIP on bulk penicillin, effective in 2026, shifts sourcing toward domestic API producers and may lift India’s production share to 35% by 2029.

How serious is antimicrobial resistance for penicillin?

Non-susceptibility in Streptococcus pneumoniae has reached 18.3% in the EU, prompting hospitals to restrict empiric penicillin use in high-risk settings.

Which region will grow fastest?

The Middle East and Africa, supported by Saudi Vision 2030 investments and expanded tele-pharmacy in the Gulf, is projected to rise at a 6.36% CAGR.

Page last updated on: