North America Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

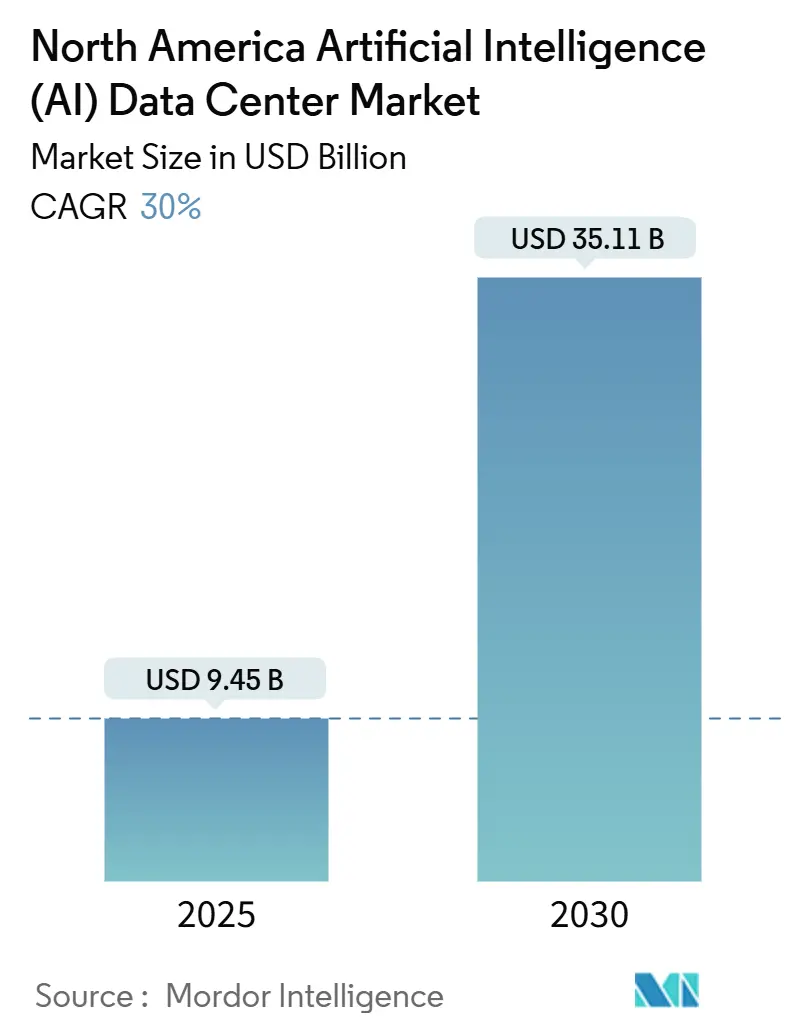

| Market Size (2025) | USD 9.45 Billion |

| Market Size (2030) | USD 35.11 Billion |

| Growth Rate (2025 - 2030) | 30.00% CAGR |

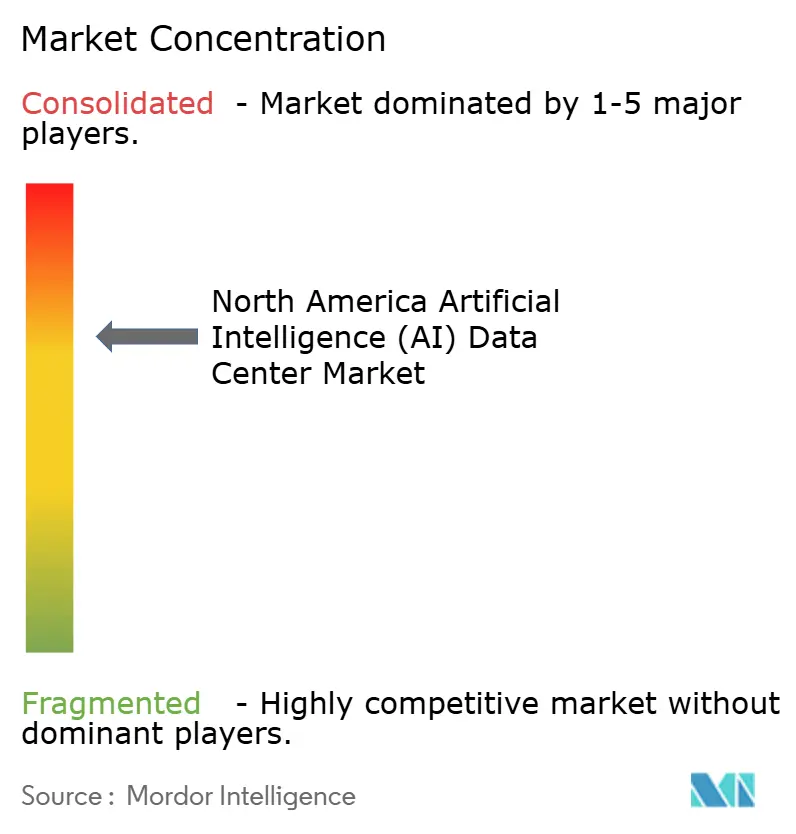

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The North America artificial intelligence data center market reached USD 9.45 billion in 2025 and is on track to attain USD 35.11 billion by 2030, exhibiting a 30.00% CAGR; the current market size reflects the region’s status as the global epicenter for hyperscale AI infrastructure development. Hyperscalers’ USD 250 billion multiyear build-out plans, the USD 52 billion CHIPS Act stimulus, and expanding corporate net-zero mandates are combining to accelerate facility commissioning, GPU procurement, and renewable-power contracting. Competitive intensity is shaped by Microsoft-OpenAI’s USD 100 billion Stargate project, Amazon’s USD 150 billion regional expansion, and a widening slate of liquid-cooling retrofits that are redefining facility design parameters for the North America artificial intelligence data center market. Supply constraints in Northern Virginia and Silicon Valley underline the strategic importance of Canada’s low-carbon power mix and Texas’ tax exemptions, while workforce shortages add operational risk for high-density campuses. Colocation operators are capturing enterprise hybrid workloads, edge nodes are proliferating alongside 5G roll-outs, and hardware investment is outpacing software spending as GPU clusters become the dominant cost line for the North America artificial intelligence data center market

Key Report Takeaways

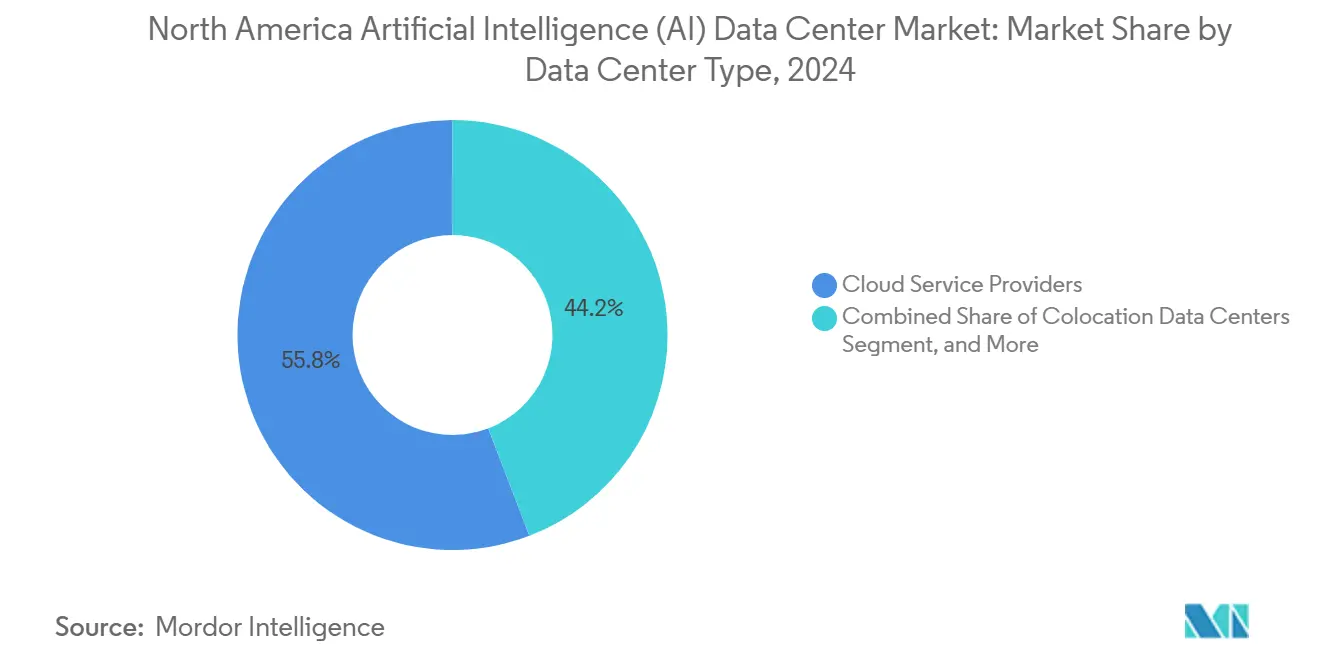

- By data center type, cloud service providers led with 55.82% revenue share in 2024 in the North America artificial intelligence data center market, while colocation facilities are forecast to expand at a 32.56% CAGR through 2030.

- By component, software technology accounted for 45.83% of the North America artificial intelligence data center market size in 2024; hardware infrastructure registers the fastest growth at 31.78% CAGR.

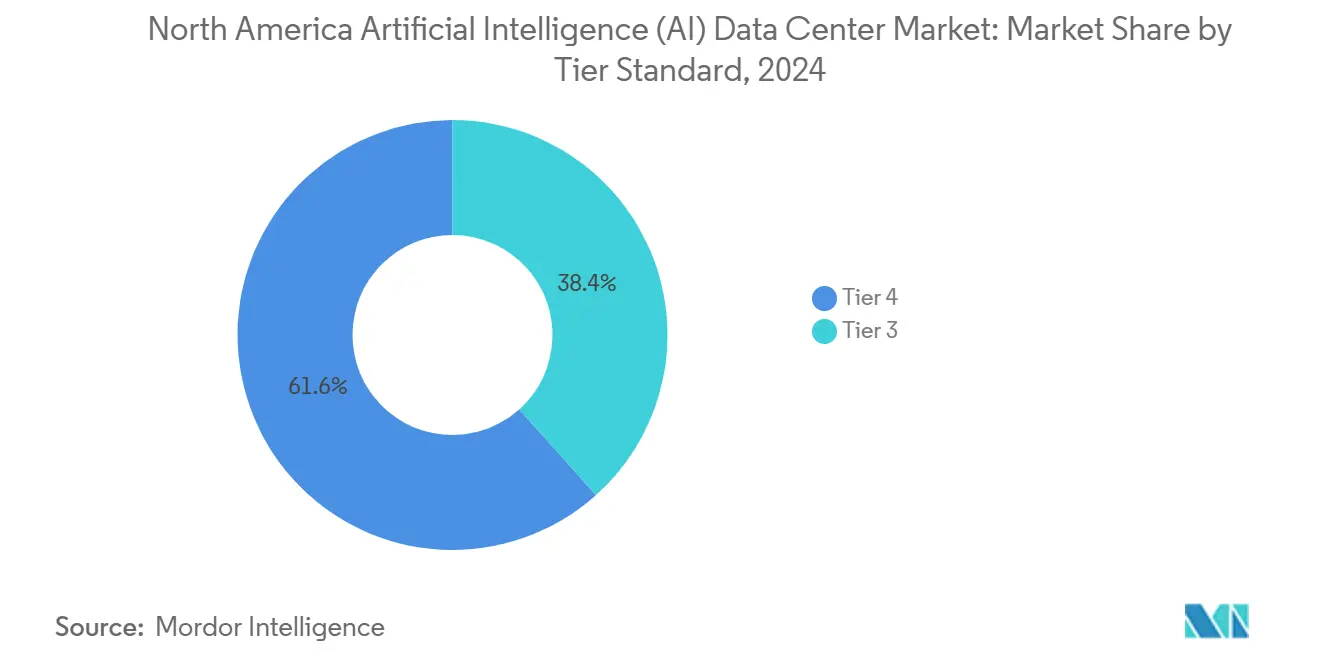

- By tier standard, Tier IV sites held 61.63% share of the North America artificial intelligence data center market in 2024 as Tier III complexes advance at a 32.89% CAGR to 2030.

- By end-user industry, IT and IT services captured 33.82% market share in 2024 in the North America artificial intelligence data center market, whereas internet and digital media workloads are poised for a 31.45% CAGR during the forecast horizon.

- By geography, the United States occupied 94.71% market share in 2024 in the North America artificial intelligence data center market; Canada is projected to climb at a 33.91% CAGR through 2030.

North america participates in a competitive field that extends beyond its own borders. The market landscape in the global artificial intelligence (ai) data center industry outlined by Mordor Intelligence covers that wider structure.

North America Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Generative-AI GPU Cluster Build-outs by U.S. Hyperscalers | +8.5% | United States, spill-over to Canada | Medium term (2-4 years) |

| U.S. CHIPS Act Incentives Accelerating Domestic AI-Chip Supply Chain | +6.2% | United States primarily | Long term (≥ 4 years) |

| Rapid Uptake of Liquid and Immersion Cooling Across Canadian Colocation Halls | +4.8% | Canada, expanding to Northern U.S. | Short term (≤ 2 years) |

| Corporate Net-Zero Mandates Driving Green-Power PPAs for AI Data Centers | +5.1% | Global, concentrated in California, Texas, Virginia | Medium term (2-4 years) |

| AI-Optimised Edge Deployments Supporting 5G and Autonomous-Vehicle Roll-outs | +3.7% | Urban centers across North America | Long term (≥ 4 years) |

| State-Level Tax Exemptions (Virginia, Texas) Reducing TCO for AI Facilities | +2.2% | Virginia, Texas, expanding to other states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Generative-AI GPU Cluster Build-outs by U.S. Hyperscalers

Hyperscaler deployment scales are unprecedented, with one facility alone integrating 100,000 NVIDIA H100 GPUs for xAI and Meta targeting an aggregate 350,000-GPU footprint across its domestic campuses. These builds draw more than 100 MW per site, resetting baseline engineering requirements for power delivery, backup generation, and substation proximity. Microsoft’s USD 10 billion renewable-energy arrangement with Brookfield underlines the parallel need for long-duration clean-power sourcing. Utility-interconnection negotiations have become board-level priorities as localized load spikes strain aging grids. New grid-stability protocols are emerging because AI training cycles present sustained, high-load curves that differ from transient cloud traffic patterns. The North America artificial intelligence data center market therefore benefits from both infrastructure CAPEX and a broad set of ancillary services aimed at grid integration compliance.

U.S. CHIPS Act Incentives Accelerating Domestic AI-Chip Supply Chain

Intel’s Ohio fabs secured USD 8.5 billion in federal incentives to fabricate AI accelerators by 2027, cutting the GPU lead-time bottleneck that historically delayed projects by up to 12 months. Complementary advanced-packaging plants in Arizona and Texas are enabling on-shore high-bandwidth memory attachment crucial for modern AI silicon. Export-control stipulations favor domestic purchasers, delivering a competitive edge to U.S. operators in the North America artificial intelligence data center market. University consortia funded under the Act are fast-tracking next-generation chip research, signaling further performance jumps that data center blueprints must accommodate. Vertical integration across foundry, packaging, and system integration is therefore shrinking deployment cycles and lowering supply-chain risk for hyperscalers and colocation vendors alike.

Rapid Uptake of Liquid and Immersion Cooling Across Canadian Colocation Halls

Canadian colocation providers now deploy liquid cooling in 70% of AI-ready halls, pushing power usage effectiveness (PUE) down to 1.05–1.10 versus 1.40–1.60 for legacy air-cooled rooms. Rack densities exceeding 100 kW enable higher revenue per square foot, especially valuable in Toronto, Montreal, and Vancouver where real-estate costs trend above regional averages. GPU roadmaps from NVIDIA and AMD increasingly assume direct-to-chip or immersion cooling interfaces, making Canadian operators early beneficiaries of the hardware transition. Provincial carbon-pricing mechanisms further tip return-on-investment calculations toward efficient cooling retrofits. These advantages position Canada as both a pressure-release valve for congested U.S. hubs and as a proving ground for liquid-cooling supply-chain specialization within the broader North America artificial intelligence data center market.

Corporate Net-Zero Mandates Driving Green-Power PPAs for AI Data Centers

Corporations have locked in more than USD 15 billion worth of renewable-energy PPAs dedicated to AI data centers, enabling predictable energy costs and compliance with ESG scorecards. Microsoft alone holds a 10.5 GW pipeline, while Amazon’s 8.5 GW portfolio integrates dedicated solar-plus-storage assets co-located with its AI campuses. Battery-energy-storage systems are mitigating intermittency, allowing GPU clusters to run at full utilization even during curtailment periods. Carbon-offset methodologies tailored to AI workload intensity are generating incremental revenue through surplus credit sales. Consequently, PPA availability and renewable portfolio depth are emerging as new site-selection screeners in the North America artificial intelligence data center market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Congestion and Power-Allocation Moratoria in Core DC Hubs | -4.3% | Northern Virginia, Silicon Valley, Chicago | Short term (≤ 2 years) |

| Shortage of Skilled Workforce for High-Density AI Operations | -2.8% | North America wide, acute in rural areas | Medium term (2-4 years) |

| High CAPEX of Liquid-Cooling Retrofits for Legacy Facilities | -2.1% | United States legacy facilities, urban markets | Short term (≤ 2 years) |

| Data-Residency Regulations Constraining Cross-Border AI Workload Migration | -1.4% | US-Canada border regions, government sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion and Power-Allocation Moratoria in Core DC Hubs

Dominion Energy’s interconnection queue now tops 40 GW, tripling since 2023 and delaying more than 2 GW of planned capacity in Northern Virginia. California has capped summer peak-hour data-center connections, limiting AI training during high-load months and pushing operators to distribute clusters geographically. PJM’s requirement for extensive grid-stability studies adds 12-18 months to project timelines for facilities above 100 MW. Developers are revisiting on-site generation via gas turbines and fuel cells to de-risk grid dependency, though doing so raises capital intensity and carbon accounting complexity. These constraints tighten supply just as GPU demand accelerates, elevating pricing power for operational assets in the North America artificial intelligence data center market.

Shortage of Skilled Workforce for High-Density AI Operations

Liquid-cooling, high-frequency power delivery, and GPU cluster orchestration skills remain scarce, affecting 60% of announced AI facilities. Salary premiums of 25–40% are common, and rural campuses must layer housing stipends onto compensation packages to attract talent. Only 15% of U.S. electrical-engineering programs include immersive-cooling coursework, extending hiring timelines and increasing reliance on specialized contractors. Certification bodies are racing to standardize curricula, but near-term fulfillment gaps persist. These labor shortages can delay ramp-up schedules and compress margins, acting as a drag on the otherwise rapid expansion of the North America artificial intelligence data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Providers Lead Scale; Colocation Captures Momentum

Cloud platforms commanded 55.82% of 2024 revenue after deploying region-wide GPU clusters that smaller enterprises cannot finance. Amazon Web Services and Microsoft Azure each announced dedicated AI regions with integrated high-density power skids, reinforcing the dominance of hyperscalers in the North America artificial intelligence data center market size. Colocation, however, is slated to grow at a 32.56% CAGR as enterprises pivot toward hybrid strategies that balance control with elasticity. Equinix now offers AI-configured cages in 15 metros, and Digital Realty’s NVIDIA alliance supplies turnkey clusters that shrink deployment cycles to weeks rather than months. Hybrid models also satisfy data-sovereignty mandates and latency-sensitive workflow placement, positioning colocation as the agility layer in the wider ecosystem.

Edge and enterprise self-builds remain comparatively small today but are rising alongside 5G-enabled services such as smart-manufacturing analytics and autonomous mobile-robot coordination. CoreSite’s 100 kW rack option lowers the entry threshold for mid-tier enterprises, while modular container designs support suburban micro-campuses where zoning is favorable. Over time, these distributed nodes can interconnect to form federated computational meshes, amplifying addressable demand across the North America artificial intelligence data center market.

By Component: Hardware Acceleration Surges Ahead of Software Maturity

Software retained 45.83% share in 2024, reflecting long-standing adoption of frameworks such as TensorFlow and PyTorch. Yet hardware is accelerating at a 31.78% CAGR as GPU spending eclipses all other line items in the North America artificial intelligence data center market share for capital allocation. Power infrastructure upgrades lead the spend, with high-density busways and 415 V distribution becoming standard. Cooling budgets follow closely, particularly for immersion systems that unlock triple-digit rack-kilowatt densities.

GPU-optimized servers now bundle AI-specific network topologies like NVIDIA NVLink to overcome inter-GPU latency bottlenecks, further intensifying capital requirements. Managed services for operations and consulting services for architecture design round out the component mix, but their growth trajectory remains secondary to physical infrastructure investment. Once hardware bottlenecks ease, software-centric optimization tools are expected to reclaim spending share, nudging the North America artificial intelligence data center industry toward a more balanced profile.

By Tier Standard: Tier IV Dominates; Tier III Accelerates

Tier IV complexes accounted for 61.63% revenue in 2024 as multi-day model-training jobs could not tolerate unscheduled downtime. Fault-tolerant electrical and mechanical paths justify the premium when a failed run can cost millions in GPU-hour wastage. However, improved checkpoint-restart capabilities and higher GPU reliability are allowing Tier III builds to satisfy many inference and short-cycle training workflows, prompting a 32.89% CAGR for this category through 2030.

The North America artificial intelligence data center market size for Tier III deployments grows fastest in sectors such as media content generation and financial-risk modeling, where application-level redundancy can absorb occasional site-level outages. Uptime Institute has adapted its standards to include liquid-cooling redundancy and GPU pool recoverability metrics, narrowing the perceived reliability gap between tiers. Cost-sensitive enterprises consequently balance CAPEX with risk appetite, creating a more diversified pipeline of facility types across the region.

By End-user Industry: IT Services Retain Lead; Digital Media Escalates

IT and IT-services firms held 33.82% of 2024 spending after harnessing the North America artificial intelligence data center market for software-development productivity gains and AI-enabled outsourcing platforms. System integrators bundle GPU cycles with consulting engagements, locking in long-term contracts that stabilize utilization rates. Meanwhile, internet and digital-media operators, streaming platforms, social-media networks, and gaming studios, are on pace for a 31.45% CAGR through 2030 as generative-AI engines personalize content, moderate user posts, and automate asset creation.

Financial-services institutions deepen investment for fraud detection and high-frequency trading, favoring colocation sites near exchange peering points. Healthcare and life-sciences researchers expand usage for diagnostic imaging and protein-folding simulations, leveraging purpose-built GPU clusters validated under HIPAA-compliant architectures. Manufacturing adopts edge AI for predictive maintenance, while public-sector agencies pilot AI ecosystems for cybersecurity and defense analytics. Across industries, workload diversity underscores the long-run elasticity of the North America artificial intelligence data center market.

Geography Analysis

The United States dominated the North America artificial intelligence data center market with 94.71% share in 2024 thanks to hyperscalers headquartered in Washington, California, and Texas, entrenched fiber routes in Northern Virginia, and state incentives that drop total cost of ownership by as much as 20%. Virginia’s Loudoun County continues to anchor multi-GW plans, although grid moratoria are nudging expansions toward Texas, Ohio, and Iowa where land and power are more readily available. California’s focus has shifted to edge-centric clusters that feed autonomous-vehicle and cinematic-rendering workloads; despite higher electricity costs, proximity to innovation hubs outweighs expense for latency-sensitive tenants.

Canada is the region’s fastest-growing submarket at a 33.91% CAGR, propelled by CAD 2.4 billion (USD 1.75 billion) in federal AI funding and abundant hydroelectric supply in Quebec that supports aggressive decarbonization targets. Montreal’s chilled-air climate augments liquid-cooling efficiency, attracting global AI start-ups seeking low-carbon compute capacity. Ontario leverages cross-border fiber and a dense financial-services customer base to justify new AI-ready halls in Toronto’s data-center corridor. Western provinces provide renewable-energy-credit advantages that resonate with multinational sustainability scorecards, adding depth to Canada’s attractiveness within the North America artificial intelligence data center market size.

Cross-border data-residency rules are shaping competitive positioning: Canadian-domiciled providers like eStruxture capture healthcare and government workloads requiring local storage, while U.S. operators form joint ventures to meet provincial sovereignty requirements. The region’s overall expansion is therefore not a zero-sum equation but a balanced redistribution of capacity that mitigates U.S. grid bottlenecks while enabling Canadian provinces to monetize clean-power endowments.

Mordor Intelligence provides coverage of the artificial intelligence (ai) data center market across other key regional markets, including South America, Europe, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, Canada, Netherlands, Germany, Chile, and France incorporating local coverage and market participation, as required.

Competitive Landscape

The North America artificial intelligence data center market shows moderate concentration: the five largest operators command roughly 45% of installed capacity, yet aggressive capacity roadmaps reduce the likelihood of any single player exceeding 25% share over the next five years. Amazon Web Services, Microsoft Azure, and Google Cloud combine infrastructure control with AI platform integration, creating ecosystem lock-in that smaller rivals counter through open-standards collaborations and multicloud on-ramps. Colocation majors like Equinix and Digital Realty specialize in vendor-neutral AI cages and liquid-cooling corridors, partnering with NVIDIA to simplify enterprise onboarding.

Emerging operators differentiate through immersion-cooling specialization, modular prefabricated halls, and low-latency edge locations adjacent to telco central offices. Chip vendors are pivotal kingmakers: NVIDIA’s preferred-partner program grants early GPU allocation to select data-center builders, while Intel’s foundry push aims to shorten lead times and shift competitive leverage. Sustainability credentials are another competitive axis; operators with deep renewable PPA portfolios win hyperscaler outsourcing mandates and ESG-tied financing.

Mergers and acquisitions target software and orchestration layers, as illustrated by NVIDIA’s Run:ai purchase, which embeds scheduling intelligence at the infrastructure stack’s core. Facility expansions are increasingly joint-ventures between capital providers and technology partners, distributing risk while securing long-duration power contracts. Regulatory proficiency, covering export controls, tax-rebate compliance, and data-localization mandates, rounds out the competitive capabilities matrix shaping the North America artificial intelligence data center market.

North America Artificial Intelligence (AI) Data Center Industry Leaders

ABB Ltd.

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Arm Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Amazon Web Services earmarked USD 150 billion for new AI regions in Ohio, Oregon, and Virginia that include purpose-built liquid-cooling and 415 V power distribution.

- August 2025: NVIDIA closed its USD 700 million acquisition of Run:ai to integrate Kubernetes-native orchestration into its DGX platform suite.

- July 2025: Equinix launched its largest AI-ready hall in Ashburn, Virginia, with 48 MW of capacity and direct cloud-exchange links.

- June 2025: Intel committed USD 25 billion to expand Ohio fabs that will supply 40% of regional AI-accelerator demand by 2027.

North America Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and IT Services |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| United States |

| Canada |

| Mexico |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and IT Services | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current value of the North America artificial intelligence data center market?

The market is valued at USD 9.45 billion in 2025 and is projected to reach USD 35.11 billion by 2030.

Which data center type is growing fastest in the region?

Colocation facilities are registering a 32.56% CAGR through 2030 as enterprises favor hybrid AI deployments.

Why is Canada attracting AI data center investment?

Abundant hydroelectric power, clean-energy mandates, and CAD 2.4 billion in federal AI funding are propelling Canada’s 33.91% CAGR.

How is the CHIPS Act influencing AI infrastructure?

The Act’s USD 52 billion incentive package accelerates domestic AI-chip production, reducing supply-chain risk and deployment timelines.

What cooling technology trend is reshaping facility design?

Liquid and immersion cooling is lowering PUE to near-1.05 levels and enabling rack densities above 100 kW, particularly in Canadian halls.

Page last updated on: