Antibiotic Resistance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

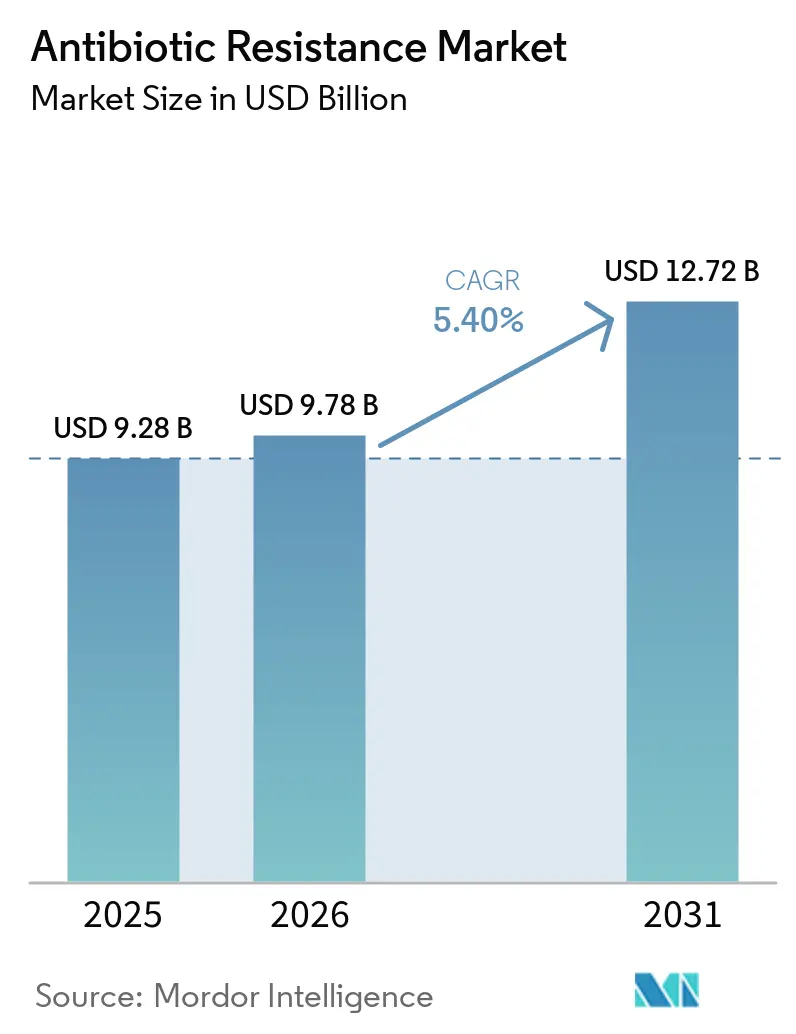

| Market Size (2026) | USD 9.78 Billion |

| Market Size (2031) | USD 12.72 Billion |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

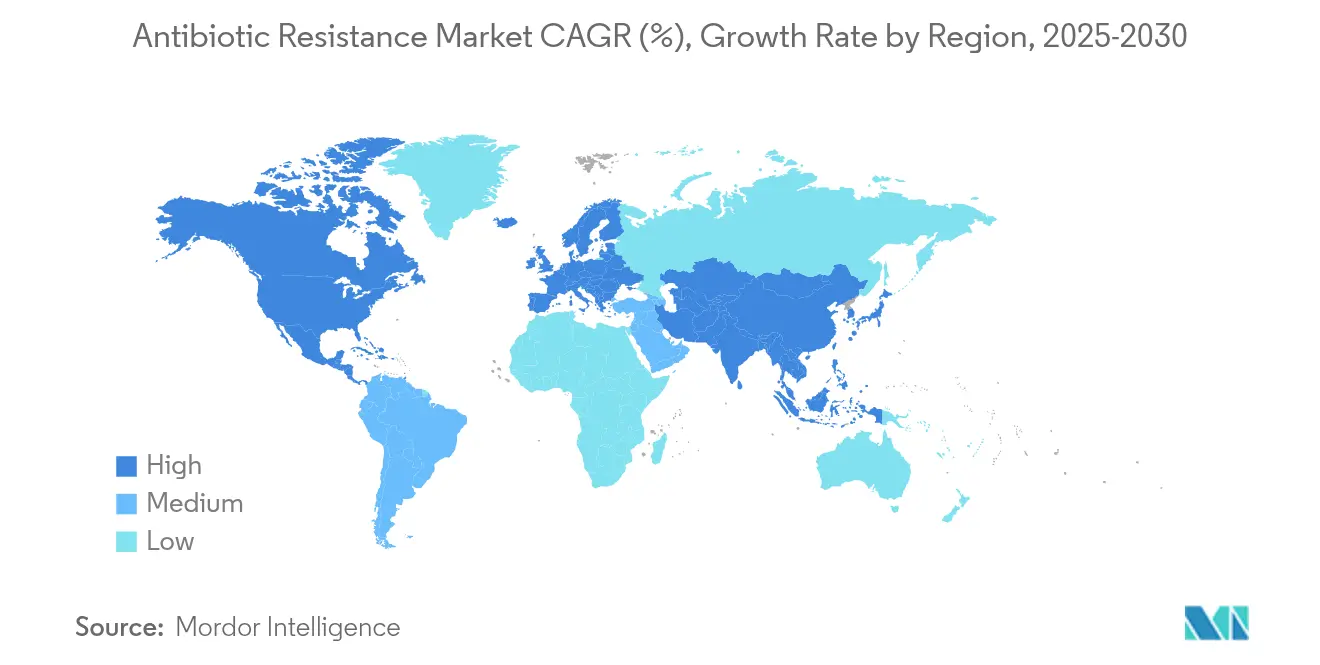

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibiotic Resistance Market Analysis by Mordor Intelligence

The antibiotic resistance market size in 2026 is estimated at USD 9.78 billion, growing from 2025 value of USD 9.28 billion with 2031 projections showing USD 12.72 billion, growing at 5.40% CAGR over 2026-2031. Rising morbidity, mounting economic losses, and renewed public-private funding are the primary forces sustaining this trajectory. Accelerating hospital stewardship mandates, expedited regulatory incentives, and AI-enabled discovery platforms are widening the clinical toolbox. Yet, persistent supply-chain fragility and an unfavorable cost-to-return profile continue to temper investment appetite. Asia Pacific retains a commanding lead, bolstered by high infection burdens and steady infrastructure upgrades, while South America’s rapid expansion signals changing market gravity. Competitive dynamics reveal a gradually tightening field in which large pharmaceutical companies spearhead late-stage launches and specialized biotech firms supply the innovation pipeline.

Key Report Takeaways

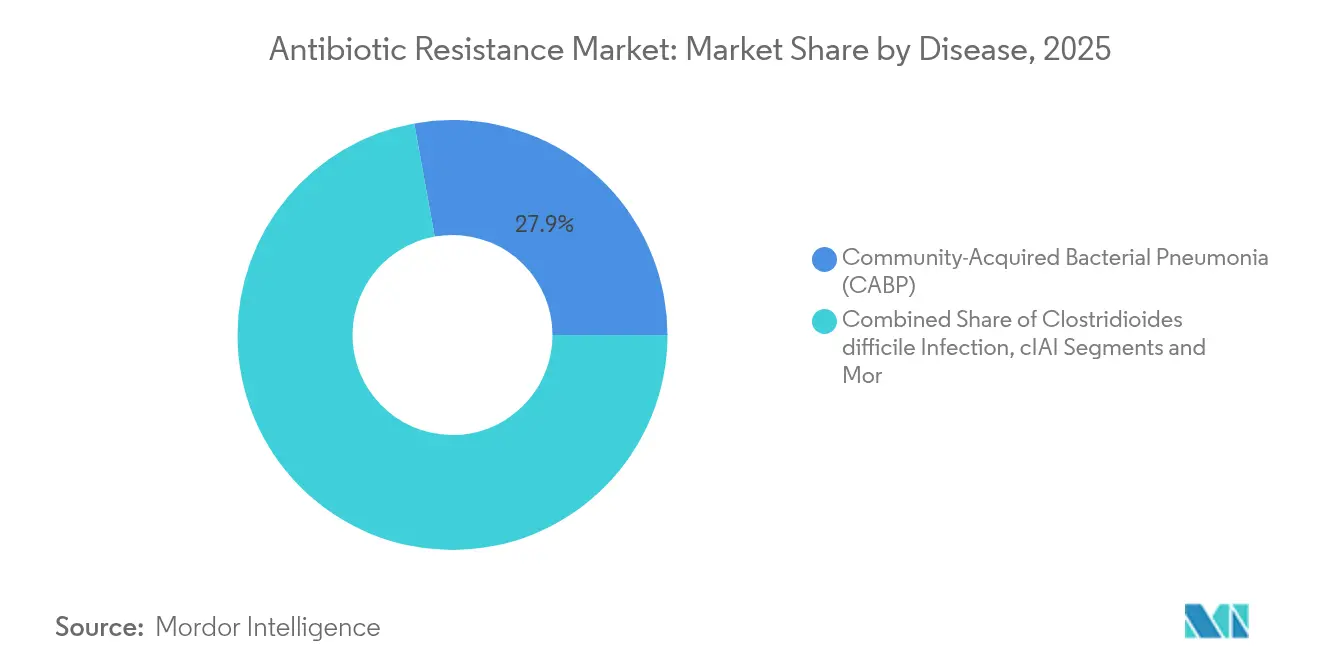

- By disease, pneumonia accounted for 27.85% of the antibiotic resistance market size in 2025, while hospital-acquired and ventilator-associated pneumonias (HABP/VABP) are forecast to expand at an 8.55% CAGR to 2031.

- By pathogen, MRSA held a 22.14% share of the antibiotic resistance market in 2025; P. aeruginosa is advancing at a 9.28% CAGR through 2031.

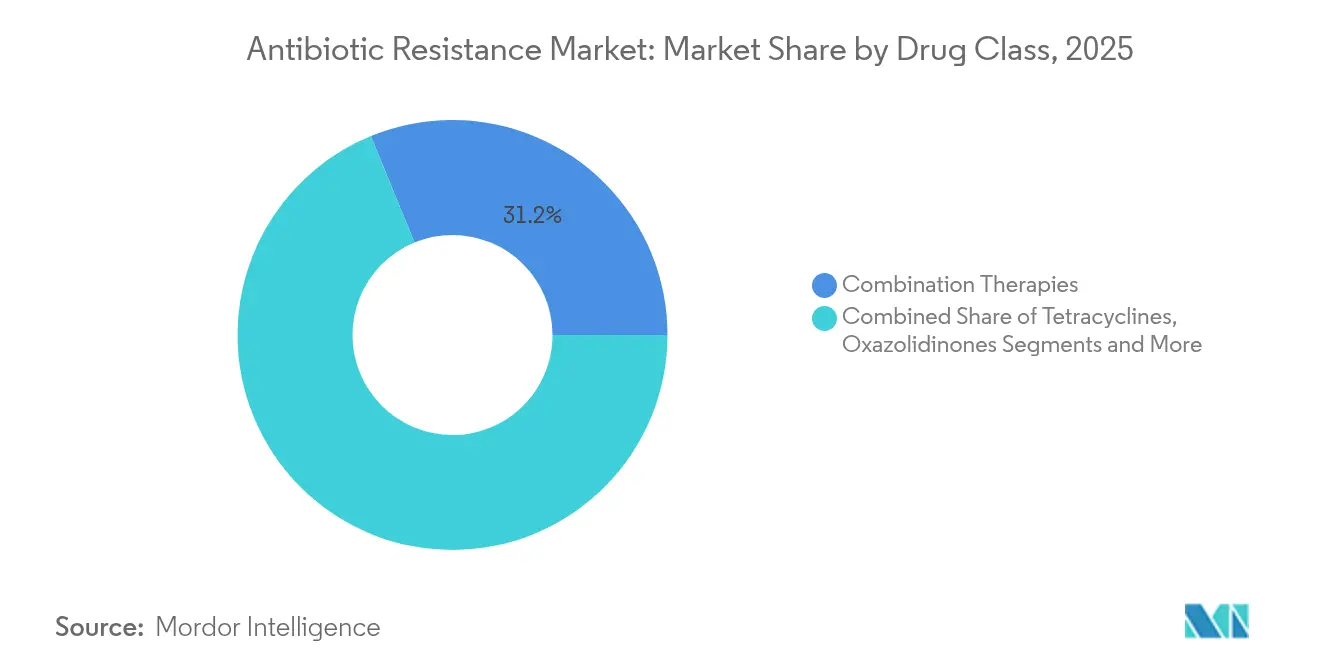

- By drug class, β-lactam & β-lactamase inhibitor combinations captured 31.20% revenue share in 2025; lipoglycopeptides post the highest 10.95% CAGR to 2031.

- By mechanism, cell-wall inhibitors controlled a 35.95% share in 2025, while RNA-synthesis inhibitors display the strongest 9.78% CAGR outlook.

- By distribution channel, hospital pharmacies held 57.55% of sales in 2025; online pharmacies recorded the fastest 13.95% CAGR to 2031.

- Geographically, Asia Pacific led with 46.50% antibiotic resistance market share in 2025, whereas South America is set to post the fastest 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antibiotic Resistance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High burden of antibiotic-resistant infections | +1.80% | Global; highest in APAC & MEA | Medium term (2-4 years) |

| Escalating global AMR funding initiatives | +1.20% | North America & Europe | Long term (≥ 4 years) |

| Expedited regulatory incentives for priority antibiotics | +0.90% | North America & EU | Short term (≤ 2 years) |

| Hospital stewardship mandates boosting novel uptake | +0.70% | Global; early adoption in developed markets | Medium term (2-4 years) |

| AI/ML-based ultra-rapid compound discovery | +0.60% | North America & Europe | Long term (≥ 4 years) |

| Nanoparticle-enabled targeted delivery vs. biofilms | +0.40% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Burden of Antibiotic-Resistant Infections

Antimicrobial resistance caused 4.71 million deaths in 2021 and threatens to reach 10 million annually by 2050 unless decisive action is taken.[1]CARB-X, “Portfolio milestones,” carb-x.org Surveillance indicates plateauing resistance in many European states, yet low- and middle-income countries continue to see rising rates due to weak monitoring and limited access to new antibiotics. The economic drag could total USD 855 billion in annual losses by 2030, intensifying payer interest in value-based procurement. Demand, therefore, concentrates on agents that align with WHO priority-pathogen guidance and preserve future treatment options. Hospitals are increasingly favoring narrow-spectrum or pathogen-targeted products that mitigate collateral resistance. This environment sustains long-run uptake of novel therapies and keeps the antibiotic resistance market on a steady growth arc.

Escalating Global AMR Funding Initiatives

More than USD 500 million has flowed into CARB-X, backing 100+ early-stage projects worldwide.[2]U.S. Food and Drug Administration, “QIDP approvals,” fda.gov The UK’s subscription purchase model, launched in August 2024, decouples developer revenue from volume and offers a reproducible template for other payers. Corporate pledges are rising, exemplified by GSK’s GBP 45 million (USD 61 million) commitment to the Fleming Initiative and Eli Lilly’s USD 100 million injection into the AMR Action Fund. Blended finance vehicles, social-impact bonds, and BARDA’s decade-long USD 300 million earmark collectively reduce the funding cliff that once stymied late-stage programs. Together, these mechanisms strengthen the pipeline and improve visibility for investors weighing entry into the antibiotic resistance industry.

Expedited Regulatory Incentives for Priority Antibiotics

The FDA’s QIDP pathway grants five-year exclusivity extensions, Fast Track interactions, and rolling reviews, promptly demonstrated by 2024-2025 approvals such as Emblaveo and Blujepa.[3]University of Queensland, “Global burden of AMR,” uq.edu.au EMA’s PRIME scheme now mirrors these advantages, harmonizing transatlantic processes and cutting duplicative workload. Small and midsize firms have capitalized, advancing assets like ibezapolstat into pivotal trials with reduced capital outlay. Adaptive designs and real-world evidence acceptance shorten timelines without diluting safety oversight. These aligned incentives make the antibiotic resistance market more accessible to specialized developers.

Hospital Stewardship Mandates Boosting Novel Uptake

CDC Core Elements became mandatory in 2024, linking stewardship compliance to Medicare reimbursement. Evidence shows mature programs can trim inappropriate antibiotic use by 28.4% while maintaining clinical outcomes. Nations such as Iran achieved 22.24% reductions in restricted antibiotic consumption following nationwide mandates. Hospitals are therefore rewarding agents with tight spectra, favorable microbiome profiles, and rapid susceptibility information. Integration into electronic health records further differentiates products that fit stewardship algorithms, guiding formulary decisions toward premium-priced, resistance-savvy molecules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Clinical Safety & Superiority Requirements | -0.80% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Unfavourable Cost-To-Return Profile For Big-Pharma | -1.10% | Global, particularly affecting developed markets | Long term (≥ 4 years) |

| Slow Reimbursement Of Rapid Diagnostics | -0.60% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Fragile API Fermentation Supply Chains | -0.90% | Global, with concentration risk in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Clinical Safety & Superiority Requirements

Regulators increasingly require superiority over legacy comparators, inflating trial sizes, timelines, and budgets. Complete Response Letters, such as the one issued for cefepime-taniborbactam, underscore the heightened bar. Enrollment proves difficult when target patients are critically ill yet scarce, forcing complex global studies that challenge smaller sponsors. Real-world evidence is slowly gaining acceptance but remains uneven across jurisdictions, prolonging the route to market for many candidates and tempering the growth rate of the antibiotic resistance market.

Unfavourable Cost-to-Return Profile for Big-Pharma

Peak sales rarely top USD 1 billion because stewardship limits usage and generics shorten exclusivity windows. Development outlays may exceed USD 1.5 billion when failures are included, eroding ROI and driving exits by major companies. Over 3,000 pharmaceutical M&A deals during 2010-2023 have consolidated know-how, heightening the risk of shortages when any one plant falters. Subscription models and advance purchase commitments are gaining traction but remain insufficient to correct the market failure fully. This structural imbalance continues to deter mainstream capital from scaling the antibiotic resistance industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: HABP/VABP Drives Critical Care Innovation

Community-Acquired Bacterial Pneumonia (CABP) retained 27.85% of 2025 revenue, underlining its ubiquitous burden across community and hospital settings. Within this spectrum, HABP/VABP exhibits the fastest 8.55% CAGR, fueled by prolonged ICU ventilation and the density of multidrug-resistant organisms in critical care wards. During 2025, the antibiotic resistance market size for HABP/VABP is set to widen further as clinicians gravitate toward pathogen-targeted combinations able to navigate complex resistance phenotypes.

Pipeline progress illustrates the trend. Aztreonam/avibactam won FDA clearance for cIAI yet shows cross-utility in high-risk pulmonary infections, while adaptive designs are enabling expedited HABP/VABP approvals. CDI advances such as ibezapolstat point to parallel momentum in severe colitis, reinforcing breadth across infection sites. Outpatient-oriented ABSSSI products like lipoglycopeptides sustain growth in ambulatory care, giving manufacturers multiple entry points into the antibiotic resistance market.

By Pathogen: Gram-Negative Threats Accelerate

MRSA kept its 22.14% share in 2025, but growth is shifting toward Gram-negative challenges. P. aeruginosa’s projected 9.28% CAGR exemplifies this pull, driven by intrinsic resistance traits and biofilm proficiency that complicate device-associated infections. Carbapenem-resistant A. baumannii is likewise climbing, with Phase 3 trials for zosurabalpin targeting this WHO-listed urgent threat.

E. coli maintains relevance through rising ESBL prevalence, while surveillance from China flags alarming gains in carbapenem-resistant K. pneumoniae. These data validate the pursuit of broad-spectrum combinations and encourage adaptive regimens leveraging rapid diagnostics. Consequently, pathogen-centric R&D underpins the steady evolution of the antibiotic resistance market.

By Drug Class: Lipoglycopeptides Lead Innovation

Combination therapies controlled 31.20% of 2025 revenue, supported by recent approvals and versatility across Gram-negative infections. Yet lipoglycopeptides headline innovation with an 10.95% CAGR as refinements overcome vancomycin limitations and enable single-dose outpatient regimens.

The antibiotic resistance market size for lipoglycopeptides is expected to climb as products like dalbavancin secure longer indications and reimbursement values reflect admission avoidance. Oxazolidinones and tetracyclines remain stable, while monobactam hybrids counter metallo-β-lactamases. Combination therapies that unite disparate modes of action gain traction, particularly where diagnostics confirm simultaneous mechanisms.

By Mechanism: RNA-Synthesis Inhibitors Gain Momentum

Cell-wall synthesis inhibitors hold 35.95% share, reflecting persistent β-lactam dominance. Conversely, RNA-synthesis inhibitors are projected to grow 9.78% annually, propelled by novel chemotypes such as lariocidin that sidestep existing resistance pathways.

These agents appeal to stewardship teams keen to diversify modes of action. The antibiotic resistance market share commanded by RNA-synthesis inhibitors is set to expand as companion diagnostics accelerate pathogen-mechanism matching and regulators champion mode-specific labeling. Downstream, emergent bacteriophage-derived endolysins suggest further mechanism diversification.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies will manage 57.55% of 2025 sales, aligning with the intravenous dominance of many late-stage therapies. However, online pharmacies will log a 13.95% CAGR due to telemedicine, enhanced cold-chain infrastructure, and a rising portfolio of oral products suitable for outpatient management.

Chain drugstores integrate stewardship modules and point-of-care diagnostics, strengthening their consultative role. Blockchain-enabled authentication mitigates counterfeit risk, particularly in regions where substandard products fuel resistance. Together, these trends blur traditional supply boundaries and enlarge the antibiotic resistance market's addressable base.

Geography Analysis

Asia Pacific generated 46.50% of global revenue in 2025, reflecting high infection prevalence, widening insurance coverage, and proactive governmental investment. Singapore advances rapid diagnostics and bacteriophage research, while Japan has revived domestic API production to buffer against overseas supply disruptions. China’s anti-espionage law raises procurement uncertainty, prompting multinationals to diversify sourcing and invest in redundancy.

North America combines sophisticated stewardship frameworks with strong funding pipelines. The FDA’s alignment with BARDA grants and QIDP incentives streamlines late-stage development, though the region remains vulnerable to ingredient shortages concentrated in India and China. Europe’s coordinated surveillance has stabilized resistance rates across 29 EEA countries, yet policymakers continue to debate manufacturing profitability versus environmental stewardship. The UK’s subscription model offers a potential corrective to the traditional volume-linked revenue barrier.

South America leads growth at 7.55% CAGR, driven by improved diagnostics, rising healthcare spend, and heightened awareness of resistance costs. Brazil’s antibiotic consumption climbed 30% from 2014-2019, signalling both stewardship gaps and commercial opportunity. The Middle East & Africa displays incremental progress, hampered by financing constraints but aided by multilateral grant programs aimed at laboratory capacity and supply-chain integrity. Together, these patterns underscore the global interconnectedness of the antibiotic resistance market.

Competitive Landscape

Market structure remains moderately fragmented, yet consolidation is advancing as scale becomes critical for late-stage trials and global distribution. GSK and Pfizer topped the 2021 Access to Medicine Foundation AMR benchmark, leveraging extensive surveillance networks and diversified pipelines. Their shared focus on AI-integrated discovery and post-approval stewardship tools sets a high bar for follow-on competitors.

Specialized biotech companies maintain innovative momentum. Acurx Pharmaceuticals rides positive ibezapolstat data toward pivotal trials, Iterum Therapeutics secured U.S. clearance for Orlynvah, and Qpex assets acquired by Shionogi complement an advanced Gram-negative portfolio. Partnership models—public-private, blended finance, and big-pharma buy-ins—shape an ecosystem in which resource-sharing offsets risk.

Technological differentiation now extends beyond chemistry. Firms able to embed susceptibility readouts into prescribing software, streamline API manufacturing for geopolitical resilience, and demonstrate minimal environmental discharge stand to gain formulary priority. Within this context, the antibiotic resistance market continues to attract mission-driven capital even as purely commercial investors remain cautious.

Antibiotic Resistance Industry Leaders

AbbVie

Merck & Co. Inc.

Pfizer Inc

Novartis AG

Basilea Pharmaceutica Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: University of Vienna and Helmholtz Institute teams identified saarvienin A, a potent glycopeptide active against vancomycin-resistant Enterococcus and MRSA, with optimization underway.

- March 2025: FDA cleared GSK’s Blujepa (gepotidacin) for uncomplicated UTIs, the first new oral class for this infection in nearly 30 years.

- March 2025: McMaster University revealed lariocidin, a novel antibiotic that targets bacterial transcription with no cross-resistance to existing classes.

- February 2025: AbbVie gained FDA approval for Emblaveo (aztreonam/avibactam) for complicated intra-abdominal infections.

- January 2025: Acurx Pharmaceuticals secured favorable EMA feedback for ibezapolstat Phase 3 trials in C. difficile infection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the antibiotic-resistance therapeutics market as all branded and generic systemic antibacterials that are indicated, labeled, or routinely used for infections caused by multi-drug-resistant pathogens across hospital and community settings.

Scope Exclusion: Preventive vaccines, rapid diagnostic kits, antivirals, and veterinary-only formulations lie outside this scope.

Segmentation Overview

- By Disease

- Clostridioides difficile Infection (CDI)

- Complicated Intra-Abdominal Infection (cIAI)

- Acute Bacterial Skin & Skin-Structure Infections (ABSSSI)

- Hospital- & Ventilator-Acquired Pneumonias (HABP/VABP)

- Complicated Urinary Tract Infection (cUTI)

- Community-Acquired Bacterial Pneumonia (CABP)

- Bloodstream Infection (BSI)

- By Pathogen

- Acinetobacter baumannii

- Staphylococcus aureus (incl. MRSA)

- Pseudomonas aeruginosa

- Haemophilus influenzae

- Escherichia coli

- Other Priority Pathogens

- By Drug Class

- Tetracyclines

- Oxazolidinones

- Cephalosporins

- Lipoglycopeptides

- Combination Therapies

- Other Classes

- By Mechanism of Action

- Cell-Wall Synthesis Inhibitors

- Protein-Synthesis Inhibitors

- DNA-Synthesis Inhibitors

- RNA-Synthesis Inhibitors

- Other Mechanisms

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with infectious-disease pharmacists, ICU clinicians, procurement managers, and public-health officials across North America, Europe, and Asia-Pacific. These discussions clarified formulary shifts, emerging combination-therapy uptake, and realistic ASP erosion, allowing us to fine-tune assumptions flagged during desk work.

Desk Research

We began with open surveillance data from WHO-GLASS, CDC AR Threats, and ECDC EARS-Net, intertwined with trade volumes from UN Comtrade, patent trends through Questel, and peer-reviewed utilization studies in The Lancet Infectious Diseases. Annual reports, SEC 10-Ks, and D&B Hoovers financials added channel-level revenue and average selling price (ASP) granularity.

Regulatory logs (FDA QIDP, EMA PRIME), reimbursement tariff lists, and national stewardship budgets supplied launch timing and treatment-rate signals. The sources named here are illustrative; many additional public and paid repositories informed, validated, and, where needed, corrected our datasets.

Market-Sizing & Forecasting

A top-down incidence-to-treatment-pool model converts resistant infection cases, average therapy days, and adherence rates into demand volumes, which are then cross-checked against sampled supplier sales (bottom-up) to reconcile totals. Key variables include MRSA and CRE prevalence, days-of-therapy per admission, pipeline launch cadence, stewardship penalty trajectories, and currency-adjusted ASP trends. Multivariate regression projects each driver to 2030, while scenario analysis stress-tests rapid uptake of pipeline agents. Any data gaps in supplier roll-ups are bridged with calibrated penetration benchmarks.

Data Validation & Update Cycle

Outputs pass anomaly filters, variance checks against sentinel metrics, and peer review by a second analyst team before sign-off. We refresh the model annually and issue interim revisions when major regulatory, pricing, or outbreak events materially move the baseline.

Why Mordor's Antibiotic Resistance Baseline Stands Firm

Published estimates often diverge because firms mix distinct disease baskets, apply list versus net prices, or lock exchange rates at different points.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.28 B (2025) | Mordor Intelligence | - |

| USD 9.17 B (2024) | Global Consultancy A | Excludes post-2023 combination therapies; FX fixed to 2021 averages |

| USD 8.20 B (2022) | Industry Journal B | Captures only hospital-pharmacy sales and applies a uniform 10 % price discount |

The comparison shows that when scope clarity, pricing realism, and timely refresh are aligned, as in Mordor's approach, decision-makers receive a balanced, transparent baseline rooted in traceable variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the antibiotic resistance market?

The antibiotic resistance market is valued at USD 9.78 billion in 2026 and is projected to reach USD 12.72 billion by 2031, registering a 5.40% CAGR over 2026-2031.

Which region dominates global revenue?

Asia Pacific generated 46.50% of global revenue in 2025 thanks to high infection prevalence and expanding healthcare infrastructure.

Who are the key players in Antibiotic Resistance Market?

AbbVie, Merck & Co. Inc., Pfizer Inc, Novartis AG and Basilea Pharmaceutica Ltd. are the major companies operating in the Antibiotic Resistance Market.

Which disease segment shows the fastest growth?

Hospital-acquired and ventilator-associated pneumonias (HABP/VABP) lead with an 8.55% CAGR forecast through 2031.

What drug class is expanding most rapidly?

Lipoglycopeptides record the highest 10.95% CAGR as refinements overcome historical vancomycin resistance.

How are regulators encouraging antibiotic innovation?

Programs such as the FDA’s QIDP designation add five extra years of exclusivity, while the UK’s subscription payment model guarantees revenue independent of sales volume.

Why is AI important for future antibiotics?

AI platforms can cut discovery cycles from a decade to as little as three years, enabling faster identification of novel compounds effective against resistant pathogens.

Page last updated on: