Antibiotic Resistance Diagnosis Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 375.32 Million |

| Market Size (2030) | USD 486.58 Million |

| Growth Rate (2025 - 2030) | 5.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Antibiotic Resistance Diagnosis Devices Market Analysis by Mordor Intelligence

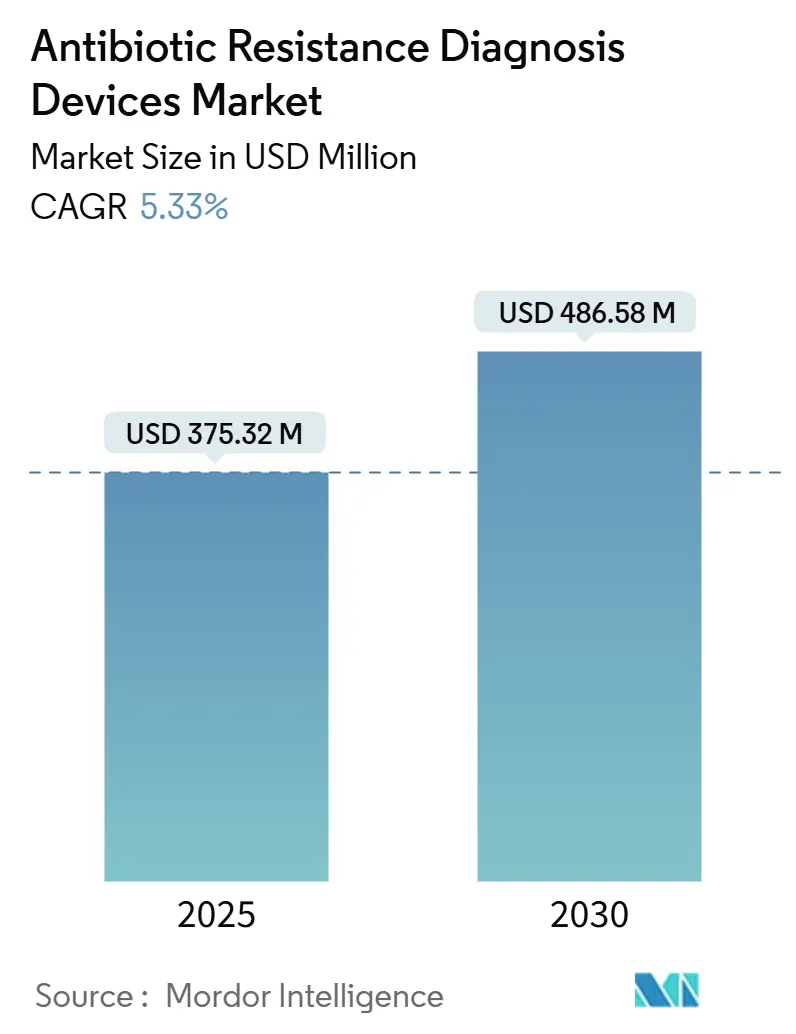

The Antibiotic Resistance Diagnosis Devices Market size is estimated at USD 375.32 million in 2025, and is expected to reach USD 486.58 million by 2030, at a CAGR of 5.33% during the forecast period (2025-2030).

Hospitals are switching from overnight culture workflows to same-shift molecular and mass-spectrometry solutions that compress antimicrobial-susceptibility-testing (AST) turnaround from 48 hours to under 6 hours, a shift reinforced by stewardship mandates that make diagnostic speed a regulatory requirement. Funding pipelines such as the U.S. CARB-X program and the European Horizon Europe framework are underwriting new installations, while AI-enabled MALDI-TOF analytics shorten time-to-AST and curb consumable use. Asia-Pacific procurement programs that favor locally assembled cartridge systems are widening global reach and lifting unit volumes, even though reimbursement gaps outside high-income countries restrain broader uptake. Competitive intensity is rising as cartridge makers bypass legacy distribution, forcing incumbents to protect installed bases with faster software upgrades and reagent-rental models.

Key Report Takeaways

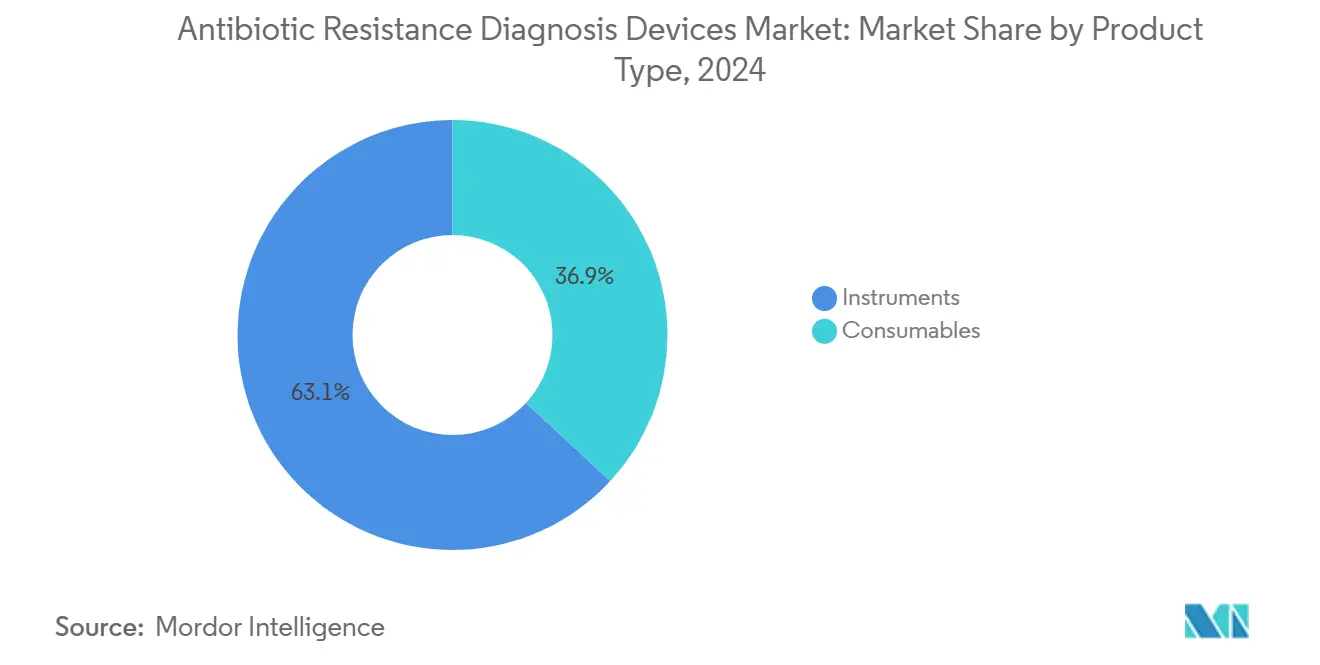

- By product type, instruments held a 63.12% share of the antibiotic resistance diagnosis devices market in 2024, whereas consumables are projected to grow at a 7.6% CAGR to 2030, outpacing the overall market by more than 2 percentage points.

- By technology, phenotypic AST accounted for 62.4% of the antibiotic resistance diagnosis devices market share in 2024, but rapid and point-of-care platforms are expected to expand at 14.8% through 2030.

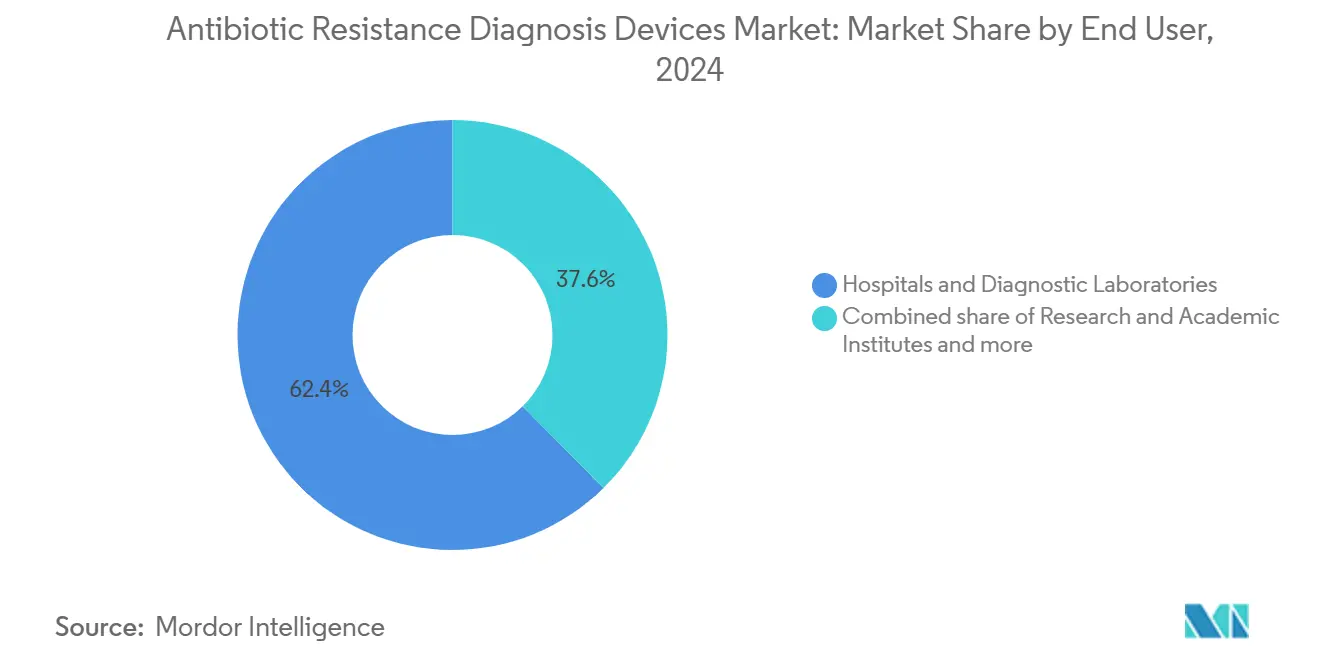

- By end user, hospitals and diagnostic laboratories contributed 62.4% of 2024 revenue, while pharmaceutical and biotechnology companies are adopting platforms at a 9.7% rate to accelerate drug-development timelines.

- By geography, North America commanded 41.5% of 2024 demand, yet Asia-Pacific is poised to register the fastest growth at 8.7% between 2025 and 2030.

Global Antibiotic Resistance Diagnosis Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of multidrug-resistant infections | +1.2% | Global, highest burden in South Asia and Sub-Saharan Africa | Medium term (2-4 years) |

| Government & multilateral funding for AMR diagnostics | +0.9% | North America, Europe, India, China | Long term (≥ 4 years) |

| Adoption of rapid molecular & POC platforms | +1.5% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Regulatory push for stewardship programs | +0.8% | North America, EU, Australia | Medium term (2-4 years) |

| AI-enabled MALDI-TOF spectral analytics | +0.6% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Decentralized cartridge manufacturing | +0.4% | India, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Multidrug-Resistant Infections

Hospitals are confronting WHO-listed priority pathogens such as carbapenem-resistant Acinetobacter baumannii and third-generation cephalosporin-resistant Enterobacterales, which now circulate widely in intensive-care units. One in 31 U.S. in-patients carried at least one healthcare-associated infection in 2024, a burden that amplifies empiric broad-spectrum prescribing [1]Centers for Disease Control and Prevention. "Core Elements of Hospital Antibiotic Stewardship Programs." Accessed November 24, 2025.. Rapid AST platforms delivering results inside 6 hours has significantly cut inappropriate antibiotic use in U.S. pilot studies. The U.S. Department of Health and Human Services allocated USD 500 million in 2024 for hospital-based AMR diagnostics, turning clinical urgency into funded demand. Similar multi-year programs in India, China, and the United Kingdom are channeling procurement toward modular cartridge systems that require limited cold-chain logistics. Together, these trends push the antibiotic resistance diagnosis devices market toward higher volumes of point-of-care and emergency-department placements.

Government & Multilateral Funding for AMR Surveillance and Diagnostics

The NIH devoted USD 703 million to AMR research in fiscal 2024, while India’s Department of Biotechnology rolled out 50 sentinel laboratories equipped with automated AST systems [2]Government of India, Department of Biotechnology. "AMR Surveillance and Research Network." 2024. The United Kingdom’s GBP 265 million Fleming Fund is steering contracts toward cartridge-based devices that can be deployed in resource-constrained settings. China’s National Health Commission mandated real-time AMR reporting from all tertiary hospitals in 2024, prompting networked-instrument orders. These public-sector channels act as forward-purchase agreements, dampening revenue cyclicality for suppliers and encouraging local component sourcing. Funding visibility also de-risks R&D investment in multiplex PCR and nanopore sequencing, sustaining pipeline momentum that supports the antibiotic resistance diagnosis devices market.

Adoption of Rapid Molecular & Point-of-Care Platforms in Hospitals

Cepheid’s GeneXpert processed is widely used for resistance-gene tests in 2024, while BD’s MAX platform crossed 1,200 U.S. installations after new FDA-cleared syndromic panels. Clinical data show that rapid molecular AST cuts time-to-appropriate therapy by 18 hours and trims 30-day sepsis mortality by 12% versus conventional culture. Emergency departments are embedding single-use cartridge instruments directly at triage desks, easing the staffing burden in centralized labs. For vendors, point-of-care adoption raises cartridge pull-through and expands the antibiotic resistance diagnosis devices market into outpatient clinics and ambulatory-surgery centers. Software links that upload results to electronic health records within minutes further solidify stewardship compliance metrics.

Regulatory Push for Antimicrobial Stewardship Programmes

CMS revised its Conditions of Participation in 2024 to require documented use of rapid diagnostics in stewardship workflows. The European Medicines Agency recommended that AST results be logged into national EHRs within 24 hours, compelling hospitals to replace manual disk-diffusion with automated or molecular platforms. Australia’s Therapeutic Goods Administration halved review timelines for six priority AST devices, echoing Japan’s decision to reimburse next-generation sequencing-based resistance testing. These policy shifts trigger replacement cycles across roughly 15,000 acute-care sites worldwide, converting optional upgrades into timetable-bound capital projects that enlarge the antibiotic resistance diagnosis devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating cost of automated AST systems | -0.7% | Global, acute in low- and middle-income countries | Short term (≤ 2 years) |

| Fragmented regulatory approval pathways | -0.5% | APAC and Latin America | Medium term (2-4 years) |

| Shortage of skilled clinical microbiologists | -0.4% | APAC, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Limited reimbursement outside high-income countries | -0.6% | APAC ex-Japan, Middle East, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Cost of Automated AST Systems

List-price for a fully configured Thermo Scientific Sensititre reaches USD 232,150, and annual service contracts push ownership costs even higher. Cartridge costs average USD 8–15 per run, dwarfing USD 2–4 disk-diffusion expenses, a gap that squeezes budgets in mid-tier hospitals. Leasing models, such as Roche’s reagent-rental proposition for the cobas Liat, postpone upfront payments but lock buyers into multi-year consumable agreements. Unless pay-per-test models spread rapidly, this cost structure will keep the antibiotic resistance diagnosis devices market from matching double-digit growth rates seen in other molecular-diagnostics categories.

Fragmented and Stringent Regulatory Approval Pathways

A single rapid AST panel requires separate submissions to the FDA, EMA, China’s NMPA, India’s CDSCO, and Brazil’s ANVISA, each demanding pathogen-specific concordance data. Accelerate Diagnostics’ Pheno won FDA clearance in 2017 but did not secure CE marking until 2020 and remains unapproved in China. India’s 2024 rule mandating local validation at three government labs adds almost a year to timelines. These frictions inflate compliance costs, divert R&D budgets, and delay revenue capture, muting the antibiotic resistance diagnosis devices market’s CAGR by an estimated 0.5 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Outpace Installed-Base Revenue

Instruments contributed 63.12% of 2024 revenue as legacy automated AST and MALDI-TOF units remained indispensable for high-throughput labs. Yet consumables are projected to climb at 7.6% through 2030, widening their slice of the antibiotic resistance diagnosis devices market size as cartridge pull-through expands[3]Becton Dickinson. Single-use reagents cut cross-contamination risk, align with lean-labor workflows, and carry higher gross margins, making them a strategic focus for suppliers. Subscription bundles that wrap cartridges, software, and service into a monthly fee offer budget-relief to cash-strapped hospitals.

While instrument purchases follow seven- to ten-year cycles, consumables deliver predictable monthly revenue. Bruker’s MALDI Biotyper added 6,500 global placements by 2024, with 80% of new units landing in Asia-Pacific and Latin America. A mid-size hospital running 50 AST tests per day now spends USD 150,000–200,000 annually on reagents, ensuring recurring cashflows that anchor the antibiotic resistance diagnosis devices market.

By Technology: Rapid POC Platforms Disrupt Phenotypic Dominance

Phenotypic methods still hold 62.4% of 2024 revenue thanks to entrenched validation and reference-standard status. Nonetheless, rapid POC instruments are projected to grow 14.8% through 2030, triple the overall market rate, because clinicians value hours saved over dollars spent panels detecting blaKPC and mecA genes equip emergency teams to initiate targeted therapy within two hours, curbing empiric broad-spectrum use.

The FDA cleared five new PCR panels in 2024, while next-generation sequencing entered reimbursement schedules in Japan, hinting at future mainstreaming. AI-enhanced MALDI-TOF augments phenotypic platforms by adding spectral AST, blending speed with established accuracy. These innovations press incumbent vendors to refresh pipelines, ensuring the antibiotic resistance diagnosis devices market doubles down on rapid formats without discarding phenotypic reliability.

By End User: Pharma and Biotech Accelerate Adoption

Hospitals and diagnostic labs processed the bulk of test volumes and retained 62.4% of 2024 revenue. Pharma and biotech firms are logging a 9.7% CAGR as regulators insist on profiling resistant strains during clinical trials.

Merck’s ceftolozane-tazobactam program alone screened more than 10,000 isolates in 2024. CROs such as Charles River now market AST services, diversifying revenue streams and easing capacity bottlenecks for smaller biotech clients. As non-clinical demand matures, it cushions the antibiotic resistance diagnosis devices market against hospital budget freezes and opens parallel growth lanes in research, surveillance, and drug discovery.

Geography Analysis

North America commanded 41.5% of 2024 demand, underpinned by CMS stewardship mandates and Medicare reimbursements that pay USD 85–120 per rapid AST run. Canada budgeted CAD 85 million (USD 63 million) to deploy rapid molecular platforms, and Mexico’s IMSS tendered 150 automated systems, signaling broader regional penetration. The antibiotic resistance diagnosis devices market size in the region is expected to climb steadily as U.S. hospitals replace 1,200–1,500 legacy systems annually.

Asia-Pacific is set to grow at an 8.7% CAGR, the fastest worldwide. India’s National Action Plan targets full tertiary-hospital coverage with automated AST by 2027. China’s compulsory real-time AMR reporting drives networked placements, while Japan’s NGS reimbursement codes accelerate uptake of sequencing-based. Australia’s fast-track reviews and South Korea’s KRW 120 billion infrastructure fund further expand regional momentum.

Europe retains roughly 30% share thanks to mature laboratory networks in Germany, the United Kingdom, and France. Germany equipped 50 additional sentinel labs in 2024, and France cut AST-device review timelines in half. Middle East growth remains nascent but promising; Saudi Arabia ordered 80 automated systems for public hospitals. South America’s progress centers on Brazil, where Fiocruz’s cartridge assembly plant shortens supply chains and trims tariffs. Collectively, these regional dynamics uphold diversified demand that stabilizes the antibiotic resistance diagnosis devices market across economic cycles.

Competitive Landscape

The antibiotic resistance diagnosis devices market exhibits moderate concentration: the top five vendors bioMérieux SA, Danaher Corporation, Becton, Dickinson and Company, Thermo Fisher Scientific Inc, and F. Hoffmann-La Roche Ltd. contributed significantly to global revenue. Their installed bases lock hospitals into proprietary consumables, yet cartridge manufacturers that undercut prices now target those very systems with cross-compatible reagents. Bruker launched MBT STAR-BL, embedding AI analytics into existing MALDI-TOF units, while BD integrated the new Kiestra IdentifA AI module to automate colony identification.

Strategic differentiation pivots on setting: bioMérieux and BD focus on high-volume core labs, Cepheid and Roche on decentralized care, and T2 Biosystems on direct-from-blood MRI-based detection. Patent activity doubled for multiplexed PCR panels and nanopore sequencing modules, reflecting a race to secure intellectual property ahead of regulatory harmonization. Smaller firms such as Alifax and HiMedia leverage ISO 13485 credentials and regional manufacturing to win share in price-sensitive markets.

Regulatory frameworks like ISO 20776 and ISO 15189 raise entry barriers, but fast-track pathways in the United States, Australia, and Japan create opportunities for validated niche players. Vendor support programs that bundle financing, cloud analytics, and stewardship dashboards are emerging as differentiators beyond pure assay performance, shaping market share control in the antibiotic resistance diagnosis devices market.

Antibiotic Resistance Diagnosis Devices Industry Leaders

-

bioMérieux SA

-

Danaher Corporation

-

Becton, Dickinson and Company

-

Thermo Fisher Scientific Inc.

-

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Oxford Nanopore and bioMérieux launched AmPORE-TB, a nanopore-based RUO assay that profiles tuberculosis resistance mutations within hours.

- January 2025: Becton Dickinson secured FDA clearance for the BD Kiestra IdentifA platform, an AI-powered module that halves technician time during AST plate reading.

- March 2024: Alifax obtained ISO 13485 certification for its MICRONAUT-S automated AST system, expanding EU sales eligibility

- February 2024: HiMedia introduced a budget phenotypic AST cartridge compatible with BD’s Phoenix, priced 30% below imports.

Global Antibiotic Resistance Diagnosis Devices Market Report Scope

As per the scope of the report, the antibiotic resistance diagnosis devices are medical diagnostic devices used to rapidly detect whether the bacterial infection is resistant or susceptible to specific antibiotics. These devices help clinicians to choose right antibiotic early and reduce trial and error treatment, and limit the spread of resistant strains.

The antibiotic resistance diagnosis devices market is segmented by product type, technology, end user, and geography. By product type, the market is categorized into instruments and consumables. By technology, it is segmented into phenotypic AST, PCR technology, immunoassay, next-generation sequencing, mass spectrometry, and rapid / POC platforms. By end user, the segmentation includes hospitals & diagnostic laboratories, research & academic institutes, and pharmaceutical & biotechnology companies. Geographically, the market is segmented into North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Instruments |

| Consumables |

| Phenotypic AST |

| PCR technology |

| Immunoassay |

| Next-Generation Sequencing |

| Mass spectrometry |

| Rapid / POC Platforms |

| Hospitals & Diagnostic Laboratories |

| Research & Academic Institutes |

| Pharmaceutical & Biotechnology Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Instruments | |

| Consumables | ||

| By Technology | Phenotypic AST | |

| PCR technology | ||

| Immunoassay | ||

| Next-Generation Sequencing | ||

| Mass spectrometry | ||

| Rapid / POC Platforms | ||

| By End User | Hospitals & Diagnostic Laboratories | |

| Research & Academic Institutes | ||

| Pharmaceutical & Biotechnology Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the antibiotic resistance diagnosis devices market?

The antibiotic resistance diagnosis devices market size is USD 375.32 million in 2025 and is projected to hit USD 486.58 million by 2030

How fast is the market expected to grow?

Revenue is forecast to advance at a 5.33% CAGR between 2025 and 2030, supported by rapid AST adoption and stewardship mandates

Which product category is growing quickest?

Consumables are expanding at a 7.6% CAGR as single-use cartridges gain favor over capital-intensive instruments

Which region will see the fastest growth

Asia-Pacific is projected to post an 8.7% CAGR thanks to large-scale procurement programs in India and China

Page last updated on: