United Kingdom Testing, Inspection, And Certification (TIC) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

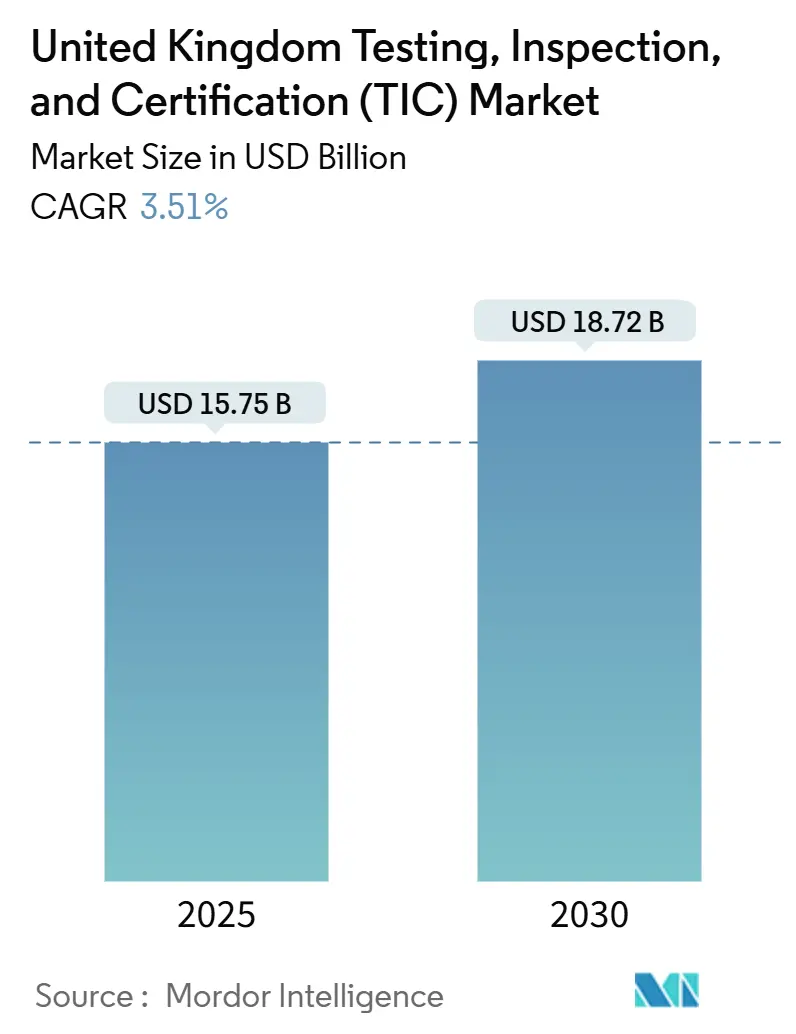

| Market Size (2025) | USD 15.75 Billion |

| Market Size (2030) | USD 18.72 Billion |

| Growth Rate (2025 - 2030) | 3.51% CAGR |

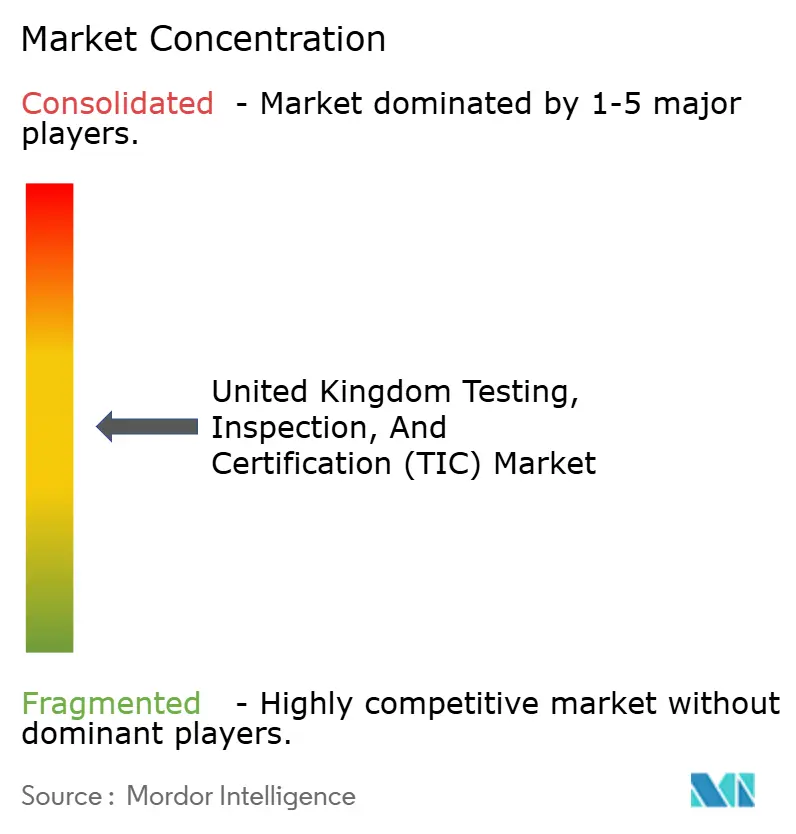

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Testing, Inspection, And Certification (TIC) Market Analysis by Mordor Intelligence

The United Kingdom testing, inspection, and certification (TIC) market is valued at USD 15.75 billion in 2025 and is projected to reach USD 18.72 billion by 2030, advancing at a 3.51% CAGR. Mandatory UKCA compliance, large-scale renewable investments, and accelerating corporate outsourcing underpin this steady expansion. Domestic regulations now diverge from EU norms yet remain technically equivalent, ensuring uninterrupted trade while creating parallel certification requirements that lift demand for local conformity assessment. Renewable energy build-out-especially offshore wind-injects sustained project pipelines that require extensive marine, structural, and grid-integration testing. Meanwhile, digital inspection platforms and remote monitoring tools improve operational productivity, tempering the impact of rising labor and energy costs. Competitive intensity is shaped more by domain expertise and accreditation breadth than by absolute scale, giving specialist UK providers room to defend pricing.

Key Report Takeaways

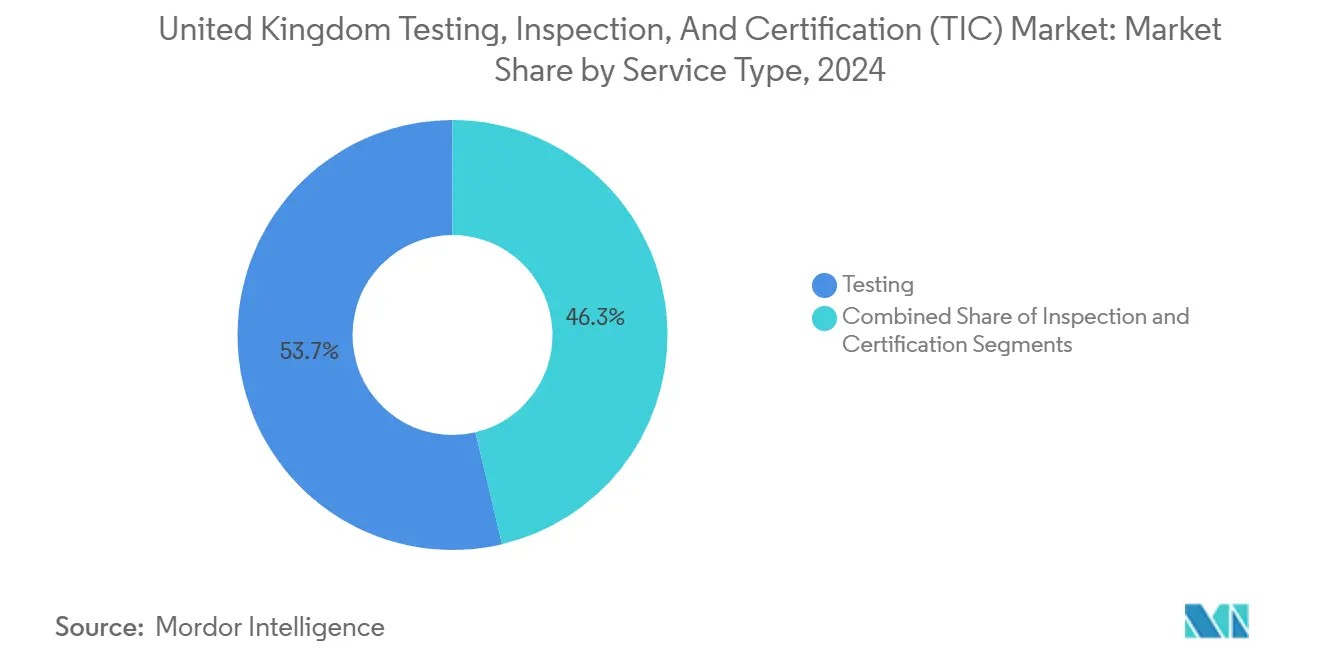

- By service type, testing captured 53.7% of the United Kingdom Testing, Inspection, and Certification market share in 2024, while certification is forecast to expand at a 4.2% CAGR through 2030.

- By sourcing type, outsourcing held 62.6% share of the United Kingdom Testing, Inspection, and Certification market size in 2024, and is projected to grow at a 3.8% CAGR to 2030.

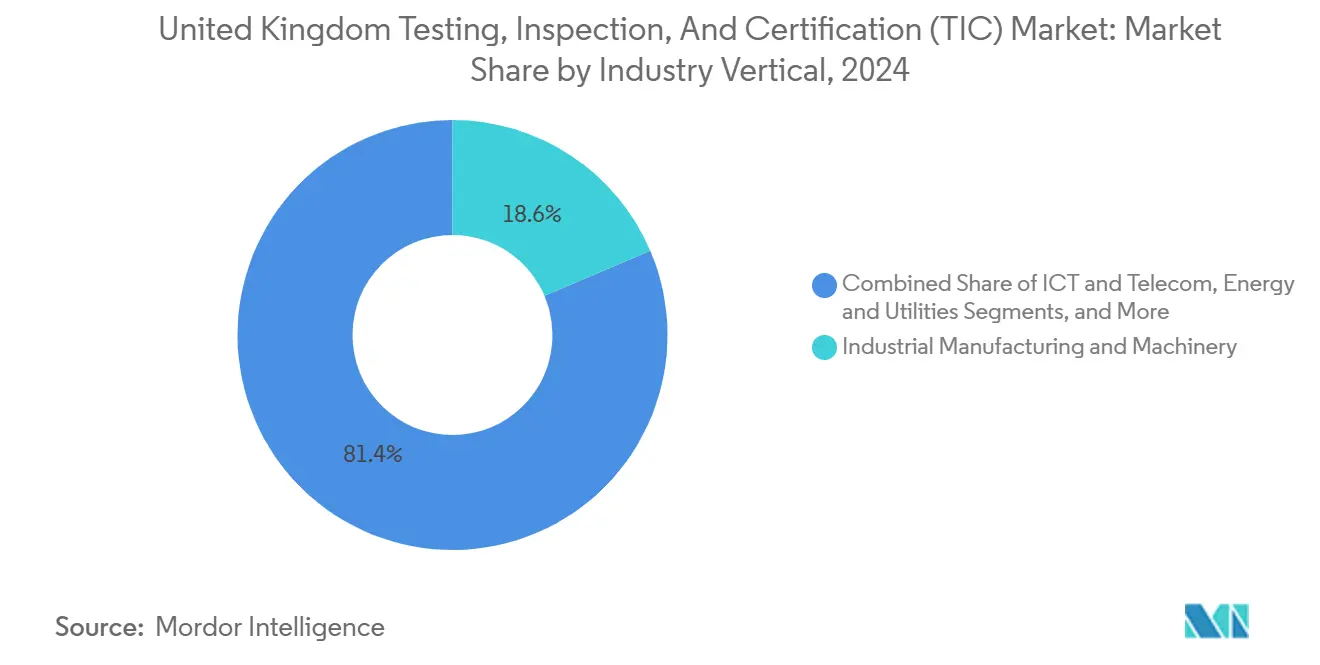

- By industry vertical, industrial manufacturing and machinery led with 18.6% of the United Kingdom Testing, Inspection, and Certification market share in 2024; energy and utilities is advancing at a 4.6% CAGR through 2030.

- By mode of service delivery, on-site engagement captured 54.2% of the United Kingdom Testing, Inspection, and Certification market in 2024, while remote and digital inspections show the fastest 4.8% CAGR to 2030.

United Kingdom Testing, Inspection, And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Brexit UKCA compliance timelines tightening | +0.8% | Great Britain | Medium term (2-4 years) |

| Accelerated offshore wind and renewable build-out | +0.6% | UK coastal regions, Scotland, North Sea | Long term (≥ 4 years) |

| Surge in EV battery-chain safety mandates | +0.4% | UK automotive manufacturing hubs | Medium term (2-4 years) |

| Corporate outsourcing for cost and speed gains | +0.3% | National, industrial centers | Short term (≤ 2 years) |

| NHS digital-pathology accreditation rollout | +0.2% | England, Wales, Scotland | Medium term (2-4 years) |

| Hydrogen pilot infrastructure safety codes | +0.1% | Industrial clusters, ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Brexit UKCA Compliance Timelines Tightening

The Department for Levelling Up, Housing and Communities confirms that recognition of CE marking ends in June 2025, obliging manufacturers to secure UKCA certificates for domestic market access. Construction products face the greatest urgency because updated fire-safety tests demand repeat laboratory cycles, stretching current capacity and inflating premium fees for fast-track services. As CE evidence cannot be reused, companies schedule dual test campaigns, creating a recurrent revenue base for UK-accredited labs. UKAS accreditation rules restrict issuance authority to qualified domestic bodies, insulating the United Kingdom Testing, Inspection, and Certification market against EU rivals.

Accelerated Offshore Wind and Renewable Build-Out

Government targets of 50 GW offshore wind by 2030 generate multi-year testing requirements for blades, nacelles, cables, and floating foundations.[1]ORE Catapult, “Offshore Renewable Energy,” ore.catapult.org.uk Marine fatigue analyses span 12-18 months, locking in demand for specialist providers possessing corrosion chambers and wave basins. The sector’s complexity favors laboratories with marine engineering pedigrees, while parallel needs for environmental impact assessments and grid-code validation fuel cross-selling. Policy commitments and climate obligations anchor project pipelines, shielding order books from macroeconomic cycles.

Surge in EV Battery-Chain Safety Mandates

OPSS guidance mandates abuse, thermal-stability, and transportation testing for lithium-ion packs, with full design certification costing USD 50,000-100,000 per battery type.[2]Office for Product Safety and Standards, “Battery Safety Guidance,” gov.uk UN 38.3 and IEC 62133 compliance now applies to vehicle, storage, and portable cells, broadening the client base. Domestic automakers prefer UK labs that can turn around results quickly while preserving intellectual property. Advanced chemistries-such as solid-state-necessitate new calorimetry rigs and gas analysis, widening the technology gap between leaders and generalists.

Corporate Outsourcing for Cost and Speed Gains

Rising accreditation costs and talent shortages push companies to externalize Testing, Inspection, and Certification functions, lifting outsourced penetration above 62% in 2024. Specialist providers deliver faster turnaround at lower unit cost because pooled volumes improve equipment utilization. Economic uncertainty magnifies this logic, as firms shift fixed laboratory expenses to variable service contracts. Digital data-sharing portals reduce coordination friction, making outsourced solutions even more attractive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs of accredited UK labs | -0.3% | National, London and Southeast | Short term (≤ 2 years) |

| Shortage of certified inspectors and analysts | -0.2% | National, specialized sectors | Medium term (2-4 years) |

| CMA scrutiny slowing TIC M and A consolidation | -0.1% | National | Medium term (2-4 years) |

| Public-sector payment lags hurting cash-flow | -0.1% | England, Wales, Scotland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Operating Costs of Accredited UK Labs

Energy-intensive tests such as environmental simulation suffer from volatile electricity prices that peaked at 30 pence per kWh in 2024, doubling prior norms. ISO/IEC 17025 quality systems consume up to 20% of annual revenue for small labs owing to proficiency schemes and auditor visits. Calibration delays of six-plus months force redundant equipment purchases, inflating capital budgets. These factors erode margins in commodity testing yet reinforce the value proposition in specialized high-complexity niches.

Shortage of Certified Inspectors and Analysts

Post-Grenfell reforms triggered a 40% undersupply of competent building-safety inspectors.[3]UK Parliament, “Building Safety Committee Reports,” committees.parliament.uk Salary inflation of 20-30% strains providers, especially in hydrogen, cybersecurity, and advanced-materials fields where talent pools are shallow. Training pathways demand two-to-three years, meaning capacity gaps persist through the medium term, risking service bottlenecks and elongated project timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Accelerates as Testing Dominates

Testing retained a 53.7% UK Testing, Inspection, and Certification market share in 2024 due to mandatory physical validation across aerospace, automotive, and construction products. Certification, though smaller, is rising at a 4.2% CAGR because distributed supply chains and heightened regulatory scrutiny mandate independent assurance. Dual UKCA-CE regimes oblige separate certificates, expanding the UK TIC market size for conformity assessments. Remote audit tools lower delivery costs while maintaining UKAS governance, enhancing segment profitability.

The UK Testing, Inspection, and Certification market continues to rely on testing for safety-critical deliverables such as pressure vessels and avionics electronics. However, artificial intelligence and robotics improve throughput, reducing per-test turnaround by up to 15%. Laboratories investing in automation unlock capacity headroom without proportional headcount growth, mitigating wage inflation.

By Sourcing Type: Outsourcing Momentum Builds

Outsourced services command 62.6% UK Testing, Inspection, and Certification market share and are forecast to grow at 3.8% annually through 2030 as firms offload non-core compliance tasks. The UK Testing, Inspection, and Certification industry benefits because external providers spread accreditation costs across many clients, achieving economies unfeasible in-house. Remote inspection and digital reporting platforms further decrease coordination overhead, reinforcing offloader economics.

In-house labs remain relevant in defense and aerospace where security clearance and proprietary technology demand internal control. Yet even those sectors increasingly contract peak-load requirements to certified partners, underlining the stickiness of the outsourcing trend.

By Industry Vertical: Industrial Manufacturing Leads, Energy Surges

Industrial manufacturing and machinery accounted for 18.6% of the UK TIC market size in 2024, anchored by stringent pressure-equipment and electromagnetic-compatibility directives. Energy and utilities exhibit the fastest trajectory at a 4.6% CAGR thanks to offshore wind and emergent hydrogen infrastructure that introduce new safety codes requiring specialized metallurgical and fatigue testing.

Automotive and transportation present fresh opportunity as battery systems, ADAS sensors, and autonomous logic demand laboratory verification beyond traditional mechanical tests. Life sciences sustain momentum driven by medical-device vigilance and Good Manufacturing Practice audits under MHRA oversight.

By Mode of Service Delivery: Remote Gains Traction

On-site inspections held 54.2% share in 2024 because many assets-bridges, turbines, petrochemical vessels-are immobile. Remote and digital modalities, however, are advancing at 4.8% CAGR as drone imaging, IoT sensor feeds, and AI anomaly detection gain regulatory acceptance. The UK TIC market leverages these tools to reduce safety risks and travel costs while capturing continuous data streams for predictive analytics. Sectors such as energy and utilities lead adoption; regulated industries like nuclear require longer evidence cycles but are piloting blended approaches.

Geography Analysis

London and the Southeast host regulatory headquarters and multinational client bases, enabling premium pricing but also exposing providers to high labor and real-estate costs. Scotland’s North Sea perimeter is the fastest-expanding sub-region, buoyed by offshore wind, hydrogen hubs, and carbon-capture pilots that require harsh-environment qualification. Local Testing, Inspection, and Certification firms pivot from legacy oil and gas know-how to meet renewable specifications, reinforcing regional capability moats.

Northern England maintains diversified demand across chemicals, heavy equipment, and advanced materials, supported by established industrial corridors. Wales benefits from aerospace and automotive clusters, sustaining workflow in materials testing and calibration. Government “level-up” infrastructure funds funnel inspection opportunities into rail, road, and flood-defense projects outside the capital, broadening revenue bases.

Remote technologies lessen geographic constraints for routine conformity checks, yet on-site mandates ensure that proximity still matters for rapid response visits. Consequently, regional providers with deep sector knowledge and UKAS accreditation preserve competitive advantage even as national players expand digital coverage.

Competitive Landscape

Intertek, SGS, and Bureau Veritas account for a sizable portion of the UK TIC market, but domestic specialists such as BSI, Lloyd’s Register, and Element Materials Technology retain a critical share by virtue of local accreditation and domain focus. The proposed EUR 32 billion (USD 35.2 billion) merger talks between Bureau Veritas and SGS illustrate an industry push toward scale amid digital disruption and client consolidation pressures.[4]Bureau Veritas, “The TIC Market,” group.bureauveritas.com Nonetheless, UK Competition and Markets Authority scrutiny tempers large-scale consolidation, preserving competitive diversity.

M&A activity continues at the niche level: Element acquired ISS Inspection Services to bolster its non-destructive testing capabilities in the energy sector, while Socotec bought ESG to deepen its environmental capabilities. Technology investment remains pivotal; Intertek’s USD 45 million upgrade of its Base Met Labs expands precious-metal analytics for renewable supply chains. Lloyd’s Register’s USD 25 million hydrogen testing facility in Aberdeen positions it at the frontier of new-energy compliance.

UKAS accreditation standards act as both quality gatekeepers and market barriers, preventing low-cost entrants from eroding pricing. Digital transformation differentiates leaders: AI-enabled defect recognition and blockchain certification are emerging service lines that promise higher margins and stickier client relationships.

United Kingdom Testing, Inspection, And Certification (TIC) Industry Leaders

Intertek Group plc

SGS United Kingdom Limited

Bureau Veritas UK Limited

Eurofins Scientific UK Limited

British Standards Institution (BSI Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bureau Veritas and SGS enter preliminary merger talks valued at EUR 32 billion (USD 35.2 billion).

- January 2025: Element Materials Technology acquires ISS Inspection Services, expanding UK energy sector coverage.

- December 2024: BSI has introduced a revised standard for fuel oils, aiming to ensure the use of suitable fuel oils and mitigate potential safety concerns.

- November 2024: Intertek invests USD 45 million in Base Met Labs acquisition to enhance precious-metals analysis.

United Kingdom Testing, Inspection, And Certification (TIC) Market Report Scope

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

What is the present value of the UK Testing, Inspection, and Certification market?

The market is valued at USD 15.75 billion in 2025.

How fast is the UK Testing, Inspection, and Certification sector expected to grow?

It is projected to expand at a 3.51% CAGR from 2025 to 2030.

Which service type is growing the quickest?

Certification services show the fastest growth at a 4.2% CAGR through 2030.

Why is outsourcing prevalent in UK conformity assessment?

Outsourcing captures 62.6% share because external providers deliver expertise, faster turnaround, and cost savings compared with in-house labs.

Which end-use segment is expanding the most rapidly?

Energy and utilities, propelled by offshore wind and hydrogen initiatives, is advancing at a 4.6% CAGR.

How are digital tools affecting UK Testing, Inspection, and Certification operations?

AI, drones, and IoT sensors enable remote inspections and predictive analytics, improving efficiency and widening service scope.

Page last updated on: