Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

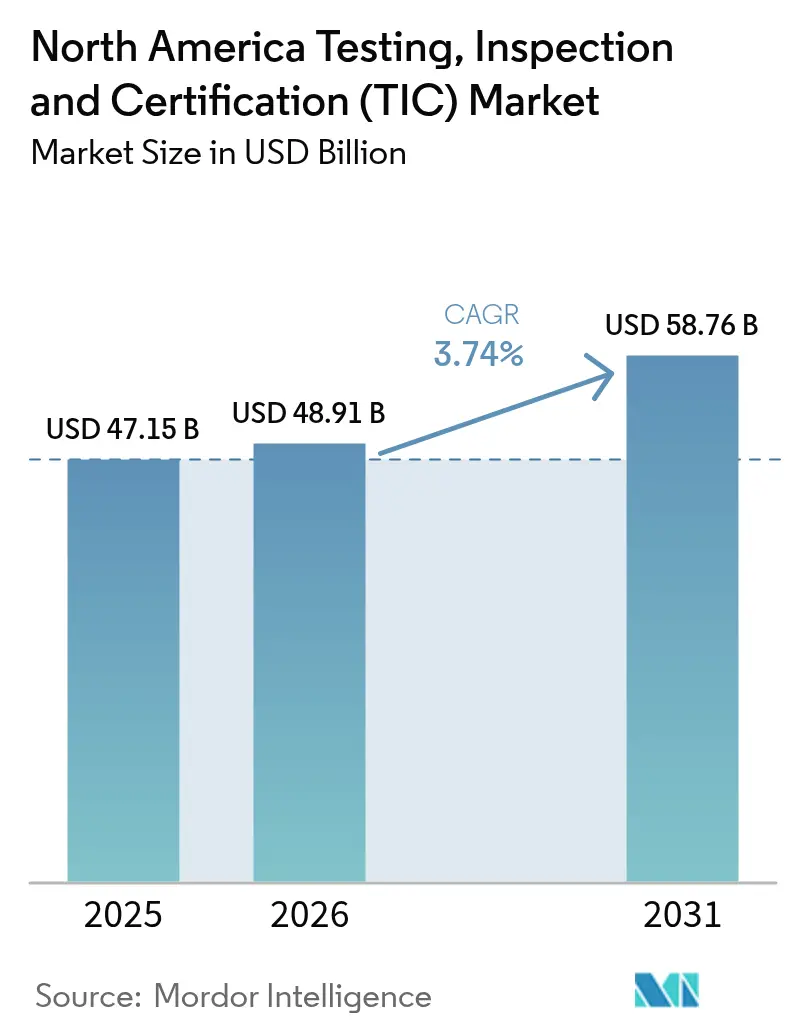

| Base Year Market Size (2025) | USD 47.15 Billion |

| Market Size (2026) | USD 48.91 Billion |

| Market Size (2031) | USD 58.76 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Testing, Inspection And Certification (TIC) Market Analysis by Mordor Intelligence

North America TIC market size in 2026 is estimated at USD 48.91 billion, growing from 2025 value of USD 47.15 billion with 2031 projections showing USD 58.76 billion, growing at 3.74% CAGR over 2026-2031. The trajectory highlights sustained demand created by stringent regulatory frameworks, digital transformation of service delivery, and rapid electrification of transportation assets. Heightened chemical-safety rules from the EPA and OSHA, accelerating battery production, and embedded-carbon verification for exporters all reinforce a stable pipeline of third-party testing engagements.[1]U.S. Environmental Protection Agency, “TSCA Risk Management Rules for Chlorinated Solvents,” epa.gov At the same time, major providers use acquisitions and digital platforms to lift productivity, offset price pressure, and deepen customer stickiness, keeping the North America TIC market on a steady expansion path. Remote inspection tools, cloud-based compliance analytics, and data-integrated supply-chain audits now serve as competitive differentiators in the North America TIC market, while nearshoring into Mexico widens geographic demand diversity.[2]Bureau Veritas, “Remote Field Services,” bureauveritas.com Electric-vehicle battery laboratories, expanded PFAS capabilities, and additive-manufacturing certifications create new revenue pools that complement the mature industrial base in the North America TIC market.

Key Report Takeaways

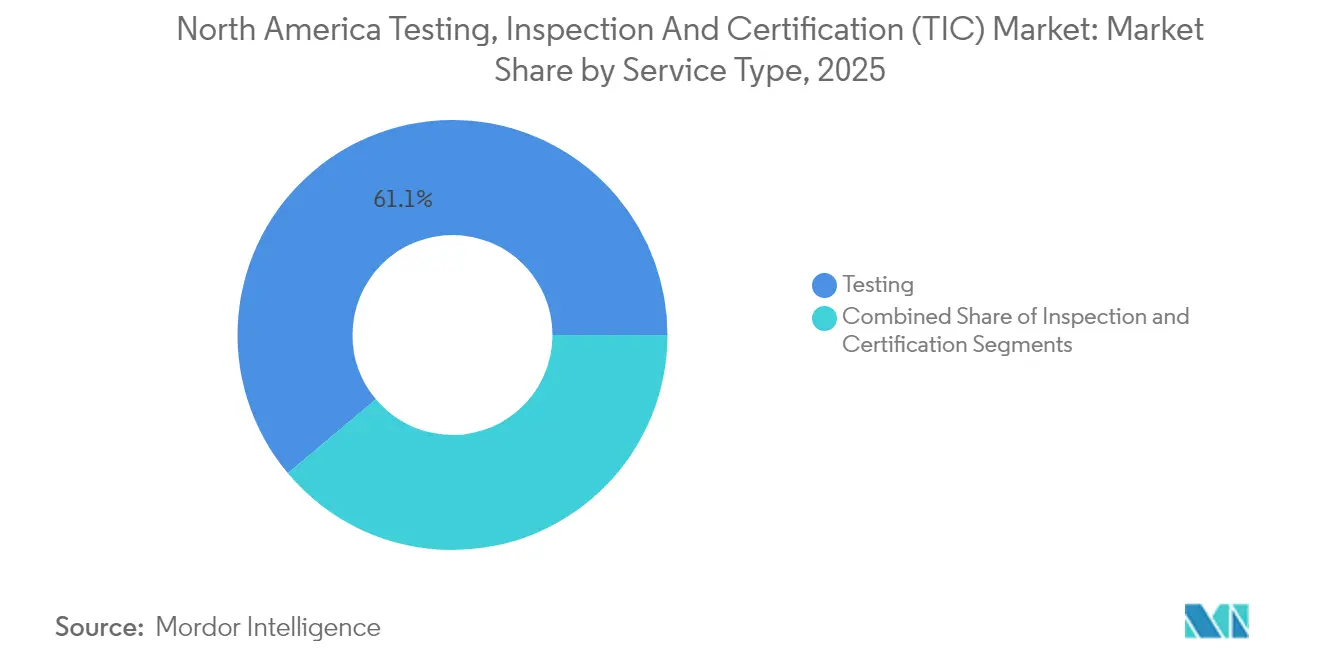

- By service type, testing captured 61.12% of the North America TIC market share in 2025, and certification is projected to lead growth at a 4.41% CAGR through 2031.

- By sourcing type, outsourced services accounted for 69.82% of the North America TIC market size in 2025, while the same segment is forecast to expand at a 4.53% CAGR to 2031.

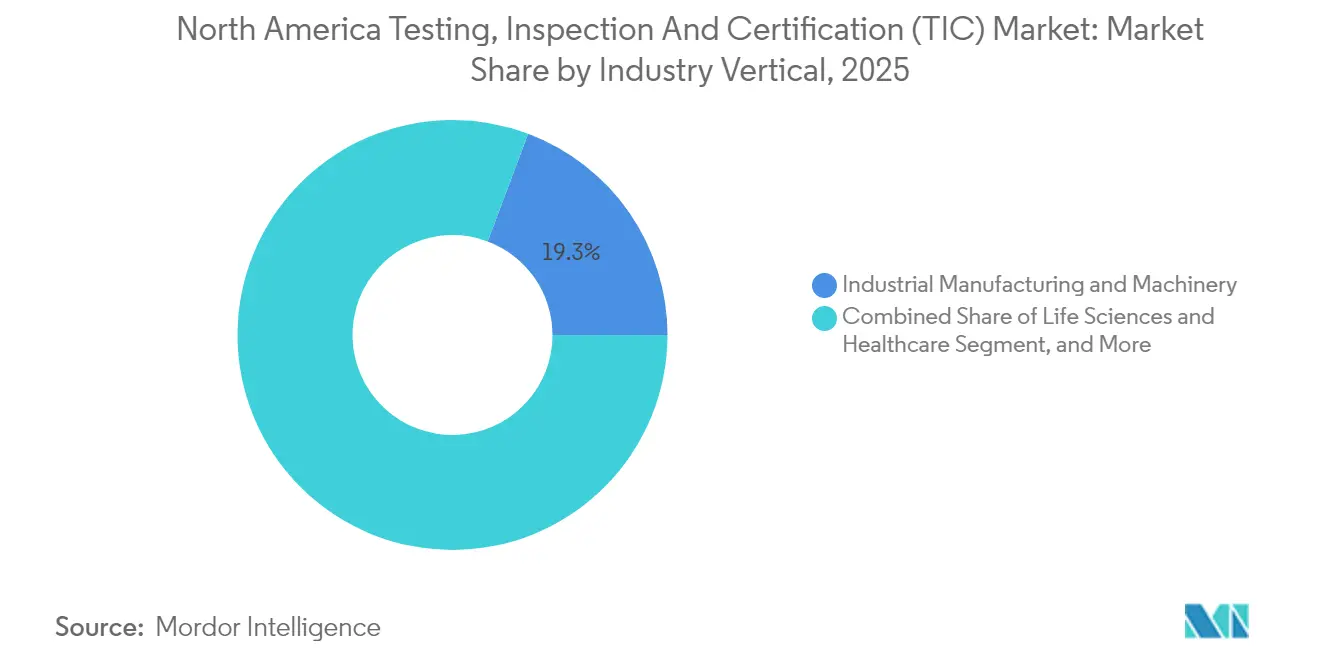

- By industry vertical, industrial manufacturing commanded 19.28% revenue of the North America TIC market in 2025; life sciences and healthcare is advancing at a 4.96% CAGR through 2031.

- By mode of service delivery, on-site services held a 49.08% share of the North America TIC market in 2025, and remote-digital services are poised for a 4.78% CAGR to 2031.

- By country, the United States led with an 80.62% share of the North America TIC market in 2025, while Mexico recorded the highest 4.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Testing, Inspection And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High compliance burden due to stringent North American regulatory frameworks | +1.2% | United States and Canada | Long term (≥ 4 years) |

| Rising complexity of manufacturing supply chains and distributed sourcing | +0.8% | North America and Mexico | Medium term (2-4 years) |

| Digital transformation driving demand for data-integrated testing and inspection services | +0.6% | Global | Medium term (2-4 years) |

| Surge in electric-vehicle and battery production requiring specialized TIC | +0.5% | United States and Mexico | Long term (≥ 4 years) |

| Carbon-border adjustment policies prompting embedded-carbon verification | +0.3% | North America exports to EU | Short term (≤ 2 years) |

| Proliferation of additive-manufacturing service bureaus needing certification | +0.2% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Compliance Burden Due to Stringent North American Regulatory Frameworks

Escalating cross-border rules obligate manufacturers to maintain rigorous third-party verification. The EPA’s 2024 TSCA solvent rules introduced exposure limits dramatically below earlier OSHA thresholds, triggering extensive monitoring requirements. OSHA’s 2024 Hazard Communication update aligned labels with GHS Rev 7, adding re-classification projects that funnel fresh work to laboratories. Canada matched U.S. formaldehyde limits for composite wood in 2025, preserving accredited-lab testing mandates while easing trade frictions. Cosmetic and pharmaceutical companies now face FDA-proposed asbestos testing protocols using standardized methods, further lifting sample volumes. As a result, the North America TIC market consistently benefits from a regulatory environment that demands documented, independent proof of compliance.

Rising Complexity of Manufacturing Supply Chains and Distributed Sourcing

Multi-tier supplier networks heighten quality-assurance risk, especially when critical components originate in dispersed plants. University of Cambridge research links supply-chain complexity to higher product-safety incidents, underscoring the need for specialized audits. SGS responded with Supplier Evaluation and Qualification Solutions that blend digital dashboards, self-assessment questionnaires, and on-site verifications to close visibility gaps. Automotive, aerospace, and electronics firms deploy such programs to uncover tier-2 weaknesses before they reach assembly. North American nearshoring adds new facilities in Mexico, forcing original equipment manufacturers to validate unfamiliar partners quickly. Consequently, the North America TIC market secures long-term demand by acting as a risk-mitigation partner for distributed production models.

Digital Transformation Driving Demand for Data-Integrated Testing and Inspection Services

Boston Consulting Group forecasts that digital tools will influence 40-60% of TIC activities this decade. Providers now leverage augmented-reality headsets, 360-degree video, and cloud platforms to reduce travel, shorten cycle times, and widen access to scarce experts. Bureau Veritas notes that remote inspection lowers carbon footprints while keeping audit rigor intact, integrating seamlessly with its case-management system. TÜV Rheinland’s Virtual Expert allows real-time annotations and guidance across multiple participants, expanding the addressable market for remote services. Automation laboratories and predictive analytics dashboards have begun shifting providers from reactive testers to proactive ecosystem orchestrators. This modernization reshapes customer expectations and enlarges the value captured by the North America TIC market.

Surge in Electric-Vehicle and Battery Production Requiring Specialized TIC

Rapid electrification has spawned highly technical battery-safety and performance protocols such as UN 38.3, UL 2580, and SAE J2929. UL Solutions opened an 89,000 sq ft battery laboratory near Detroit to run abuse, fire, and environmental tests on cells, modules, and packs. SGS upgraded its Georgia site to 100 V and 1,200 A capacity, accommodating light-EV and energy-storage applications. Southwest Research Institute supports transport-certification tests that OEMs need before shipping lithium-ion systems internationally. These investments expand capacity just as the North America TIC market faces a wave of gigafactory projects, solid-state innovations, and stricter EPA range-certification procedures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost pressure and price competition among TIC providers | -0.7% | North America | Medium term (2-4 years) |

| Shortage of skilled inspectors and laboratory technicians in specialized domains | -0.4% | United States and Canada | Long term (≥ 4 years) |

| Ambiguity in jurisdiction over remote/digital inspection results | -0.2% | North America | Short term (≤ 2 years) |

| Corporate sustainability self-declarations reducing third-party certification demand | -0.3% | Global, with North America focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost Pressure and Price Competition among TIC Providers

Global players vie aggressively for high-volume, standardized projects, compressing margins even as demand grows. UL Solutions, holding roughly 7% of outsourced product services, targets a 24% EBITDA margin but currently hovers near 20%, reflecting efficiency headwinds. SGS added environmental and connectivity labs via multiple acquisitions to drive scale economies. Bureau Veritas purchased Maxxam Analytics for USD 485 million, integrating it to broaden Canadian coverage and dilute fixed costs. Commoditized chemical screens and repetitive safety audits leave little room for differentiation, forcing providers to negotiate bundled contracts and multi-year price locks. Persistent consolidation tempers the growth rate of the North America TIC market, even as volumes trend upward.

Shortage of Skilled Inspectors and Laboratory Technicians in Specialized Domains

Clinical laboratories, battery test centers, and advanced-materials facilities all face sizable talent gaps. The U.S. Bureau of Labor Statistics sees over 24,000 lab-technologist vacancies annually, compared with only 5,000 two decades ago. Surveys show just 12% of technicians are highly likely to remain in the field, citing pay dissatisfaction and high burnout. Similar deficits permeate wire-and-cable and additive-manufacturing inspections, where fewer experienced engineers manage ever more complex evaluations. Providers invest in automation, knowledge-capture systems, and augmented-reality guidance to ease bottlenecks, yet mission-critical tests still hinge on seasoned staff. This scarcity slows project throughput and marginally tempers the CAGR of the North America TIC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Commands Market Leadership

Testing services accounted for 61.12% of the North America TIC market size in 2025, underlining the foundational role laboratory verification plays across regulatory compliance and product development. Certification, while smaller, is forecast to record a 4.41% CAGR through 2031, aided by rules that increasingly demand documented conformity beyond raw data. The North America TIC market continues to rely on large-scale chemical, environmental, and material analyses as new PFAS, battery-safety, and additive-manufacturing standards emerge.

Certification growth reflects OSHA’s GHS alignment and EPA’s PFAS mandates, which compel manufacturers to secure accredited sign-offs before shipments. Aerospace and maritime fire-testing upgrades, such as SGS’s ISO/IEC 17025-accredited Farmingdale facility, demonstrate how integrated testing-plus-certification packages add value. Providers bundling both services can capture wallet share and create stickier client relationships, reinforcing competitive positioning within the North America TIC industry.

By Sourcing Type: Outsourced Services Dominate Market Dynamics

Outsourced engagements represented 69.82% of the North America TIC market share in 2025, rising as companies focus on core competencies and grapple with capital-intensive lab investments. Forecasts show the outsourced segment growing at 4.53% through 2031 as regulations proliferate and specialized instrumentation costs escalate. Consequently, the North America TIC market aligns with strategic procurement patterns, shifting quality control from in-house teams to external experts.

Digital remote-inspection platforms accelerate outsourcing adoption. Bureau Veritas reports faster project cycles and smaller carbon footprints when customers pivot to hybrid audit models combining on-site sampling with virtual oversight. UL Solutions’ CableBuilder software augments this trend by digitizing documentation flows, reducing rework for manufacturers facing skilled-labor gaps. These examples illustrate how outsourced providers deploy technology to amplify value and cement their role as extensions of client quality teams.

By Industry Vertical: Industrial Manufacturing Leads while Life Sciences Accelerates

Industrial manufacturing and machinery generated 19.28% of 2025 revenue, reflecting broad-based equipment certification, non-destructive testing, and materials analysis. Life sciences and healthcare, though smaller, carry the fastest 4.96% CAGR to 2031, propelled by medical-device certifications and stricter cosmetic-safety assessments. Both verticals draw on the North America TIC market for specialized, accredited evaluations that satisfy FDA, OSHA, and international standards.

Pharmaceutical serialization audits, PFAS water-testing mandates, and medical-battery safety validations combine to bolster the life sciences pipeline. Meanwhile, additive-manufacturing qualification paths under the Pressure Equipment Directive show how industrial OEMs converge on standardized TIC protocols to unlock production efficiencies. The cross-pollination of digital twins, material-traceability systems, and predictive maintenance analytics widens the service scope and reinforces growth prospects within the North America TIC industry.

By Mode of Service Delivery: On-Site Services Lead with Remote Gaining Momentum

On-site inspections held 49.08% of 2025 revenue, covering asset-integrity checks, construction verifications, and factory audits that mandate physical presence. Remote-digital services, however, are primed for a 4.78% CAGR to 2031, buoyed by bandwidth advances and regulator acceptance of virtual methods. The North America TIC market now blends physical and digital workflows to match risk levels and budget constraints.

TÜV Rheinland completed over 5,000 remote audits using its Virtual Expert tool, confirming that real-time guidance and cloud-based evidence capture satisfy most conformity-assessment needs. SGS’s QiiQ mobile app offers 360-degree video, smart-glasses integration, and secure data storage, illustrating how providers replicate on-site rigor without travel. Nonetheless, destructive tests, fire-safety trials, and high-voltage battery abuses still demand laboratory or field presence, preserving a balanced delivery mix across the North America TIC market.

Geography Analysis

The United States generated 80.62% of 2025 revenue for the North America TIC market, sustained by expansive federal and state regulations, dense manufacturing clusters, and leading technology ecosystems. EPA solvent restrictions, OSHA hazard-communication revisions, and FDA battery-range certifications alone feed a robust pipeline of high-value tests. Global providers maintain flagship laboratories from New York to California, ensuring rapid turnaround for domestic clients.

Canada contributes a steady share, supported by resource-sector assays, environmental testing, and harmonized rules with the U.S. Formaldehyde emissions alignment in 2025 minimizes duplicate testing, yet accredited laboratories remain mandatory, anchoring services in the North America TIC market. Bureau Veritas’ acquisition of Maxxam Analytics enlarged its Canadian portfolio, signaling that consolidation elevates scale and specialization.

Mexico stands out with a 4.97% forecast CAGR to 2031 as nearshoring shifts automotive, electronics, and industrial machinery production southward. Manufacturers depend on cross-border auditors for supplier verification, PFAS water-testing, and battery-component certifications. U.S. International Trade Commission data on aluminum extrusions highlights Mexico’s rising role in regional supply chains, confirming strong opportunities for TIC providers. Together, these dynamics diversify revenue streams and fortify long-run growth for the North America TIC market.

Competitive Landscape

Market leadership is moderately concentrated among global multinationals, yet niches remain for regional specialists. UL Solutions ranks first with roughly 7% of outsourced product services, leveraging deep standards expertise and aggressive M&A to expand hydrogen, battery, and wire-and-cable offerings. SGS, Bureau Veritas, and Intertek collectively pursue bolt-on acquisitions, enlarging capacity in environmental testing, renewables consulting, and minerals analysis.

Digitalization has become the new battleground. Providers roll out augmented-reality inspections, asset-monitoring dashboards, and AI-powered document reviews to differentiate on speed and insight. Checkfirst’s TICC AI Innovator Program claims a 2.1× ROI boost for adopters, signaling that data analytics may soon reshape pricing and productivity benchmarks.[4]Checkfirst, “TICC AI Innovator Program,” checkfirst.ai The North America TIC market, therefore, rewards firms that blend scale, specialization, and technology.

The terminated USD 33 billion merger talks between SGS and Bureau Veritas in January 2025 illustrate ongoing consolidation pressures. Acquisitions such as SGS’s purchase of RTI Laboratories for PFAS capabilities and Bureau Veritas’ buyout of ArcVera Renewables show a pivot toward high-growth verticals. As regulatory mandates intensify and supply-chain complexity grows, strategic forays into cybersecurity, battery safety, and carbon-verification segments are expected to accelerate.

North America Testing, Inspection And Certification (TIC) Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SGS and Bureau Veritas ended merger discussions that aimed to create a USD 33 billion entity.

- January 2025: SGS acquired RTI Laboratories to deepen PFAS and materials analysis capacity.

- January 2025: Bureau Veritas acquired Maxxam Analytics for CAD 650 million (USD 485 million).

- November 2024: Bureau Veritas bought Versatec Energy B.V. to strengthen renewables consulting.

North America Testing, Inspection And Certification (TIC) Market Report Scope

Testing represents the industrial activities that ensure that manufactured products, individual components, and multicomponent systems are adequate for their intended purposes. Inspection and testing are the operational parts of quality control, which is the most crucial factor in any manufacturing company's survival. Quality control directly supports the other elements of cost, productivity, on-time delivery, and market share.

The North America Testing, Inspection, and Certification (TIC) Market is segmented by Type (Outsourced, In-house), End-User Vertical (Consumer Goods and Retail, Environmental (Effluent, Water, Soil, Air), Food and Agriculture, Manufacturing and Industrial Goods, Oil and Gas, Construction and Engineering), and Country (United States, Canada).

For each segment, the market sizing and forecasts have been provided on the basis of value (in USD million) and volume (in metric tons).

By Service Type

| Testing |

| Inspection |

| Certification |

By Sourcing Type

| In-house |

| Outsourced |

By Industry Vertical

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Other Industry Verticals (Environment, Sustainability, etc.) |

By Mode of Service Delivery

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

By Country

| United States |

| Canada |

| Mexico |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Other Industry Verticals (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America TIC market in 2031?

The market is expected to reach USD 58.76 billion by 2031, growing at a 3.74% CAGR.

Which service type currently generates the largest revenue?

Testing services lead, capturing 61.12% of 2025 revenue.

Why is Mexico growing faster than the United States and Canada?

Nearshoring shifts manufacturing to Mexico, driving a 4.97% CAGR for TIC services linked to new plants and supply-chain audits.

How are digital tools changing TIC service delivery?

Remote inspections, 360-degree video, and cloud analytics accelerate project cycles, reduce travel costs, and expand expert reach.

Which verticals will contribute most to future growth?

Life sciences, battery-electric mobility, and renewables testing are forecast to grow fastest due to stricter regulatory demands and technology shifts.

What are the main challenges facing TIC providers?

Intense price competition and shortages of skilled inspectors and lab technicians constrain margin expansion and capacity scaling.

Page last updated on: