United States Testing, Inspection, And Certification (TIC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

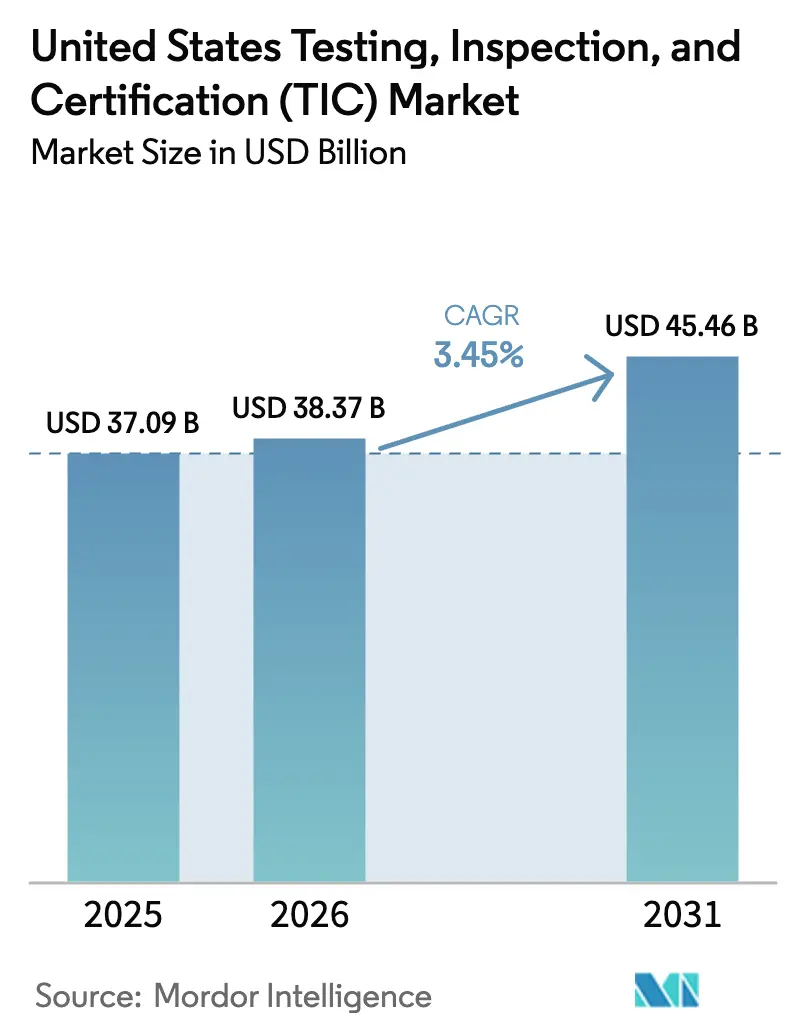

| Base Year Market Size (2025) | USD 37.09 Billion |

| Market Size (2026) | USD 38.37 Billion |

| Market Size (2031) | USD 45.46 Billion |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Testing, Inspection, And Certification (TIC) Market Analysis by Mordor Intelligence

The US Testing, Inspection, and Certification market size was valued at USD 37.09 billion in 2025 and estimated to grow from USD 38.37 billion in 2026 to reach USD 45.46 billion by 2031, at a CAGR of 3.45% during the forecast period (2026-2031). This moderate expansion reflects a mature but opportunity-rich landscape supported by USD 1.2 trillion in federal infrastructure spending, multi-agency regulatory mandates, and accelerating digital transformation across critical industries. Service demand is led by materials testing for stimulus-funded projects, cybersecurity assessments triggered by the U.S. Cyber Trust Mark, and analytical protocols tied to emerging PFAS standards. Consolidation remains the preferred growth vector for established laboratories striving to add niche capabilities; yet the failed USD 33 billion SGS–Bureau Veritas merger illustrates regulatory headwinds that preserve competitive diversity. Acute talent shortages, fragmented accreditations, and cost-sensitive SMEs pose persistent constraints, even as digital inspection tools unlock remote revenue streams and efficiencies.

Key Report Takeaways

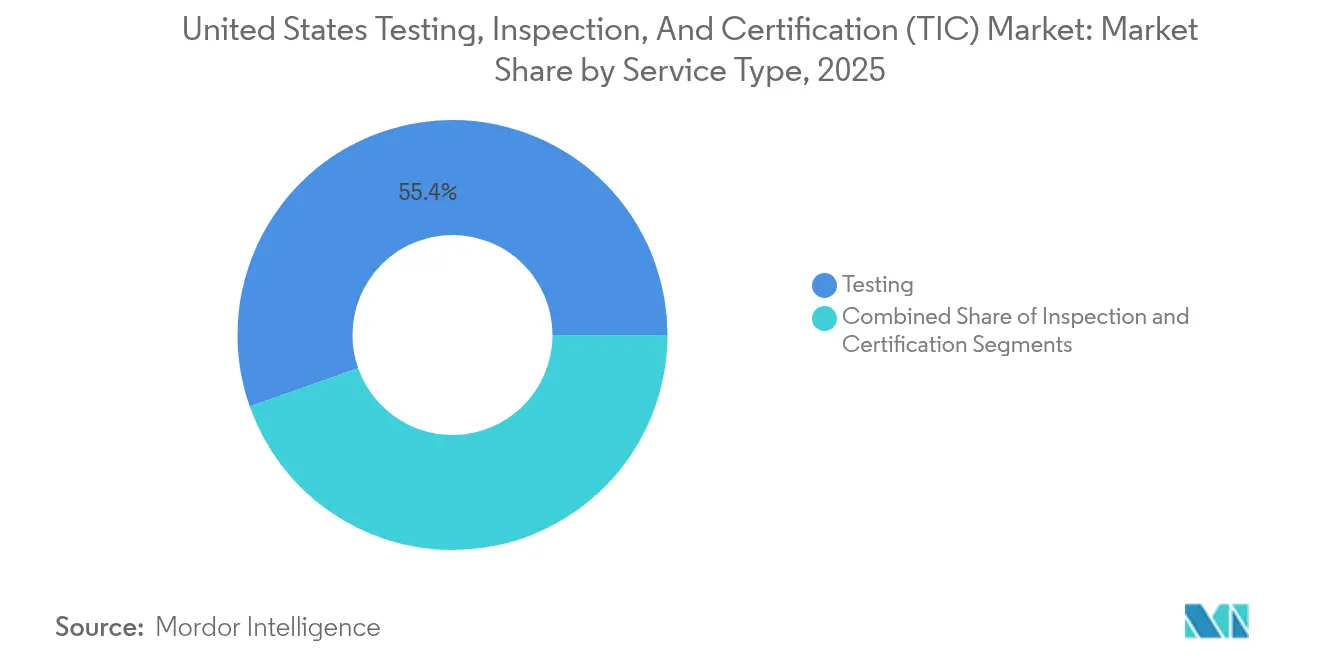

- By service type, Testing held 55.40% of the US Testing, Inspection, and Certification market share in 2025, while Certification is forecast to expand at a 4.05% CAGR through 2031.

- By sourcing type, In-house programs controlled 53.10% of the US Testing, Inspection, and Certification market size in 2025, whereas Outsourced activity is advancing at a 3.82% CAGR to 2031.

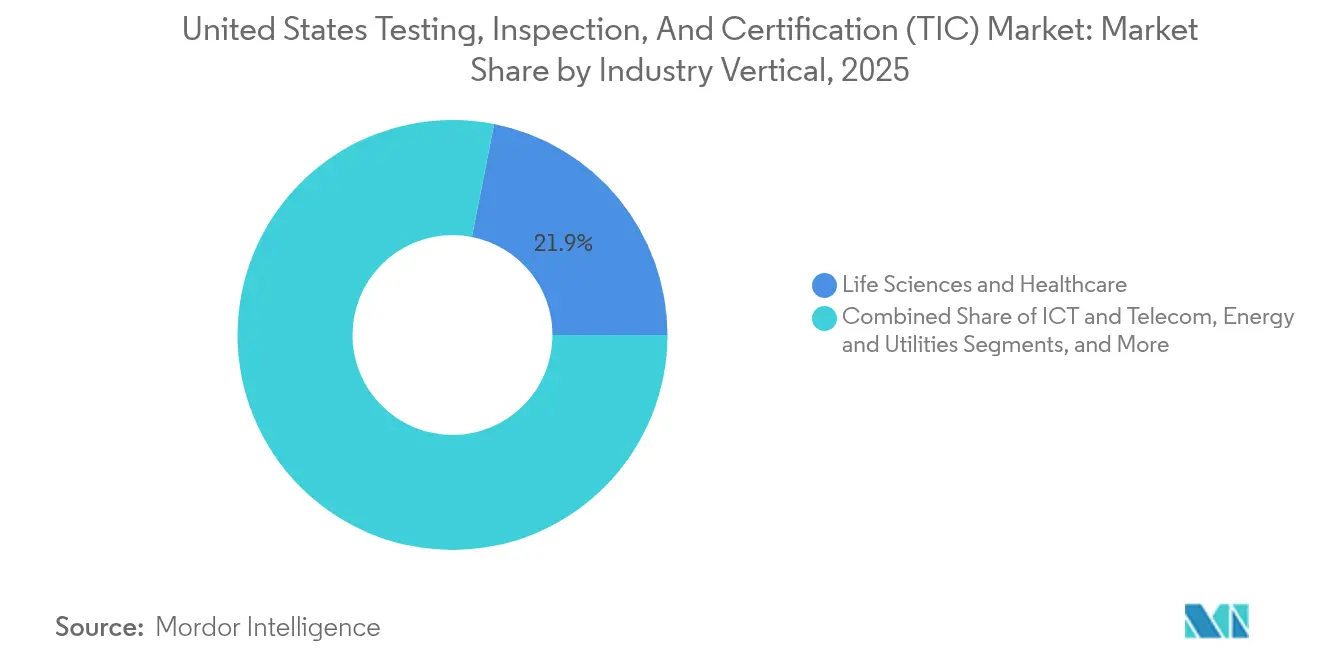

- By industry vertical, Life Sciences and Healthcare generated 21.90% of 2025 revenue, but Automotive and Transportation is projected to post the fastest 5.05% CAGR to 2031.

- By mode of service delivery, On-site solutions commanded 56.85% revenue in 2025, and Remote and Digital options are accelerating at a 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Testing, Inspection, And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter multi-agency regulatory compliance mandates | +1.2% | National, concentrated in high-regulation states | Medium term (2-4 years) |

| Increasing outsourcing of TIC by OEMs and brand owners | +0.8% | National, with emphasis on manufacturing hubs | Long term (≥ 4 years) |

| Digital and remote inspection technologies adoption | +0.6% | National, accelerated in tech-forward regions | Short term (≤ 2 years) |

| Renewable-energy and EV build-out quality requirements | +0.9% | National, concentrated in renewable energy corridors | Medium term (2-4 years) |

| Cyber-security certification for connected products | +0.4% | National, with tech sector concentration | Short term (≤ 2 years) |

| Federal infrastructure-stimulus materials testing surge | +0.7% | National, prioritizing infrastructure-deficit states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Multi-Agency Regulatory Compliance Mandates

Federal agencies are imposing unprecedented requirements that expand the US Testing, Inspection, And Certification market by compelling utilities, manufacturers, and consumer brands to verify compliance across overlapping rule sets. The EPA’s PFAS rule obligates 4,100-6,700 U.S. water systems to conduct compound-specific testing and remediation planning, creating a multi-year analytics backlog. Simultaneously, the FDA’s Cosmetics Regulation Act modernizes safety substantiation and GMP protocols, pushing personal-care companies toward third-party certification.[1]NSF, “The FDA Modernization of Cosmetics Regulation Act: What You Need To Know,” nsf.org Providers able to maintain dual EPA-FDA accreditations gain an edge as clients seek single-source partners for complex, cross-regulatory portfolios.

Increasing Outsourcing of TIC by OEMs and Brand Owners

Persistent shortages in specialized technicians and engineers elevate external demand. The Semiconductor Industry Association foresees 70,000 unfilled U.S. positions by 2030, compelling fabs to import expertise or partner with accredited labs for critical verifications. Industry associations highlight managed-service models that combine skills-convergence training with stringent data-security controls, making outsourcing an attractive capability-building lever.[2]IAOP, “PULSE: Outsourcing's Role in Filling Talent Gap,” iaop.org As supply-chain complexity rises, brand owners prioritize specialized laboratories that can scale quickly across multiple sites and regulatory regimes.

Digital and Remote Inspection Technologies Adoption

Remote platforms such as SGS QiiQ and TÜV Rheinland’s Virtual Expert deliver live video, augmented reality overlays, and secure documentation, enabling real-time audits without travel. Early adopters report reduced inspection cycle-times and lower carbon footprints. Regulatory bodies now allow virtual witnessing for defined scopes, accelerating client acceptance. Providers investing in 5G-enabled cameras, IoT sensors, and AI-driven analytics differentiate by offering predictive insights alongside compliance confirmation, reinforcing the digital pivot within the US Testing, Inspection, and Certification market.

Renewable-Energy and EV Build-Out Quality Requirements

Ramp-ups in wind, solar, and battery storage installations elevate demand for grid-code compliance testing. UL Solutions is conducting turbine certification against evolving European grid requirements, a template migrating to U.S. projects as interconnection rules tighten. IEEE 1547-2018 and UL 1741 SB establish uniform inverter benchmarks, driving laboratory workflows for distributed generation assets. Parallel EV acceleration expands demand for battery material validation and high-voltage safety certification, enlarging the addressable pool for Testing, Inspection, and Certification providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and price sensitivity among SMEs | -0.7% | National, concentrated in cost-sensitive industries | Long term (≥ 4 years) |

| Supply-chain disruptions delaying sample logistics | -0.3% | National, with regional variation | Short term (≤ 2 years) |

| Acute shortage of specialized TIC workforce | -0.9% | National, severe in high-tech regions | Medium term (2-4 years) |

| Fragmented accreditation and overlapping standards | -0.4% | National, complex in multi-state operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost and Price Sensitivity Among SMEs

Construction inflation and higher wage bills squeeze smaller enterprises, forcing them to triage compliance spending. The Congressional Budget Office projects a 24.3% erosion in the purchasing power of Infrastructure Investment and Jobs Act allocations by 2031, reshaping bid strategies toward basic compliance at minimal cost. Without volume-based discounts, SMEs defer non-mandatory testing, curbing addressable revenue for Testing, Inspection, and Certification vendors focused on value-added services.

Acute Shortage of Specialized TIC Workforce

The scarcity of metrologists, chemists, and cybersecurity auditors caps throughput and inflates wages. Semiconductor fab expansions underscore the problem, as companies import technicians to bridge domestic gaps. Thin regional talent pools elevate project lead-times and complicate nationwide service coverage, dampening growth prospects where staffing becomes the critical path.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Remains Core as Certification Accelerates

Testing dominated the US Testing, Inspection, And Certification market size with 55.40% share in 2025 due to immutable regulatory mandates. High-volume water, materials, and electronics analyses continue to flow through accredited labs, anchoring revenue stability. Conversely, certification is set to outpace with a 4.05% CAGR, fueled by the U.S. Cyber Trust Mark and grid-code compliance programs that require periodic reassessments. The segment’s ascent mirrors a customer shift toward validation credentials that unlock market access. Major laboratories broaden scope by integrating certification into existing testing chains, strengthening one-stop value propositions across consumer IoT, EV batteries, and renewable components.

Testing growth is hampered slightly by automation that reduces repetitive manual tasks; however, complex chemistries and evolving standards sustain minimum testing volumes. Certification’s faster trajectory stems from policy-driven expansion in connected-device labeling and ESG-linked supply-chain audits. Laboratories equipped with both ISO 17025 and ISO 17065 accreditations command premium pricing as clients consolidate providers to streamline oversight. The interplay between mandatory tests and voluntary labels keeps both sub-segments central to the US Testing, Inspection, And Certification market.

By Sourcing Type: Outsourcing Gains on Capability Gaps

In-house labs controlled 53.10% of 2025 revenue, reflecting legacy investments in sectors such as pharmaceuticals, aerospace, and petrochemicals. These captive units ensure intellectual-property protection and immediate turnaround times. Outsourcing, advancing at a 3.82% CAGR, benefits from the widening gap between regulatory scope and internal capacity. OEMs favor external partners that guarantee multi-jurisdictional compliance while absorbing capital expenditures on advanced equipment.

Cost is no longer the sole driver for externalization. Skill shortages, cybersecurity complexity, and accelerated product cycles push corporations to contract accredited specialists. Framework agreements featuring performance KPIs, secure data pipelines, and co-development of test protocols become common. Providers deepen partnerships by embedding staff onsite, blending outsourced expertise with client oversight, thereby expanding the US TIC market size attributed to managed-service models.

By Industry Vertical: Life Sciences Leads as Automotive Accelerates

Life Sciences and Healthcare accounted for 21.90% of 2025 revenue, boosted by FDA modernization, biologic innovations, and constant GMP upgrades. High test volumes for sterility, potency, and bioequivalence underpin stable demand. The vertical’s reliance on third-party validation remains pronounced due to the criticality of patient safety and escalating global submission requirements.

Automotive and Transportation is projected to register the fastest 5.05% CAGR, propelled by EV drivetrain testing, functional safety for autonomous features, and stringent battery performance metrics. Laboratories with climatic chambers, shaker rigs, and high-voltage expertise attract automakers racing to meet ambitious rollout timelines. Investments in energy transition materials testing further swell workloads. Other verticals-ICT and Telecom, Energy and Utilities, Industrial Manufacturing-continue to contribute but at lower incremental rates, ensuring diversity within the US TIC market.

By Mode of Service Delivery: Remote Formats Scale Rapidly

On-site activities held 56.85% share in 2025 because many inspections require direct asset access. Despite travel logistics, physical presence remains indispensable for weld integrity checks, structural assessments, and destructive sampling. Remote and Digital services, expanding at a 5.55% CAGR, exploit high-bandwidth networks and sensor proliferation to reduce field visits.

Providers deploy secure mobile applications and AR headsets enabling clients to livestream evidence to off-site experts. Hybrid models emerge: preliminary remote verification followed by targeted onsite follow-up. Off-site laboratories retain value for specialized analyses that demand controlled environments; however, throughput is optimized by digital intake portals and automated data processing. Combined, these advances broaden the US TIC market by integrating flexibility without sacrificing rigor.

Geography Analysis

Federal funding steers demand toward states with the largest infrastructure allocations. California, Texas, New York, Florida, and Illinois collectively attracted the bulk of awards through early 2023, concentrating materials testing and compliance workloads in their metropolitan corridors. Texas alone secured USD 31.7 billion for transportation, enhancing long-term pipelines for asphalt, concrete, and structural lab work. Parallel PFAS restrictions in California, Washington, and Maine amplify analytical chemistry requirements, bolstering revenues within highly regulated coastal markets.

Regional infrastructure quality shapes TIC needs. The American Society of Civil Engineers graded national assets a C in 2025, an uptick credited to sustained funding yet still indicative of substantial rehabilitation tasks. Harsh climates across the Midwest accelerate material degradation, spurring routine inspection contracts. Meanwhile, high-tech clusters in Arizona and Ohio experience surges in clean-room validation linked to semiconductor fabs, intensifying demand for ISO-class verification services and advanced metrology.

Labor dynamics influence capacity distribution. California’s Independent Assurance Program mandates technician certification and laboratory accreditation for highway projects, reinforcing localized compliance ecosystems. In contrast, regions with limited talent pools face longer lead-times, pushing clients to relocate testing or adopt remote oversight. The heterogeneity of state procurement rules, notably Build America Buy America content thresholds, further diversifies local service mixes, collectively shaping a geographically varied yet integrally connected US TIC market.

Competitive Landscape

The United States TIC market remains moderately concentrated. The top four global providers capture roughly one-quarter of domestic revenue, leaving ample room for midsize specialists. SGS’s January 2025 purchase of Accutest (620 employees) added extensive PFAS capabilities, echoing prior acquisitions of cybersecurity and pharma labs to build a tiered portfolio. Intertek’s 2024 acquisition of Base Met Labs signaled a pivot into battery and critical minerals testing, aligning with energy transition tailwinds. UL Solutions acquired BatterieIngenieure and is constructing a Michigan advanced battery site, underlining the strategic importance of EV supply-chain validation.

Despite expansion appetite, mega-mergers confront scrutiny. The collapsed SGS-Bureau Veritas tie-up underscores antitrust sensitivities and integration complexity.[4]SGS, “Discussions Between SGS and Bureau Veritas Have Ended,” sgs.com Domestic consolidation, therefore, favors bolt-on deals that add niche credentials without triggering regulatory backlash. Digital investment is the other battleground: platforms like Bureau Veritas QuikTrak and SGS QiiQ compete on usability, cybersecurity, and analytics depth. Success increasingly hinges on blending physical networks with virtual interfaces, ensuring coverage breadth, speed, and data integrity.

Pricing power remains balanced. Tier-one providers leverage brand trust and global accreditation portfolios, but agile regional labs win contracts through proximity, specialization, and tailored service. Talent acquisition, particularly in cyber and battery domains, is emerging as a decisive factor because expertise differentiates offerings more than commodity test methods. Collectively, these dynamics sustain a vibrant yet disciplined US TIC market.

United States Testing, Inspection, And Certification (TIC) Industry Leaders

SGS North America Inc.

Intertek USA Inc.

Bureau Veritas North America Inc.

UL LLC

Eurofins Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SGS acquired Accutest Laboratories to expand PFAS and environmental testing coverage in the United States.

- January 2025: SGS and Bureau Veritas ended merger negotiations valued at USD 33 billion, maintaining competitive balance.

- December 2024: The FCC appointed UL Solutions Lead Administrator for the U.S. Cyber Trust Mark program, formalizing its role in consumer IoT cybersecurity labeling.

- September 2024: UL Solutions completed a secondary share offering at USD 49.00 per share; proceeds went to UL Standards and Engagement.

United States Testing, Inspection, And Certification (TIC) Market Report Scope

The United States TIC market encompasses conformity assessment entities that provide various services, such as auditing, inspection, testing, verification, quality assurance, and certification. This market covers both internal and external services.

The study tracks the revenue accrued through the sale of TIC services by various players in the United States market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. It further analyses the aftereffects of COVID-19 and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The United States testing, inspection, and certification market is segmented by services type (testing and inspection services, and certification services), sourcing type (outsourced, and in-house), and by end-user vertical (retail and consumer goods, food and agriculture, oil and gas, construction and engineering, energy and chemicals, manufacturing and industrial goods, transportation (railways and logistics), automotive, and other end-user verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

How large is the US TIC market in 2026?

The US TIC market size stands at USD 38.37 billion in 2026, supported by infrastructure investments and new regulatory mandates.

What is the forecast CAGR for TIC services in the United States?

Revenue is projected to grow at a 3.45% CAGR, pushing market value to USD 45.46 billion by 2031.

Which service type is growing fastest?

Certification services are expected to record a 4.05% CAGR as cybersecurity labeling and renewable-energy compliance rise.

Why are companies increasing TIC outsourcing?

Tight labor markets and widening regulatory scope make specialized external providers more cost-effective and scalable than maintaining in-house labs.

Which industry vertical holds the largest share?

Life Sciences and Healthcare leads with 21.90% revenue, driven by stringent FDA oversight and biotech innovation.

What technologies are changing TIC delivery?

Remote inspection apps, augmented-reality audits, and IoT-based monitoring are expanding digital and hybrid service models across the US TIC market.

Page last updated on: