Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

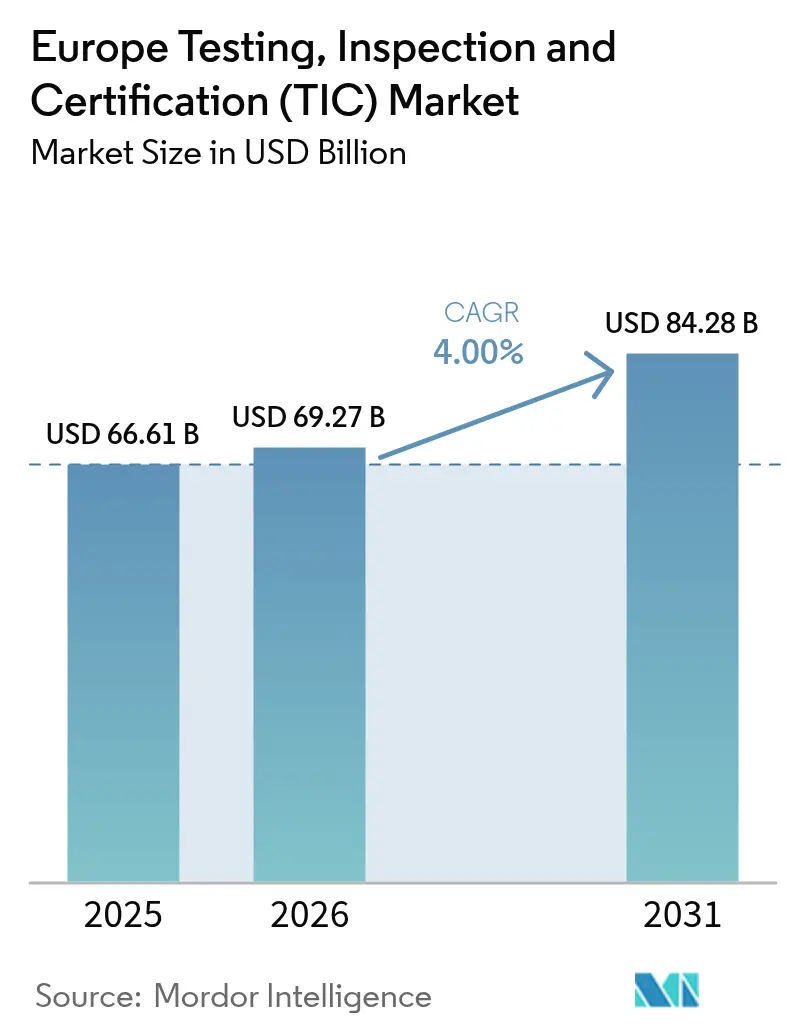

| Base Year Market Size (2025) | USD 66.61 Billion |

| Market Size (2026) | USD 69.27 Billion |

| Market Size (2031) | USD 84.28 Billion |

| Growth Rate (2026 - 2031) | 4.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Testing, Inspection And Certification (TIC) Market Analysis by Mordor Intelligence

The European TIC market size was valued at USD 66.61 billion in 2025 and estimated to grow from USD 69.27 billion in 2026 to reach USD 84.28 billion by 2031, at a CAGR of 4.00% during the forecast period (2026-2031).[1]TIC Council, “What Is the TIC Sector?,” tic-council.org The market’s structural momentum is anchored in escalating regulatory demands under the EU Digital Operational Resilience Act, Corporate Sustainability Reporting Directive, and Cyber Resilience Act, each of which now compels demonstrable third-party assurance across financial, sustainability, and connected-product domains.[2]European Parliament, “The Farm to Fork Strategy,” europarl.europa.eu Accelerated renewable-energy build-outs, a sustained shift toward outsourced verification, and the rapid emergence of AI-enabled inspection technologies further reinforce growth prospects even as economic sentiment remains uneven across member states. At the same time, the European TIC market is navigating cybersecurity constraints that temper full-scale remote inspection uptake, while cost pressures on small and medium enterprises keep price sensitivity elevated. Consolidation attempts such as the terminated SGS–Bureau Veritas merger illustrate both the strategic value and complexity of achieving scale in one of the world’s most heavily regulated business services arenas.

Key Report Takeaways

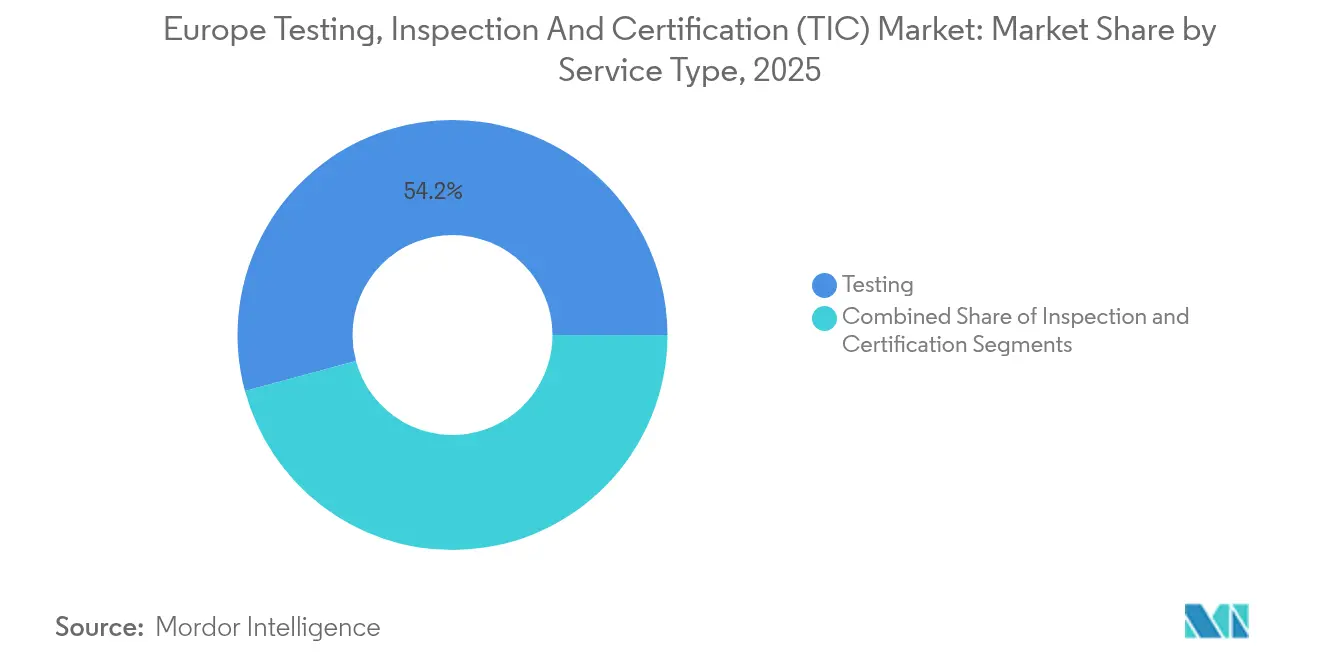

- By service type, Testing captured 54.20% of the European TIC market share in 2025; Certification is projected to expand at a 4.58% CAGR through 2031.

- By sourcing type, the outsourced segment accounted for 63.05% of the European TIC market size in 2025 and is advancing at a 4.37% CAGR over the forecast period.

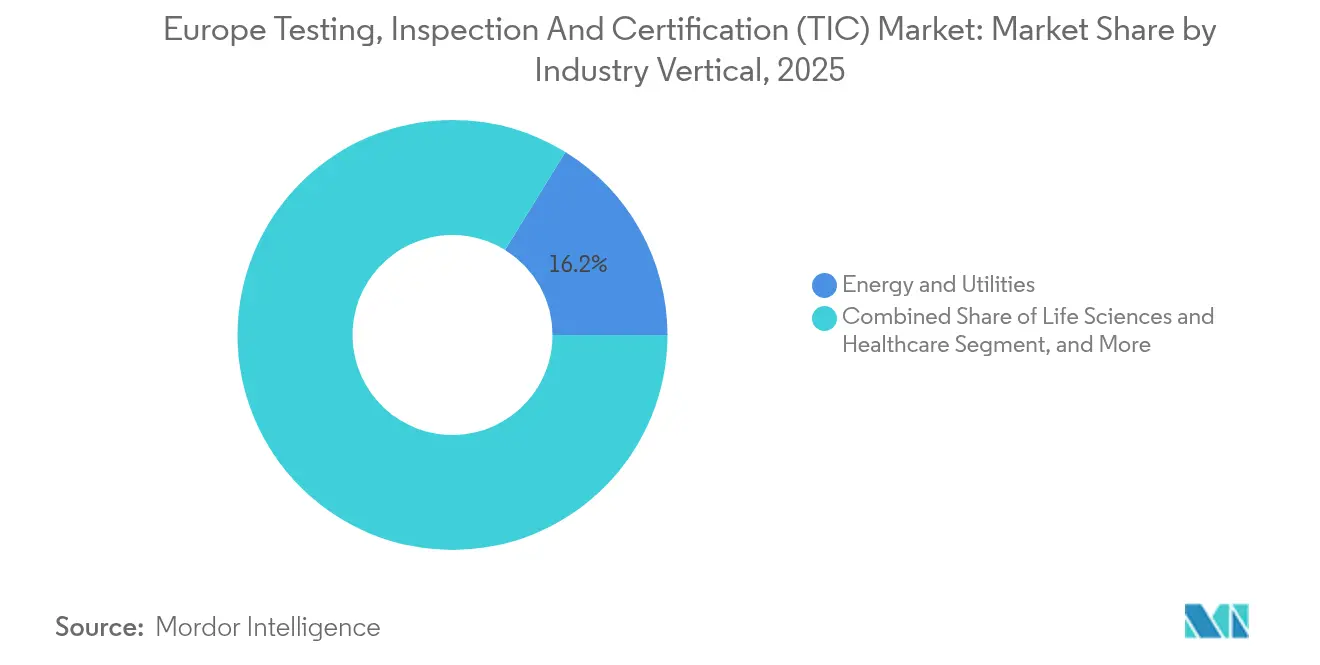

- By industry vertical, Energy and Utilities held 16.20% of the European TIC market share in 2025, while Life Sciences and Healthcare are expected to grow at a 4.92% CAGR to 2031.

- By mode of service delivery, on-site services led with 46.10% revenue share of the European TIC market in 2025; remote and digital services record the highest forecast CAGR at 4.72%.

- By country, Germany dominated with 26.95% of the European TIC market share in 2025, whereas Spain is set to post the fastest 5.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Testing, Inspection And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing regulatory compliance complexity across EU industries | +1.2% | EU core, UK, Switzerland | Medium term (2-4 years) |

| Expansion of renewable-energy projects requiring specialized certification | +0.8% | Germany, Spain, Nordics | Long term (≥ 4 years) |

| Rising outsourcing trend for TIC services among manufacturers | +0.7% | Germany, France, Italy | Short term (≤ 2 years) |

| Stringent food-safety standards under EU Farm-to-Fork strategy | +0.5% | EU-wide agri regions | Medium term (2-4 years) |

| Rapid proliferation of AI-enabled inspection drones in infrastructure maintenance | +0.4% | Northern Europe, UK | Medium term (2-4 years) |

| Emergence of ESG-linked financing mandating independent verification audits | +0.6% | London, Frankfurt, Paris | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Regulatory Compliance Complexity Across EU Industries

DORA, CSRD, and the Cyber Resilience Act became enforceable during 2024, compelling financial firms, large corporates, and connected-product manufacturers to secure multi-layered third-party assurance for ICT risk, sustainability disclosures, and product cybersecurity, respectively.[3]European Parliament, “Digital Operational Resilience Act Overview,” europarl.europa.eu Compliance budgets now allocate roughly 30% to external audits, translating into fresh revenue pools for end-to-end providers able to cover cyber, ESG, and operational-resilience scopes in a single engagement. Demand aggregation across these domains amplifies cross-selling potential, particularly for providers with integrated digital audit platforms. Because the European TIC market is one of the few service categories legally mandated for market entry, spending remains relatively inelastic even amid broader cost-containment drives. Medium-term growth, therefore, hinges on providers’ capacity to scale multidisciplinary expertise while assuring data-integrity standards acceptable to supervisory authorities.

Expansion of Renewable Energy Projects Requiring Specialized Certification

Record wind and solar build-outs under the REPowerEU plan require exhaustive verification of turbine integrity, power-curve performance, and grid-integration safety, creating high-margin opportunities for TIC specialists in marine classification and environmental impact assessment. Project developers face certification bottlenecks as national authorities uphold stringent technical codes but streamline permitting deadlines, magnifying the strategic value of accredited labs with deep domain know-how. Offshore wind growth in the North Sea alone commands premium fees because of complex subsea cabling tests and harsh-environment material qualification. As renewable-asset owners adopt AI-driven drone monitoring to manage aging fleets, certification bodies able to validate both hardware and data analytics algorithms gain a competitive advantage. The European TIC market consequently secures a long-run growth engine that is closely tied to the continent’s net-zero timetable.

Rising Outsourcing Trend for TIC Services Among Manufacturers

Capital-intensive sectors such as aerospace and automotive increasingly convert fixed in-house testing costs into variable service contracts, accelerating the shift toward outsourced verification. Element Materials Technology’s EUR 30 million Toulouse laboratory expansion illustrates the scale of investments most manufacturers prefer to avoid on their own balance sheets. Outsourcing also mitigates compliance risk because liability effectively transfers to accredited providers with globally recognized marks. For small and medium enterprises, outsourcing democratizes access to advanced analytics such as CT scanning or creep testing that would otherwise be cost-prohibitive. In response, major TIC firms are productizing “laboratory-as-a-service” models that bundle physical tests, data storage, and real-time dashboards. These offerings are strengthening customer lock-in and underpinning subscription-based revenue streams within the European TIC market.

Emergence of ESG-Linked Financing Mandating Independent Verification Audits

Banks now tie interest-rate discounts to borrowers’ verified sustainability KPIs, making third-party assurance a prerequisite for raising cheaper capital. Demand is especially pronounced in London, Frankfurt, and Paris, where green-bond issuance surged in 2024. TIC providers with proven carbon-footprint verification or supply-chain traceability services are winning multi-year audit mandates embedded into lending agreements. Early movers are packaging ESG verification with cyber-risk assessments to meet integrated risk-framework requirements under DORA, creating new cross-functional service lines. Long-term, ESG-linked financing is expected to institutionalize external verification budgets much as ISO 9001 did for quality management a generation ago.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of accreditation and certification for SMEs | -0.6% | EU-wide, Eastern Europe | Short term (≤ 2 years) |

| Fragmented regulatory framework across non-EU European states | -0.4% | UK, Switzerland, Norway, Balkans | Medium term (2-4 years) |

| Talent shortage of advanced NDT specialists | -0.3% | Germany, Northern Italy | Long term (≥ 4 years) |

| Cyber-security concerns hampering remote/digital inspections | -0.2% | Critical infrastructure EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Accreditation and Certification for SMEs

Certification expenses often equal 2-3% of SME revenue, pressuring smaller firms to postpone full compliance and, in some cases, forgo export opportunities. Multiple national accreditation bodies, despite mutual-recognition accords, still impose duplicative paperwork that raises administrative burdens.[4]TÜV NORD, “Digital Certification Services for SMEs,” tuevnord.com While digital audit portals are lowering transaction costs, the economics of maintaining ISO-accredited capacity continue to favor large service groups, creating an access gap that can inhibit broader European TIC market penetration, particularly in Eastern Europe, where purchasing power is lower.

Fragmented Regulatory Framework Across Non-EU European States

Post-Brexit divergence has introduced dual-certification requirements for goods moving between the United Kingdom and EU member states, adding time and cost to cross-border compliance workflows. Switzerland, Norway, and Balkan markets each retain unique conformity-assessment codes that fall outside EU harmonization, complicating service delivery models for TIC firms that operate pan-European networks. Although bilateral agreements mitigate some duplication, persistent fragmentation restrains scalability and erodes margins for smaller providers lacking dedicated country teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Anchors Growth Through Technical Complexity

Testing services contributed USD 36.09 billion, equivalent to 54.20% of the European TIC market in 2025, as advanced electronics, medical devices, and automotive components all require multi-disciplinary performance assessments before commercialization. Digital workflows such as cloud-based test-data portals shorten turnaround times and enhance client transparency, deepening competitive moats for early adopters. Certification, though smaller today, is forecast to compound at 4.58% annually, driven by CSRD-mandated assurance and expanding management-system standards that now cover cybersecurity, business continuity, and social responsibility. Inspection maintains steady relevance in infrastructure life-cycle management, especially in legacy manufacturing hubs where periodic structural assessments are compulsory.

Integrated platforms that unify test scheduling, real-time analytics, and certificate issuance are blurring boundaries between traditional service silos. Providers that can bundle lab tests with on-site and remote inspection in a single engagement are capturing wallet share as clients pursue one-stop compliance solutions. Investment is flowing into AI-enabled defect-recognition algorithms that raise lab throughput while preserving data integrity, reinforcing Testing’s primacy within the European TIC market.

By Sourcing Type: Outsourcing Unlocks Variable-Cost Flexibility

Outsourced verification accounted for 63.05% of the European TIC market size in 2025, reflecting a decisive shift away from capital-intensive in-house labs. Manufacturers in aerospace and automotive segments, faced with material science advances and evolving safety standards, prefer variable cost models that align spending with production volumes. Outsourced services also provide immediate access to global accreditations, which accelerate time-to-market for exports and mitigate regulatory risk.

Outcome-based contracts under which TIC firms assume compliance responsibility for a defined scope are expanding, generating recurring revenue, and incentivizing continuous process improvement. Although intellectual-property concerns keep some testing activities internal, the broader outsourcing trend is expected to sustain a 4.37% CAGR, positioning the European TIC market for stable double-digit revenue contribution from service contracts linked to long-term framework agreements.

By Industry Vertical: Energy Transition Drives Largest Revenue Pool

Energy and Utilities represented 16.20% of 2025 revenue, reflecting intensive certification needs for grid integration, turbine reliability, and environmental compliance across expanding renewable portfolios. Life Sciences and Healthcare, while smaller, is projected to deliver the highest 4.92% CAGR as the EU Medical Device Regulation tightens oversight and pandemic-era supply-chain vulnerabilities prompt broader quality-assurance spending.

Convergence of electrification, digitalization, and sustainability is opening cross-vertical opportunities: for example, battery durability tests originally used in automotive now underpin stationary-storage safety evaluations. TIC providers leveraging domain expertise across sectors can therefore cross-sell, enhancing lifetime customer value within the European TIC market.

By Mode of Service Delivery: Digital Transformation Reconfigures Operations

On-site services remained the single largest mode at 46.10% revenue share in 2025 because many hazardous-location inspections still require physical presence. Remote and digital services, however, are expanding at a 4.72% CAGR, fueled by drone-based imaging, IoT sensor feeds, and AI-driven anomaly detection that reduce travel time and carbon emissions. Off-site labs continue to underpin high-precision analytics such as PFAS testing or CT scanning.

Hybrid delivery combining sensor-enabled real-time monitoring with periodic on-site confirmation is emerging as the dominant operating model. Yet cybersecurity concerns temper adoption in critical infrastructure, underscoring the need for TIC firms to embed secure-by-design architectures and compliance with the EU Cyber Resilience Act. Providers that successfully integrate secure remote inspection workflows are poised to capture an outsized share of incremental growth in the European TIC market.

Geography Analysis

Germany held 26.95% of 2025 revenue, anchored by its dense concentration of automotive, aerospace, and chemical production and by a regulatory culture that positions TÜV-affiliated bodies as global benchmarks for conformity assessment. The Energiewende timetable and robust offshore-wind pipeline are keeping demand elevated for specialized material, grid integration, and environmental testing services. Local players increasingly partner with AI software vendors to automate field inspection reporting, sharpening competitive differentiation.

Spain is projected to log a 5.01% CAGR through 2031, the fastest among major economies, as Recovery and Resilience Facility funding accelerates digital-infrastructure and renewable-energy deployments. New battery-production capacity, notably Clarios’s EUR 200 million investment, is spurring demand for safety, environmental, and supply-chain assessments, translating into multi-year frameworks for TIC providers. Spain’s export-oriented agrifood sector further boosts inspection volumes under EU Farm-to-Fork traceability mandates.

France, Italy, and the United Kingdom each command high-single-digit shares, supported by diversified industrial bases and specialized aerospace, luxury goods, and biotech niches that require advanced conformity services. Post-Brexit divergence forces dual certification on UK-EU trade flows, enlarging total addressable spend for providers able to navigate both regimes efficiently. Eastern European markets remain smaller but are growing steadily as EU accession and nearshoring trends drive supply-chain localization, reinforcing a positive outlook for the Europe TIC market through 2031.

Regulatory Landscape

Europe’s TIC demand is increasingly shaped by EU-level conformity assessment and assurance requirements that span cyber, sustainability, and product safety. For digital products and connected equipment, the Cyber Resilience Act formalizes obligations for products with digital elements and clarifies when manufacturers can rely on internal control versus when a notified body is needed for EU-type examination, based on criticality. This pulls cybersecurity testing and certification deeper into go-to-market processes.

Cybersecurity certification is also being standardized through ENISA-linked schemes under the European Cybersecurity Certification Framework, including the EUCC (Common Criteria-based) scheme grounded in ISO/IEC Common Criteria. In December 2025, the European Commission adopted a second amendment to EUCC, updating definitions and continuity provisions. In January 2026, the Commission advanced COM(2026) 13 final to revise the Cybersecurity Act framework and ENISA mandate, positioning certification more explicitly as a compliance tool alongside broader security obligations.

Value Chain Analysis

The Europe TIC value chain starts with regulation and standards setting (EU law, harmonized standards, and sector standards such as IEC 62443 and Common Criteria), then moves through accreditation and notified-body designation, and finally to service execution across labs, on-site inspection, and remote and digital delivery. TIC providers rely on inputs such as calibrated instrumentation, secure data platforms for evidence handling, and scarce technical talent (notably NDT and cybersecurity evaluators), while demand comes from OEMs, network operators, hyperscalers, and infrastructure owners that need third-party proof for market access and risk transfer.

Downstream, buyers are embedding TIC into digital transformation and infrastructure lifecycle programs, which is tightening integration between engineering workflows and assurance delivery. Several ecosystem moves are influencing how TIC work is specified and consumed, including Bouygues Group partnering with AWS (February 2025) to accelerate AI-enabled transformation across telecom and media operations, TCS launching a telecom lease management platform with Vantage Towers (March 2025), and ASML and imec signing a 5-year R&D partnership (March 2025) for advanced semiconductor technology. These initiatives raise requirements for secure test data, repeatable validation, and specialized certification across complex supply chains.

Competitive Landscape

The five largest operators, SGS, Bureau Veritas, Intertek, DEKRA, and TÜV SÜD, collectively account for roughly 35% of 2024 revenue, demonstrating moderate concentration yet leaving ample space for specialist and regional firms. SGS posted CHF 6.79 billion (USD 7.47 billion) in 2024 revenue and executed 11 acquisitions targeting digital and sustainability niches, but ultimately terminated merger talks with Bureau Veritas because of antitrust and valuation hurdles. Bureau Veritas, meanwhile, generated EUR 6.24 billion (USD 6.86 billion) and completed 10 bolt-on deals while divesting non-core food-testing assets to sharpen focus on higher-growth verticals.

Strategic focus areas include AI-driven defect recognition, cybersecurity assurance, and ESG verification. Intertek is investing in “Assurance-as-a-Service” platforms that combine audit, certification, and continuous monitoring in a subscription model. Regional consolidators such as Nordic Inspekt Group are purchasing niche NDT specialists to secure scarce talent and proprietary methods, a trend likely to continue given the aging workforce. Entry barriers remain high due to accreditation requirements and deeply entrenched regulatory relationships, yet white-space opportunities exist in quantum-device testing, circular-economy certification, and AI system validation where incumbents lack mature offerings, paving the way for innovative entrants to capture share within the European TIC market.

Europe Testing, Inspection And Certification (TIC) Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity area is conformity assessment and assurance for digital regulation packages that broaden the need for independent verification beyond traditional physical testing. The EU AI Act creates a new assurance layer for high-risk AI systems (risk management, documentation, and compliance evidence), while the Cyber Resilience Act increases the addressable scope for cybersecurity testing and, for certain categories, third-party involvement via notified bodies. This supports TIC providers that can combine product cybersecurity evaluation, software lifecycle evidence collection, and secure remote audit workflows in a single engagement, especially where clients want to reduce duplicated audits across overlapping regimes.

Infrastructure modernization and regulatory streamlining also create whitespace for TIC offerings positioned between engineering delivery and compliance. In January 2026, the European Commission proposed the Digital Networks Act to consolidate key connectivity-related frameworks into a single regulation, which increases demand for integrated testing that spans network deployment readiness, cybersecurity controls, and operational resilience. Separately, in June 2026, ETIX moving to acquire four Eurofiber datacenters in France highlights continued build-out and consolidation of sovereign digital infrastructure, supporting recurring inspection, commissioning tests, and compliance monitoring across facilities and critical systems.

Recent Industry Developments

- March 2026: SGS completed the acquisition of Granite River Labs Services, adding high-speed connectivity testing capabilities to its Digital Trust and Connectivity activities. The acquisition expands SGS coverage across wireless, wired, and device interoperability assurance used by manufacturers to accelerate certification and market access in Europe.

- January 2026: SGS announced the acquisition of Panacea Infosec in India to strengthen Digital Trust offerings in payment security and information security assurance. Scaling cybersecurity assurance capacity supports European clients with globally distributed product development and compliance programs.

- December 2025: Bureau Veritas, Advantech, and MediaTek achieved IEC 62443-4-2 certification for an Arm-based industrial platform. The certification milestone reflects industry alignment on product security controls with emerging EU cybersecurity compliance requirements and expands the pool of certified industrial platforms available for European deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers third party revenues earned from testing, inspection, and certification services delivered to European customers for compliance, quality, safety, and performance needs, across industrial and consumer end uses.

Scope exclusions: We exclude internal (in-house) cost centers when they do not generate external service revenue, and we exclude pure consulting that is not tied to an auditable TIC engagement.

Segmentation Overview

- By Service Type

- Testing

- Inspection

- Certification

- By Sourcing Type

- In-house

- Outsourced

- By Industry Vertical

- Consumer Goods and Retail

- ICT and Telecom

- Automotive and Transportation

- Aerospace and Defense

- Oil, Gas and Petrochemicals

- Energy and Utilities

- Industrial Manufacturing and Machinery

- Chemicals and Materials

- Construction and Infrastructure

- Life Sciences and Healthcare

- Food, Agriculture and Beverage

- Other Industry Verticals (Environment, Sustainability, etc.)

- By Mode of Service Delivery

- On-site

- Off-site / Laboratory

- Remote / Digital

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to frame the demand pool for Europe TIC services and to understand where regulation and trade create recurring testing and certification needs. Public sources such as Eurostat industry output and trade series, the European Commission legal and policy publications, and national statistics offices help size the industrial base that most often triggers inspections and audits.

We also review sources such as European and national accreditation-body registers and guidance, notified-body listings where relevant, and standards publications from ISO and IEC to track which conformity pathways are active. Company annual reports, investor presentations, association websites, and reputable press coverage are used to interpret service mix shifts and pricing direction, and then the inputs are cross-checked using paid subscriptions only for company financials and news context. This list is not exhaustive, and many other sources were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary interviews and surveys are used to validate how outsourced versus in-house activity is counted in practice, and how contract renewals move pricing for different TIC service lines across Europe. We cover respondents from service providers, accreditation and quality teams, procurement functions, and operational users in industries such as manufacturing, energy, and consumer goods, so gaps from desk sources can be filled and then reconciled back into the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | |

| Mid tier: 55% | Functional/Unit leaders: 27% | |

| Smaller Players: 14% | Managers: 60% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach, where Europe's regulated activity and industrial output indicators are translated into a serviceable TIC demand pool, and then converted into revenue using realistic utilization and price assumptions. For the top-down build, we link end-market activity to TIC intensity using variables such as outsourcing penetration by industry, inspection or recertification frequency, audit-day or per-sample volumes, and the share of projects that require third-party certification for market access.

Selective bottom-up approximations are then used to corroborate totals, including sampled provider revenue splits from public disclosures, country-level rollups where financials are visible, and simple volume times average price checks for common testing categories. Where private-company disclosure is thin, we fill gaps using ratios guided by accreditation coverage and the local industry mix, and those ratios are refined after expert feedback.

Forecasts are developed using scenario analysis, since demand is shaped by a few observable drivers that can shift with policy and industrial cycles. Inputs commonly include manufacturing output direction, EU regulatory rollouts that expand conformity needs, renewable and grid investment inspection requirements, and trade complexity that increases verification work, with assumptions aligned to what interviewees expect for capacity and pricing over the forecast window.

Data Validation & Update Cycle

Validation is done by comparing model outputs with independent signals such as provider revenue direction, visible accreditation activity, and whether country totals match known industrial concentration. When a variance looks high, the drivers are re-checked, and then the assumptions are reviewed in a second analyst pass before sign-off.

The report is refreshed annually, with interim updates triggered by material events such as sharp currency moves, major regulatory enforcement changes, or step-changes in outsourcing behavior. Before delivery, we perform a fresh check of key inputs and the latest public information so clients receive an up-to-date view.

Mordor Intelligence's Europe Testing Inspection and Certification Market Size Compared Against Other Published Estimates

Published values for the Europe TIC market can diverge because the counted service set is not always the same, and because authors anchor on different years and conversion windows when reporting USD totals. The gap also widens when one estimate smooths price progression evenly, even though many TIC contracts reset pricing around renewal cycles.

Refresh cadence matters in this market because contract repricing, compliance deadlines, and exchange-rate windows can shift the reported USD value in a short period. By rechecking renewal-led ASP steps, aligning currency timing to the base-year reporting window, and running variance follow-ups on outlier country totals, Mordor Intelligence keeps the 2025 figure closer to what providers could actually bill for TIC service work in Europe.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 66.61 B (2025) | |

| Global Consultancy A | USD 56.99 B (2025) | This estimate appears to use a broader TIC-style bundle that can include adjacent services like training and consulting, and it applies a lower growth and pricing progression, which can reduce the 2025 USD total if renewal-step pricing is smoothed and currency timing differs. |

| Regional Advisory B | USD 59.19 B (2024) | This figure is anchored to 2024 rather than a 2025 base year, so it may not capture later contract repricing and compliance-led volume increases. Differences can also come from how outsourced revenue is separated from in-house activity when building the market value. |

Across sources, the spread is mainly explained by year anchoring, what is counted as TIC service revenue versus adjacent support work, and how pricing progression is handled during renewal periods. The methodology used here keeps inputs tied to observable demand signals and repeatable checks, which makes the final total easier to reconcile back to clear assumptions.

Key Questions Answered in the Report

How large is the Europe TIC market in 2026?

The Europe TIC market size is valued at USD 69.27 billion in 2026 and is projected to reach USD 84.28 billion by 2031 at a 4.00% CAGR.

Which country contributes the most revenue to European TIC services?

Germany leads with 26.95% share, supported by its large industrial base and strict quality-assurance culture.

What segments are growing fastest within European TIC services?

Certification services are set to expand at a 4.58% CAGR, while remote and digital delivery modes advance at 4.72% CAGR.

Why are manufacturers outsourcing TIC activities?

Outsourcing converts fixed testing costs into variable expenses, accelerates access to global accreditations, and transfers regulatory liability to expert providers.

How is renewable energy driving TIC demand?

Offshore wind, solar, and grid-integration projects require extensive safety, performance, and environmental certification, establishing a long-term growth engine for specialized TIC services.

Page last updated on: