India Testing, Inspection, And Certification (TIC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

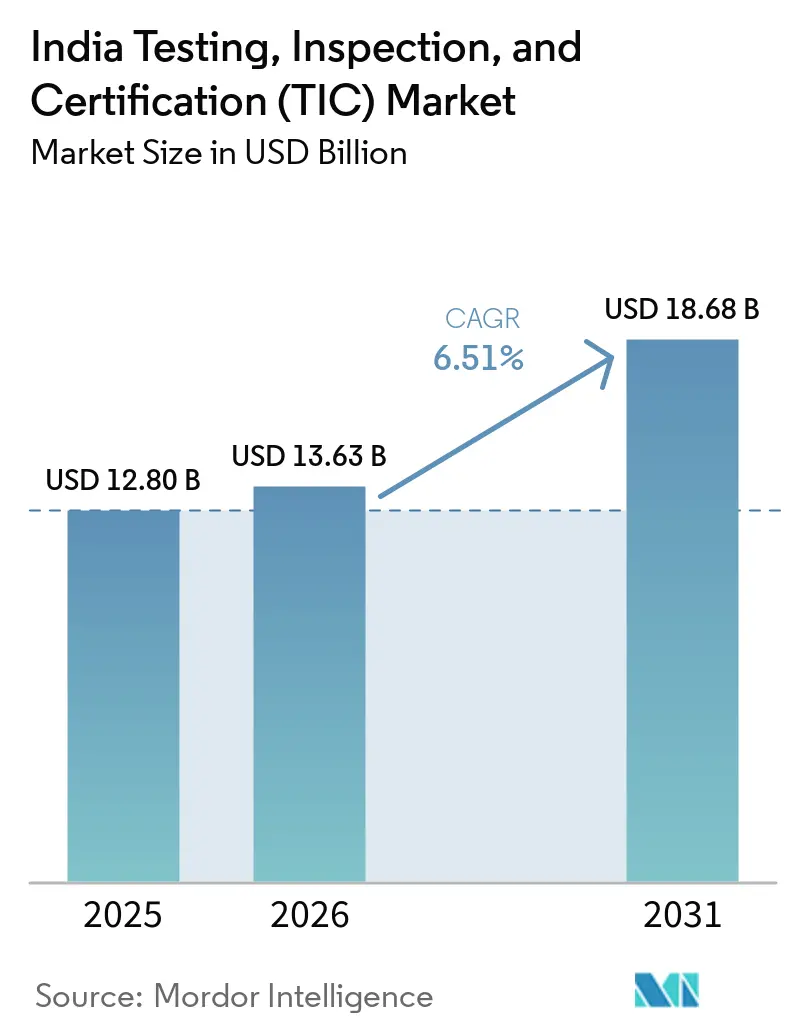

| Base Year Market Size (2025) | USD 12.80 Billion |

| Market Size (2026) | USD 13.63 Billion |

| Market Size (2031) | USD 18.68 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

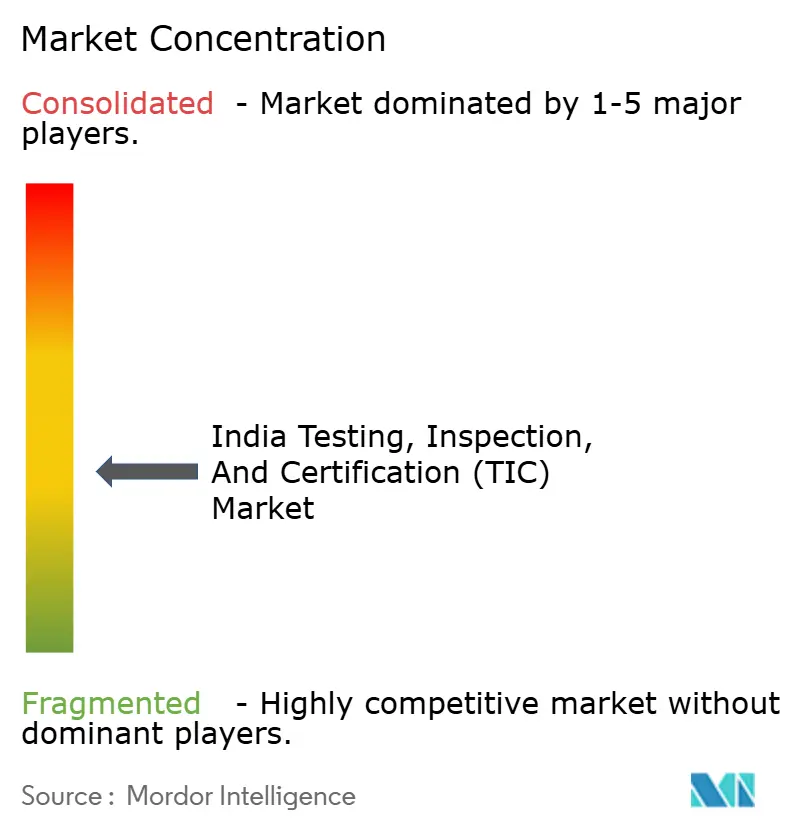

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Testing, Inspection, And Certification (TIC) Market Analysis by Mordor Intelligence

The India testing, inspection, and certification (TIC) market size is expected to increase from USD 12.8 billion in 2025 to USD 13.63 billion in 2026 and reach USD 18.68 billion by 2031, growing at a CAGR of 6.51% over 2026-2031. Robust enforcement of new Quality Control Orders, subsidies that convert compliance into an export incentive, and rapid adoption of digital assurance platforms are pulling demand forward. Expanded BIS oversight across 769 products, government funding that refunds up to 75% of certification costs, and the arrival of indigenous calibration capacity for air-pollution equipment all translate into more frequent, multi-standard audits and repeat certification cycles. At the same time, a pivot toward capital-light operations pushes manufacturers to outsource lab work so they can tap into specialized accreditations without new capex. Global majors deepen their footprints through targeted acquisitions in solar, EMC, and cybersecurity, while domestic laboratories use niche expertise and regional proximity to stay relevant. The upshot is a market where regulatory stringency and digital modernization combine to keep pricing power intact for accredited providers even as competitive intensity rises.

Key Report Takeaways

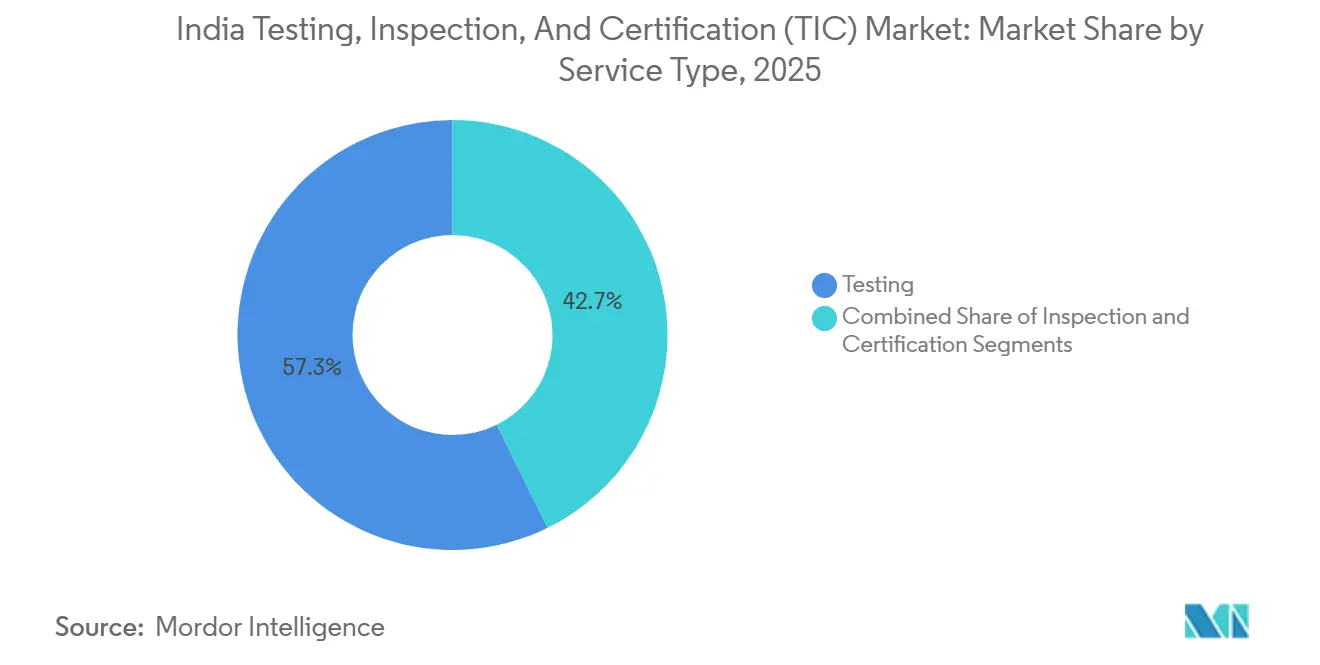

- By service type, testing led with 57.31% share of the India testing, inspection, and certification market in 2025, whereas certification is the fastest-growing segment with a 6.91% CAGR through 2031.

- By sourcing type, outsourced services commanded 65.21% of India testing, inspection, and certification market share in 2025 and are advancing at a 7.11% CAGR to 2031.

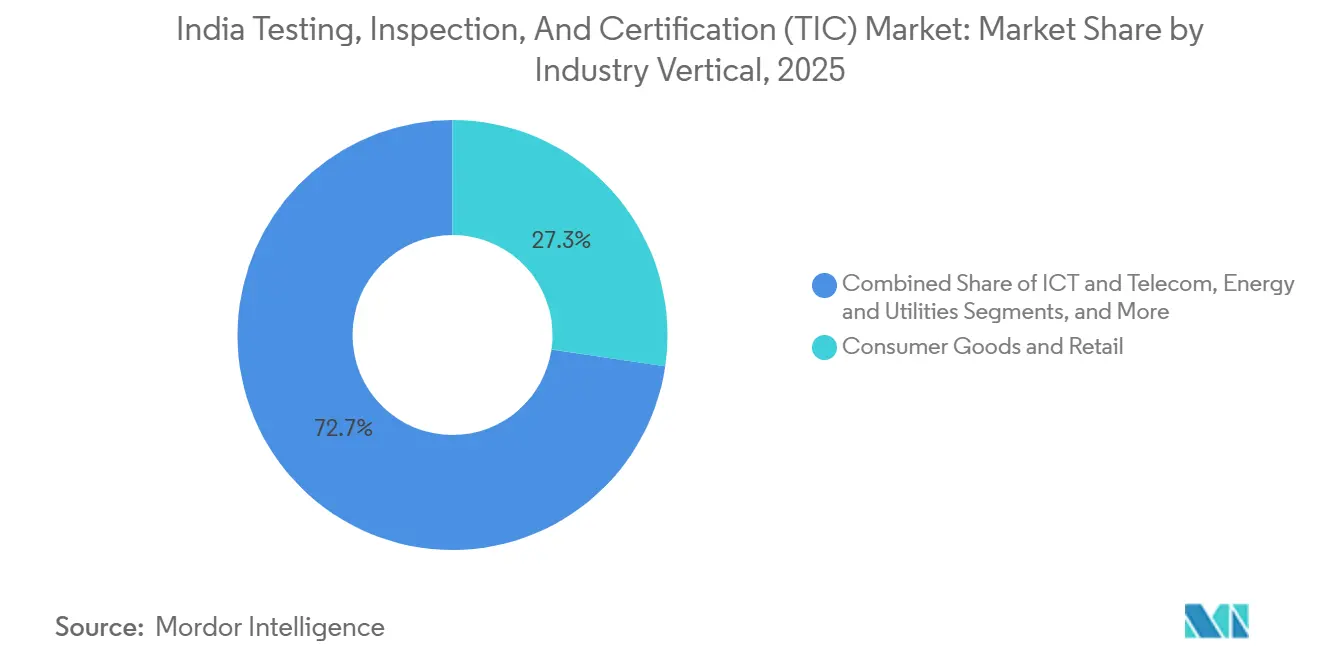

- By industry vertical, consumer goods and retail accounted for 27.32% revenue in 2025, while life sciences and healthcare is projected to expand at a 6.89% CAGR during 2026-2031.

- By mode of service delivery, on-site inspection retained 46.76% share in 2025, yet remote and digital services are set to grow at a 7.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Testing, Inspection, And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Regulatory Enforcement Across Indian Industries | +1.2% | National, concentrated in Maharashtra, Gujarat, Tamil Nadu, Karnataka | Short term (≤ 2 years) |

| Growing Outsourcing of TIC by Exporters and OEMs | +1.0% | National, export hubs in Gujarat, Tamil Nadu, Maharashtra, Haryana | Medium term (2-4 years) |

| Rapid Growth of Life Sciences and Healthcare Sector | +0.8% | National, clusters in Hyderabad, Bengaluru, Ahmedabad, Mumbai | Medium term (2-4 years) |

| Expansion of Consumer Goods and Retail Requiring Compliance | +0.7% | National, e-commerce centers in Delhi NCR, Bengaluru, Mumbai | Short term (≤ 2 years) |

| Digital Bharat Push Enabling Remote and AI-Driven Inspections | +0.5% | National, early adoption in metros and industrial corridors | Long term (≥ 4 years) |

| Surge in ESG-Linked Audits from Lenders and PE Investors | +0.4% | National, focus on large corporates in manufacturing, energy, infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Enforcement Across Indian Industries

BIS inspections uncovered 142 non-compliant items on major e-commerce sites, putting platforms on notice and widening demand for third-party verification. The March 2025 Quality Control Orders added 769 products to mandatory certification, instantly pulling manufacturers of hand tools, aluminum goods, and household appliances into the compliance net. Revised 2025 solar-module guidelines toughened performance tests just as domestic capacity scaled, requiring fresh rounds of conformity assessments before modules could ship.[1]Mercom India, “Revised 2025 Guidelines for Solar Module Series Approval,” mercomindia.com Parallel scrutiny from export markets forces firms to layer foreign standards atop domestic ones, multiplying the volume of test reports they must secure. This synchronized enforcement at home and abroad ensures a durable pipeline for accredited laboratories able to cover BIS, IEC, and destination-market norms.

Growing Outsourcing of TIC by Exporters and OEMs

Government reimbursement of certification fees turns outsourced assurance into a subsidized service, making it financially irrational for most MSMEs to maintain internal labs. Automotive OEMs exemplify the shift, funneling battery-safety and homologation work to ARAI, which logged a 19% revenue jump as a result. Global TIC majors keep pace: a EUR 15 million (USD 16 million) Bengaluru complex by TÜV SÜD centralizes EMC and medical-device testing, while Intertek’s purchase of a solar PV lab in Ahmedabad offers one-stop BIS and IECEE approvals. Manufacturers increasingly view external labs as an elastic cost that flexes with output, grants faster time-to-market, and instantly opens access to coveted international accreditations.

Rapid Growth of Life Sciences and Healthcare Sector

Eurofins launched India’s first GLP-compliant bioanalytical hub, giving pharmaceutical sponsors local access to services once sourced overseas. CDSCO tightened device rules that mandate pre-market biocompatibility and post-market surveillance, channeling work into NABL-accredited facilities. Updated NABL criteria now demand proficiency testing and SI-unit traceability, pressuring smaller medical labs to upgrade or exit. NDDB’s CALF lab in Kochi begins with dairy but plans to span spices, seafood, and produce, mirroring export markets that insist on third-party certificates for contaminants. Together, these moves cement life sciences as the fastest-rising vertical within the India TIC market.

Expansion of Consumer Goods and Retail Requiring Compliance

Section 17 of the BIS Act shifts liability to online marketplaces, so platforms pre-screen sellers and demand valid certification before listing. New QCOs for appliances and tools swell the number of SKUs requiring lab tests prior to sale. FSSAI’s NABL mandate forced roughly 200 unaccredited food labs out, channeling business to certified providers that can clear products for both domestic shelves and foreign customs. Government funding for 100 new food labs in FY 2025-26 aims to plug geographic gaps, yet simultaneously raises the compliance baseline. Retailers also hard-wire supplier certification into private-label contracts, ensuring a stable revenue stream for labs with nationwide footprints and quick turnarounds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Qualified Inspectors and Lab Analysts | -0.6% | National, acute in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Fragmented Lab Infrastructure and Inconsistent Quality | -0.5% | National, concentrated in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Slow NABL and BIS Accreditation Turnaround Times | -0.3% | National, affecting new lab entrants and capacity expansions | Medium term (2-4 years) |

| Price-Cutting by Unaccredited Local Labs Eroding Margins | -0.2% | National, pronounced in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified Inspectors and Lab Analysts

Revised accreditation rules heightened the skill bar just as demand spiked, leaving the country short by around 10,000 qualified professionals.[2]National Accreditation Board for Testing and Calibration Laboratories, “Revised Accreditation Criteria for Medical Testing Laboratories 2025-2026,” nabl-india.org Large expansions, such as TÜV SÜD’s 70,000-square-foot site, required nine-month hiring cycles to fill specialized EMC roles. New regional labs like CPRI Nashik had to borrow engineers from other sites, illustrating internal cannibalization. Scarcity is acute in non-destructive testing, where Level III technicians cluster in metros and command premium wages, swelling certification queues during seasonal peaks. The mismatch between talent supply and industry need stretches turnaround times and occasionally forces clients toward unaccredited alternatives despite the risks.

Fragmented Lab Infrastructure and Inconsistent Quality

Only about one-third of India’s 1,200-plus labs carry NABL seals, and inter-laboratory audits regularly expose wide result swings on identical samples. Many of the 205 labs funded under food-processing schemes lack instrumentation to meet U.S. or EU residue norms, causing exporters to reroute samples to metro labs. Closure of unaccredited food labs after the FSSAI ruling created temporary capacity vacuums, lengthening queues for dairy and spice exporters. Regional disparities persist: accredited metro facilities boast climate-controlled environments and digital LIMS, while tier-2 labs struggle with calibration and documentation, leading to repeat tests and higher costs for manufacturers. The new National Environmental Standard Laboratory shows what world-class infrastructure can achieve, but scaling this model nationwide demands sustained investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Gains as Export Documentation Intensifies

Certification captured growing relevance as export markets insisted on third-party attestations tied to ESG and product-safety norms. While testing still represented 57.31% of the India TIC market in 2025, certification revenue is rising faster because surveillance audits and management-system renewals generate steady annuities. Subsidies under the TRACE scheme reposition certification from discretionary spend to strategic advantage, especially for MSMEs chasing European and North American orders. Inspection remains critical in construction, energy, and machinery, yet rising drone and AI use trims labor hours and lifts margins.

Certification momentum draws strength from lender-mandated ESG audits and programs such as GRIHA’s Decarbonizing Habitat tiers. Intertek’s CarbonClear and CarbonZero offerings cater to exporters needing verified low-carbon labels to pass buyer scorecards. Testing keeps its primacy through ever-widening QCO coverage that mandates laboratory analysis before goods hit shelves, but certification now delivers the sharper growth slope, anchoring long-term order books for providers with deep multi-standard portfolios.

By Sourcing Type: Outsourced Services Dominate as Capital-Light Models Prevail

Outsourced contracts owned 65.21% share in 2025 and are forecast to rise at 7.11% CAGR, underscoring how firms favor variable costs and instant access to accreditations. Automotive, renewable energy, and consumer-goods exporters outsource whole compliance cycles to avoid multimillion-dollar outlays on EMC chambers, vibration rigs, or bioanalytical suites. The India TIC market size attached to outsourced work keeps expanding as policies like the TRACE subsidy tilt the economics decisively away from in-house builds.

Large manufacturers still keep pilot-phase labs for R&D, yet final conformity is usually entrusted to external bodies whose certificates regulators and overseas buyers recognize. Network effects accrue to global majors running 25-plus sites nationwide, enabling one-stop assurance and uniform quality. Revised NABL rules further hobble smaller corporate labs, steering even conservative firms toward accredited outsourcers that can clear products for multiple jurisdictions in a single engagement.

By Industry Vertical: Life Sciences Outpaces Consumer Goods Despite Smaller Base

Consumer goods and retail remained the revenue leader at 27.32% in 2025, benefiting from stringent e-commerce policing and sweeping BIS mandates. However, life sciences and healthcare are pacing the field with a 6.89% CAGR. Pharma sponsors now conduct bioequivalence, biomarker, and toxicology studies domestically at Eurofins’ GLP site, avoiding costly overseas slots. Medical-device makers must clear tougher CDSCO protocols, pushing steady flows to labs versed in ISO 10993 and IEC 60601.

Automotive retains heft thanks to battery-safety and ADAS testing, illuminated by TÜV Rheinland’s multi-discipline Manesar hub. Solar module makers drive energy-vertical demand after rule changes that require BIS and IEC conformity for every capacity band, with Intertek’s new Ahmedabad center poised to capture volume. Food safety continues to tighten under FSSAI, deepening the client base for accredited laboratories across India’s agri-export belt.

By Mode of Service Delivery: Remote and Digital Surge as Technology Adoption Accelerates

Physical on-site work still held 46.76% share in 2025 but growth tilts to remote and digital workflows advancing at 7.23% CAGR. Drone flyovers, AI-based visual inspections, and video audits shrink time on-site and reduce exposure risks in petrochemical tanks or high-rise facades. The Digital Bharat initiative strengthens uptake by embedding e-signatures and blockchain validation into compliance portals, letting regulators verify certificates instantly.

Laboratory testing remains inherent for destructive or high-precision tasks, yet even here digital LIMS and robotic sample handling elevate throughput. Clients accept remote surveillance for ISO management audits and supplier screenings, particularly after the pandemic normalized video evidence. Remaining hurdles, like witness testing for pressure vessels, keep physical visits relevant, but the share shift is unmistakable as customers chase speed and lower travel costs.

Geography Analysis

Maharashtra, Gujarat, Tamil Nadu, Karnataka, and Haryana together generated roughly 60% of India's testing, inspection, and certification market demand in 2025. Mumbai-Pune’s automotive and electronics belt leans on sizable SGS and Intertek labs, while Gujarat’s chemical and solar exporters benefit from Ahmedabad’s new PV testing center. Chennai-Coimbatore’s vehicle corridor and Bengaluru’s ICT and bio-pharma clusters underpin steady order books for TÜV SÜD, Eurofins, and Bureau Veritas.

Second-tier cities are climbing the value chain. CPRI’s Nashik laboratory trims lead times for western India’s transformer makers.[3]Press Information Bureau, “Union Minister Inaugurates CPRI Regional Testing Laboratory at Nashik,” pib.gov.in Kochi’s CALF facility caters to dairy and spice exporters that previously shipped samples to metros. Indore’s NATRAX site offers battery safety, and ADAS tracks that attract central-India automakers. Government plans for 100 new NABL food labs in FY 2025-26 will shift more compliance activity into agricultural heartlands spanning Punjab, Uttar Pradesh, and Andhra Pradesh.

Despite gains, tier-3 regions still rely on mobile labs and remote audits because accredited infrastructure remains thin. Export-heavy hubs such as Tirupur textiles or Surat diamonds queue for certification slots during seasonal peaks, a gap the TRACE subsidy and new lab projects aim to close. Over the forecast horizon, digital channels will help decentralize access, but physical capacity additions in underserved states will remain critical to unlock full demand potential.

Competitive Landscape

Global majors, SGS, Bureau Veritas, Intertek, TÜV SÜD, TÜV Rheinland, UL, DNV, and DEKRA, jointly hold about 40-45% of the India testing, inspection, and certification market, while regional specialists fill gaps in maritime classification, metals testing, and local regulatory know-how. Strategy hinges on capability deepening and geographic reach: SGS bought cybersecurity firm Panacea Infosec to chase CHF 200 million (USD 220 million) in digital-trust revenue by 2027, and closed the USD 1.33 billion ATS deal to bulk up North-American earnings that flow into global client contracts.[4]SGS, “SGS Expands Digital Trust Leadership with Acquisition of Panacea Infosec in India,” sgs.com

Intertek doubled down on high-growth niches with an 11,000-square-foot EMC lab in Bengaluru and the acquisition of Mitsui Chemicals’ solar facility in Gujarat, aligning with India’s push for electronics self-reliance and 500 GW of renewable capacity by 2030. TÜV Rheinland answered with an automotive component complex in Manesar that folds structural, corrosion, and environmental simulations into one roof, accelerating EV part homologation.

Technology adoption distinguishes leaders: AI-guided inspections, blockchain certificates, and carbon-intensity labels create defensible service tiers beyond price competition. Private equity interest, evident in QIMA’s purchase of EFRAC and KKR’s USD 250 million TIC platform, signals an active consolidation pipeline. Regulatory barriers, 12-18-month accreditation cycles, and mandatory proficiency testing continue to protect incumbents from rapid new-entrant encroachment, sustaining moderate pricing power even as the field broadens.

India Testing, Inspection, And Certification (TIC) Industry Leaders

SGS India Pvt. Ltd.

Bureau Veritas (India) Pvt. Ltd.

Intertek India Pvt. Ltd.

TÜV SÜD South Asia Pvt. Ltd.

TÜV Rheinland India Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: TÜV Rheinland opened an advanced automotive component testing laboratory in Manesar, Haryana, pooling structural, corrosion, durability, and environmental simulation under one roof to speed EV component releases.

- April 2026: Intertek inaugurated its first dedicated EMC laboratory in Bengaluru, featuring a 3-meter semi-anechoic chamber capable of radiated spurious emission tests up to 40 GHz.

- April 2026: Intertek acquired the ISO/IEC 17025-accredited solar PV testing assets of Mitsui Chemicals in Ahmedabad, strengthening on-shore module conformity programs.

- January 2026: SGS completed the USD 1.325 billion purchase of Applied Technical Services, adding 2,100 staff and advancing its Strategy 27 revenue goals.

India Testing, Inspection, And Certification (TIC) Market Report Scope

The Testing, Inspection, and Certification (TIC) Market refers to the global industry that provides services ensuring products, systems, and processes meet regulatory standards, quality benchmarks, and safety requirements across diverse sectors such as manufacturing, healthcare, automotive, energy, consumer goods, and construction.

The India Testing, Inspection, and Certification (TIC) Market Report is Segmented by Service Type (Testing, Inspection, Certification), Sourcing Type (In-house, Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Automotive and Transportation, Aerospace and Defense, Oil, Gas and Petrochemicals, Energy and Utilities, Industrial Manufacturing and Machinery, Chemicals and Materials, Construction and Infrastructure, Life Sciences and Healthcare, Food, Agriculture and Beverage, Others Industry Verticals), Mode of Service Delivery (On-site, Off-site/Laboratory, and Remote/Digital). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others Industry Verticals |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others Industry Verticals | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

What is the current India testing, inspection, and certification market size and its expected value by 2031?

The India testing, inspection, and certification market size is expected to increase from USD 12.8 billion in 2025 to USD 13.63 billion in 2026 and reach USD 18.68 billion by 2031, growing at a CAGR of 6.51% during the forecast period.

Which service segment is growing the fastest through 2031?

Certification services are expanding at a 6.91% CAGR, the quickest among all service categories, due to export documentation and ESG-linked audit requirements.

Why are outsourced TIC services gaining share in India?

Manufacturers favor outsourcing to avoid heavy capital outlays, tap specialized accreditations instantly, and leverage government subsidies that refund up to 75% of certification costs.

Which industry vertical is expected to see the highest growth?

Life sciences and healthcare leads growth at a 6.89% CAGR, driven by tighter CDSCO rules and new GLP-compliant labs that support clinical research and medical-device testing.

How is technology changing service delivery in the India TIC space?

Drone surveys, AI-enabled visual inspections, and blockchain-based certificate validation are accelerating remote audits, reducing site-visit costs, and shortening compliance cycles.

What are the main restraints holding back market growth?

A persistent shortage of qualified inspectors and fragmented lab infrastructure in tier-2 and tier-3 cities lengthen turnaround times and introduce quality inconsistencies across regions.

Page last updated on: