Market Overview

| Study Period | 2020 - 2031 |

|---|---|

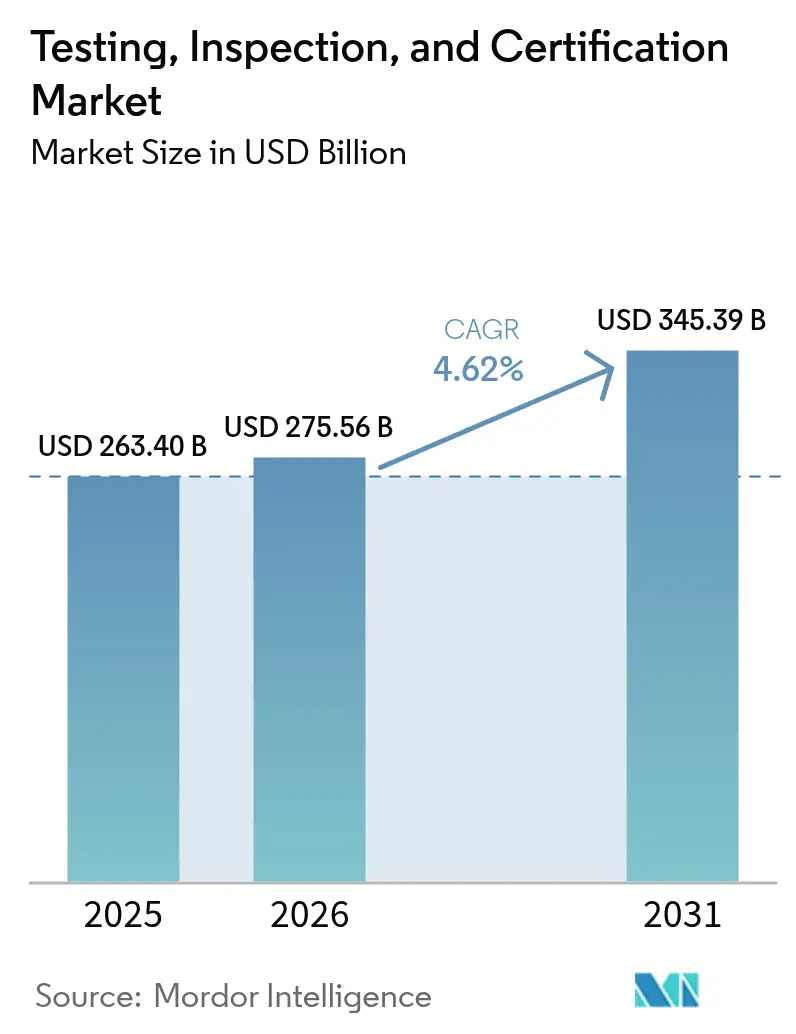

| Market Size (2026) | USD 275.56 Billion |

| Market Size (2031) | USD 345.39 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

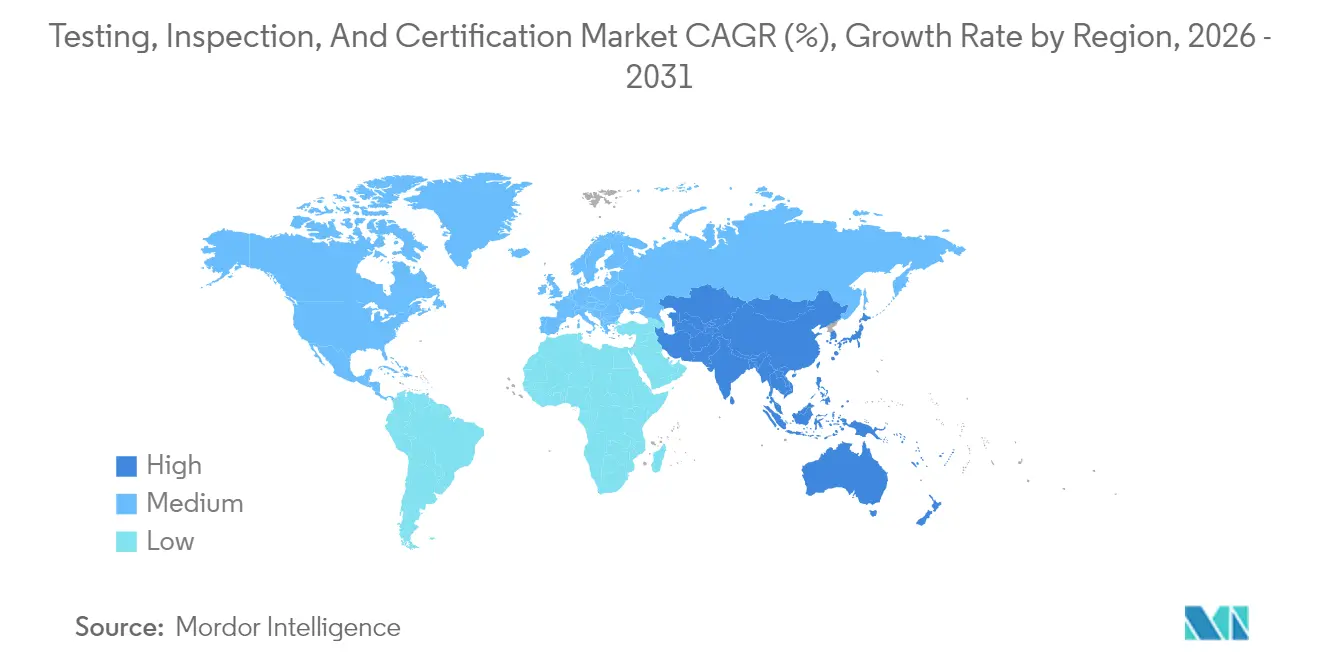

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Testing, Inspection, And Certification Market Analysis by Mordor Intelligence

The testing inspection certification market size is expected to grow from USD 263.40 billion in 2025 to USD 275.56 billion in 2026 and is forecast to reach USD 345.39 billion by 2031 at 4.62% CAGR over 2026-2031. Escalating regulatory scrutiny, rising product-safety expectations, and digital transformation are strengthening demand for independent assurance services across consumer goods, electronics, energy storage, and automotive value chains. Mandatory ESG and carbon-footprint verification requirements, tighter cybersecurity rules for connected products, and the complexity of globalized supply networks are compelling firms to rely on accredited third parties. Strategic consolidation combined with AI-enabled inspection technologies is allowing market leaders to widen service scope and improve efficiency. At the same time, cost pressures and talent shortages in niche domains such as battery and 5G testing are forcing providers to invest in automation and workforce development to protect margins.

Key Report Takeaways

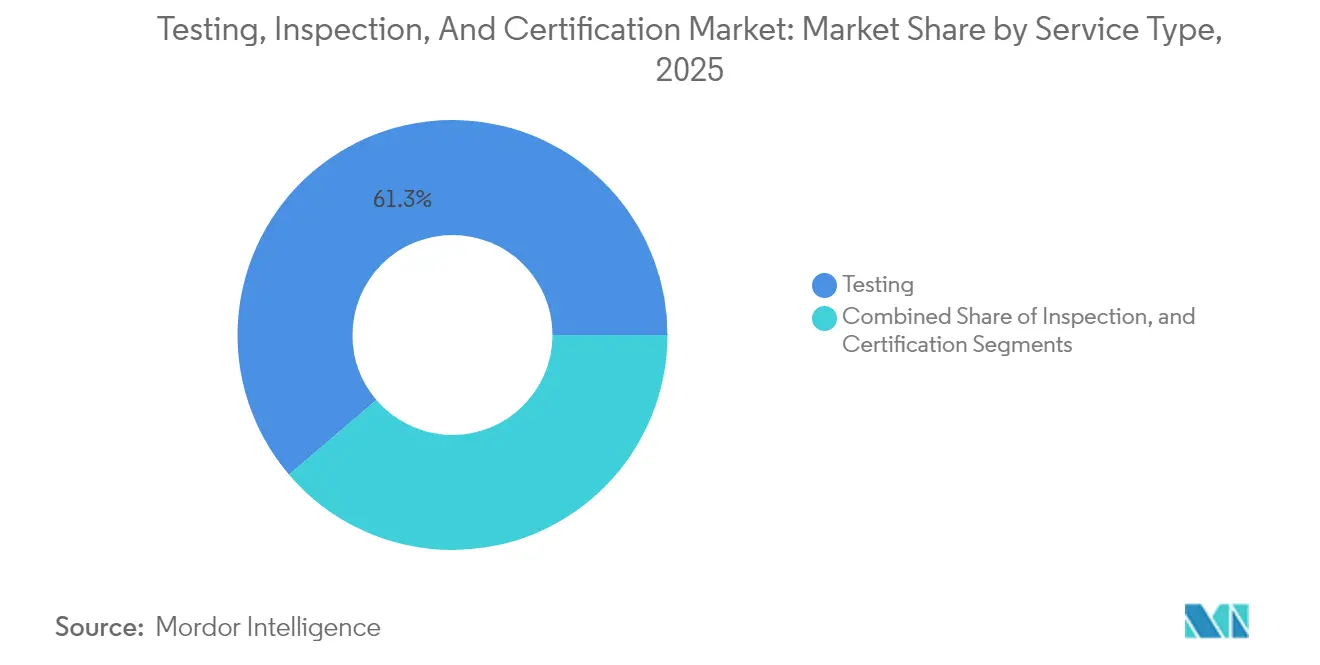

- By service type, testing services led with 61.25% of the testing inspection certification market share in 2025, while certification is projected to expand at a 4.88% CAGR through 2031.

- By sourcing, outsourced services accounted for 74.65% of the testing, inspection certification market size in 2025 and are expected to grow at a 4.66% CAGR to 2031.

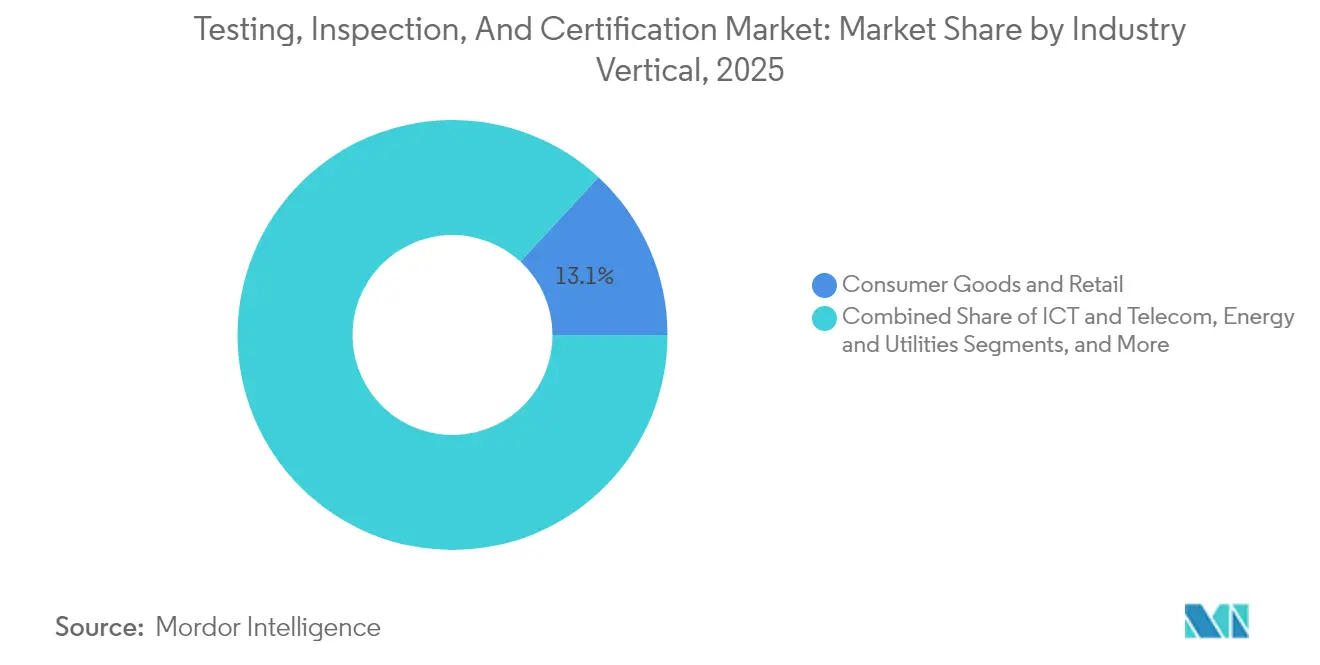

- By industry vertical, consumer goods and retail held 13.12% revenue share in 2025, whereas food, agriculture, and beverage are poised for the fastest 6.15% CAGR to 2031.

- By mode of delivery, on-site services retained a 44.62% share in 2025; remote/digital services represent the fastest growth trajectory with a 6.78% CAGR through 2031.

- By geography, Asia-Pacific accounted for 47.05% of the testing, inspection certification market size in 2025 and is expected to grow at a 5.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Testing, Inspection, And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory compliance and product-safety mandates | +1.2% | Global (early gains in EU, North America) | Medium term (2-4 years) |

| Expansion of global supply chains is demanding third-party assurance | +0.9% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Surge in consumer electronics and IoT product launches | +1.1% | Global | Short term (≤ 2 years) |

| AI-enabled remote and continuous monitoring platforms | +0.8% | North America and the EU, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Mandatory ESG / carbon-footprint verification in export markets | +1.0% | Global (EU CBAM driving adoption) | Medium term (2-4 years) |

| Cyber-physical security certification for connected products | +0.7% | North America and EU regulatory frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory ESG / Carbon-Footprint Verification Accelerates Export Compliance

Global decarbonization policies are repositioning carbon-footprint certification from a voluntary gesture to a prerequisite for cross-border trade. The EU Carbon Border Adjustment Mechanism requires ISO 14067 product carbon-footprint verification and is encouraging exporters worldwide to secure accredited assurance. SGS has leveraged three decades of sustainability expertise to launch expanded verification programs, while Bureau Veritas has rolled out organization-level ESG certification suites. Integrated digital platforms, such as SGS’s data-validation partnership with Worldly, couple continuous supply-chain emissions tracking with independent verification, aligning with regulators’ preference for auditable, real-time evidence.[1]SGS, “Product Carbon Footprint,” sgs.com

AI-Enabled Remote Monitoring Transforms Service Delivery Models

Artificial intelligence tools are automating repetitive visual checks, predicting equipment failures, and enabling continuous quality monitoring without on-site presence. Digital twins recreate physical assets virtually, permitting inspectors to identify anomalies and validate performance parameters in near real time. Major TIC providers report up to 50% cuts in field visits after adopting AI-supported image analytics and sensor fusion. Savings in travel time and faster feedback loops allow reallocation of skilled technicians to higher-value tasks while reducing customer downtime. Growing acceptance of remotely issued certificates by regulatory bodies in North America and Europe is accelerating the large-scale deployment of these platforms.

Cyber-Physical Security Certification Drives IoT Testing Demand

The convergence of cybersecurity and functional safety regulations is generating fresh requirements for connected devices. The U.S. Cyber Trust Mark program, administered by UL Solutions, stipulates ISO/IEC 17025-accredited testing and ISO/IEC 17065 certification before consumer IoT products can display the voluntary label. European standards such as ETSI EN 303 645 and forthcoming CENELEC EN 18031 add further layers of mandatory security testing. TÜV SÜD issued the first consumer IoT cybersecurity certificate for iRobot’s Roomba devices in 2025, highlighting an early-mover advantage for labs with specialized expertise.[2]TÜV SÜD, “Helping iRobot Achieve Internet of Things Cybersecurity,” tuvsud.com Bureau Veritas’s acquisition of Dutch cybersecurity firm Secura underscores a broader strategic push among incumbents to embed cyber-testing capability within traditional conformity-assessment portfolios.

Global Supply-Chain Complexity Intensifies Third-Party Assurance

With procurement footprints spanning multiple jurisdictional regimes, manufacturers increasingly view independent verification as insurance against compliance lapses. SGS’s Supplier Verification Program now covers capacity audits, quality management, and environmental checks across more than 100 countries. The International Featured Standards organization introduced its Supply Chain Processes Check in 2025, mandating annual auditor-validated assessments of commodity-related risks. These developments illustrate the growing intersection of digital traceability solutions with on-ground audits, creating demand for hybrid service models that consolidate ESG, quality, and security metrics under a single assurance umbrella.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin squeeze from price competition | -0.6% | Global (particularly Asia-Pacific) | Short term (≤ 2 years) |

| Trade frictions and divergent national standards | -0.4% | US-EU-China corridors | Medium term (2-4 years) |

| OEM self-certification via digital twins | -0.3% | Advanced manufacturing hubs | Long term (≥ 4 years) |

| Talent shortages in niche test domains | -0.5% | Global (acute in specialized hubs) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin Squeeze from Price Competition Pressures Traditional Models

Thousands of small laboratories compete in commoditized testing niches, eroding pricing power for routine chemical, materials, and consumer-product assays. Larger providers are responding by migrating toward subscription-based continuous-monitoring offers and data-rich ESG verification, aiming to shift customer conversations away from unit pricing toward value creation. However, building digital platforms, integrating IoT sensors, and training staff in data analytics entail substantial capital outlays that disproportionately burden mid-tier firms. The resulting cost-to-serve gap risks widening the divide between global leaders and regional specialists.

Talent Shortages in Specialized Domains Constrain Growth

Rapid innovation in batteries, advanced wireless, and biotechnology is creating demand for test engineers with highly specific skills. For example, thermal-runaway evaluations under UN 38.3 and ECE R100 require experts versed in electrified-vehicle safety protocols, yet few academic programs address this niche. A Nature survey of cellular-therapy labs in 2024 reported persistent vacancies for technologists trained in regulatory affairs and Good Manufacturing Practice.[3]Nature, “Cellular therapy processing laboratory: a workforce hiring nightmare,” nature.com Providers are stepping up in-house academies, remote-learning modules, and international recruitment campaigns, but near-term capacity constraints remain a bottleneck for high-growth service lines.

Increase in Lead Times Due to Complex Global Supply Chains

Extended component pathways exacerbate scheduling conflict between production and certification. SourceBlue’s construction-equipment index rose 2.9% year on year in Q3 2024, mirroring delivery delays for specialized instruments. In medical devices, ISO 13485 requires clear role assignment across multi-tier suppliers; incomplete documentation frequently triggers re-audits. Logistics provider XMAE attributes 78% of shipment delays to missing or inaccurate Certificates of Conformity. Companies must therefore embed compliance checkpoints earlier in product-development cycles or risk deferred market entry and sunk costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Dominance Amid Certification Growth Acceleration

Testing accounted for 61.25% of the 2025 testing inspection certification market share, underlining its foundational role in product development and compliance cycles. Stringent automotive cybersecurity rules and complex 5G radio frequency characteristics are driving laboratories to invest in millimeter-wave chambers and over-the-air systems. The testing, inspection certification market size for battery evaluations is also expanding as UL Solutions extends laboratories near major EV production clusters to support thermal-runaway and vibration protocols.

Certification services, although smaller, are forecast to record the fastest 4.88% CAGR. New programs such as the Cyber Trust Mark require ISO/IEC 17065-accredited bodies to authorize cybersecurity labels, creating additional revenue streams for firms with the right accreditations. ESG standards linked to carbon-footprint verification further amplify demand, making certification a strategic priority for providers seeking margin-resilient growth. Inspection sits between the two segments, benefiting from supply-chain verification mandates yet facing substitution pressure from AI-enabled remote visual tools.

By Sourcing Type: Outsourced Services Capitalize on Complexity

Outsourced services dominated the 2025 testing, inspection certification market, capturing a 74.65% share as manufacturers relied on third-party expertise to navigate proliferating standards. Independent labs offer scale advantages in capital-intensive domains such as electromagnetic compatibility and high-energy battery abuse testing, while their global footprint helps multinational clients harmonize compliance processes. The trend is strongest in consumer electronics, where rapid model refresh cycles favor external labs that maintain state-of-the-art facilities.

In-house programs remain essential for life-science, utility, and defense entities that insist on data confidentiality and operational control, but their market share is gradually eroding. Hybrid approaches are emerging: automotive OEMs retain design-validation benches yet outsource type-approval testing to accredited bodies for global market entry, illustrating how internal oversight and external certification can coexist to optimize resources.

By Industry Vertical: Consumer-Goods Leadership Challenged by Food Sector Acceleration

Consumer goods and retail led the testing, inspection certification market size with 13.12% share in 2025, reflecting ongoing demand for quality checks, social-audit programs, and cybersecurity labels on smart-home devices. The FCC’s Cyber Trust Mark is expected to further boost testing volumes for fitness trackers, connected appliances, and voice-activated accessories.

Food, agriculture, and beverage are poised for the fastest 6.15% CAGR to 2031 as regulators tighten traceability and import-safety protocols. The FDA’s Voluntary Qualified Importer Program allows compliant foreign suppliers expedited U.S. entry, but only after third-party auditors such as SGS confirm adherence to Hazard Analysis and Risk-based Preventive Controls. Bureau Veritas’s farm-to-fork framework adds upstream farm-gate audits to bolster provenance claims, indicating a shift toward end-to-end certification across agri-food chains.

By Mode of Service Delivery: Remote Digital Services Transform Traditional Models

On-site visits still represented 44.62% of revenue in 2025 as inspectors issued welding certificates, construction compliance reports, and equipment approvals that regulators prefer to witness physically. Yet the share is gradually tilting toward off-site analyses bolstered by real-time data feeds.

Remote/digital delivery is the fastest-growing sub-segment, advancing at a 6.78% CAGR as labs deploy AI-powered cameras and cloud dashboards. Tata Consultancy Services has demonstrated cloud-based automation that lets dispersed engineering teams run vehicle infotainment tests on physical hardware via web portals. Laboratory-centered services continue to thrive in areas requiring controlled atmospheres—battery abuse, EMC, chemical composition—but are increasingly complemented by sensors that trigger laboratory tests automatically when field data cross critical thresholds.

Geography Analysis

Asia-Pacific remains the fulcrum of demand with a 47.05% share in 2025 and is expected to grow at a rapid rate of 5.28% during the forecast period. The region is mainly driven by expanding manufacturing footprints in China, India, Vietnam, and Indonesia, and by progressively stringent domestic standards across electronics, automotive, and renewables. International TIC groups have ramped up laboratory investments near EV battery gigafactories in the region to meet escalating local certification requirements. Rising middle-income consumption is also raising awareness of product-safety labels, accelerating market penetration for third-party assurance providers.

North America holds the second-largest slice of the testing, inspection certification market, supported by robust aerospace, medical-device, and advanced electronics sectors. The Cyber Trust Mark shows regulatory willingness to pioneer voluntary cybersecurity labeling, stimulating lab accreditation in wireless, cryptography, and over-the-air testing. Food safety continues to underpin steady inspection volumes as importers seek Qualified Importer Certification to unlock expedited FDA clearance.

Europe benefits from a dense regulatory framework that integrates ESG, cybersecurity, and automotive functional-safety directives. The continent’s leadership in circular-economy measures, such as the EU Deforestation Regulation and CBAM, pushes exporters worldwide to obtain verified sustainability certificates. UNECE’s R155 and R156 rules for automotive cybersecurity and software update management have spawned new homologation programs, prompting TIC providers to establish specialized tracks for threat analysis, penetration testing, and secure update validation.

Competitive Landscape

The global testing inspection certification market is moderately concentrated: the top 10 providers control a significant share of total revenue, leaving space for regional specialists and digital disruptors. Strategic M&A is reshaping the field. Nordic Inspekt Group’s acquisition of Norway-based Testpartner Gruppen in April 2025 expanded its presence in non-destructive testing and welding certification.[4]Qben Infra AB, “Platform company signs SPA to acquire TIC specialist,” view.news.eu.nasdaq.com Bureau Veritas’s 2024 divestment of its food-testing arm to Mérieux NutriSciences freed capital to pursue higher-margin cyber-physical assurance and ESG services.

Technology adoption is the primary differentiation lever. SGS pairs its global lab network with blockchain-enabled supply-chain data-validation, while Bureau Veritas folded Dutch cybersecurity lab Secura into its consumer-products division to accelerate connected-device testing capacity. UL Solutions is extending global battery and 5G test beds to consolidate leadership in safety-critical domains. Private-equity interest remains robust: Sansidor, backed by IK Partners since 2024, is stitching together a platform of 18 specialist providers in water safety, fire protection, and electrical testing, illustrating buy-and-build momentum in fragmented niches.

Emerging startups focus on AI-first visual-inspection software and automated reporting engines. However, barriers such as accreditation costs, global cross-recognition of certificates, and reputational track record continue to shield incumbents. The resulting landscape mixes scale-driven giants, regionally entrenched mid-caps, and agile digital entrants competing on speed and specialization.

Testing, Inspection, And Certification Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nordic Inspekt Group finalized the NOK 41.2 million acquisition of Testpartner Gruppen, enhancing Nordic coverage in materials testing and welding certification.

- March 2025: The U.S. Federal Communications Commission issued final rules for the Cyber Trust Mark program and appointed UL Solutions as Lead Administrator.

- February 2025: The International Featured Standards organization launched its Supply Chain Processes Check, requiring annual auditor-validated assessments of commodity-specific risks.

- January 2025: TÜV SÜD granted its Cyber Security Certification mark to iRobot’s Roomba j7 line, marking the first consumer-IoT device to achieve the designation.

Global Testing, Inspection, And Certification Market Report Scope

The market can be defined as the revenue generated by vendors offering TIC solutions to various end users. The scope of the study includes the market by service type for testing and inspection services and certification services with various sourcing types, such as outsourced and in-house to end-user verticals, including consumer goods and retail, food and agriculture, oil and gas, construction and engineering, energy and chemicals, manufacturing of industrial goods, transportation (rail and aerospace), industrial and automotive, and other end-user verticals operating worldwide.

The testing, inspection, and certification market is segmented by service type (testing and inspection service and certification service), by sourcing type (outsourced and in-house), by end-user vertical (consumer goods and retail, food and agriculture, oil and gas, construction and engineering, energy and chemicals, manufacturing of industrial goods, transportation (rail and aerospace), industrial and automotive, other end-user verticals), and by geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Spain, Norway, Rest of Europe], Asia-Pacific [China, Japan, South Korea, India, Rest of Asia-Pacific], Latin America [Brazil, Mexico, Rest of Latin America], Middle East and Africa [Saudi Arabia, United Arab Emirates, Qatar, Turkey, Nigeria, Rest of Middle East and Africa]). The report offers market forecasts and size in value (USD) for all the above segments.

By Service Type

| Testing |

| Inspection |

| Certification |

By Sourcing Type

| In-house |

| Outsourced |

By Industry Vertical

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others (Environment, Sustainability, etc.) |

By Mode of Service Delivery

| On-site |

| Off-site/Laboratory |

| Remote / Digital |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing | ||

| Inspection | |||

| Certification | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Industry Vertical | Consumer Goods and Retail | ||

| ICT and Telecom | |||

| Automotive and Transportation | |||

| Aerospace and Defense | |||

| Oil, Gas and Petrochemicals | |||

| Energy and Utilities | |||

| Industrial Manufacturing and Machinery | |||

| Chemicals and Materials | |||

| Construction and Infrastructure | |||

| Life Sciences and Healthcare | |||

| Food, Agriculture and Beverage | |||

| Others (Environment, Sustainability, etc.) | |||

| By Mode of Service Delivery | On-site | ||

| Off-site/Laboratory | |||

| Remote / Digital | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the testing, inspection, and certification market in 2026?

It is valued at USD 275.56 billion in 2026, with a projected 4.62% CAGR through 2031.

Which service type dominates spending?

Testing services lead with 61.25% share thanks to mandatory performance validation across automotive, electronics, and battery domains.

What drives the fastest growth within service offerings?

Certification is the quickest-growing segment, expanding at a 4.88% CAGR as ESG and cybersecurity rules add new labeling requirements.

Why are outsourced TIC services gaining popularity?

Regulatory complexity and capital-intensive test equipment make external labs more cost-effective, driving outsourced services to a 74.65% share in 2025.

Which region shows the highest growth potential?

Asia-Pacific is expected to post the fastest expansion at a 5.28% CAGR during the forecast period due to manufacturing relocation and strengthening domestic standards across the electronics and renewable energy sectors.

How is technology changing TIC delivery models?

AI-enabled remote monitoring and digital twins are cutting on-site visits, enabling continuous assurance and transforming traditional inspection workflows.

Page last updated on: