Japan Testing, Inspection, And Certification (TIC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

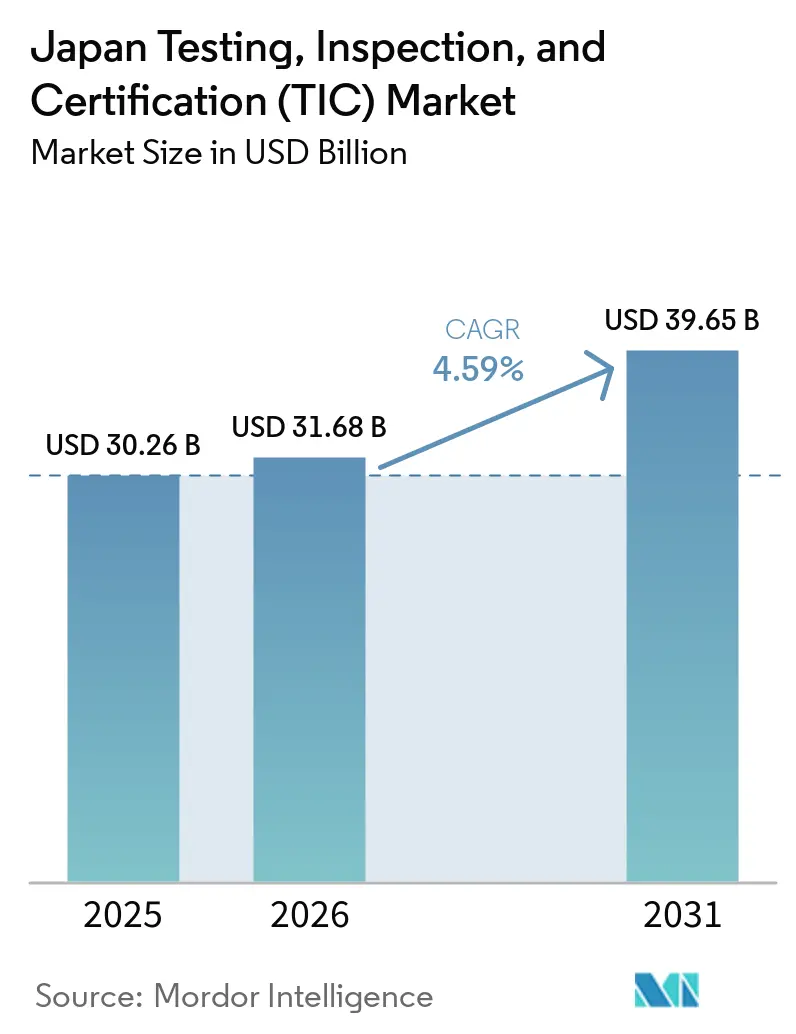

| Base Year Market Size (2025) | USD 30.26 Billion |

| Market Size (2026) | USD 31.68 Billion |

| Market Size (2031) | USD 39.65 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Testing, Inspection, And Certification (TIC) Market Analysis by Mordor Intelligence

The Japan testing, inspection, and certification (TIC) market size is expected to increase from USD 30.26 billion in 2025 to USD 31.68 billion in 2026 and reach USD 39.65 billion by 2031, growing at a CAGR of 4.59% over 2026-2031. Continuing reallocation of compliance budgets from mature consumer-electronics checks toward battery-safety, hydrogen-supply-chain, and remote-inspection mandates is reshaping demand. Ministries now require cybersecurity attestation for connected vehicles, carbon-intensity verification for imported hydrogen, and lithium-ion fire-propagation tests, so laboratories are purchasing thermal-abuse chambers, high-voltage cyclers, and penetration-testing toolkits. Outsourcing expands because new equipment costs exceed USD 5 million per site and skilled-staff shortages persist. Digital delivery accelerates as 5G-enabled robots, Internet-of-Things sensors, and artificial-intelligence analytics let technicians supervise assets hundreds of kilometers away, cutting mobilization costs and easing the engineer shortfall.

Key Report Takeaways

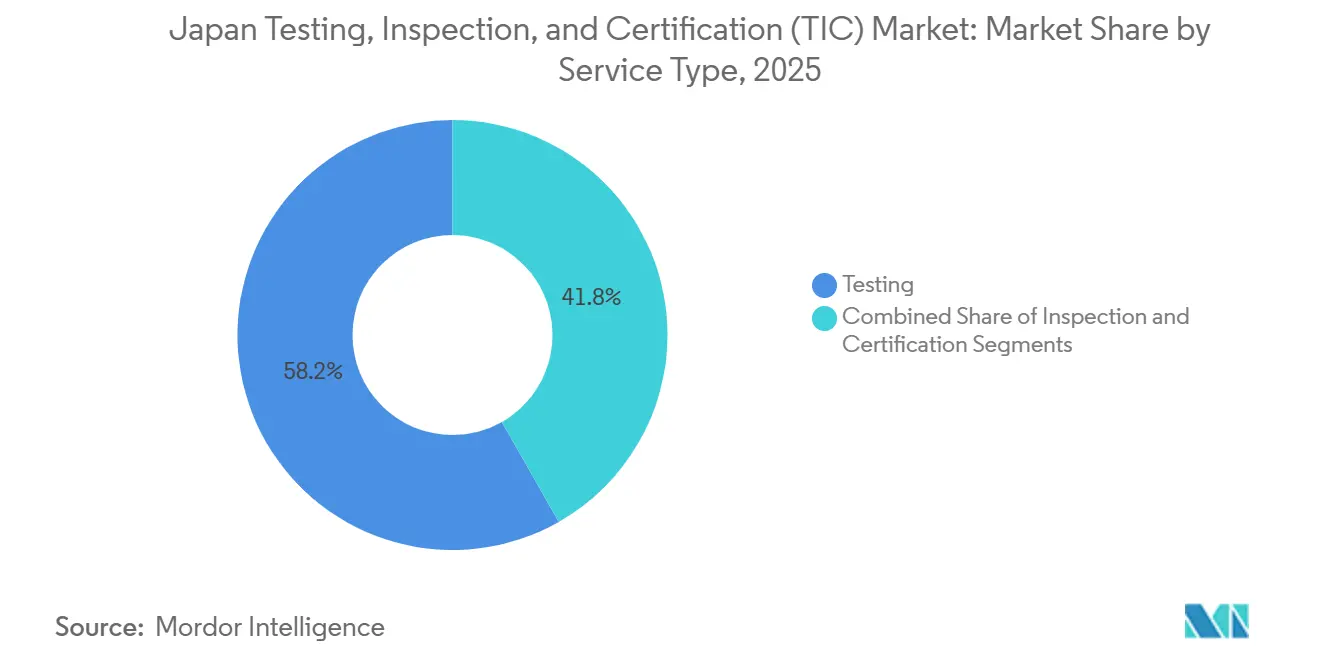

- By service type, testing led with 58.23% revenue share in 2025, whereas certification is forecast to post the fastest 5.26% CAGR through 2031.

- By sourcing type, outsourced engagements held 62.27% of the Japan testing, inspection, and certification market share in 2025, while the same model registers the highest projected 5.15% CAGR to 2031.

- By delivery mode, on-site inspections accounted for 44.76% of spending in 2025, yet remote and digital methods are projected to expand at a 6.21% CAGR between 2026-2031.

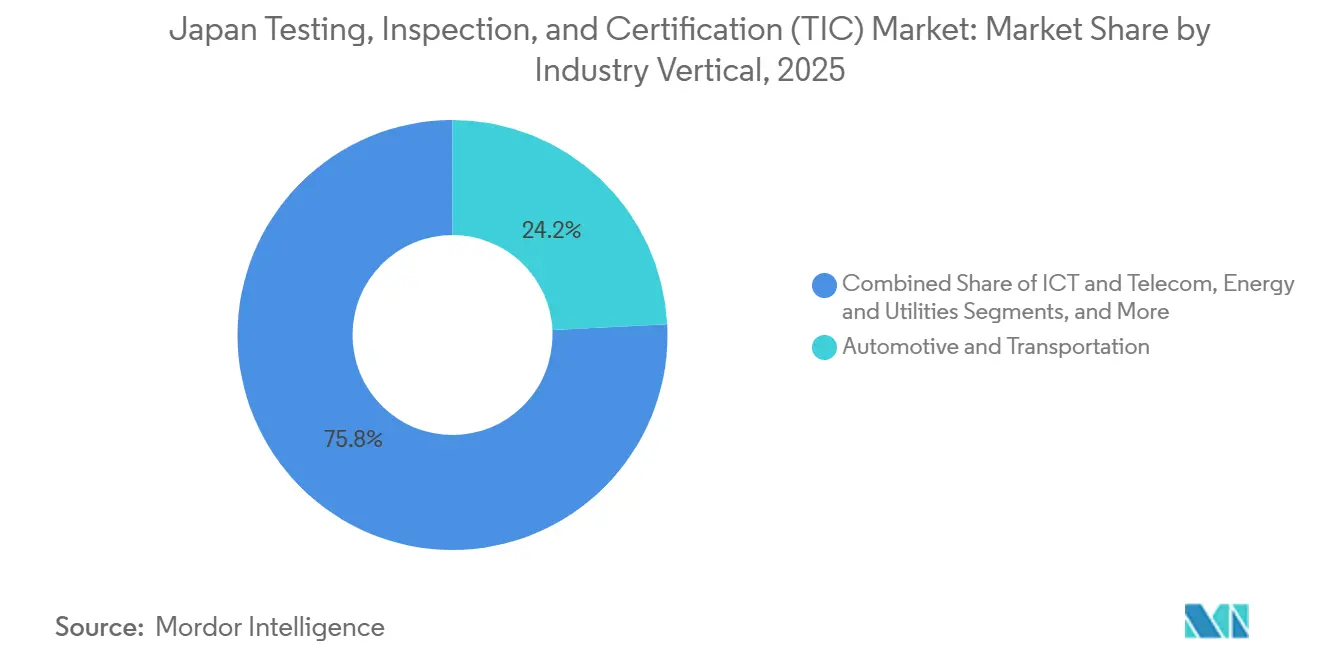

- By industry vertical, automotive and transportation captured 24.21% of outlays in 2025, while life sciences and healthcare is advancing at a 4.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Testing, Inspection, And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Regulatory Stringency Across Automotive, Life Sciences and Environment | +1.2% | Tokyo, Aichi, Osaka metropolitan areas | Medium term (2-4 years) |

| EV and Advanced Mobility Safety Requirements (Battery, ADAS, Cybersecurity) | +1.0% | Aichi, Kanagawa, Hiroshima | Short term (≤ 2 years) |

| Industry 4.0 Complexity Boosting Demand for Digital TIC | +0.8% | Kanto and Kansai industrial corridors | Medium term (2-4 years) |

| Infrastructure Life-Extension and Renewable-Energy Projects | +0.7% | Hokkaido, Tohoku, Kyushu coastal zones | Long term (≥ 4 years) |

| Certification Needs in Emerging Hydrogen and Ammonia Value Chains | +0.5% | Fukuoka, Yamaguchi, Hyogo | Long term (≥ 4 years) |

| High-Speed Maglev and Rail Electrification Driving Catenary Inspections | +0.3% | Tokyo-Nagoya-Osaka corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Regulatory Stringency Across Automotive, Life Sciences and Environment

New vehicle models must clear UN No. 155 cybersecurity audits, regenerative-medicine sponsors have to submit 24-month real-world evidence, and utilities face ultra-trace PFAS limits. These overlapping mandates expand compliance scopes and shorten approval windows, so companies allocate larger budgets to established laboratories.[1]Ministry of Economy, Trade and Industry, “Hydrogen Society Promotion Act and Carbon Intensity Guidelines,” meti.go.jp Market leaders capitalize on their ISO 17025 and ISO 17065 track records to secure multi-year contracts, reinforcing the Japan testing, inspection, and certification market dominance of accredited providers. Market leaders capitalize on their ISO 17025 and ISO 17065 track records to secure multi-year contracts, reinforcing the Japan testing, inspection, and certification market dominance of accredited providers.

EV and Advanced Mobility Safety Requirements

From 2025-2027, every lithium-ion module must demonstrate five-minute thermal-runaway containment, ADAS algorithms must pass ISO 23792 and ISO 34502 scenarios, and vehicle controllers require penetration tests. Automakers redirect validation spend from combustion systems to high-voltage, high-data-rate platforms, raising demand for USD 3-5 million abuse chambers and 800-volt anechoic cells. The result is a rapid surge in specialized battery, radar, and cybersecurity orders across the Japan testing, inspection, and certification market. Japan’s strong position in automotive manufacturing and next-generation mobility technologies further accelerates investments in advanced testing infrastructure. Growing production of electric and software-defined vehicles is increasing demand for specialized certification services, supporting sustained expansion of the TIC market.

Industry 4.0 Complexity Boosting Demand for Digital TIC

IoT security labeling, sensor-driven predictive maintenance, and Open-RAN verification introduce inspection categories that rely on continuous data feeds rather than batch sampling. Laboratories deploy cloud portals, machine-vision analytics, and remote robots, letting a single engineer audit multiple plants in real time. This shift enables capacity growth without proportional headcount, enhancing scalability for the Japan testing, inspection, and certification market. Growing investment in Industry 4.0 technologies is encouraging TIC providers to expand remote auditing, AI-enabled analytics, and digital compliance platforms, improving operational efficiency and service coverage.

Infrastructure Life-Extension and Renewable-Energy Projects

Aging bridges and emerging offshore wind farms need ultrasonic phased-array imaging, infrared thermography, and drone surveys. Local governments schedule five-year visual exams and ten-year soundness checks, while wind developers mandate annual blade diagnostics. These steady, contract-based engagements provide a long-tail revenue stream that cushions cyclical industries and extends the regional reach of the Japan testing, inspection, and certification market. The growing need to maintain aging public assets while supporting new offshore wind and energy projects is creating sustained opportunities for TIC providers across both urban and coastal regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Advanced Labs and Skilled-Staff Shortages | -0.6% | Kanto, Kansai, Chubu industrial zones | Short term (≤ 2 years) |

| Fragmented Domestic and International Standard Alignment Costs | -0.4% | National cross-border sectors | Medium term (2-4 years) |

| Data-Sovereignty Hurdles for Remote and Cloud-Based TIC | -0.3% | Enterprises with overseas data centers | Medium term (2-4 years) |

| Shrinking Low-Value Manufacturing Segments Curbing Routine Testing Volumes | -0.2% | Consumer-electronics and textile areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Advanced Labs and Skilled-Staff Shortages

Capital outlays ranging from USD 5-15 million for anechoic chambers and GMP cleanrooms pose significant barriers for new entrants and exert pressure on mid-tier laboratories, as these investments require substantial financial resources and long-term planning. Despite a projected gap of 500 engineers by 2030, firms are hastening their automation efforts to address workforce shortages and improve operational efficiency. However, the high costs associated with integrating automation technologies and the extensive retraining required for existing staff are hindering a swift ramp-up of these initiatives. Additionally, capacity constraints, driven by limited resources and increasing demand, are extending turnaround times for testing, inspection, and certification processes. These delays are negatively impacting the overall growth potential of Japan's testing, inspection, and certification market, as companies struggle to meet market demands efficiently.

Fragmented Domestic and International Standard Alignment Costs

In Japan, the implementation of stricter cybersecurity documentation requirements, pharmaceutical bridging studies, and simultaneous RoHS-REACH chemical testing has resulted in repeated audits and redundant sampling processes. These regulatory demands compel manufacturers to allocate a significant portion of their budgets toward maintaining compliance. Consequently, resources that could have been directed toward innovation and new product launches are instead diverted to meet these obligations. This reallocation of funds not only hampers the immediate growth potential of manufacturers but also creates a ripple effect, limiting expansion opportunities for service providers operating within Japan's testing, inspection, and certification market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Momentum Builds

In 2025, testing accounted for 58.23% of the revenue, driven by high-value orders in destructive battery abuse, bioequivalence trials, and microbiology assays. Meanwhile, certification is poised to surpass testing, boasting a projected 5.26% CAGR, fueled by the demand for third-party marks in hydrogen stations, offshore wind turbines, and expedited medical devices. The Japan TIC Market is witnessing significant growth due to advancements in renewable energy and medical technology sectors. This evolution is further supported by stricter regulatory convergence with international standards and increasing cross-border product approvals, which amplify the importance of globally recognized certification bodies.

Voluntary eco-labels and lender-mandated due-diligence reports elevate recurring surveillance audits, so laboratories pivot to ISO 19870 hydrogen and renewable-energy certificates.[2]Japan Accreditation Board, “Conformity Assessment Body Oversight,” jab.or.jp This transition will gradually redistribute fees, yet the Japan testing, inspection, and certification market size for testing remains the largest absolute pool through 2031. Japan’s national hydrogen strategy is further accelerating certification demand for hydrogen production, storage, and renewable infrastructure projects. In parallel, increasing cross-border energy trade requirements and stricter decarbonization reporting frameworks are pushing TIC providers to expand specialized verification capabilities across the hydrogen value chain.

By Sourcing Type: Outsourcing Deepens

By sourcing type, outsourced engagements held 62.27% of the Japan testing, inspection, and certification market share in 2025, while the same model registers the highest projected 5.15% CAGR to 2031. This was largely due to the USD 4-6 million investment in each automotive anechoic chamber and the USD 2 million cost associated with long-cycle battery testers. The increasing reliance on outsourced services highlights the growing demand for cost-effective solutions in the Japan TIC market. This trend is further reinforced by rising complexity in compliance requirements and the need for continuous upgrades in testing infrastructure, which makes in-house expansion less economically efficient for most manufacturers.

As hybrid models gain traction, enterprises, faced with new remote-inspection pilots and significant capital requirements, increasingly turn to third parties for project execution. As a result, the portion of Japan's testing, inspection, and certification (TIC) market that is outsourced is set to expand further in the coming years. This trend highlights the growing reliance on specialized third-party providers to meet evolving industry demands. This shift is also supported by the rising adoption of digital assurance models, where AI-enabled inspections and cloud-based compliance platforms reduce on-site dependency while improving audit frequency and traceability.

By Industry Vertical: Life Sciences Accelerates

Thanks to battery, ADAS, and cybersecurity regulations, the automotive and transportation sector captured a 24.21% market share. Meanwhile, bolstered by the Pharmaceuticals and Medical Devices Agency’s conditional-approval framework, the life sciences and healthcare sector experienced the most significant growth, boasting a 4.96% CAGR. The Japan TIC market is witnessing increased demand for testing and certification services across these sectors due to evolving regulatory standards. This momentum is further reinforced by rapid innovation cycles in electric vehicles and biopharmaceuticals, which are increasing the frequency and complexity of compliance requirements, thereby strengthening the role of accredited TIC providers in both product validation and market authorization processes.

Global sponsors, leveraging international harmonization, are now conducting pivotal trials locally. This shift directs new budgets to contract-research organizations and testing facilities. As a result, Japan's market for testing, inspection, and certification is increasingly favoring therapeutic and diagnostic pipelines. The Japan TIC Market is also witnessing increased collaboration between local and international stakeholders to streamline processes and enhance efficiency.

By Mode of Service Delivery: Remote and Digital Gains

In 2025, on-site work accounted for 44.76% of the revenue. Yet, with the emergence of 5G-robot demonstrations, it's clear that not all visual and functional inspections require travel. This shift highlights the potential of remote inspection solutions to transform the Japan TIC Market. The adoption of advanced technologies like 5G is expected to drive innovation and efficiency in the Japan TIC Market. This transition is further enabling real-time data transmission for high-precision inspections, allowing TIC providers to expand coverage across geographically dispersed assets while reducing operational downtime and inspection costs.

In Japan's testing, inspection, and certification (TIC) market, remote services are projected to grow at a CAGR of 6.21%, driven by sensor-led continuous monitoring. Meanwhile, mandates for domestic servers are fueling investments in sovereign clouds and integrating digital workflows. The increasing adoption of advanced technologies is further transforming the operational landscape of the Japan TIC market. This shift is also accelerating the convergence of TIC operations with cybersecurity and data governance requirements, as secure data hosting becomes a core component of compliance-driven inspection and certification services.

Geography Analysis

Kanto generated roughly 35% of 2025 revenue because Tokyo hosts headquarters for automakers, pharma giants, and electronics firms, while adjacent prefectures supply research centers. Chubu delivered 22% owing to Toyota City’s battery hubs and Nagoya’s aerospace cluster, and Kansai followed at 18%, anchored by chemical and steel complexes. This regional distribution is further supported by dense industrial clustering and strong R&D ecosystems, which continue to concentrate high-value testing and certification demand around major manufacturing and innovation corridors across Japan.

Uniform bridge-inspection rules extend demand to rural prefectures, and offshore wind auctions funnel blade and cable tests to Hokkaido and Tohoku. Kyushu and Chugoku prefectures rise as hydrogen and ammonia certification hubs, with supply-chain audits verifying carbon-intensity thresholds.[3]Japan Organization for Metals and Energy Security, “Hydrogen Carbon-Intensity Verification,” jogmec.go.jp This geographic diversification is gradually reducing overdependence on major metropolitan clusters while expanding the TIC service footprint into energy transition and infrastructure-driven regional economies across Japan.

The maglev corridor between Tokyo, Nagoya, and Osaka requires catenary and electromagnetic interference validations, and remote inspection technology lets metropolitan laboratories serve nationwide assets without brick-and-mortar expansion, broadening the geographic scope of the Japan testing, inspection, and certification market. This also reinforces the shift toward centralized, high-capability TIC hubs in major cities, where advanced simulation and digital twin platforms enable continuous validation of large-scale infrastructure projects across Japan without proportional increases in field deployment.

Competitive Landscape

The top five multinationals hold about 28-32% combined share, showing moderate concentration, while domestic specialists retain niche strongholds tied to ministry accreditation. SGS completed 19 acquisitions in 2025 and added North American non-destructive testing capacity in 2026, integrating global portals for seamless cross-border orders. Bureau Veritas purchased Lotusworks to create a USD 339 million semiconductor platform, and Intertek bought solar and environmental labs to deepen renewable-energy reach. This consolidation trend is further strengthening global standardization of testing protocols while intensifying competition in high-growth segments such as semiconductors, renewable energy, and advanced mobility, where scale and cross-border certification capabilities are becoming key differentiators.

Companies are consolidating services into unified contracts and introducing client dashboards for real-time tracking of samples and certificates. Emerging opportunities exist in hydrogen-station certification, ammonia-fuel management, and cybersecurity for medical devices, all of which are still developing their frameworks. In the Japan TIC Market, the demand for integrated solutions is driving innovation in service offerings. This trend is further supported by the shift toward end-to-end digital assurance ecosystems, where TIC providers bundle testing, certification, and compliance monitoring into a single platform to improve transparency, reduce turnaround time, and enhance client decision-making across complex regulatory environments.

Technology investment continues: UL Solutions opened a high-voltage electromagnetic-compatibility center, and the Japan Aerospace Exploration Agency introduced simulation-based component approval, positioning computation-heavy providers for future gains within the Japan testing, inspection, and certification market. This ongoing shift toward simulation-led and digitally verified compliance is reducing reliance on purely physical testing while increasing demand for high-performance computing, advanced modeling tools, and integrated digital certification platforms across TIC service providers.

Japan Testing, Inspection, And Certification (TIC) Industry Leaders

SGS Japan Inc.

Bureau Veritas Japan Co., Ltd.

Intertek Testing Services Japan K.K.

TÜV SÜD Japan Ltd.

TÜV Rheinland Japan Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bureau Veritas acquired Lotusworks, a data-center and semiconductor testing specialist, to establish a EUR 300 million (USD 339 million) growth platform across Asia Pacific, enabling the company to serve hyperscale cloud operators and fabless chip designers with reliability testing, electromagnetic-compatibility evaluations, and environmental stress screening.

- April 2026: The Japan Food Safety Management Association reported that 2,924 organizations held active certifications under its scheme, reflecting a 12% increase from 2025 as food manufacturers, distributors, and restaurant chains sought third-party validation to differentiate products in competitive retail channels.

- April 2026: Intertek acquired Mitsui Chemicals' solar-laboratory assets in India, expanding its photovoltaic module testing capacity and enabling the company to offer integrated services spanning cell efficiency, durability, and safety certifications for renewable-energy developers.

- March 2026: CO.L.MAR deployed acoustic leak-detection systems across 11 kilometers of 48-inch subsea crude-oil pipeline at Ube Storage Base, identifying micro-leaks before they escalated into environmental incidents and demonstrating the viability of continuous monitoring for high-risk petrochemical infrastructure.

Japan Testing, Inspection, And Certification (TIC) Market Report Scope

The Japan Testing, Inspection, and Certification (TIC) Market refers to the global industry that provides services ensuring products, systems, and processes meet regulatory standards, quality benchmarks, and safety requirements across diverse sectors such as manufacturing, healthcare, automotive, energy, consumer goods, and construction.

The Japan Testing, Inspection, and Certification (TIC) Market Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-house and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Automotive and Transportation, Aerospace and Defense, Oil Gas and Petrochemicals, Energy and Utilities, Industrial Manufacturing and Machinery, Chemicals and Materials, Construction and Infrastructure, Life Sciences and Healthcare, Food Agriculture and Beverage, and Others Industry Verticals), Mode of Service Delivery (On-site, Off-site Laboratory, and Remote / Digital). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Others Industry Verticals |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Others Industry Verticals | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital |

Key Questions Answered in the Report

What is the current size of the Japan testing, inspection, and certification market?

The market stands at USD 31.68 billion in 2026 and is projected to reach USD 39.65 billion by 2031.

Which service type is growing fastest within Japan’s TIC space?

Certification is expanding at a 5.26% CAGR to 2031 as hydrogen stations, offshore wind turbines, and advanced medical devices seek third-party marks.

Why are remote and digital inspections gaining traction?

5G connectivity, IoT sensors, and AI analytics allow real-time monitoring, cutting mobilization costs by roughly 30% and mitigating the shortage of qualified engineers.

How are hydrogen regulations shaping TIC demand?

Imports must verify carbon intensity below 3.4 kg-CO₂ per kg-H₂, so lifecycle audits and supply-chain traceability certifications are becoming mandatory.

Which regions inside Japan are seeing the strongest new TIC activity?

Offshore-wind projects channel tests to Hokkaido and Tohoku, while hydrogen hubs in Fukuoka, Yamaguchi, and Hyogo drive certification growth.

What strategic moves are leading TIC firms making?

Multinationals such as SGS, Bureau Veritas, and Intertek are acquiring specialized labs and rolling out cloud portals to bundle testing, inspection, and certification services.

Page last updated on: