Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

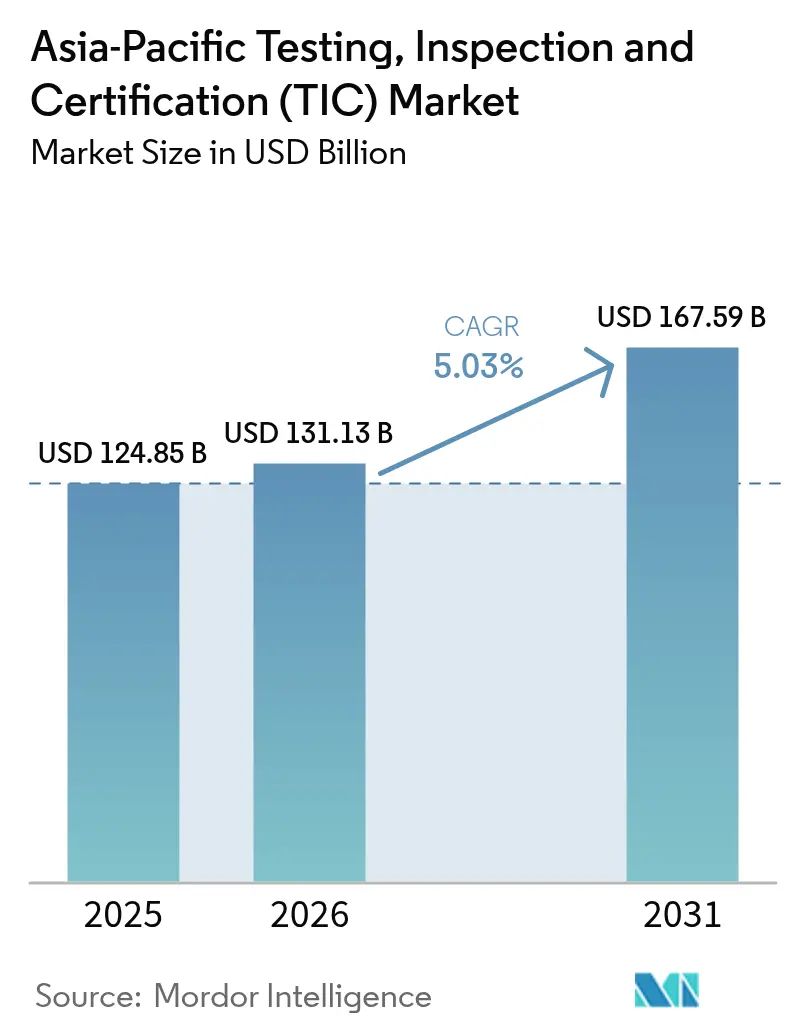

| Base Year Market Size (2025) | USD 124.85 Billion |

| Market Size (2026) | USD 131.13 Billion |

| Market Size (2031) | USD 167.59 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Testing, Inspection And Certification (TIC) Market Analysis by Mordor Intelligence

The Asia-Pacific TIC market size was valued at USD 124.85 billion in 2025 and estimated to grow from USD 131.13 billion in 2026 to reach USD 167.59 billion by 2031, at a CAGR of 5.03% during the forecast period (2026-2031). Expanding cross-border manufacturing networks, fast-tracking of sustainability rules, and accelerated digital adoption across factories, laboratories, and infrastructure programs collectively sustain demand for testing, inspection, and certification services. The continual rollout of electric-vehicle battery safety rules, medical-device cybersecurity labels, and hydrogen-fuel quality standards adds fresh compliance layers that favor providers able to mobilize multidisciplinary expertise across multiple jurisdictions. Outsourced providers strengthen their edge as regulatory duties outstrip in-house capabilities, while remote inspection platforms gain traction as enterprises pursue cost-effective coverage in locked-down or hard-to-reach sites. Certification, in particular, draws attention as companies seek independent assurance for ESG disclosures and supply-chain traceability.

Key Report Takeaways

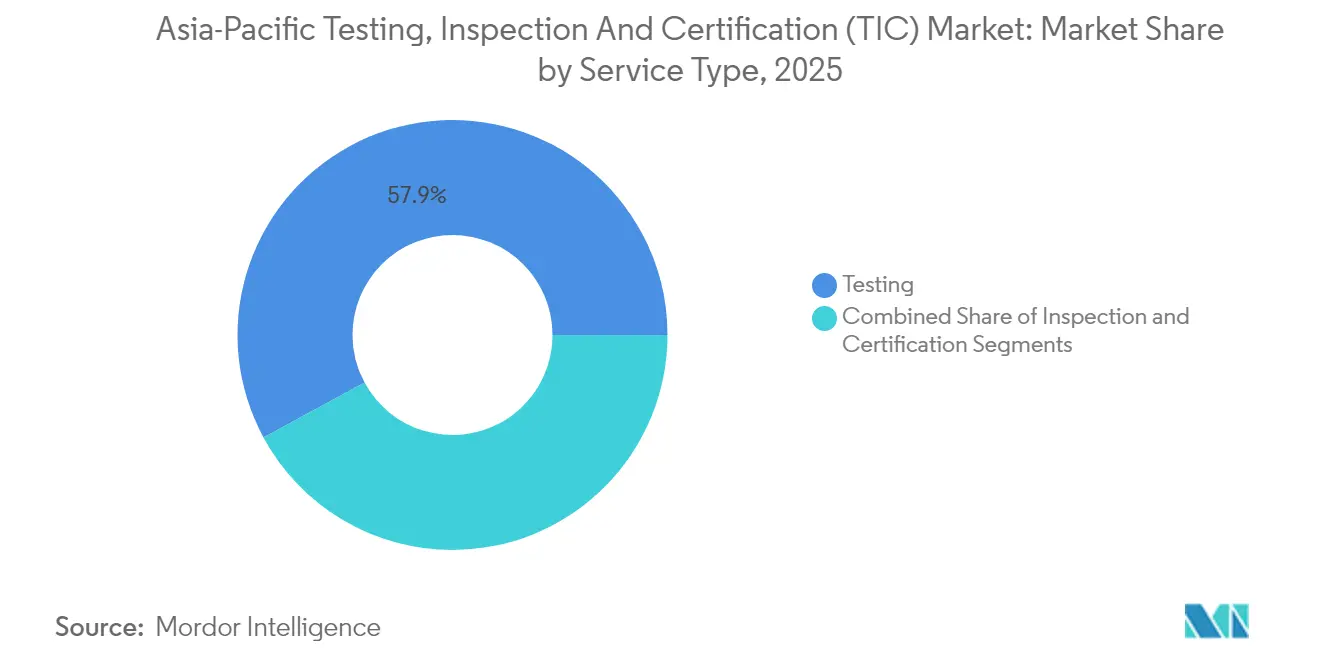

- By service type, testing led with 57.90% revenue share of the Asia-Pacific TIC market in 2025; certification is forecast to grow at a 5.62% CAGR to 2031.

- By sourcing type, outsourced services captured a 63.10% share of the Asia-Pacific TIC market in 2025 and are projected to expand at a 5.32% CAGR through 2031.

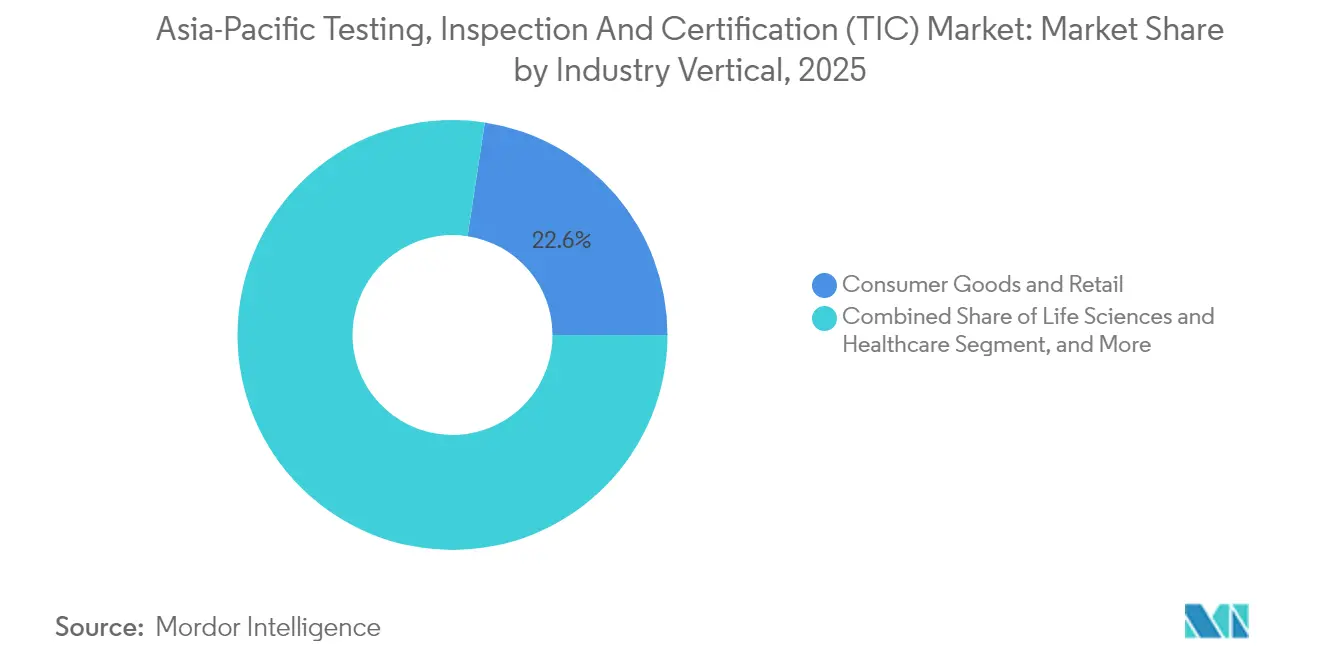

- By industry vertical, consumer goods and retail held 22.60% of revenue of the Asia-Pacific TIC market in 2025, while food, agriculture, and beverage are advancing at a 6.05% CAGR to 2031.

- By mode of service delivery, on-site services retained a 52.05% share of the Asia-Pacific TIC market in 2025; remote and digital inspection is scaling fastest at a 5.86% CAGR to 2031.

- By country, China commanded 40.25% of the regional revenue of the Asia-Pacific TIC market in 2025, whereas India registered the fastest trajectory at a 6.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Testing, Inspection And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain complexity | +1.2% | China, ASEAN export hubs | Medium term (2-4 years) |

| Sustainability and ESG audits | +0.9% | Singapore, Hong Kong, Australia | Short term (≤ 2 years) |

| EV and battery safety harmonization | +0.8% | China, Japan, South Korea, ASEAN | Medium term (2-4 years) |

| Real-time digital-health compliance | +0.7% | Singapore, Japan, Australia | Short term (≤ 2 years) |

| Green hydrogen pilot scaling | +0.5% | Australia, Japan | Long term (≥ 4 years) |

| AI-driven predictive maintenance | +0.4% | Advanced manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Trade-centric supply-chain complexity drives regional TIC demand

Asia sits at the heart of global manufacturing and now supports intricate, multi-jurisdictional supply chains that span hundreds of tier-1 and tier-2 suppliers. The ASEAN digital economy alone is targeting USD 1 trillion by 2030, a scale that intensifies conformity-assessment needs from chemicals to consumer electronics.[1]US-ASEAN Business Council, “Southeast Asia’s Digital Economy Generates Profits but Subdued Investment Levels,” usasean.org TIC firms respond by expanding regional footprints. QIMA signed an MoU with Korea Testing and Research Institute to deepen cross-border quality control, while SGS launched its SMART cloud platform to provide real-time supply-chain oversight. The forthcoming ASEAN Digital Economy Framework Agreement is expected to harmonize cross-border data rules and further lift demand for unified testing and certification services across member states.

ESG and sustainability audits accelerate across regional markets

Ninety-eight of the region’s 110 largest listed companies now publish sustainability disclosures, compared with fewer than half a decade earlier, reflecting tightened listing-rule requirements and rising investor scrutiny.[2]Institute for Energy Economics and Financial Analysis, “ESG Is Gaining Momentum With Regulators in Asia,” ieefa.org Australia’s AASB S2 climate rules mandate externally assured emissions statements from 2025, and Singapore will require limited assurance of Scope 1 and 2 data by fiscal year 2027. The global release of ISSA 5000 in late 2024 established a baseline for sustainability assurance, giving providers a consistent methodology to serve clients operating across multiple frameworks. Regional sustainable-bond issuance jumped 40% year-on-year in 2023, generating additional demand for pre- and post-issuance verifications and life-cycle carbon evaluations.

EV battery safety regulations drive harmonization and testing demand

China’s GB 38031 update, effective July 2026, compels batteries to withstand two hours of thermal-runaway fire without explosion, alongside new impact and charge-cycle tests. Malaysia’s MIROS issued three battery-electric safety codes that ASEAN members are already referencing, while Vietnam circulated draft lithium-battery rules that mirror United Nations transport guidelines. The EU Battery Regulation further raises the bar for Asia-Pacific exporters by imposing digital passports and recycled-content disclosure from 2027. Together, these measures push OEMs to engage accredited labs early in the design process to avoid certification bottlenecks.

Digital-health compliance creates real-time testing opportunities

The Medical Device Single Audit Program allows one audit to satisfy five major markets, but region-specific add-ons persist for example, Singapore’s Cybersecurity Labelling Scheme for connected medical devices and Malaysia’s reinstated conformity-assessment for COVID-19 test kits. Rapid rulemaking was evident when Thailand cleared Mpox test-kit registrations within weeks of the outbreak. Governments are upgrading lab capacity and accreditation programs, opening doors for private TIC firms to form public-private partnerships that expand compliant testing networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of advanced semiconductor labs | −0.8% | Taiwan, South Korea, Singapore | Medium term (2-4 years) |

| Fragmented national accreditation regimes | −0.6% | Emerging ASEAN economies | Long term (≥ 4 years) |

| Low TIC spend per capita | −0.4% | Vietnam, Cambodia, Laos | Medium term (2-4 years) |

| Cyber-security concerns on digital inspection | −0.3% | Region-wide critical infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advanced semiconductor testing capacity constraints limit growth

Asia hosts more than 80% of global assembly, test, and packaging capacity, yet shortages of skilled labor and EUV-ready test benches slow the expansion of next-generation fabrication lines. India alone needs an additional 250,000 engineers for its nascent foundry push, while Vietnam currently fulfils only one-fifth of the required semiconductor talent.[3]International Research Journal of Economics and Management Studies, “Human Resources in the Semiconductor Industry in Vietnam,” irjems.org Fan-out wafer-level packaging and 3D stack inspections demand expensive, high-precision gear that smaller labs struggle to finance, elongating certification lead times and raising costs for chipmakers.

Cyber-security vulnerabilities challenge digital inspection adoption

Forty-five percent of Asia-Pacific manufacturers cite cyber-security risks as the main hurdle when shifting to remote inspection, exceeding the global average of 39%. Capability gaps remain: 68% report insufficient OT security skills, and 56% lack budgets for comprehensive protection. Remote inspection platforms must therefore embed end-to-end encryption, tamper-proof evidence logs, and secure video streaming to gain regulator acceptance. Applus+ has begun layering blockchain verification onto its remote-inspection packages to address these concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Dominant Testing, Accelerating Certification

Testing held 57.90% of the Asia-Pacific TIC market share in 2025, as product safety, quality control, and regulatory compliance underpin every manufacturing supply chain. Heavy semiconductor exposure amplifies volumes because over 80% of global assembly and test work is carried out within the region, requiring high-frequency yield monitoring and failure-analysis routines. Asia-Pacific TIC market size attributed to testing is projected to grow steadily as fabs migrate to sub-5 nm nodes that raise complexity and require new fault-isolation protocols.

Certification is the fastest-advancing slice at a 5.62% CAGR through 2031, propelled by mandatory ESG assurance, voluntary carbon-credit verification, and new hydrogen-fuel quality marks. Leon Inspection’s overseas revenue climbed 21.3% in 2024 after it deployed AI-enabled spectral analysis and blockchain-backed data chains to speed CE-mark issuance for exporters. Providers investing in digital certificate vaults and auto-validation tools are positioned to capture share as governments pivot from self-declaration to third-party assurance.

By Sourcing Type: Outsourced Services Capture Strategic Spend

Outsourced providers controlled 63.10% of the Asia-Pacific TIC market size in 2025 and are forecast to expand at a 5.32% CAGR. Moving compliance tasks to specialists allows OEMs to focus resources on design and distribution while accessing deep domain expertise, multi-country accreditation, and scalable lab networks. SGS’s SMART platform integrates scheduling, document management, and analytics across thousands of factories, illustrating how outsourced partners enhance transparency to win new contracts.

In-house labs remain relevant in sectors where intellectual property is sensitive or continuous-process testing is embedded in the production line, such as pharmaceutical API analysis or petrochemical feedstock monitoring. Yet even these operators increasingly outsource niche tests such as recycled-content proof for EU battery exports when external labs can supply accredited results faster and at lower cost.

By Industry Vertical: Consumer Goods Lead, Food and Agriculture Surge

Consumer goods and retail claimed 22.60% of regional revenue in 2025, supported by long-established export compliance routines for toys, apparel, and homeware. SGS’s new furniture-testing center in Indonesia highlights continuing investment to serve this mature segment. Asia-Pacific TIC market size for consumer goods is set to grow alongside nearshoring trends that diversify manufacturing from coastal China to Indonesia and Vietnam.

Food, agriculture, and beverage sectors register the most rapid expansion at 6.05% CAGR as regulators tighten contaminant thresholds and traceability rules from farm to fork. Singapore’s Laboratory Recognition Programme now requires ISO/IEC 17025 accreditation before labs can carry out official food-safety tests, catalyzing private-lab upgrades and new market entrants. Exporters of seafood, fruit, and infant formula across ASEAN increasingly rely on accredited third parties for pesticide, heavy-metal, and microbial screens to satisfy European Union and United States import checks.

By Mode of Service Delivery: On-Site Persists, Remote Rises

On-site services retained a 52.05% share in 2025 because many infrastructure, energy, and heavy-equipment inspections still demand physical assessment of weld integrity, vibration levels, or hazardous-area compliance. Regulatory bodies often insist on witnessing destructive tests or reviewing calibration records in person. Asia-Pacific TIC market size for on-site inspection is forecast to grow modestly, given the continuing rollout of power-grid upgrades and rail projects.

Remote and digital inspections show the fastest momentum at 5.86% CAGR. Asia Quality Focus offers real-time video streams, standardized evidence collection, and immediate defect tagging that reduce travel time and carbon footprint while meeting buyer expectations for speed. Hybrid models are emerging, where initial document reviews and virtual walkthroughs precede targeted on-site sampling, optimizing resource allocation.

Geography Analysis

China led the Asia-Pacific TIC market with 40.25% revenue share in 2025, fueled by large-scale electronics, EV, and renewable-energy manufacturing. Domestic authorities actively standardize rules such as GB 38031 for batteries and fund metrology institutes, reinforcing demand for local conformity-assessment services. Leon Inspection reported HKD 1,263.1 million revenue in 2024, with almost 45% generated overseas, underscoring its rising global influence.

India ranks as the fastest-growing geography at a 6.22% CAGR through 2031. Government schemes, including the Performance-Linked Incentive for electronics and the Medical-Device Parks program, incentivize localized production and thereby multiply testing volumes. Nevertheless, a widening engineering talent gap and limited advanced-node semiconductor labs may cap near-term scaling until capacity catches up.

Japan, South Korea, and Australia contribute sizable revenue backed by technology leadership and proactive sustainability agendas. Japan’s Hydrogen Society Promotion Act introduces a detailed certification pipeline for low-carbon hydrogen and ammonia, demanding robust sampling, analytics, and chain-of-custody verification. Australia’s green-hydrogen pilots, often co-financed by Japanese investors, create cross-border opportunities for providers offering dual-jurisdiction accreditation.

ASEAN collectively registers steady growth as its digital economy targets USD 1 trillion gross merchandise value, translating into higher telecom-equipment type approvals, cybersecurity labelling, and e-commerce product-quality checks. Mutual-recognition initiatives under the Asia Pacific Accreditation Cooperation gradually smooth inter-country acceptance of reports, reducing redundant testing and encouraging providers to set up regional hubs.

Competitive Landscape

The Asia-Pacific TIC market is moderately concentrated. SGS, Bureau Veritas, and Intertek operate extensive lab networks and multivertical service portfolios, together accounting for 28% of regional revenue in 2024. The February 2025 termination of merger talks between SGS and Bureau Veritas keeps the competitive field open, prompting both to accelerate standalone digital initiatives.[4]Fuels & Lubes Asia, “SGS and Bureau Veritas End Merger Talks,” fuelsandlubes.com Intertek continues to expand ESG-assurance practices following heightened disclosure mandates.

Regional champions leverage local knowledge. China Leon Inspection integrates AI computer-vision systems into textile and footwear lines, shortening defect-detection cycles and differentiating on turnaround time. Japan’s JQA invests in hydrogen-quality analytics, while South Korea’s KTR builds 800V EV-battery test bays to align with upcoming UL and IEC standards. Technical depth and rapid accreditation across emerging categories, such as cyber-physical-system security certification, are becoming the primary differentiation levers.

White-space expansion is visible in advanced semiconductor reliability, recycled-content verification, and green-hydrogen passporting. EnerMech’s JV with TSI aims to combine mechanical-integrity engineering with core TIC services to supply large-scale LNG and hydrogen projects in Australia and Papua New Guinea. Partnerships that fuse engineering, software, and accreditation expertise are expected to proliferate as clients favor turnkey assurance covering complete asset life cycles.

Asia-Pacific Testing, Inspection And Certification (TIC) Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SMX Plc partnered with Aegis Packaging and Skypac Packaging to embed blockchain traceability markers in flexible packaging.

- April 2025: SGS experts spoke at Global Sources Summit 2025 on green electronics, pet products, and functional sportswear trends.

- March 2025: SGS Hong Kong became an accredited validation and verification body under the Asia Carbon Institute’s carbon-credit scheme.

- March 2025: SGS Hong Kong secured Singapore Civil Defence Force accreditation to certify fire-safety products, easing regional market entry.

- March 2025: SGS inaugurated a furniture and transit-packaging test center in Semarang, Indonesia, aligned with ISTA protocols.

- February 2025: ISO released ISO 14687:2025, broadening hydrogen-fuel quality grades and adding cybersecurity criteria for fueling infrastructure.

- February 2025: SGS and Bureau Veritas ended merger talks without agreement, maintaining independent strategies.

- January 2025: EnerMech and TSI formed a joint venture targeting integrated TIC and engineering services across Asia-Pacific.

- January 2025: China Leon Inspection posted HKD 1,263.1 million in 2024 revenue, with overseas sales up 21.3% on AI-driven service expansion.

Asia-Pacific Testing, Inspection And Certification (TIC) Market Report Scope

The testing, inspection, and certification industry consist of conformity assessment bodies that offer services ranging from auditing and inspection to testing, verification, quality assurance, and certification.

The study tracks the revenue accrued from the various types of TIC services that are provided across end-user industries in the Asia-Pacific by service providers. In addition, the study provides the TIC market trends, along with key vendor profiles. The study further analyzes the overall impact of COVID-19 on the ecosystem.

The Asia-Pacific testing, inspection, and certification (TIC) market study provides a comprehensive analysis of the market segmented by type (in-house and outsourced), by service type (testing and inspection, and certification), by end-user (industrial manufacturing, automotive and transportation, oil and gas, mining and downstream applications, food and agriculture, building and infrastructure, consumer goods and retail, and other end users), and by country (China, India, Japan, South Korea, Southeast Asia, and Rest of Asia-Pacific). The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

By Service Type

| Testing |

| Inspection |

| Certification |

By Sourcing Type

| In-house |

| Outsourced |

By Industry Vertical

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Other Industry Verticals (Environment, Sustainability, etc.) |

By Mode of Service Delivery

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

By Country

| China |

| Japan |

| India |

| South Korea |

| ASEAN |

| Rest of Asia-Pacific |

| By Service Type | Testing |

| Inspection | |

| Certification | |

| By Sourcing Type | In-house |

| Outsourced | |

| By Industry Vertical | Consumer Goods and Retail |

| ICT and Telecom | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Oil, Gas and Petrochemicals | |

| Energy and Utilities | |

| Industrial Manufacturing and Machinery | |

| Chemicals and Materials | |

| Construction and Infrastructure | |

| Life Sciences and Healthcare | |

| Food, Agriculture and Beverage | |

| Other Industry Verticals (Environment, Sustainability, etc.) | |

| By Mode of Service Delivery | On-site |

| Off-site / Laboratory | |

| Remote / Digital | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific TIC market in 2026?

Asia-Pacific TIC market size is valued at USD 131.13 billion in 2026.

What is the projected CAGR through 2031?

The market is forecast to grow at a 5.03% CAGR between 2026 and 2031.

Which country is the fastest-growing TIC customer?

India shows the quickest pace, expanding at a 6.22% CAGR through 2031.

Which service category is growing the fastest?

Certification services lead growth, tracking a 5.62% CAGR during the forecast period.

What trend is accelerating remote inspections?

Post-pandemic digital-audit adoption and newer cyber-secure video platforms are lifting remote inspections at a 5.86% CAGR.

Which vertical presents the greatest upside beyond 2026?

Food, agriculture, and beverage sees the strongest outlook at a 6.05% CAGR as regulators tighten safety and traceability rules.

Page last updated on: