Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

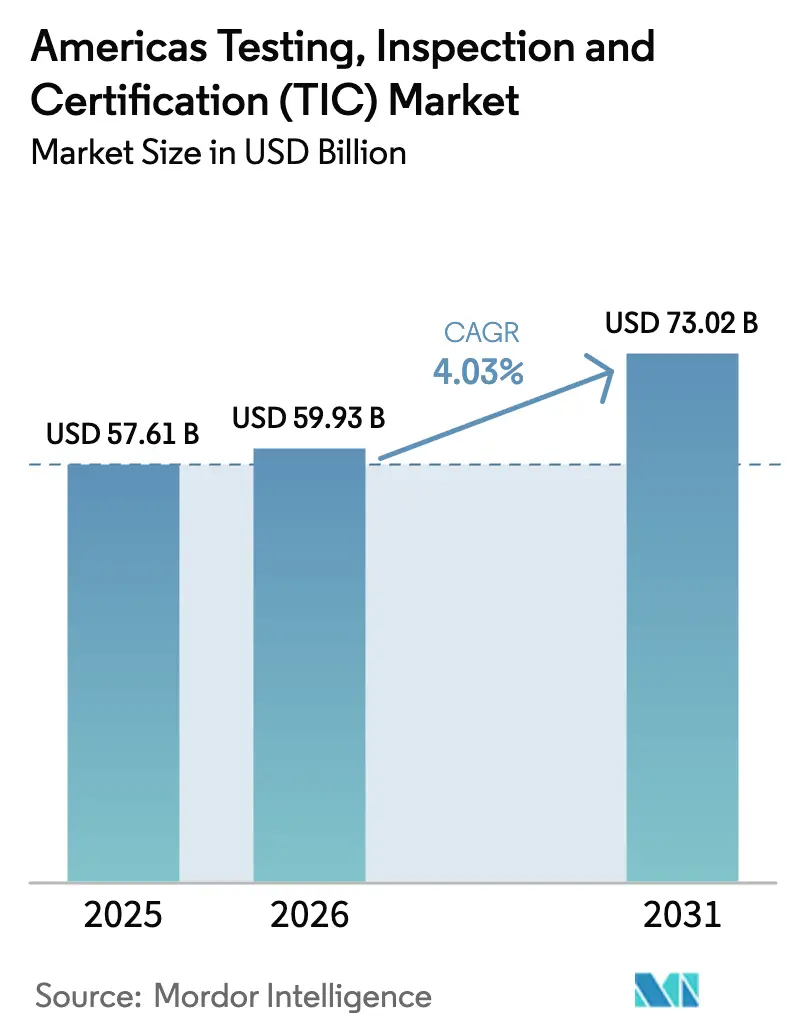

| Base Year Market Size (2025) | USD 57.61 Billion |

| Market Size (2026) | USD 59.93 Billion |

| Market Size (2031) | USD 73.02 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Testing, Inspection And Certification (TIC) Market Analysis by Mordor Intelligence

The Americas TIC market size is expected to grow from USD 57.61 billion in 2025 to USD 59.93 billion in 2026 and is forecast to reach USD 73.02 billion by 2031 at 4.03% CAGR over 2026-2031. The near-shoring wave that pulls production from Asia to the Americas fuels steady demand for local compliance testing, while stricter ESG disclosure rules issued by the U.S. SEC and the Canadian CSA elevate verification volumes. North America retains clear primacy because its mature regulatory environment, deep manufacturing base, and robust capital expenditure on advanced testing infrastructure sustain high ticket engagements. South America is recording the quickest growth as governments modernize industrial policy and multinational firms invest in fresh capacity, especially in Brazil and Mexico. Across every geography, the convergence of AI-enabled inspection, digital reporting platforms, and reciprocal certification agreements between aviation regulators compresses project timelines and lifts the overall value proposition of third-party providers.

Key Report Takeaways

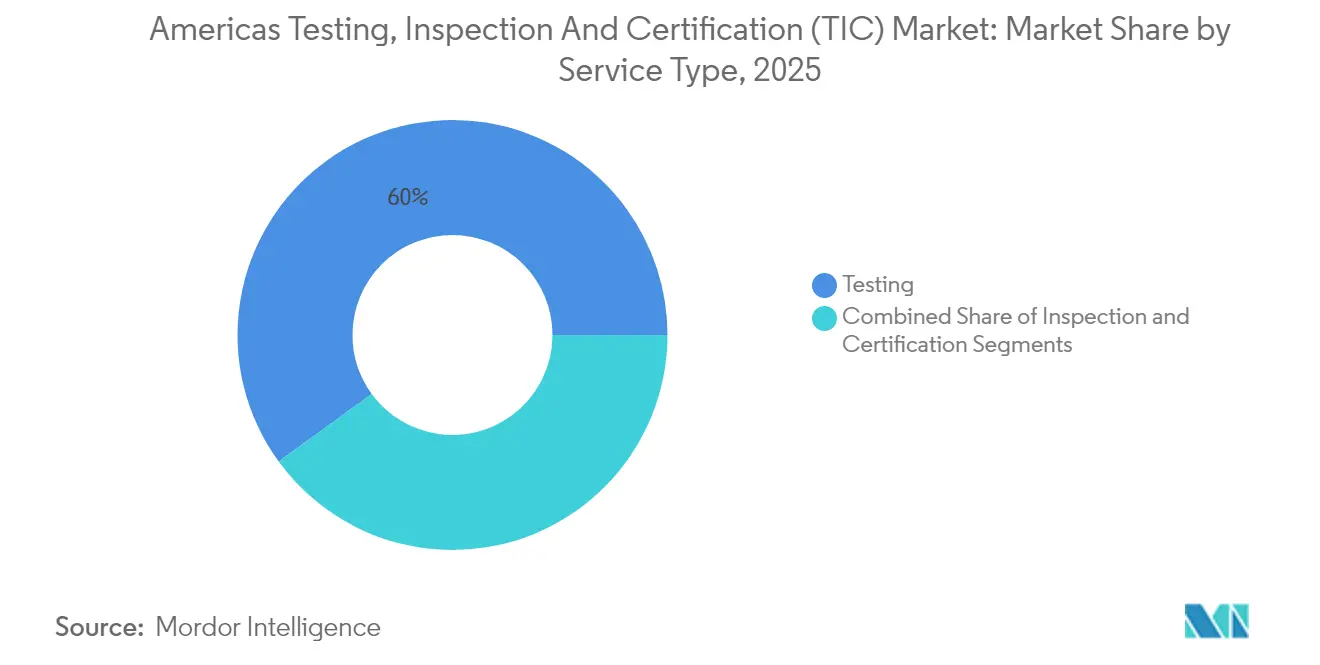

- By service type, testing services held 60.02% of the Americas TIC market share in 2025, while certification services are expanding at a 4.74% CAGR through 2031.

- By sourcing model, the outsourced segment controlled 68.72% of the Americas TIC market size in 2025 and is projected to grow at a 4.55% CAGR to 2031.

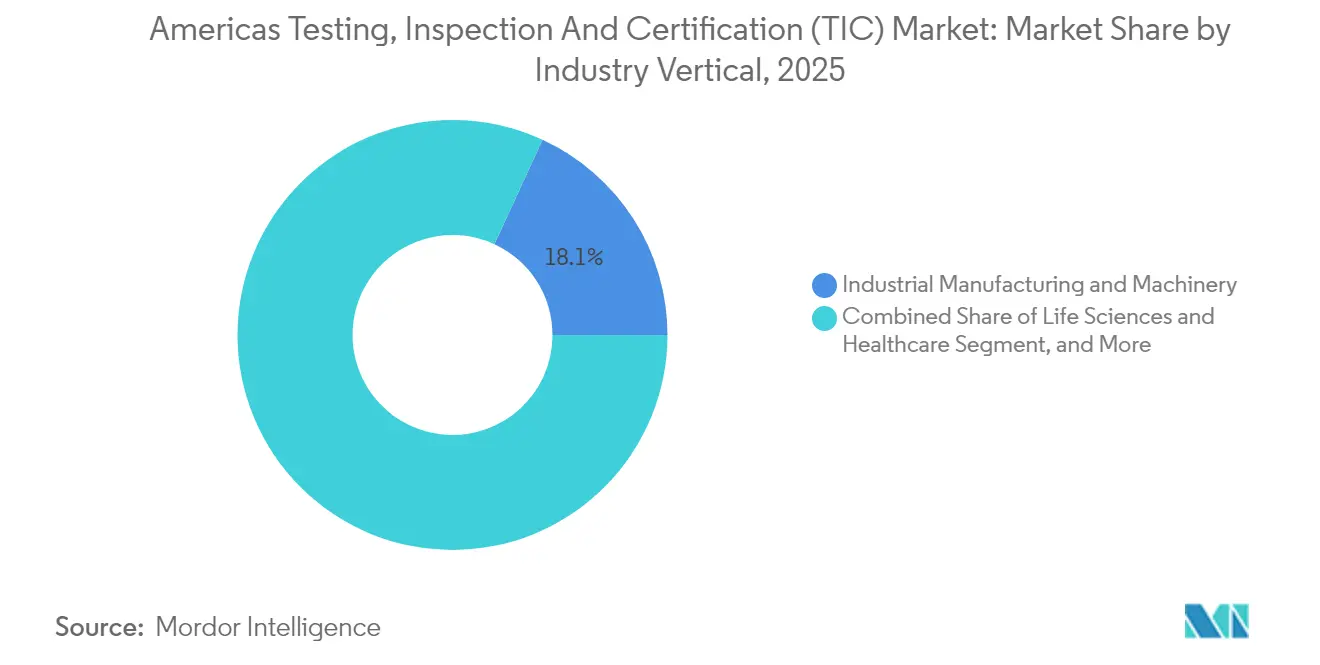

- By industry vertical, life sciences and healthcare are forecast to post the fastest 5.18% CAGR to 2031, whereas industrial manufacturing and machinery retained the largest revenue share at 18.12% in 2025 of the Americas TIC market.

- By mode of service delivery, on-site service delivery captured 47.96% revenue in 2025 of the Americas TIC market, but remote and digital inspection solutions are projected to advance at a 4.93% CAGR through 2031.

- By region, South America is set to register a 5.29% CAGR between 2026 and 2031, outpacing all other sub-regions of the Americas TIC market, whereas North America retained the largest revenue share at 64.62% in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Americas Testing, Inspection And Certification (TIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising near-shoring drives demand for local compliance testing | +0.8% | North America and Mexico, spillover to Central America | Medium term (2-4 years) |

| Stricter ESG auditing mandates by U.S. SEC and Canadian CSA | +0.6% | North America, extending to South American subsidiaries | Short term (≤ 2 years) |

| Accelerated 5G / 6G roll-outs require new radio-equipment certification | +0.5% | Global, with early deployment in major metropolitan areas | Medium term (2-4 years) |

| Surging Li-ion battery gigafactories in Mexico and Brazil | +0.4% | Mexico, Brazil, with supply-chain effects across Americas | Long term (≥ 4 years) |

| Digital traceability legislation in food supply chains | +0.3% | United States, Canada, with harmonization pressure on LATAM | Short term (≤ 2 years) |

| Insurance underwriters tightening loss-control inspection clauses | +0.2% | North America, selective adoption in South American markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-shoring compliance testing surge reshapes market dynamics

Local production shifts accelerated after pandemic-era supply chain disruptions, prompting new factories in Mexico’s border states to commission extensive safety, environmental, and quality audits before products may enter the United States. Companies report that 70% of open technical roles remain unfilled, which obliges heavier reliance on outsourced providers to satisfy ISO 17025 and sector-specific standards.[1]Bloomberg, “Mexico's Tech Worker Shortage Hampers Nearshoring Push,” bloomberg.com Spillover benefits reach logistics firms that require verification of warehouse automation systems, as well as financial service centers tasked with regional compliance oversight. The Americas TIC market enlarges as near-shoring also extends to consumer electronics, automotive drivetrains, and precision machinery that demand complex multi-discipline testing.

ESG auditing mandates create new revenue streams

The U.S. SEC rule, effective for 2025 large accelerated filers, obliges third-party assurance of Scope 1 and Scope 2 emissions, while the Canadian CSA implements parallel disclosure guidelines. The extraterritorial reach means subsidiaries across Latin America must submit verified carbon inventories, leading to cross-border engagements for established TIC firms. Insurers add weight by requesting ESG compliance certificates before underwriting property and casualty coverage. In response, providers launch carbon accounting, supply-chain transparency, and social-impact audit services, stimulating premium-rate contracts that lift overall Americas TIC market growth.

5G / 6G equipment certification drives technical innovation

Rapid 5G rollout across urban corridors compels handset makers, network equipment vendors, and private-network operators to meet new FCC and ISED protocols that cover millimeter-wave bands and massive MIMO antenna arrays.[2]Federal Communications Commission, “Equipment Authorization – RF Device,” fcc.gov Capital-heavy RF chambers priced around USD 10–15 million per site set a high entry barrier, thus reinforcing the competitive edge of incumbents. Preparations for 6G prototypes due after 2028 spawn advance bookings for reliability and coexistence testing. Mutual recognition agreements cut duplicate testing burdens, yet national spectrum allocations still diverge, ensuring steady advisory revenue.

Li-ion battery gigafactory expansion fuels specialized testing

BMW’s USD 1.7 billion plant in Mexico represents a broader battery manufacturing wave that also touches Brazil, where government incentives catalyze new capacity. Comprehensive protocols such as UL 2580 demand abuse, thermal runaway, and cycle-life analysis, activities that rely on purpose-built chambers and chem-analysis labs unavailable to most in-house teams. Suppliers of cathode, anode, and electrolyte materials enter the compliance queue, multiplying addressable spend for service providers with electrochemical expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of qualified lab technicians across LATAM | -0.4% | Latin America, spillover effects to North American operations | Long term (≥ 4 years) |

| Fragmented regulatory regimes between Mercosur and USMCA | -0.3% | Cross-border operations between North and South America | Medium term (2-4 years) |

| High capex for AI-driven remote inspection hardware | -0.2% | Global, with slower adoption in cost-sensitive LATAM markets | Short term (≤ 2 years) |

| Rising in-house testing capabilities by mega OEMs | -0.2% | North America primarily, selective adoption by large South American manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technician shortage constrains market expansion

UNESCO warns that regional technical education shortfalls leave 70% of Mexican technology firms scrambling to source qualified workers.[3]UNESCO, “Latin America Faces Technical Education Crisis,” unesco.org Specialized domains such as RF characterization, chemical analytics, and advanced materials see persistent vacancy rates, forcing providers to build intensive training pipelines that extend payback periods. Wage inflation for scarce skill sets compresses margins, especially for commoditized assays. Cross-border relocation of senior experts mitigates bottlenecks but adds visa and relocation costs.

Regulatory fragmentation increases compliance costs

Despite reciprocal aviation agreements, notable divergences linger between USMCA and Mercosur frameworks for food safety, automotive components, and telecommunication devices. Multinationals navigating both blocs must often repeat entire test batteries, prolonging time-to-market and inflating budgets. Large TIC firms leverage multi-jurisdiction labs to centralize program management, whereas smaller specialists face barriers to continental expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing retains lead while certification accelerates

Testing solutions delivered 60.02% of 2025 revenue, underlining their foundational role in product validation across every vertical. Certification, though smaller, is set to grow at a 4.74% CAGR because ESG audits, cybersecurity seals, and functional-safety endorsements carry increasing regulatory weight. Inspection services occupy the median niche, sustaining infrastructure integrity projects and preventive maintenance programs. Battery safety initiatives illustrate how demand migrates toward high-complexity assays where expert judgment and purpose-built chambers matter. The Americas TIC market size for certification services is projected to widen in tandem with mandates that require audited disclosures.

Competitive positioning shifts as labs pursue ISO 17025 baseline accreditation before layering sector-specific endorsements such as UL 2580 or IATF 16949. UL Solutions expanded its electric-vehicle battery test line to capture premium assignments, signaling a pivot toward high-value niches. Smaller firms without capital latitude gravitate to subcontract models under network partners, reinforcing the outsourced ecosystem. Automation and data analytics permeate routine tests, freeing skilled personnel to focus on interpretive tasks, yet staff shortages in advanced disciplines temper volume scalability.

By Sourcing Type: Outsourced dominance persists

Corporations continued to channel 68.72% of verification budgets to external partners in 2025, a pattern projected to hold with a 4.55% CAGR through 2031. Risk mitigation, regulator preference for independent sign-off, and ever-broadening standard catalogs underpin the outsourced share. The Americas TIC market share for outsourced activities benefits from cross-border manufacturing that complicates single-entity compliance.

Digital transformation amplifies this appeal. Providers embed real-time dashboards, seamless data feeds, and audit-ready report generators, reducing internal administrative loads. Mega-OEMs that have built captive labs still require impartial attestations before product launch. Consequently, the outsourced model remains integral, while hybrid arrangements surface in which corporate labs run pre-screens and external partners supply conformance certificates.

By Industry Vertical: Manufacturing leads, healthcare outpaces

Industrial manufacturing and machinery accounted for an 18.12% slice of 2025 turnover as capital goods producers validated equipment for regional plants. The Americas TIC market size for life sciences and healthcare is poised to climb fastest at 5.18% CAGR because post-pandemic regulatory scrutiny reinforces sterility, efficacy, and supply-chain integrity norms.

Consumer goods and retail maintain baseline volume through safety and labeling checks, while ICT and telecom ride the 5G/6G deployment cycle. Automotive ventures into electrification and autonomy necessitate fresh test suites for batteries and perception systems. Oil, gas, and petrochemical operators adhere to pipeline integrity standards under PHMSA jurisdiction. Renewable energy uptake expands demand for blade inspection, inverter certification, and grid compliance. Aerospace firms leverage reciprocal certification pacts to expedite cross-border approvals, and construction material labs benefit from rising infrastructure spend across Brazil, Mexico, and Chile.

By Mode of Service Delivery: Digital uptake accelerates

On-site engagements maintained 47.96% revenue in 2025 as heavy equipment and infrastructure still require physical examination. Remote and digital methodologies posted a 4.93% CAGR, leveraging AI vision, drones, and IoT sensors to perform continuous or periodic checks without travel. Off-site laboratories remain essential for activities such as destructive testing, chemical analytics, and climatic stress cycles.

Pandemic-era constraints triggered rapid remote adoption; the model persists because clients appreciate cost, speed, and carbon footprint savings. Yet regulatory acceptance varies, prompting blended models where remote sensing delivers raw data and periodic field visits serve as quality anchors. Providers invest in interoperability layers that integrate sensor outputs into secure cloud dashboards detailed enough for auditors.

Geography Analysis

North America’s outsized 64.62% share derives from comprehensive legislation that spans health, environment, and technology. The Americas TIC market share split favors the United States because its multi-agency oversight places mandatory tests on pharmaceuticals, electronics, and agriculture. Canada amplifies activity through mining core assays and oil sands environmental audits, while Mexico’s border expansion funnels automotive driveline and consumer electronics checks into nearby accredited labs. USMCA has aligned many technical requirements, yet implementation lags in niche domains, sustaining advisory opportunities.

South America posts the sharpest growth, forecast at 5.29% CAGR to 2031, as Brazil injects capital into transport corridors and power grids. Federal programs require certified concrete, steel, and composite materials, widening the Americas TIC market size devoted to civil engineering verification. Argentina leverages lithium and copper resource expansion, prompting specialized spectroscopy and metallurgical services. Chile’s renewables boom requires IEC-compatible turbine and solar panel validation, while Peru and Colombia demand pipeline inspections aligned with U.S. integrity protocols.

Cross-border manufacturers encounter dual testing when USMCA and Mercosur rules diverge in food additives limits, vehicle emissions, and cellular handset SAR thresholds. Larger TIC players capitalize on regional lab footprints that streamline sample logistics and coordinate multi-standard test plans. Emerging mutual recognition talks promise long-range efficiency gains yet are unlikely to erase all local certification layers within the forecast window.

Competitive Landscape

The Americas TIC market remains moderately fragmented, though M&A accelerates as providers pursue scale and niche expertise. The abandoned USD 30–35 billion SGS-Bureau Veritas merger in January 2025 shows antitrust sensitivity at mega-deal levels. Instead, acquisitive activity pivots toward bolt-ons: Bureau Veritas paid CAD 650 million (USD 481 million) for Maxxam Analytics to bolster Canadian environmental coverage, while SGS integrated Accutest Laboratories to deepen U.S. soil and water portfolios.

Strategic themes concentrate on electrification, ESG audits, and digital inspection. Intertek’s USD 15 million Electrification Centre of Excellence near Detroit exemplifies capital deployment toward high-growth verticals. TÜV Rheinland’s Mexico cybersecurity lab positions the company for rising automotive connectivity demands. Mérieux NutriSciences purchased Bureau Veritas’ food unit for EUR 350 million (USD 378 million) to craft a continental network that targets farm-to-fork traceability validations. Providers that command comprehensive accreditations across multiple domains and regions gain pricing power, whereas commodity assays experience competitive rate squeezing.

Digital capabilities serve as new differentiators. Firms deploy AI for anomaly detection, predictive analytics, and virtual witness solutions. Early adopters secure multi-year master service agreements that bundle traditional checks with data services. Smaller specialists preserve relevance by focusing on single-discipline expertise and servicing subcontract flow from prime contractors.

Americas Testing, Inspection And Certification (TIC) Industry Leaders

Bureau Veritas SA

SGS SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Bureau Veritas and SGS terminated merger discussions valued at USD 30–35 billion after failing to align on terms and regulatory clearance.

- December 2024: Bureau Veritas completed the acquisition of Maxxam Analytics for CAD 650 million (USD 481 million), expanding environmental testing capacity within Canada.

- November 2024: SGS acquired Accutest Laboratories to broaden its North American environmental testing reach.

- October 2024: Mérieux NutriSciences purchased Bureau Veritas’ food testing business for EUR 350 million (USD 378 million).

Americas Testing, Inspection And Certification (TIC) Market Report Scope

The testing, inspection, and certification industry consists of conformity assessment bodies that offer services ranging from auditing and inspection to testing, verification, quality assurance, and certification.

The Americas testing, inspection, and certification market is segmented by service type (testing and inspection service, certification service), end-user industry (consumer products & retail, energy & power, automotive, oil & gas, mining, agriculture/food, chemical, building infrastructure/construction, industrial equipment [heavy equipment and machinery], transportation [aerospace and rail], and other end-user industries) and country (United States, Canada, Brazil, Mexico, Chile, Argentina, and the Rest of Americas). The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Testing |

| Inspection |

| Certification |

By Sourcing Type

| In-house |

| Outsourced |

By Industry Vertical

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Other Industry Verticals (Environment, Sustainability, etc.) |

By Mode of Service Delivery

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

By Region

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

| By Service Type | Testing | |

| Inspection | ||

| Certification | ||

| By Sourcing Type | In-house | |

| Outsourced | ||

| By Industry Vertical | Consumer Goods and Retail | |

| ICT and Telecom | ||

| Automotive and Transportation | ||

| Aerospace and Defense | ||

| Oil, Gas and Petrochemicals | ||

| Energy and Utilities | ||

| Industrial Manufacturing and Machinery | ||

| Chemicals and Materials | ||

| Construction and Infrastructure | ||

| Life Sciences and Healthcare | ||

| Food, Agriculture and Beverage | ||

| Other Industry Verticals (Environment, Sustainability, etc.) | ||

| By Mode of Service Delivery | On-site | |

| Off-site / Laboratory | ||

| Remote / Digital | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Americas TIC market in 2026?

It is valued at USD 59.93 billion and is projected to reach USD 73.02 billion by 2031 at a 4.03% CAGR.

Which region is expanding fastest within testing and inspection services?

South America is forecast to grow at 5.29% CAGR through 2031, driven by industrial development and regulatory modernization.

Why are ESG mandates boosting TIC demand?

The U.S. SEC and Canadian CSA require third-party assurance of emissions data starting in 2025, pushing companies to contract certified auditors.

What service type leads the Americas TIC market?

Testing services hold 60.02% revenue share, reflecting their foundational role in product and process validation.

How is digital inspection changing the landscape?

AI-enabled remote solutions are growing at 4.93% CAGR, reducing field costs and enabling continuous monitoring while still requiring periodic on-site validation.

Which industry shows the fastest projected growth?

Life sciences and healthcare is expected to grow at 5.18% CAGR because post-pandemic regulations demand rigorous compliance checks.

Page last updated on: